Vertigo3d

Vertigo3d

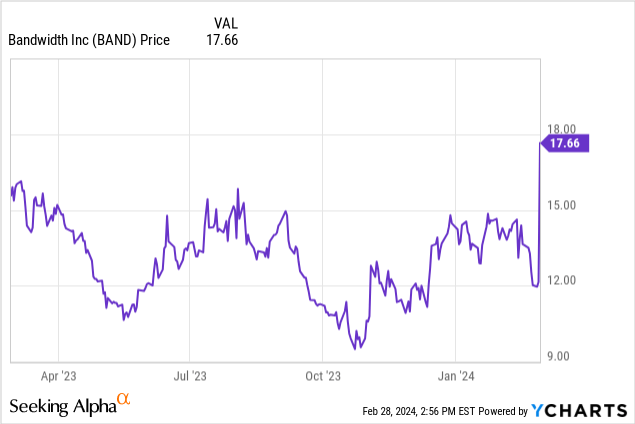

In a complete illustration of how volatile small-cap tech stocks can be, CPaaS software vendor Bandwidth (NASDAQ:BAND) shot up more than 50% after reporting Q4 results - and more importantly, issuing robust guidance for FY24 and beyond. The optimistic angle of Bandwidth’s press release was a complete change in tone versus its much better-known competitor Twilio (TWLO), which has seen its once-formidable growth rates decline to the mid single-digits, while also dealing with leadership turnover and operational issues in one of its major segments.

Still - Bandwidth’s post-earnings jump is barely enough to offset recent losses. Over the past twelve months, the stock is still up only 15% - while the S&P 500 and most other tech stocks have seen much more aggressive gains.

I last wrote a bearish report on Bandwidth in November, when the stock was trading in the low teens. Bandwidth’s turnaround was unseen, and in light of the most recent updates the company has shared, I’m upgrading the stock to neutral.

There are a number of (relatively balanced) pluses and minuses here that investors should be aware of. On the positive side for this company:

On the flip side, however, we should be mindful of the fact that:

All in all, if Bandwidth can truly execute to its new expectations this year, the company may turn sentiment around: especially if it gains a leg up on Twilio while the latter is struggling with severe growth churn issues. At the same time, however, it’s very prudent to remain cautious as the company has yet to show any reported acceleration yet.

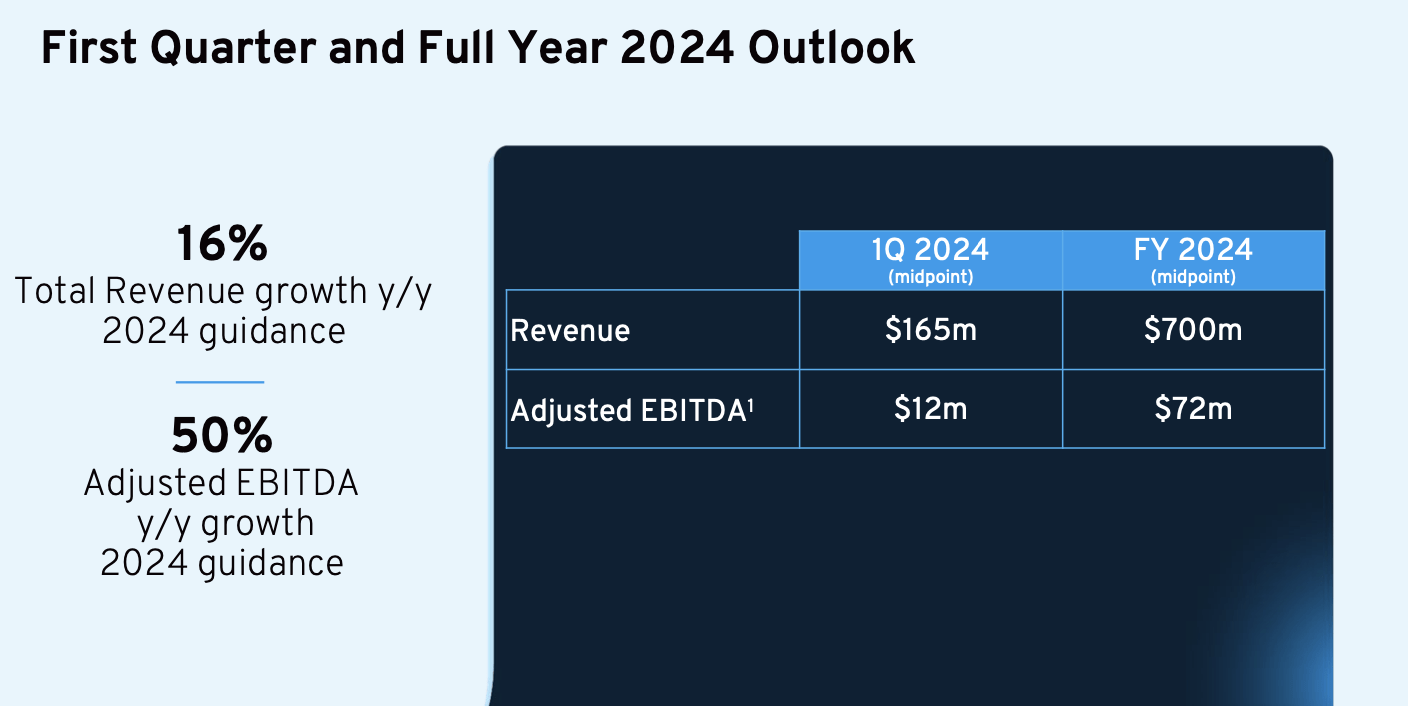

Since pandemic-era tailwinds came to a halt, Bandwidth's forward guidance has been littered with caution. Not so in the company's 2024 outlook, which has growth accelerating back to 16% y/y (from only 5% y/y exiting Q4):

Bandwidth outlook (Bandwidth Q4 earnings deck)

And if Q1 guidance is to be taken at face value, then Bandwidth is indicating that its growth trajectory will accelerate to 20% y/y growth as soon as in Q1.

Product innovation and rollouts are partially driving the improved performance. The company has introduced 10 new enterprise-oriented products, including a new one called Bandwidth Maestro. This AI-powered tool helps businesses to design call flows that route incoming traffic and help to decrease total agent interactions.

Another expected uplift to 2024 is the upcoming election cycle - which always invites more campaign-related messaging.

Here is helpful anecdotal commentary from CEO David Morken’s remarks on the Q4 earnings call:

In our enterprise category, we launched 10 new products, including Bandwidth Maestro, our AI ready next gen software platform, which was judged by our peers to be such a game changer that it won best of show at Enterprise Connect. In fact, industry recognition for Maestro continues as it won a product of the year award from internet Lefty just last week. These new offerings, each substantial in their own right, drove our opportunity pipeline to new highs, accelerated our enterprise revenue growth 21% year-over-year and led to new customer wins like Ally Financial, Western Union, Children's Health, Fabletics and so many others. All chose Bandwidth to improve their customer experiences and to adopt conversational AI […]

In 2024, we expect our growth in commercial messaging to be joined by further benefit from the U.S. election season, where our capabilities uniquely serve many longstanding customers. Each one of these examples demonstrates the growth and rapid innovative capabilities of the Bandwidth communications cloud. As we reflect on the past year, we are pleased with our execution and forward momentum through any crosswinds in the current macro environment.”

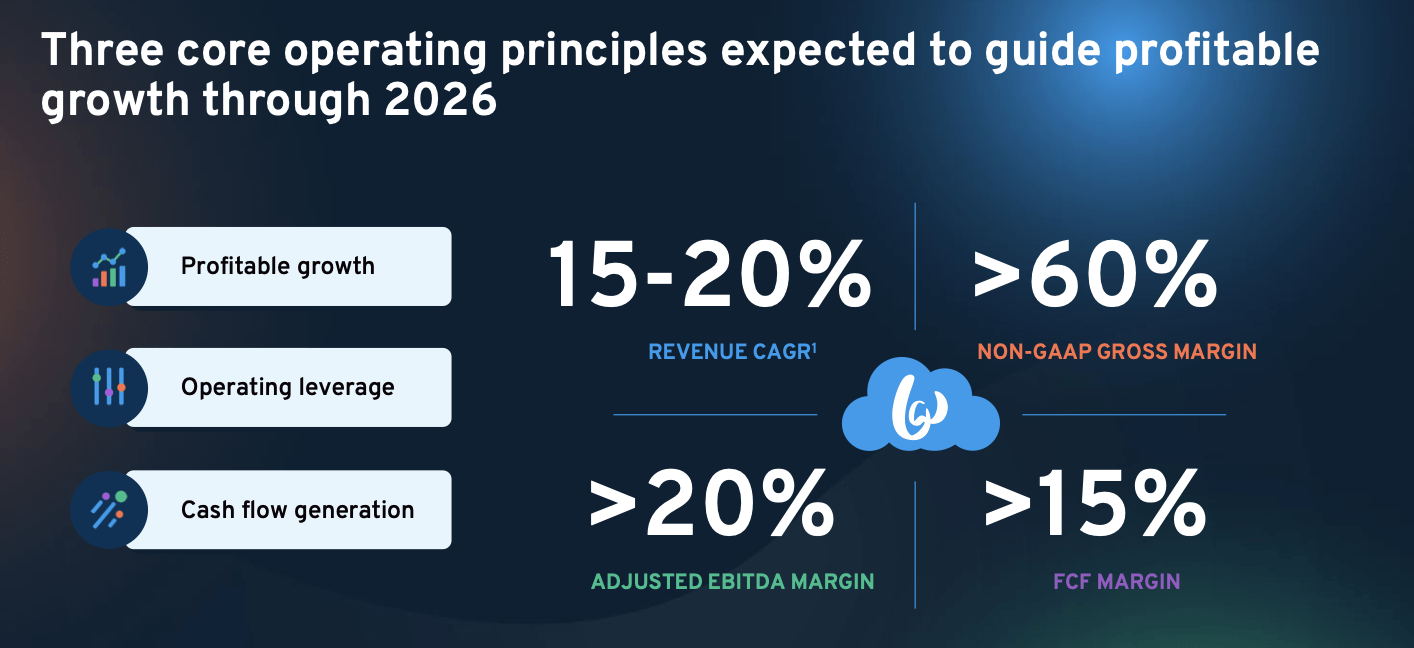

It’s worth noting as well that it’s not just that 2024 will benefit from campaign-related traffic and growth thereafter will suffer: through 2026, the company has issued a long-term outlook that calls for a revenue growth CAGR of 15-20% y/y.

Bandwidth long-term growth principles (Bandwidth Q4 earnings deck)

It’s also expecting continued improvement in bottom-line margins, with adjusted EBITDA margins expected to enrich to 20% by FY26 - up from 10% in FY23.

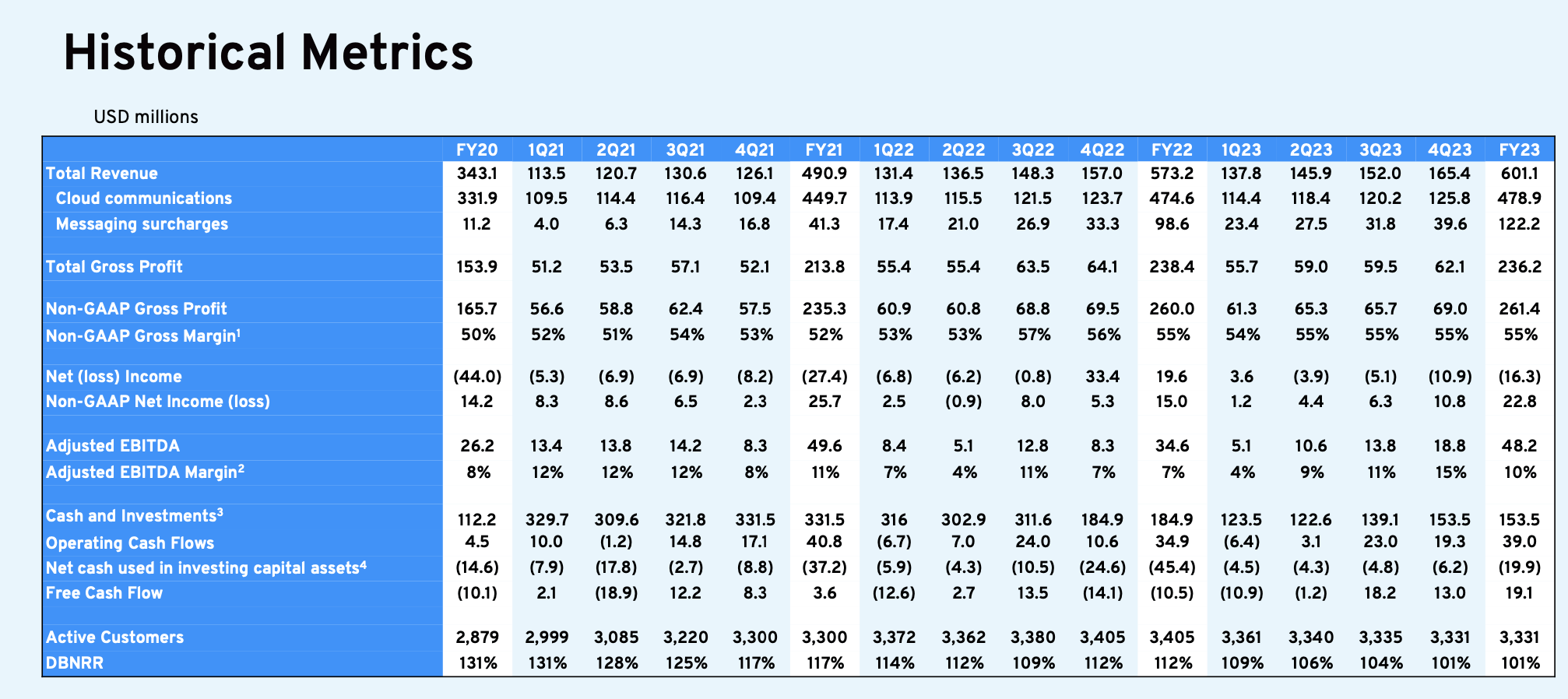

This all being said, an outlook is one thing and execution is another: and as of its most recent quarter, Bandwidth was still growing at only a 5% y/y pace.

Bandwidth trended metrics (Bandwidth Q4 earnings deck)

As previously mentioned, and as shown on the chart above, Bandwidth's dollar-based net retention rates have been in decline. Rates slipped to 101% in Q4, down three points sequentially versus 104% in Q3. Now, Bandwidth noted that it has specific headwinds from lapping FY22's mid-year election campaign traffic - but we'll need to see signs of improvement in order to support Bandwidth's revenue growth targets for the year.

The other risk worth calling out: Bandwidth continues to lose customers. The company lost 4 net customers in Q4, down to a total of 3,331 (down by more than 70 customers year-over-year). In its defense, Bandwidth is focusing its sales efforts upstream toward enterprise customers while letting smaller customers adopt a self-service model.

Bandwidth's outlook for re-accelerating revenue growth and significant improvements in adjusted EBITDA margins are certainly quite encouraging after a long dry streak for this company. Still, Bandwidth's ability to execute has been questionable based on recent trends, and with the 50%+ jump in Bandwidth's stock post-earnings, I'd say quite a bit of enthusiasm is already baked into Bandwidth's prospects in 2024. Maintain caution here.