izusek

izusek

Dear readers,

In early November, I published a controversial piece on Brookfield Asset Management (NYSE:BAM). I had been bullish on BAM and the stock represented one of my biggest positions, but when I learned that (1) distributions from Brookfield's daughter funds (Brookfield Infrastructure Partners - BIP and Brookfield Renewable Partners - BEP) may not be covered by cash FFO and especially that (2) the management fees received from BIP and BEP are effectively tied to the market cap of those funds, I flipped bearish and issued a SELL rating at $30 per share.

Seeking Alpha

The reason was that BIP's and BEP's prices had plummeted and it was therefore very clear that Q3 management fees from those funds would be lower than in previous quarters. I estimated that lower management fees from BIP and BEP would cause about a 5% drag on fee-related earnings (FRE) and would cause Brookfield to fall short of its 15%+ earnings growth target. I expected that to be a big deal, because BAM was trading at a premium valuation of 25x FRE which, many argued, was primarily caused by high double-digit expected growth. With growth expectation down by 5%, I worried that BAM may re-rate to a lower multiple.

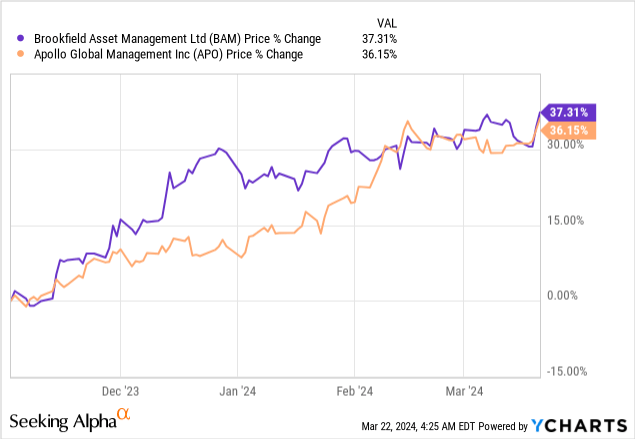

I sold most of my position and allocated the proceeds to my favorite alternative asset manager - Apollo Global Management (APO), which I saw as better positioned due to their high private credit and insurance exposure and due to a much lower valuation (learn more about APO here). Admittedly, BAM has rallied since early November, but so has Apollo. And in fact, their performance has been fairly similar with RoR of 36-37%.

BAM reported their Q4 2023 results recently and, in many ways, they revealed what I warned against. BIP and BEP performance has been terrible and overall FRE growth has slowed to 6% YoY. Regardless, the stock has only gone up and now trades at an even more stretched valuation of 31x FRE.

BAM has targeted 15-20% earnings growth for a while now and historically they have done a great job of delivering on that promise. As a result, nobody questioned BAM's somewhat high earnings multiple of 25x and a sub-4% dividend yield.

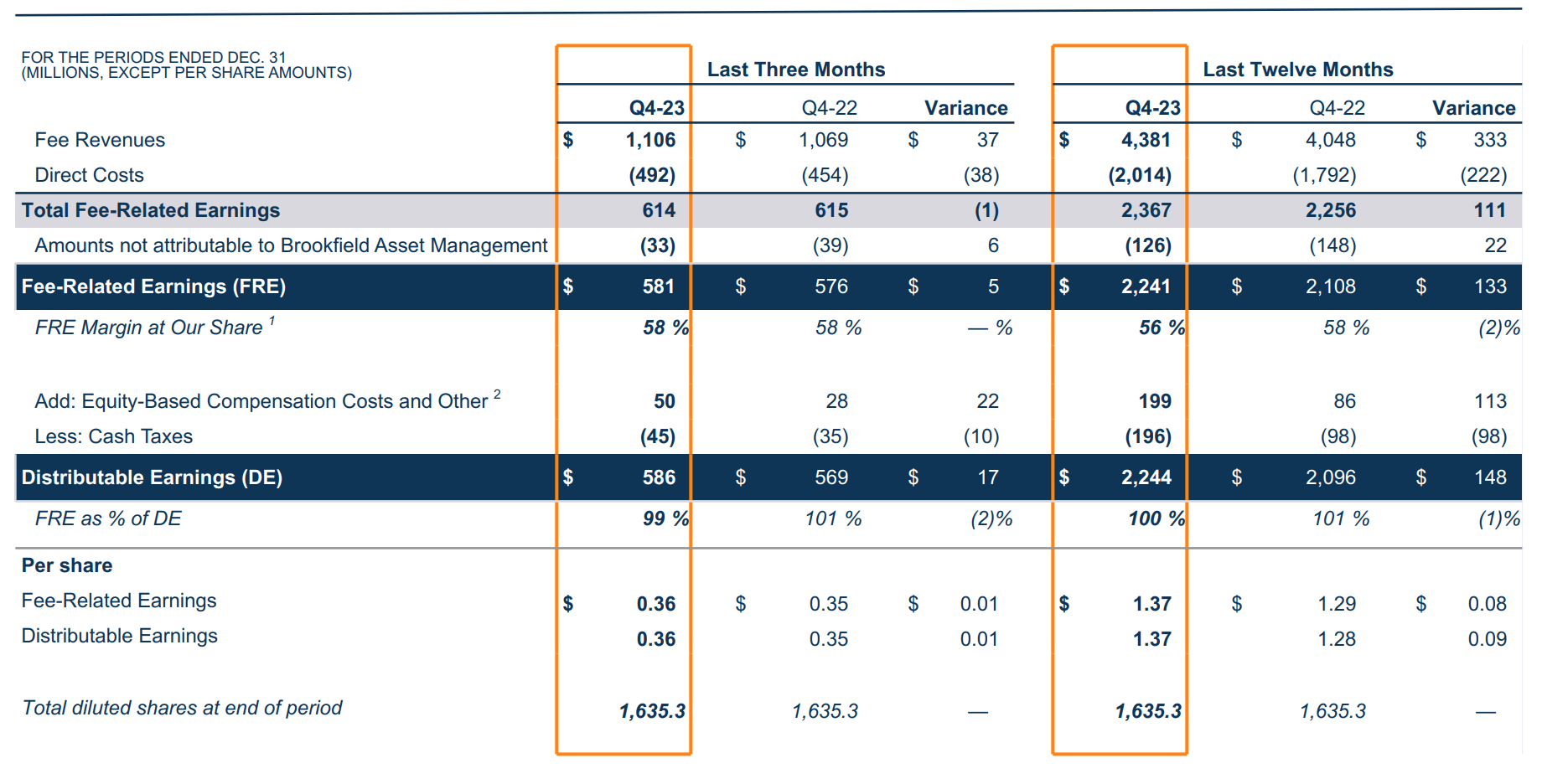

In 2023, however, fee revenue growth decelerated to 8.2% and the FRE margin declined from 58% to 56%. As a result, fee-related earnings only increased by $133 Million YoY (up only 6.3% YoY). That's less than half the bottom-end of the target and something that I would consider a major miss.

BAM IR

Sluggish performance was, as expected, largely caused by low management fees from Brookfield's daughter funds.

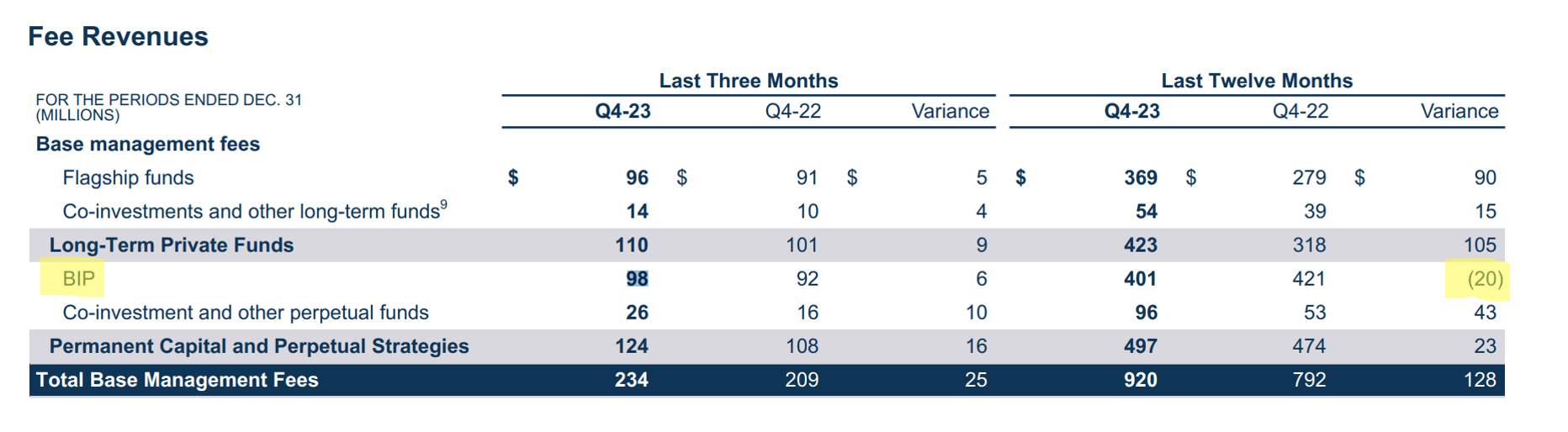

First, let's have a look at BIP.

In my last article I expected Q3 management fees to decline by about 5% (see the math below). And since the price of BIP hasn't recovered by much since then, the implication for Q4 was similar.

Seeking Alpha - my previous article on BAM

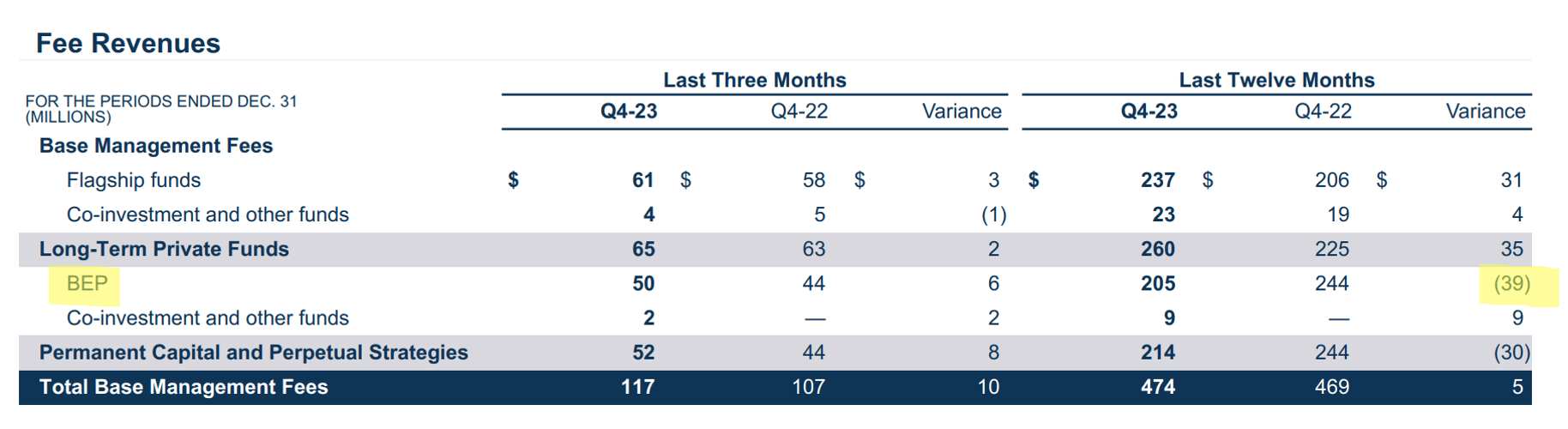

Looking at full year 2023 result, it's apparent that BIP base management fees did decline by $20 Million over the year, a decline of exactly 5%, in line with my expectations.

BAM IR

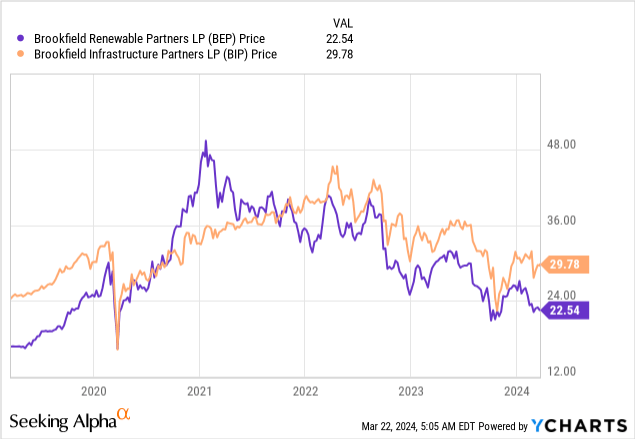

BEP's stock price has suffered more than BIP's and consequently BEP base management fees were down by $39 Million, which is as much as a 19% decline compared to the previous year.

BAM IR

The price of BIP and BEP has remained low, which means that Q1 2024 fees are very likely to be poor as well. I consider both funds interest rate sensitive which means that their price going forward is likely to be driven by interest rate expectations.

The Fed signaled three cuts most recently, but raised their longer term rate expectations for 2025 and 2026. If the Fed's current forecast holds, I don't expect interest rate sensitive stocks, including BIP and BEP, to rally any time soon.

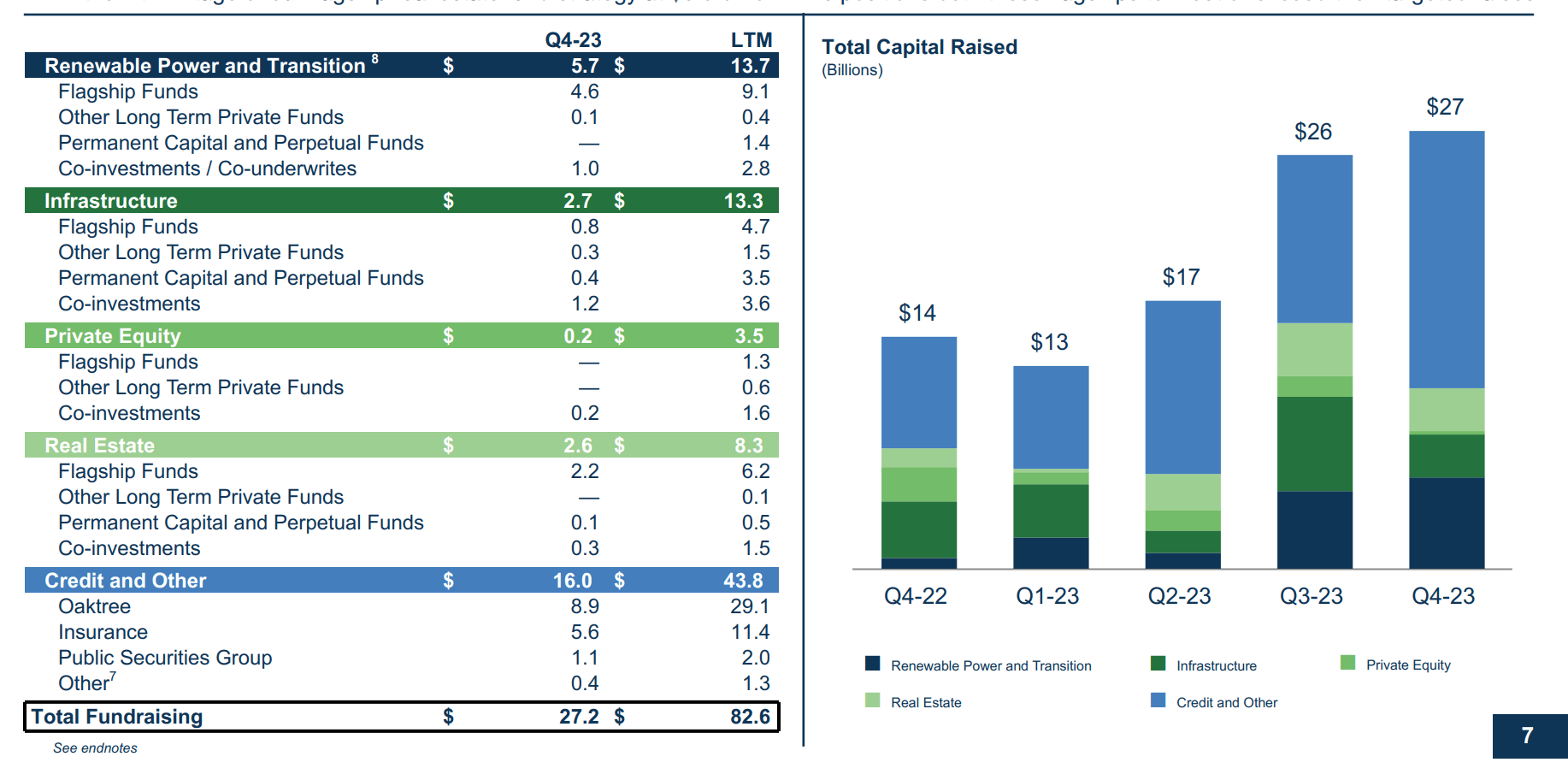

Therefore, BAM will have to lean heavily into other sectors if it wants to hit its ambitious double-digit earnings growth target. Recently, the best performing sectors have been private credit and insurance. And unsurprisingly, this is where the majority of fundraising came from in 2023 and especially in the latter half of the year.

BAM IR

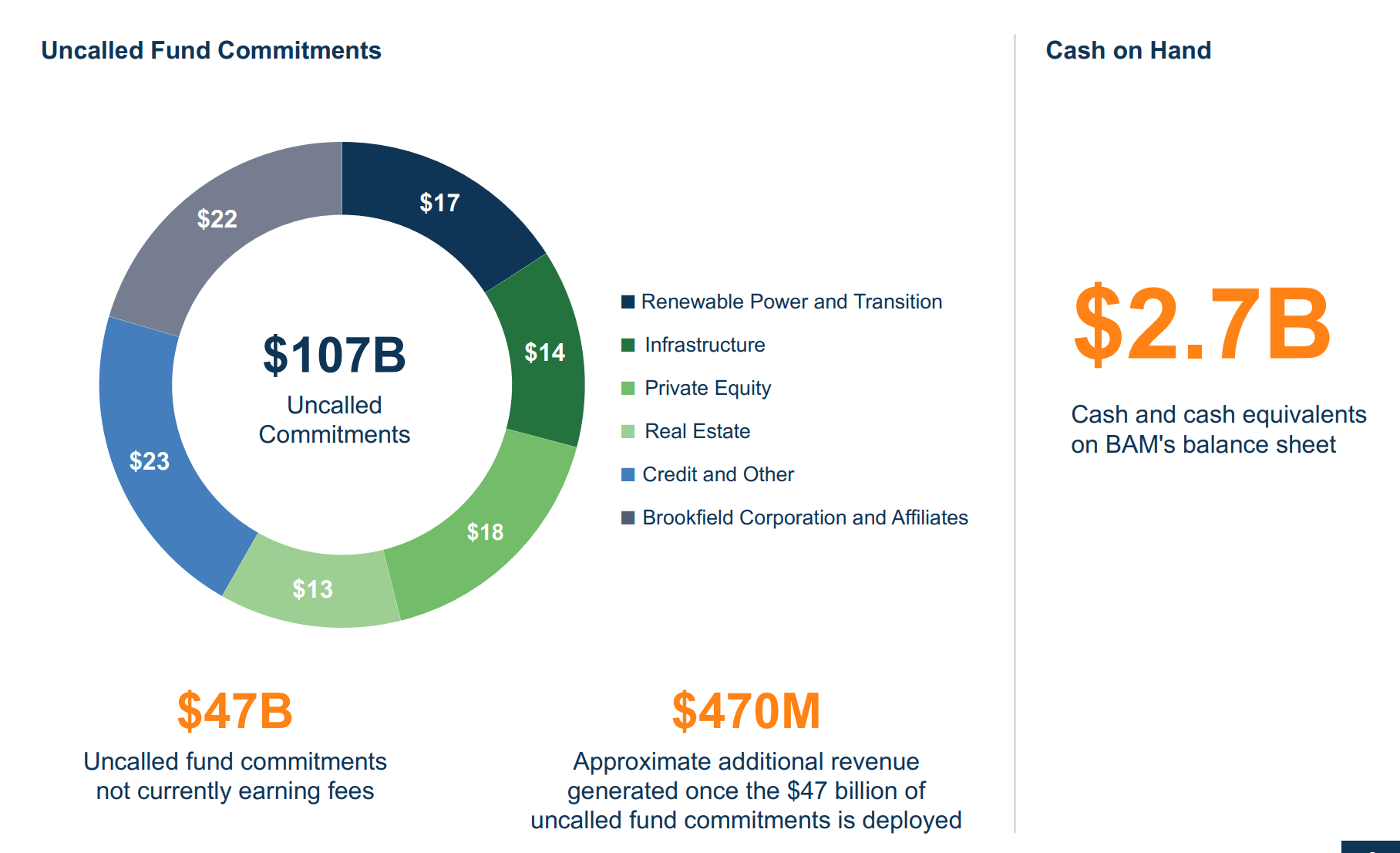

I don't know if BAM will be able to offset the negative impact of its renewable energy and infrastructure funds and reach the target in 2024, but its enormous dry powder position with more than $100 Billion in liquidity will certainly help. Once the $47 Billion in uncalled fund commitments is deployed, it will earn an additional $470 in management fees. More than enough to offset the $60 Million drop from BIP+BEP over time.

BAM IR

Long-term I think BAM is in a good position to grow its earnings, but deploying this capital will take time. Therefore, I'm not convinced that the company will be able to accelerate its FRE growth soon enough to hit its targets in 2024 and neither are the analysts covering the stock with a median growth forecast of 11.83% for 2024.

Seeking Alpha

Management seems confident and said this on their earnings call:

We set out that 15% to 20% CAGR that we expect to deliver on from an FRE perspective over the plan period. And to clarify, what I meant is 2024 should exceed that target.

However, I want to point out that they say this every year and did say it last year as well. Therefore, I would take their guidance with a grain of salt here.

The bottom line is that BAM delivered 6% annual earnings growth last year and is expected to deliver under 12% growth this year. Both below the ambitious target of 15-20%.

At the same time, the stock is very expensive at 31x fee-related earnings and a dividend yield barely above 3%. Historically, I argued for a fair multiple of 25x. That was back when BAM was still growing its bottom line by 15%+ per year. With growth down and the multiple up, I have no choice but to re-iterate my SELL rating here at $42.60 per share.