Scott Olson/Getty Images News

Scott Olson/Getty Images News

My investment portfolio looked very disbalanced just a couple of months ago since it was overwhelmed with the tech and growth. In recent months I started to balance growth with value and continue seeking for reliable opportunities among dividend stocks. My fundamental analysis suggests that Bank of America (NYSE:BAC) is highly likely to continue building value for shareholders at a stable pace. The bank is unlikely to outperform the market leader, JP Morgan Chase, in foreseeable future but its number two spot in the largest banking industry in the world is undisputed. The stock is attractively valued with an 11% discount and offers a solid dividend yield which makes it a "Strong Buy".

Bank of America is the second largest bank in the world by market capitalization, according to Forbes. At the same time, the bank's market cap is around two times lower than JPMorgan Chase (JPM), which is the number one. Apart from BAC and JPM, Wells Fargo (WFC) and Citigroup (C) form the so-called "Big four" group of the prominent U.S. banks. From the profitability metrics perspective BAC is less profitable than JPM, but looks much better in comparison with WFC and C.

SA

I think that a business model of any bank relies on just couple key pillars to drive revenue and profitability improvements. First is the customer base expansion and the second is the ability to sell as many services as possible to these customers. From the perspective of the second pillar BAC looks extremely good as it provides a wide array of services both to individuals, institutions, and businesses.

bankofamerica.com

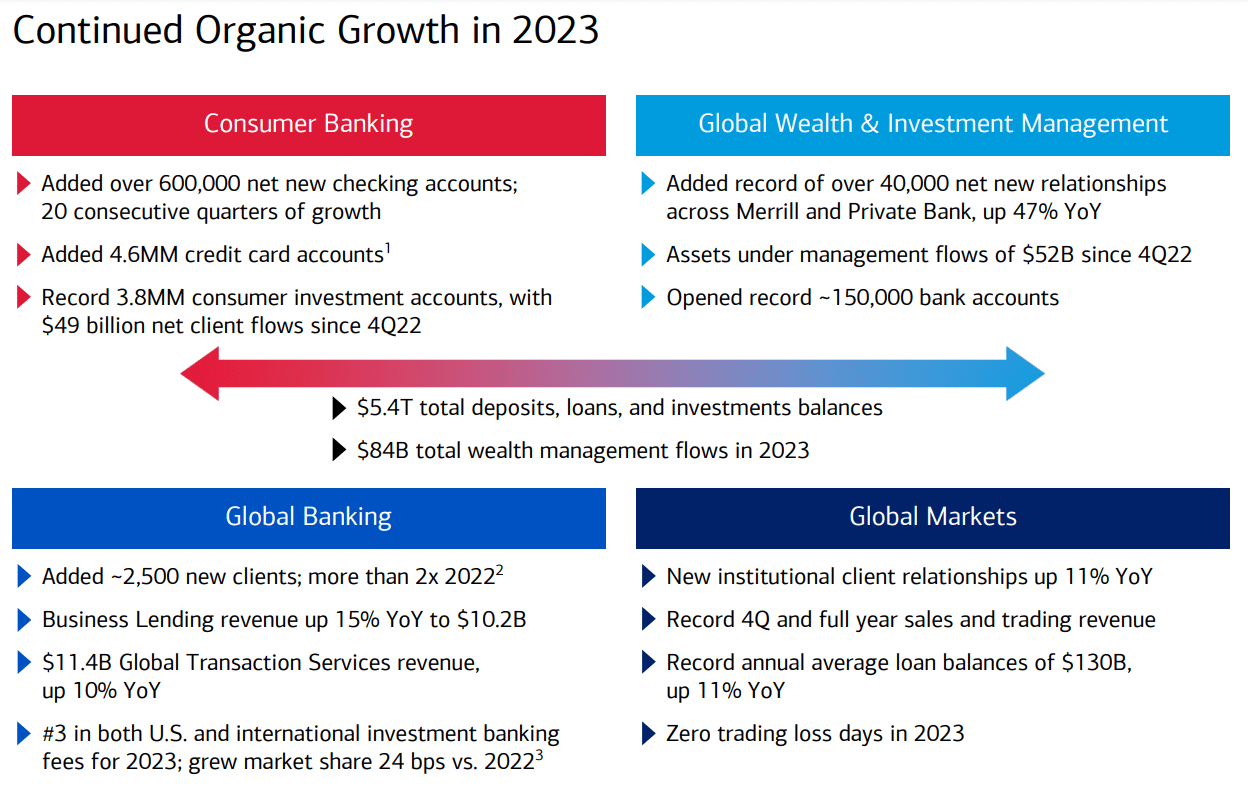

According to the latest earnings presentation, BAC also performs well to nurture the first pillar as well. The bank demonstrated solid growth in customer base across all lines of business, which looks especially impressive considering the bank's scale and that the growth is organic.

BAC's Q4 earnings presentation

Considering BAC's strong brand and the fact that its diverse portfolio of services is likely to make it an attractive option for customers who value having all financial services in one place, I think that the bank is well positioned to sustain its impressive customer base expansion.

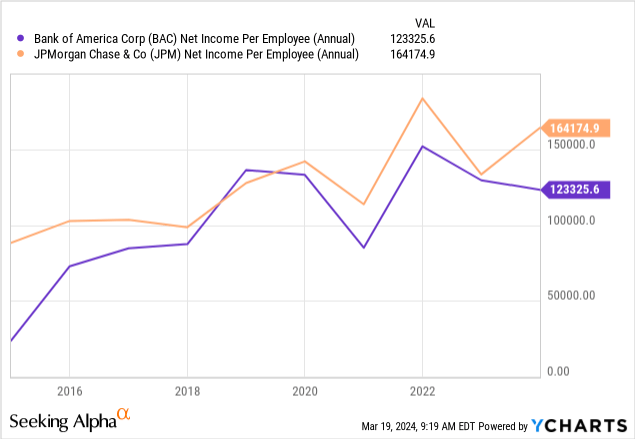

From the diversity of services perspective I am also positive. Being the second largest bank in the U.S. means BAC has ample resources to invest in new products development and be the trendsetter in the banking industry. The solid net income per employee dynamic compared to the leader, suggests that BAC's operational efficiency is close to JPM. This underscores the commitment of management to grow without forgetting about the financial discipline.

With solid and predictable prospects to continue expanding the top line combined with a track record of financial discipline, BAC is likely to continue steadily building value for its shareholders.

The financial performance demonstrated by BAC in the latest quarter should not mislead readers as the bank faces temporary headwinds due to the tight monetary policy, which is a cyclical, not a secular, matter. Higher deposit costs was the primary reason which weighted on the net interest margin and the bottom line, but I am quite optimistic because the Fed has not hiked rates further during several previous FOMC meetings and Goldman Sachs analysts expect three rate cuts this year. Therefore, I expect the pressure of higher interest rates to highly likely ease starting from Q3 2024. Moreover, despite all the external challenges caused by the tight monetary policy in 2023, the bank recorded a 4% revenue growth in the full fiscal year and expanded the adjusted EPS from $3.18 to $3.42. This underscores that the bank is able to exercise its strong customer based and cross-selling potential.

To smoothen the effect of cyclicality in interest rates on the bank's earnings, I think that the management will highly likely focus on its Global Wealth and Investment Management. The segment kept up well in Q4 2023 despite slight YoY decline in financial performance. What is crucial is that the business is expanding and BAC added over 7,000 new relationships in Q4. I am confident in future potential here because the global wealth management industry is projected to compound with a 10.7% CAGR by 2030, a strong secular factor for this segment. The largest portion of the segment's revenue is generated from asset management fees, which are growing and the decline in net interest income ("NII") is temporary, as I mentioned earlier.

BAC's Q4 earnings presentation

Considering that the segment adds new relationships consistently and client balances are growing, this means that the management does well in expanding opportunities for the bank to generate more asset management fees over the long-term, which will highly likely continue decreasing the effect of NII on the segment.

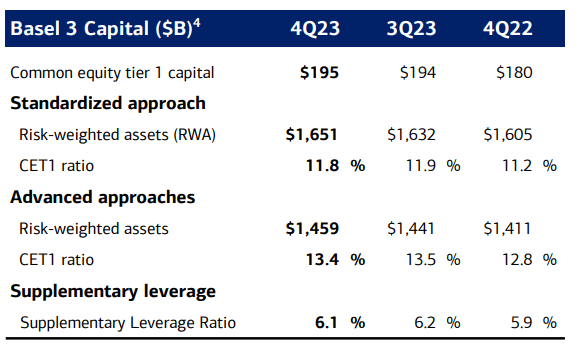

Highlighting the bank's strong balance sheet is also crucial in my bullish thesis about BAC. Assets and deposits grew sequentially, meaning more favorable funding mix for the bank. Common equity Tier 1 under the Basel III approach looks healthy and the bank is well positioned to meet all capital requirements from regulators.

BAC Q4 earnings presentation

BAC demonstrates robust momentum across multiple timeframes and rallied by 7% since the beginning of 2024. For a value stock like BAC looking at valuation ratios looks like a sound option. BAC looks fairly valued considering that currently valuation ratios are approximately perfectly in line with historical averages.

SA

Multiplying historical average non-GAAP forward P/E of 11.73 by a $3.41 consensus FY 2025 adjusted EPS estimate gives me the 12-months BAC target price at $40. This means that there is around 11% upside potential from the current $36 share price. Apart from the upside potential, investors should also keep in mind that the stock offers a decent 2.7% forward dividend yield backed by robust dividend consistency.

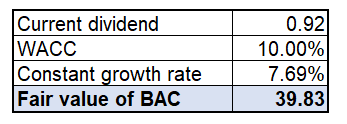

I want to cross-check the target price derived with the help of valuation ratios by calculating the fair stock price with the dividend discount model ("DDM"). As usual, I take a WACC recommended by Finbox, which is 10% at the midpoint of the suggested range. For "year zero" dividend I check the dividend payout history and take the FY 2023 dividend, $0.92 per share. BAC has a robust dividend growth history and its last decade's 37% dividend CAGR makes my DDM calculations irrelevant since I have to subtract constant growth rate from WACC. Therefore, I am using the sector median last 10-years' CAGR of 7.69%. Putting all the assumptions together into the DDM formula gives me fair value of BAC at slightly below $40, which aligns with outcomes of the first valuation method.

Calculated by the author

Since both methods' outcomes are very close to each other, I have high confidence in a $40 fair value of the stock.

Bank of America was a financial institution of the same fundamental strength a year ago as well, but its stock traded 30% lower. The stock suffered a notable sell-off after failures of few regional banks in March 2023. I think that such an overreaction even in respect of the second largest U.S. bank's stock is explained by the big share price declines during the financial crisis 2007-2008. BAC's shares decreased by more than ten times between 2007 peaks and early 2009, and I believe that many investors recall such a nosedive. Therefore, BAC's share price might suffer significantly even if much smaller banks fail due to the increased fears around the financial sector.

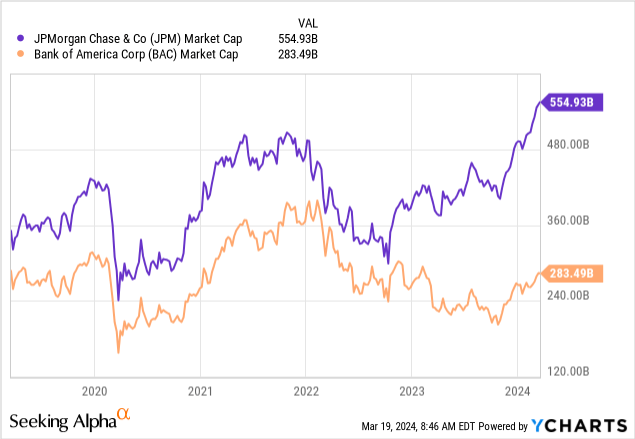

Based on the chart below, it looks like investors' sentiment around JPM is now much more positive compared to BAC. I reached this conclusion considering that market caps of both banks demonstrated almost perfect correlation in recent years, but JPM recovered from the 2023 banking sector selloff much faster and now the market cap of JPM is almost two times higher than BAC has. Of course, the acquisition of a substantial majority of assets of First Republic Bank contributed to the market cap from an accounting perspective, but such acquisitions are rarely absorbed by the market with big optimism. The fact that JPM recovered from the 2023 crisis and big acquisition (with all the underlying risks of acquiring assets of the bank that just failed) faster than BAC did indicates that investors consider JPM deserving premium to the share price more than BAC does. This might limit BAC's potential to share in price above its fair value.

There was a significant controversy last year around BAC's massive unrealized losses in its held-to-maturity bond portfolio. I consider this a purely theoretical and accounting issue, because BAC's bond portfolio mostly consists of U.S. treasuries which are considered risk-free and will highly likely be held to maturity. The probability of this loss being ever realized is close to zero in my opinion. Moreover, as yields and valuations of treasuries moderate, this unrealized loss narrows. However, such headlines might significantly hurt investors' sentiment around BAC.

Bank of America looks like a very attractive investment opportunity at the current share price level. The bank is strong in improving two key pillars of any bank: customer base growth and selling as much services to customers as possible. Let us also not forget about the bank's solid dividend consistency and a 2.7% dividend yield.