BogdanVj

BogdanVj

AZZ (NYSE:AZZ) specializes in hot-dip galvanizing and coil coating solutions, and it operates mainly in North America. AZZ's historical revenue growth has been volatile due to major events such as the COVID-19 pandemic. In 2023, strong revenue growth was primarily driven by its acquisition of Precoat Metals. Its margins were robust from 2020 to 2022, but the net income margin fell in 2023 due to a ~$132 million loss on the disposal of a discontinued operation. For 3Q24, revenue continued to grow, but at a modest rate of 2.2%. On a brighter note, its margins expanded year-over-year due to lower expenses and improved operational efficiencies. Looking ahead, the construction market is anticipated to grow in 2024, which will provide a tailwind for AZZ's growth. However, my simplified DCF model indicates no upside potential. Therefore, I am recommending a hold rating, despite the expectation that AZZ will grow for the next two fiscal years.

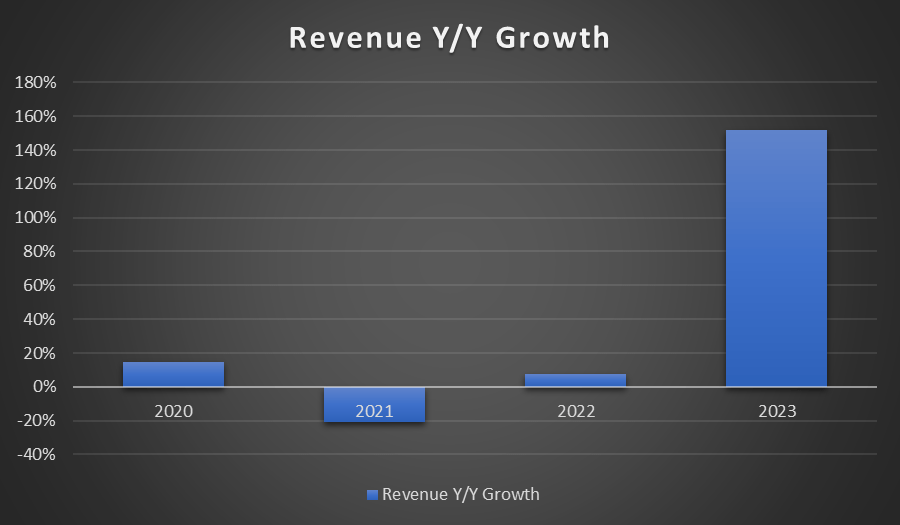

AZZ’s past four years of sales growth were volatile. In 2021, sales were down 21% due to the impact of COVID-19, which drove volume down. In 2023, sales were up 151.8% due to strong growth in its Metal Coatings segment. Metal Coating in 2023 increased by 21.2% due to improved price realization and increased volume. However, the main driver was its acquisition of Precoat Metals, which contributed ~$686 million in sales to AZZ. If I exclude the acquisition, organic growth is ~21.2%, which is still higher than 2022’s growth rate and signals a recovering trend.

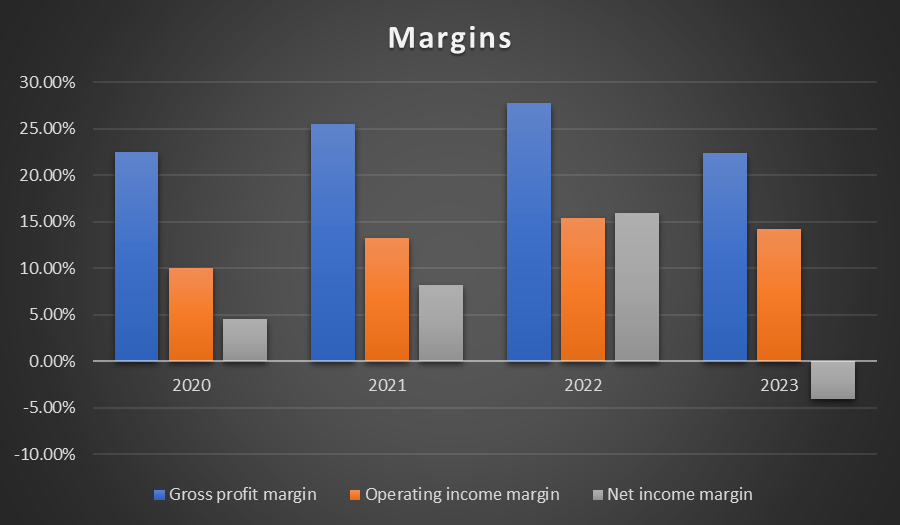

In terms of margins, it performed relatively well from 2020 to 2022, as all of them expanded annually despite fluctuating revenue growth. In 2023, AZZ’s operating income was down slightly year-over-year, but its net income margin took a hit. Net income margin fell due to a ~$132 million loss on disposal of discontinued operations. If we adjusted for this one-time expense, the net income margin for 2023 is ~5%, which is still lower than 2022’s margin. The reason behind this is the significant increase in interest expense of ~$82.4 million to $88.8 million vs. 2022’s $6.4 million. Interest expense rose because of additional debt that was obtained in order to acquire Precoat Metals.

Author's Chart

Author's Chart

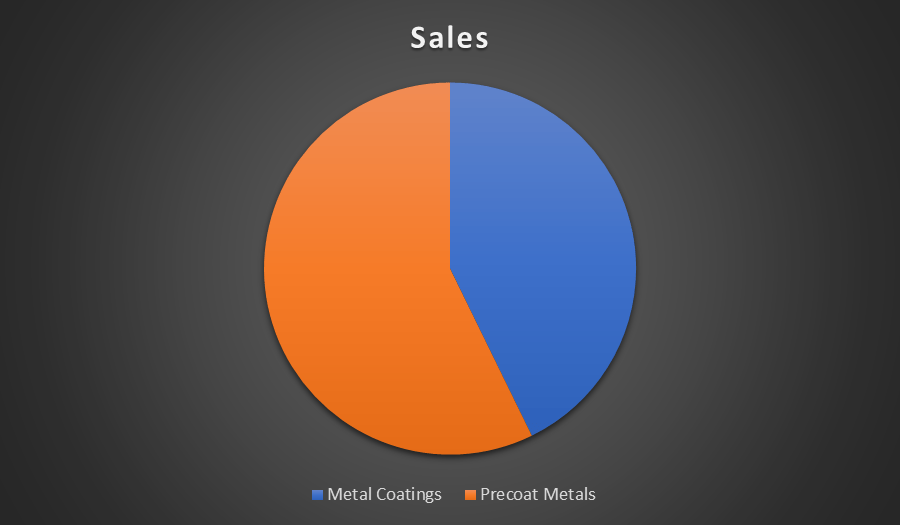

For 3Q24 results released in January, Metal Coatings reported sales of ~$163 million, while Precoat Metals reported ~$218 million. Total revenue reported was ~$381 million, up 2.2% year-over-year. Metal Coatings’ sales increased 3.1% year-over-year, driven by an increase in price but partially offset by lower volume. Turning to Precoat Metals, it was up 1.6% year-over-year, and the growth was also driven by price increase offset by lower volume.

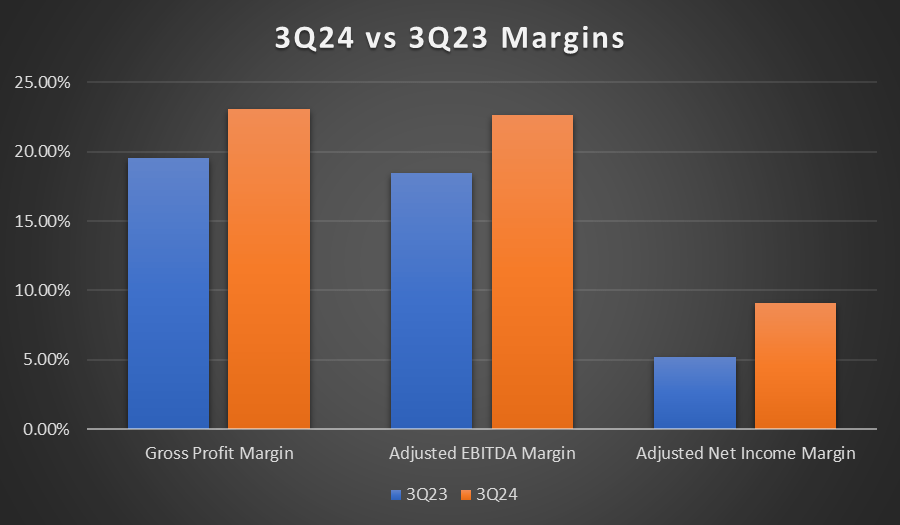

Moving down the P&L, AZZ’s 3Q24 margins grew year-over-year. Firstly, 3Q24’s gross profit margin expanded from 19.6% to 23.1%. The expansion in gross profit margin was due to lower zinc costs and overhead expenses. Its adjusted EBITDA margin increased from 18.5% to 22.6% in 3Q24. Apart from gross profit expansion benefiting its adjusted EBITDA margin, the growth was also driven by favorable mix as well as improved operational efficiencies in Metal Coatings and Precoat Metals.

As a result of growth in its gross profit and adjusted EBITDA margins, its adjusted net income margin expanded to 9.1% from 3Q23’s 5.22%. Adjusted diluted EPS for 3Q24 was $1.19, up 52.6% from the previous period’s $0.78.

Author's Chart

Author's Chart

In 2022, AZZ acquired Precoat Metals for ~$1.28 billion. Precoat Metals is a company that specializes in metal coil coating solutions, and it is the leading provider in North America [NA]. For the nine months ended 30 November 2023, Precoat Metals reported sales of $669 million, compared to the previous period’s $499 million. This represents a year-over-year growth of 34%. In addition to strong revenue growth, its EBITDA also increased, with the previous period reporting ~$93 million compared to ~$129 million for the nine months ended 30 November 2023, representing a growth rate of ~38%. Based on management, the size of the market Precoat operates in is estimated to be ~$3.7 billion. Currently, it owns ~23% of the total share, and it is the current market leader.

Investor Relations

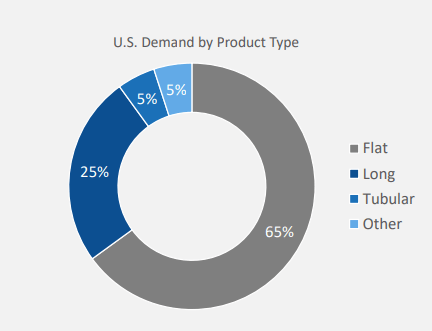

The acquisition of Precoat Metals adds new capabilities for AZZ, allowing it to offer coating solutions to the market. More importantly, it will be able to offer coating solutions to the flat steel market, which forms the largest share of total US demand by product type. Based on the chart, flat steel accounts for 65% of total US demand by product type. In addition, it also allows AZZ to tap into the expanding aluminum sector.

Investor Relations

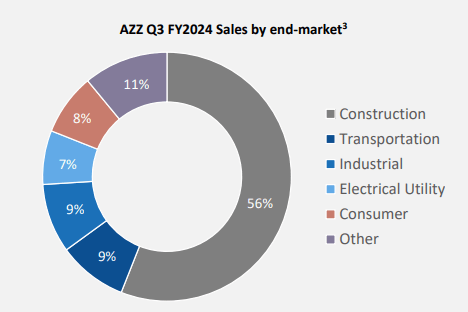

Looking at the sales by end market chart, construction forms the largest share of AZZ sales, with the remainder split evenly amongst transportation, industrial, electrical utility, consumer, and others. Based on the Dodge Construction Network Outlook 2024 report, total construction starts are anticipated to increase by 7% in 2024 to ~$1.2 trillion. This is an improvement when compared to 2023, which saw growth decelerate to 1%.

Nonbuilding is expected to grow, but at a modest rate of ~7% to ~$342 million. Due to the $1.2 trillion Infrastructure Investment and Jobs Act [IIJA], public works is expected to grow at a double-digit rate of 17% in 2024. For institutional construction, it is anticipated to grow by ~3% in 2024. Residential construction can be segmented into single-family and multifamily. For single family, it is expected to grow 9% while multifamily at 14%. Lastly, for manufacturing construction starts, it will continue to grow in 2024 at ~16% due to improving supply chains.

As the construction end market forms the largest share of AZZ’s sales, at 56%, growth in this segment has a higher weightage as compared to the rest. Overall, growth is expected across all segments in construction, and the strong outlook is expected to bolster and support AZZ’s growth outlook in 2024.

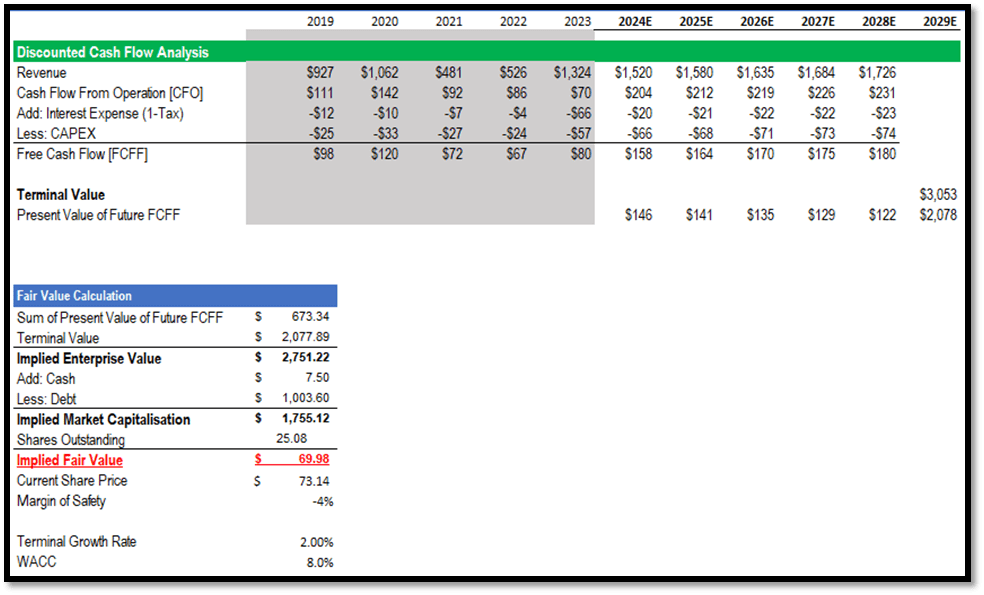

As there are no direct competitors listed, I will be using a simplified 5-year DCF model to calculate the intrinsic value of AZZ, as relative valuation is not feasible. For 2024 and 2025, the revenue growth rates used are in line with the market estimate of ~15% and ~3.9%, respectively. Given the strong performance from Precoat Metals and a positive construction outlook, these factors provide AZZ with the tailwind and opportunity to grow. Therefore, the market revenue estimates are justified in my view. For the remaining three years, I model the growth rate to taper to the terminal growth rate to allow for a smoother transition towards the terminal period.

AZZ's 5-year median cash flow from operations [CFO] as a percentage of total revenue is ~13%. In my DCF model, I used AZZ's 5-year median CFO as a percentage of total revenue and extrapolated it for the next 5 years, ensuring that my model remains conservative. For CAPEX, I also used the same methodology and used AZZ’s 5-year median CAPEX as a percentage of total revenue, which was ~4%.

To calculate the terminal value, a terminal growth rate, WACC, and the FCFF for 2028 are required. To maintain conservatism, I will use 2% for the terminal growth rate. Although the current US 30-year treasury yield is approximately 4.4%, which is above the US historical average GDP growth rate, the terminal growth rate should not exceed a country's GDP growth rate. Consequently, my terminal value is ~$3 billion, or a present value [PV] of ~$2 billion.

The sum of the PV of AZZ's future free cash flow to the firm [FCFF] is ~$673 million. By adding the sum of the PV of its future FCFF to the PV of the terminal value, its implied enterprise value is ~$2.75 billion. Based on my conservative assumptions previously discussed, my implied intrinsic value for AZZ is ~$69, which is slightly below its last traded share price.

Author's Valuation Model

The upside risk to my hold rating pertains to the positive outlook of the construction market in 2024. It is anticipated that the construction market will grow and outperform that of 2023. Given that construction accounts for 56% of AZZ’s sales, this growth is likely to have a significant positive impact on AZZ’s future revenue. Additionally, AZZ’s 3Q24 margins expanded, partially due to improved operational efficiencies in its Metal Coatings and Precoat Metals segments. Therefore, with higher revenue, AZZ is expected to generate higher profits. In this scenario, the market might adjust its expectations for AZZ upwards if its performance exceeds expectations.

In conclusion, AZZ's revenue growth over the past four years has been volatile. In 2021, the decline in revenue was caused by the COVID-19 pandemic, but it recovered in 2022. In 2023, the strong year-over-year growth was driven by its acquisition of Precoat Metals. Despite fluctuating revenue growth, its margins remained relatively robust, except for 2023, due to a ~$132 million loss from the disposal of a discontinued operation. Moving on to its most recent 3Q24 results, its revenue continued to grow, but at a modest rate of low single digits. However, its margins expanded year-over-year due to lower costs and improved operational efficiencies in its Metal Coatings and Precoat Metals segments. Moreover, its acquisition of Precoat Metals has been yielding positive results.

Looking ahead to 2024, the Dodge Construction Network expects construction starts to grow by 7%. Compared to 2023, which saw growth decelerating to 1%, this represents a significant improvement. With construction accounting for 56% of AZZ’s sales by end market, the positive outlook is expected to have a significant impact on AZZ’s future growth. Despite the positives mentioned above, my simplified DCF model indicates no upside potential, suggesting it is fairly valued currently. On this note, I am recommending a hold rating for AZZ as of now.