cagkansayin

cagkansayin

AstraZeneca (NASDAQ:AZN) announced it will acquire Fusion Pharmaceuticals (NASDAQ:FUSN) for $21 per share, or approximately $2 billion, plus a contingent value right (‘CVR’) of $3 per share payable upon the achievement of a specified regulatory milestone, which brings the total potential value to approximately $2.4 billion and premiums to Fusion’s closing price yesterday of 97% and 126%, respectively. The deal is expected to close next quarter.

This is a somewhat unsatisfying end of the story for IPO investors of Fusion as the company went public in June 2020 at $17 per share, but a generally good end of the story for all investors who bought the stock at least a few months following the IPO as the stock spent all this time trading far below the IPO price.

In my December 2023 article on AstraZeneca, I noted that the company had built an envious product portfolio and pipeline. With the Fusion acquisition, AstraZeneca is getting a late-stage radiopharmaceutical company through the program FPI-2265 which could bring $1 billion in peak annual sales in the initially targeted third line+ metastatic castration-resistant prostate cancer (‘mCRPC’) and this could increase to several billion if the candidate is able to move to earlier lines of therapy.

The acquisition also brings Fusion’s radiopharmaceuticals manufacturing expertise, two early-stage clinical candidates and full rights to FPI-2068, a phase 1-ready candidate AstraZeneca had already in-licensed from Fusion.

Fusion Pharmaceuticals investor relations

The radiopharmaceuticals market is becoming a hot space for biotech M&A. This deal comes on top of Bristol Myers Squibb’s $4.1 billion acquisition of RayzeBio and Eli Lilly’s $1.4 billion acquisition of POINT Biopharma. AstraZeneca decided to join the party by acquiring Fusion.

Fusion itself acquired FPI-2265 from RadioMedix in February 2023, and it targets prostate-specific membrane antigens, or PSMA, found on the surface of prostate cancer cells in higher amounts than normal prostate cells and is a validated target for the treatment of prostate cancer. PSMA is expressed in more than 80% of men with prostate cancer and higher PSMA expression is correlated with worse outcomes.

FP-2265 is following in the footsteps of Novartis’ (NVS) Pluvicto, a lutetium-177 PSMA-targeted therapy approved for the treatment of mCRPC. Pluvicto was approved in 2022 and generated $271 million and $980 million in net sales in 2022 and 2023, respectively.

FPI-2265 is an actinium-225 based PSMA targeting radioconjugate and it emits a greater radiation dose over a shorter distance, and Fusion believes that alpha particles (compared to Pluvicto's beta approach) such as actinium-225 “have the potential for more potent cancer cell killing, and targeted delivers, thereby minimizing damage to surrounding healthy tissue.”

FPI-2265 is now a late-stage candidate as Fusion was planning to start a phase 2/3 trial in the second quarter with potential for FDA approval, assuming the data are positive.

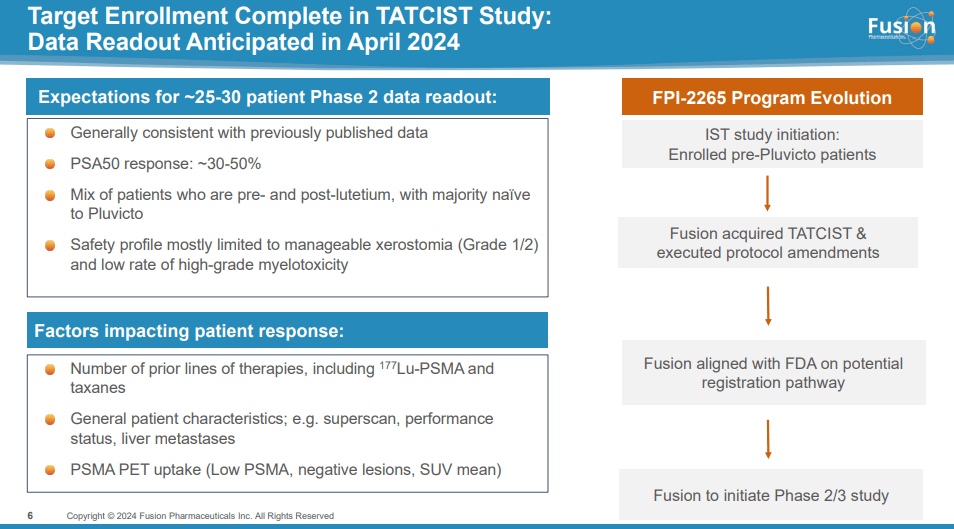

Interestingly, the acquisition comes just before the expected data readout from the TATCIST trial of Fusion’s lead asset FPI-2265 in April. It's just speculation on my part, but I believe it's more than likely that AstraZeneca saw these data and decided to pull the trigger before they were publicly available which could have pushed Fusion’s price higher. Fusion set expectations for the data in 25 to 30 patients by saying the PSA50 response (defined as a 50% decrease in PSA from baseline) should be in the 30% to 50% range and that safety profile would be manageable with grade 1/2 xerostomia (dry mouth) and low rate of high-grade bone marrow toxicity. It's possible, if not likely, that the data to be presented next month have exceeded the thresholds set by Fusion.

Fusion Pharmaceuticals investor presentation

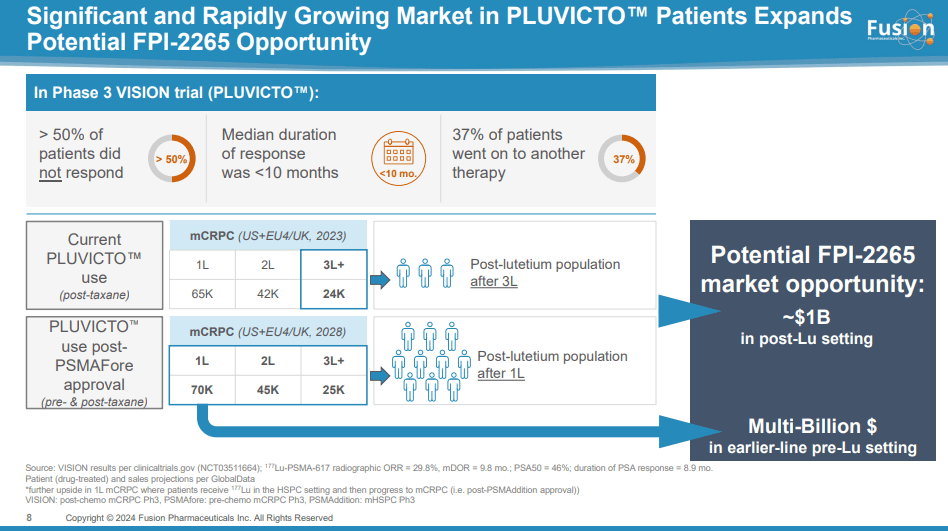

The addressable market even in the third-line+ population post-Pluvicto is significant with more than 24,000 patients and a billion dollar+ opportunity, based on Pluvicto's price per patient that is in excess of $200,000 per year. AstraZeneca will likely adopt Fusion’s development plan and attempt to expand to first-line and second-line treatment of mCRPC which would significantly expand the market by nearly six times the initial addressable market.

Fusion Pharmaceuticals investor presentation

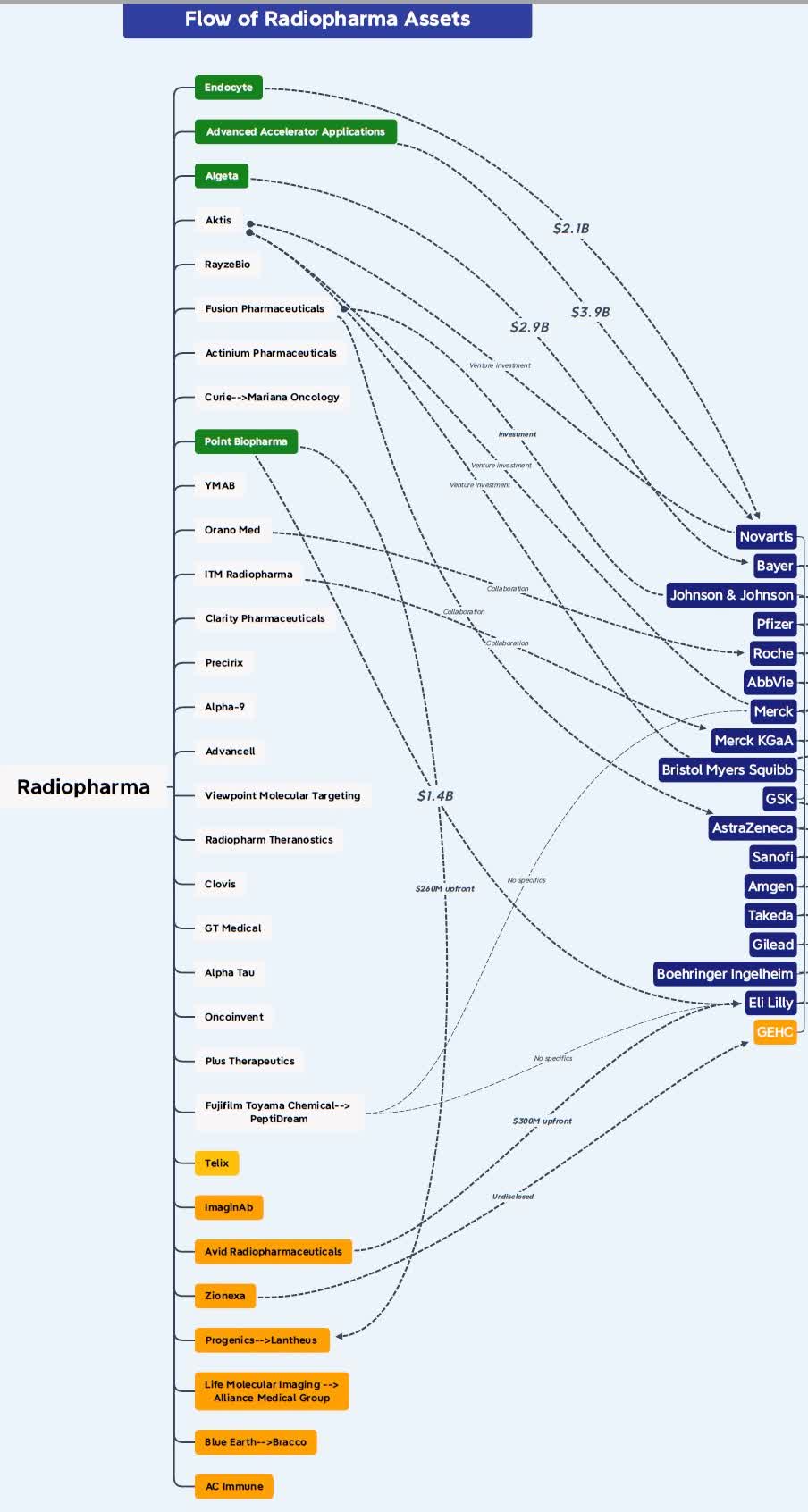

Of course, this is not a straightforward proposition and AstraZeneca is taking on the development risk and the competition risk as this is not the only approach for the treatment of mCRPC and this is a very attractive and increasingly competitive market. And the radiopharmaceuticals market is evolving rapidly and several big pharma companies are now active – Bayer (OTCPK:BAYZF), Novartis, Johnson & Johnson (JNJ), and more recently Bristol-Myers Squibb (BMY) and Eli Lilly (LLY) through the acquisitions of RayzeBio and POINT Pharma, respectively. The graph from Jacob Plieth at X (formerly Twitter) from October 2023 (that now needs to be updated) shows the flow of radiopharma assets, but also the crowding.

X (formerly Twitter)

However, getting Fusion’s radiopharmaceuticals expertise and manufacturing operations and the early-stage pipeline along with this valuable late-stage shot on goal with FPI-2265 seems worth the risk of spending between $2 billion and $2.4 billion.

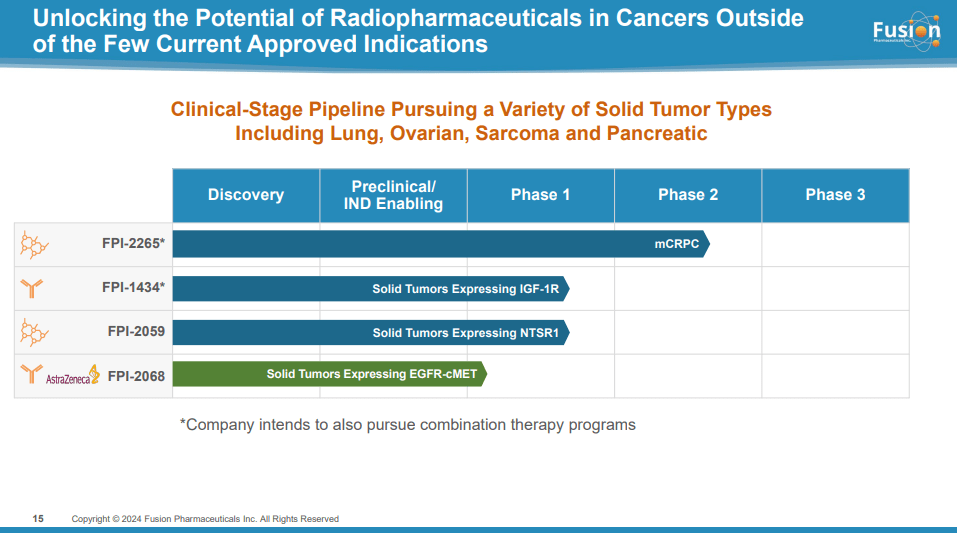

Fusion’s early-stage pipeline consists of three candidates:

The early-stage pipeline is unproven but provides something AstraZeneca could fall back on if FP-2265 disappoints in late-stage trials in mCRPC patients.

The acquisition of Fusion Pharmaceuticals expands AstraZeneca’s operations in the radiopharmaceuticals market beyond the initial FPI-2068 candidate that was in-licensed from Fusion. At the very least, AstraZeneca is getting Fusion’s radiopharmaceuticals expertise, the manufacturing operations and a base from which to expand in the following years. However, that alone is not enough to justify the price tag and the company would need to show clinical success with FPI-2265 or other earlier stage candidates. The upside from FPI-2265 in mCRPC is significant and success in third-line+ population could pay off handsomely and FPI-2265’s expansion into earlier lines of mCRPC and early-stage pipeline success could add to AstraZeneca’s top and bottom line in the late 2020s and early 2030s.

And for the majority of Fusion Pharmaceuticals investors, this should be a satisfactory outcome given where the share price has traded since the June 2020 IPO and all the risk is now transferred to AstraZeneca shareholders.