JHVEPhoto/iStock Editorial via Getty Images

JHVEPhoto/iStock Editorial via Getty Images

Axalta Coating Systems (NYSE:AXTA) is a company that manufactures and supplies high-performance coating systems. AXTA’s past financials have shown volatile revenue growth due to the impact of COVID-19, but it has also demonstrated a strong recovery. Due to rising inflation, gross profit margins were under pressure, but it managed to maintain its net income margin. In 2023, revenue continued to report growth. In addition, margins expanded year-over-year when compared to 2022. Looking ahead, its refinish and mobility segment’s outlook is positive, which is expected to bolster its growth outlook. With double-digit upside potential, I am recommending a buy rating for AXTA.

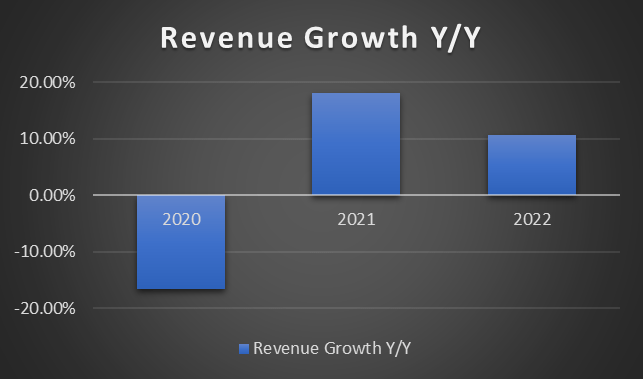

Over the last three years, AXTA’s revenue growth year-over-year was volatile, but it showed a strong recovery in 2021 onward. In 2020, revenue was down ~16% due to a significant reduction in global automotive production, lower driving distance, and low collision repairs caused by the COVID-19 pandemic. In 2021, revenue recovered and grew ~18% year-over-year, driven by demand recovery as COVID-19 subsides. In 2022, revenue continues to report strong growth of ~10.6%, driven by increased pricing and higher volume.

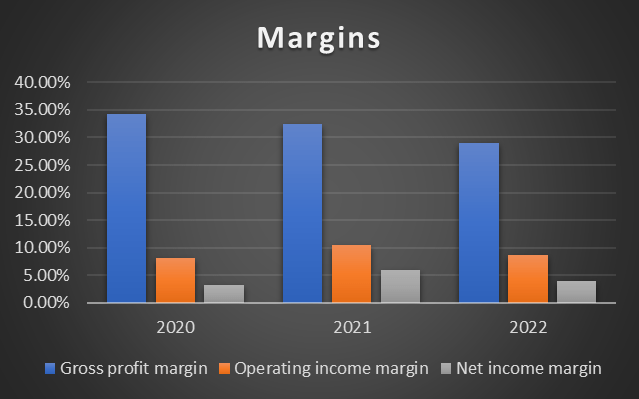

In terms of margins, operating income margin and net income margin have remained robust throughout the years despite contracting gross profit margin. In 2022, the gross profit margin contraction was caused by higher input costs due to rising inflation. The gross profit margin contraction seen in 2021 was also caused by rising inflation.

Author's Chart Author's Chart

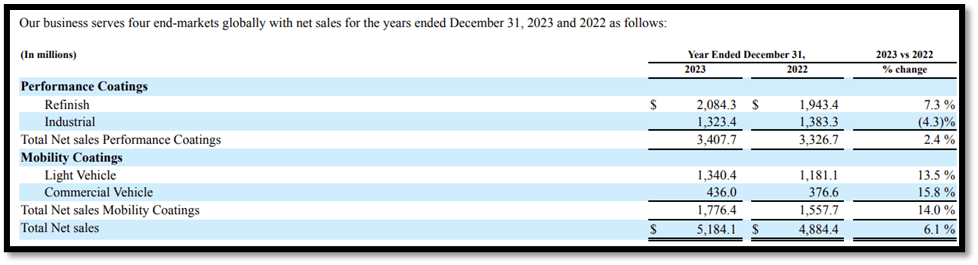

For 4Q23, revenue was up 4.9% year-over-year. This growth was driven by improvements in both volume and price/mix. They were up 1.7% and 0.9%, respectively. Revenue can be segmented into performance coating and mobility coating. For its performance coating, revenue increased 3.7% for 4Q23, and the growth was due to a strong price/mix in both refinish and industrial. For mobility coating, revenue increased 7.3% for 4Q23, driven by strong volume as light vehicle volume grew strongly but was partially offset by a decrease in class 8 production in North America.

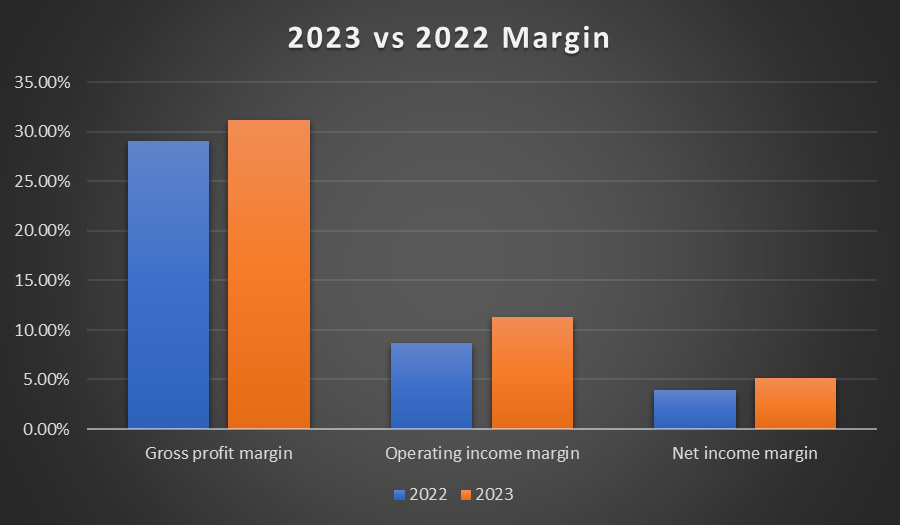

For the full year, revenue was up 6.1% year-over-year. The growth is driven by increased pricing and a higher product mix in both revenue segments, as mentioned. However, it was partially reduced by lower volume due to a weaker industrial market environment. In terms of margins, 2023’s saw all margins expand year-over-year. Gross profit margin expansion was due to increased pricing in both the performance coating and mobility coating segments, lower input costs due to lower inflation, and cost savings generated from its productivity programs that were introduced in 2023. The expansion in gross profit margin benefits its operating income margin and net income margin. As a result, diluted EPS grew from $0.86 to $1.21.

Author's Chart

Annual Report Author's Chart

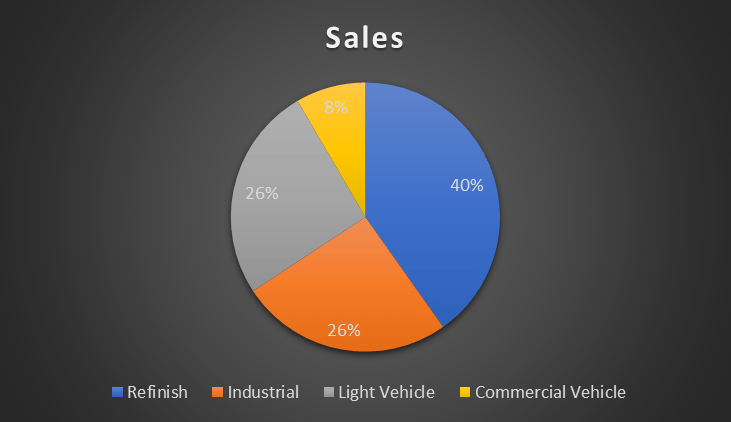

Based on the chart, the refinish segment forms the largest share of total revenue, at approximately 40%. Refinish's key focus areas are mainly independent body shops, multi-store operators (MSO), and auto dealership groups. Refinish's revenue is dependent on the volume of vehicle collisions, the vehicle owner’s inclination to repair their vehicles, and the size of the car parc. Although refinish coating forms a small percentage of the total vehicle repair cost, the appearance of the vehicle repair is important as it affects clients’ satisfaction levels. Therefore, many body shops seek coating from manufacturers that is of the highest standard. AXTA is a leading manufacturer and supplier of high-performance coating systems with more than 150 years of experience.

World Economic Forum

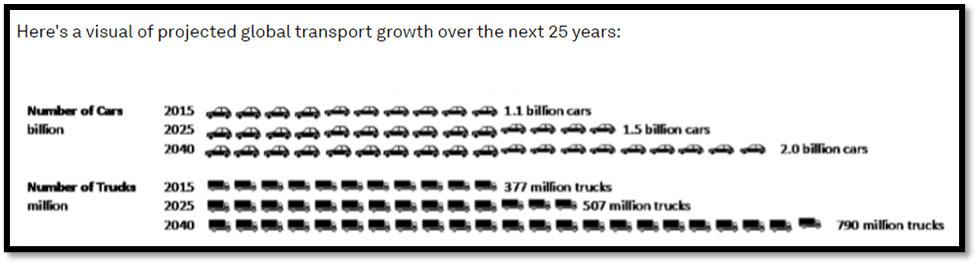

As mentioned, one of the key factors that drives refinish revenue is the size of the car parc. Based on the World Economic Forum, the total number of cars is expected to almost double by 2040, reaching ~2 billion cars vs. 2015’s 1.1 billion cars. Additionally, in 2022, the global automotive refinish coating market reached ~$10 billion. This market is anticipated to grow at a CAGR of 4.4% and reach ~$13.2 billion by 2028.

Looking ahead to 2024, management is expecting the refinish segment to remain robust. In 2023, AXTA reported net body shop wins in the range of more than 2500, which is a testament to its branding image, and such a win further extended its leading market position in the refinish segment.

Mobility coating forms the second-largest share of total revenue, and it is made up of light and commercial vehicles. In order to support growth in this segment, strategic investments were made, especially with local Chinese OEMs. One such example is the opening of a manufacturing site in Jilin, China, and management anticipates attractive long-term growth opportunities in this area.

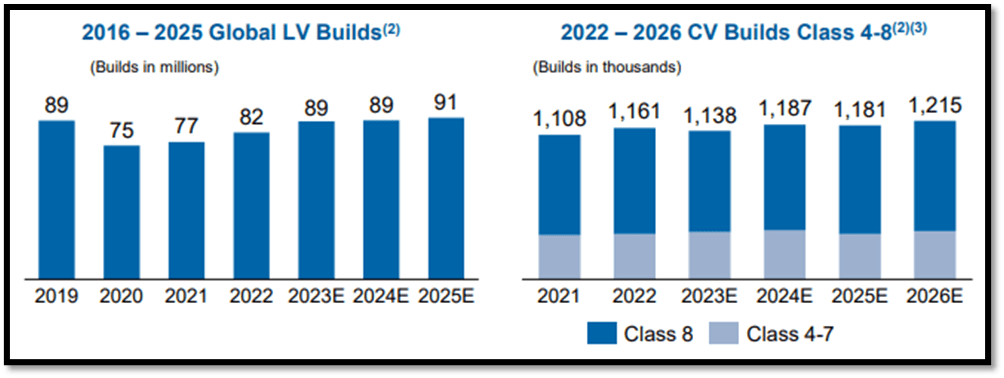

For light vehicles (LV), which account for 26% of total revenue, global LV build is expected to be flat in 2024 due to the strong recovery in production in 2023. However, the global build is expected to grow to ~91 million in 2025. For commercial vehicles (CV), it is expected that demand will increase in 2025 and 2026 before the 2027 new emission standards are implemented. However, management did mention that the Class 8 build will slow down in 2024, but modestly.

Investor Presentation

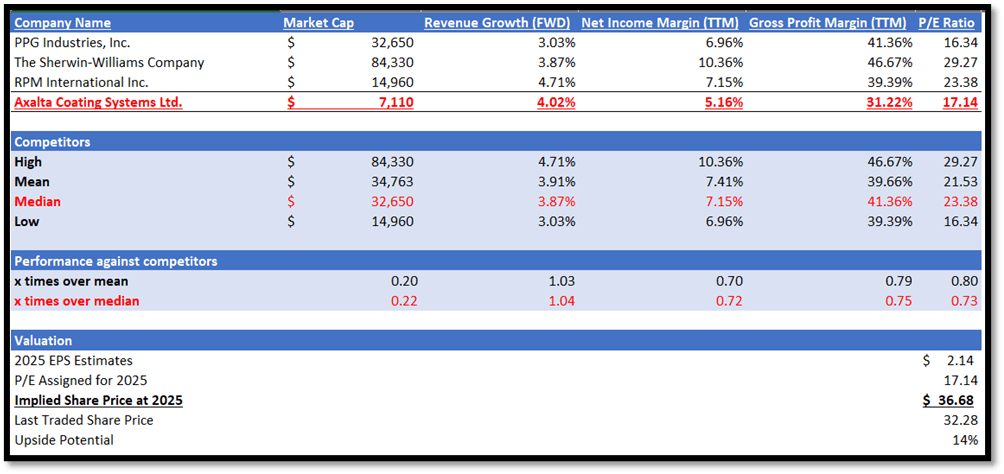

AXTA operates in the specialty chemicals industry, and the peers listed in my model also operate in the same industry. I will be comparing them in terms of forward growth outlook and TTM profitability margins. In terms of forward growth outlook, AXTA only slightly outperformed its peers’ median. AXTA has a forward revenue growth rate of 4.02% vs. peers’ median 3.87%, which represents a modest outperformance of only 0.15%.

In terms of TTM profitability margin, AXTA underperformed its peers. AXTA has a gross profit TTM of 31.22%, which is lower than its peers’ median of 41.36%. Secondly, AXTA’s net income margin TTM is also lower. It has a net income margin TTM of 5.16% vs. peers’ median of 7.15%.

Currently, AXTA forward P/E ratio trades at 17.14x, which is lower than peers’ median of 23.38x. Given its modest outperformance in forward revenue growth rate and underperformance in profitability margin TTM, I argue that it is fair for AXTA to be trading at a discount.

For 2025, the market revenue estimate for AXTA is $5.50 billion, while EPS is $2.14. Given the growth catalysts discussed above, the market estimates are justified as they echo the same positive sentiments. By applying 17.14x to AXTA’s 2025 EPS estimate, my target share price is $36.68, which represents an upside potential of 14%.

Author's Valuation Model

The downside risk to my buy recommendation is in regards to the anticipated slowdown in global LV and class 8 builds in 2024 before they recover from 2025 onward. LV and CV combined account for ~34% of total revenue, which is significant as they form the second largest share of AXTA’s total revenue. Therefore, any slowdown, or more than expected slowdown, will have an impact on AXTA’s upcoming quarter’s earnings results. In this scenario, it might cause some uncertainties in regards to AXTA’s growth outlook, and the market might adjust its expectations accordingly to reflect the headwind the company is facing.

In conclusion, AXTA’s past financial results have demonstrated strong revenue recovery from the impact of COVID-19, which severely impacted its 2020’s result. Despite rising inflation, which caused its gross profit margins to contract, its operating margin and net margin remained relatively robust. For 2023, it continues to report revenue growth driven by improvements in volume and price/mix. Additionally, its 2023 margins also expanded when compared to 2022.

Looking ahead, its largest revenue segment, refinishing, is expected to remain strong. In addition, its second-largest segment, mobility coating, is also expected to grow from 2025 onward, with 2024 being almost flat. In my relative valuation model, my target price indicates that there is double-digit upside potential. Therefore, I am recommending a buy rating for AXTA.