AsiaVision

AsiaVision

Axsome Therapeutics (NASDAQ:AXSM) revealed Q4 earnings on Tuesday. The company's depression drug, Auvelity (dextromethorphan-bupropion), continues steady growth in a competitive market. For the fourth quarter and the full year, Auvelity achieved $49.0 million and $130.1 million, respectively. This is definitely an accomplishment given the treatment landscape for depression, which is jam-packed with established and frontline alternatives like SSRIs (e.g., Prozac) and SNRIs (e.g., Cymbalta). I went into greater detail in previous writings about how Auvelity fits in.

My last update on Axsome expressed concern that losses were outpacing revenue. This is still the case.

Axsome Therapeutics

The company continues massive R&D efforts in historically difficult indications like fibromyalgia, Alzheimer’s disease agitation, and migraines. Furthermore, the costs associated with getting a new depression drug out there on the market are high (as evidenced by ballooning SG&A expenses).

A significant detail in Axsome's financial report underscores a less favorable view of its operations: The "Loss in fair value of contingent consideration," attributed to "updated sales projections for the recently announced new indications in solriamfetol," resulted in a higher net loss compared to the same period last year. Absent this factor, Axsome's net losses would have shown a reduction.

In practice, Auvelity is seen as a later resort that "may" be more effective than bupropion alone. Auvelity has not been tested against other antidepressants. In a study of Auvelity against bupropion alone, according to its label, "dextromethorphan contributes to the antidepressant properties of Auvelity."

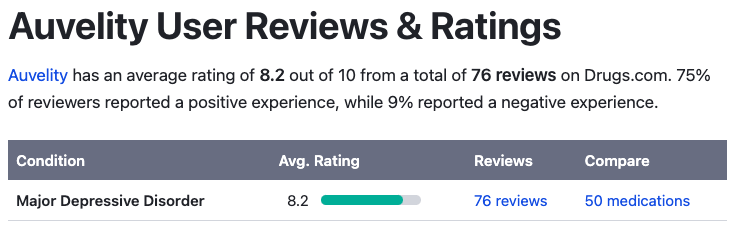

Drugs.com offers some insights into the user experience with Auvelity. The drug appears to be popular so far, although 76 reviews is a small sample size.

Drugs.com

For reference, Zoloft has an average rating of 7.2 (1,935 reviews).

Overall, Auvelity has had a successful first full year on the market, but Axsome, for better or worse, is far more complex than Auvelity. Axsome is still very much concerned with their long-term growth and figures to continue to incur significant investments in the near future.

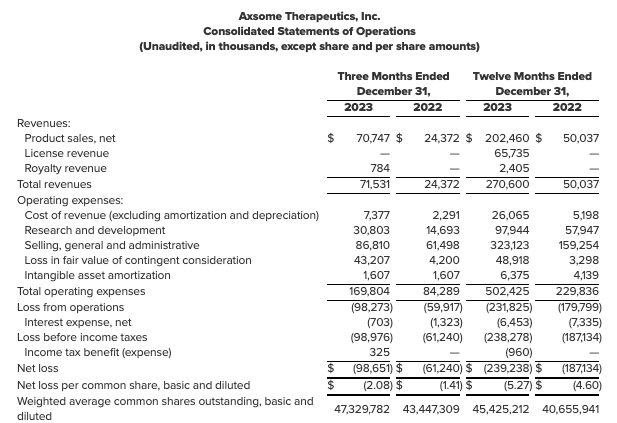

Taking a closer look at Axsome's most recent earnings report, Q4 and full-year 2023 total revenues surged to $71.5 million and $270.6 million, reflecting Y/Y growth of 193% and 441%, driven by Auvelity and Sunosi sales. However, operating expenses ballooned to $169.8 million in Q4 and $502.4 million annually, widening net losses. Notably, share dilution is evident with an increase in weighted average shares from 43.4 million to 47.3 million Y/Y, raising concerns about shareholder value erosion amidst growing expenses.

Turning to Axsome's balance sheet, the company's liquid assets include $386.2 million in cash and cash equivalents. The total current liabilities amount to $138.9 million, leading to a current ratio of approximately 2.78, indicating a robust ability to cover short-term obligations.

(In lieu of a cash flow statement at the time of writing, the net loss will be used to assess the cash runway.) The net loss for the year amounted to $239.2 million. Given this net loss, the monthly cash burn rate can be approximated at $19.9 million, leading to a cash runway of roughly 19.4 months. This estimate, however, relies on past data and may not reflect future performance accurately.

Considering the significant net loss and the existing cash runway, the odds of Axsome requiring additional financing within the next twelve months are medium, depending on its ability to manage expenses or generate revenue.

However, Axsome has guided that its "current cash is sufficient to fund anticipated operations into cash flow positivity, based on the current operating plan." As always, it's important to remember that there are different ways to estimate cash runway. I have provided a historical cash runway estimate, while the company, more familiar with the intricacies of their own business operations, has provided a forecasted cash runway estimate.

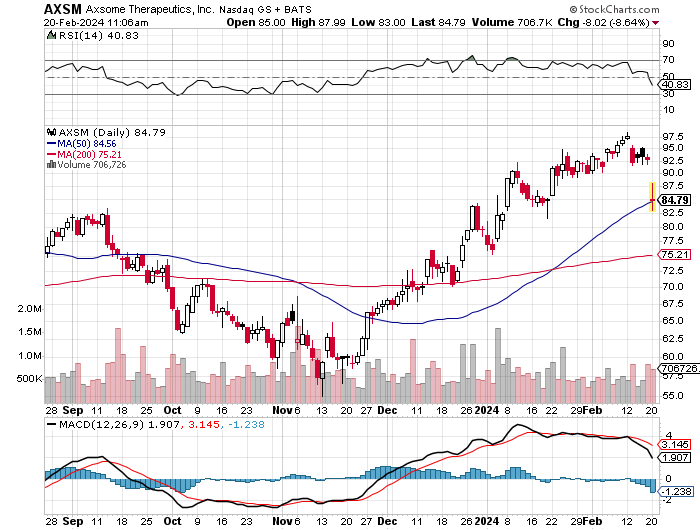

According to Seeking Alpha data, AXSM's market capitalization stands at $3.84 billion. Its growth prospects appear strong, with analyst projections pointing to a significant revenue increase from $268.17 million in FY2023 to $702.07 million by FY2025, highlighting a potential for substantial financial growth. The stock's momentum is outperforming the S&P 500 (SP500), especially notable over a 3-month (+55.43% vs. +11.03%) and 1-year (+44.95% vs. +22.37%) timeframe, suggesting robust investor confidence.

StockCharts.com

According to Fintel, short interest is remarkably high at 21.61% of the float, reflecting a significant bearish sentiment or speculative interest in potential downturns. Institutional ownership stands at 82.61%, with noteworthy movements such as Perceptive Advisors increasing their position by 556,370 shares, contrasting with Citadel Advisors reducing theirs by 206,539, indicating mixed institutional strategies. Insider activities over the past year exhibit a minor net sell of 29,588 shares, hinting at cautious optimism or routine portfolio adjustments among insiders.

Given these dynamics—impressive growth outlook, strong stock momentum against the S&P 500, substantial short interest, mixed but predominantly strong institutional ownership, and relatively stable insider activity — the market sentiment surrounding AXSM can be qualified as "robust."

In conclusion, Axsome has navigated a challenging landscape in the competitive depression market, as underscored by its Q4 earnings report. The continued revenue growth from Auvelity, alongside the strategic expansions into new indications, underscores a company on the move, albeit with significant operational risks ahead. The financial health of Axsome, characterized by a robust cash position against a backdrop of escalating operating expenses and net losses, suggests a precarious yet manageable financial trajectory. Investors should take note of the company's confidence in achieving cash flow positivity without further financing, underpinned by current projections. However, the looming specter of share dilution, high short interest, and the inherent uncertainties in drug development and market acceptance for new indications cannot be overlooked. To mitigate these risks, investors are encouraged to maintain a diversified portfolio, closely monitor Axsome's operational efficiency, and stay abreast of developments in the CNS drug market. Given the strong revenue growth and solid market sentiment, but balanced against financial and operational risks, a "hold" recommendation is still warranted for AXSM stock. This stance reflects a higher level of confidence in the company's direction post-Q4 earnings, yet it remains cautious of the hurdles that lie ahead.