Pratchaya

Pratchaya

The investment thesis around Aviat Networks (NASDAQ:AVNW) is the attractive valuation and better growth prospects. Traditionally, a company in decline, they have completely turned around and now sport an average revenue growth rate of 13.2% since 2021. This has been instrumental in driving positive operating leverage and below is why I think it will continue.

AVNW is a global supplier of microwave and wireless access networking solutions. They supply a range of wireless and access networking products to two primary customers, CSP's that include fixed telecommunication operators and private network operators.

On May 9th, AVNW bought NEC Corporation's Wireless Transport Business, now known as Pasolink for $45 million. Pasolink serves as a wireless communications solution, providing high-speed digital communication. The rationale behind the acquisition is to create a leading global wireless transport specialist with increased scale. I think the acquisition positions AVNW to further benefit from key drivers such as 5G, rural broadband and private networks, and they benefit from being highly complimentary businesses reducing costs.

Investor presentation

Furthermore, the combination of both companies effectively doubles AVNW's market share, allowing them to compete with larger industry players such as Ericsson. Due to previous collaborations between both companies, NEC products are already available on AVNW's order system and the deal has resulted in immediate cost synergies, while also being incremental to profit.

I think it is worth going into the financials here because it paints a good idea into the type of turn around this company has had in recent years. Up to 2021 the 10-years CAGR was -5% but due to their excellent market opportunities in Private Markets, Mobile Networks & 5G, and Rural Broadband sales have picked up notably.

The Communications Equipment industry is plagued by unprofitable companies, just under 50% of them are loss making, and the median EBIT Margin is just 2.5%. That being said, AVNW ranks 14th in the industry, with EBIT Margins over 8% and room for further upside.

Total Revenue & EBIT Margins (Seeking Alpha)

Free Cash Flow is not as strong. The company currently has negative Free Cash Flow numbers due to the working capital taken on from the acquisitions. However, in the years leading to the first Redline acquisition they sported 5% FCF Margins which rank 22nd in the industry with improving prospects going forward. I foresee a recovery here, as the company is forecasting longer-term EBITDA Margins of over 15%.

In my view, the Balance Sheet has weakened slightly after the acquisition. They drew down on a $50 million term loan to finance the deal, resulting in AVNW no longer having a net cash position with Net Debt to Sales of 4%. However, debt-to-equity still ranks below the industry median.

In Q2, revenues grew 4.8% despite lapping the effects of the Bharti Airtel order a year ago, driven by 6% growth in North America and 13.1% growth internationally. Gross Margins climbed 330 bps due to higher software revenue and a favorable project mix. However, EBIT Margins dipped due to the restructuring charges from the Pasolink acquisition, excluding the charges, non-GAAP operating income grew 10.9%. Finally, non-GAAP EPS grew 3.2% to $0.97 even with the additional 251,000 shares from the Pasolink acquisition.

In terms of guidance, AVNW raised guidance with revenues expected in the range of $425 and $432 which is growth of 23% accounting for the Pasolink acquisition. Adjusted EBITDA Margins are expected in, at 11.8%, down 200 bps on fiscal 2023.

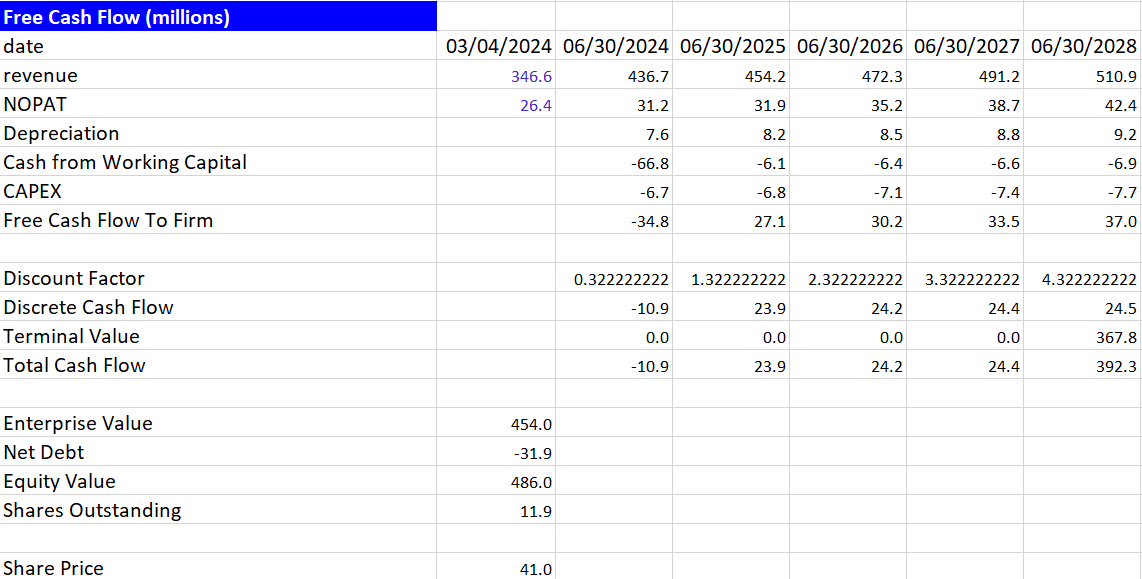

Source: Author's calculations

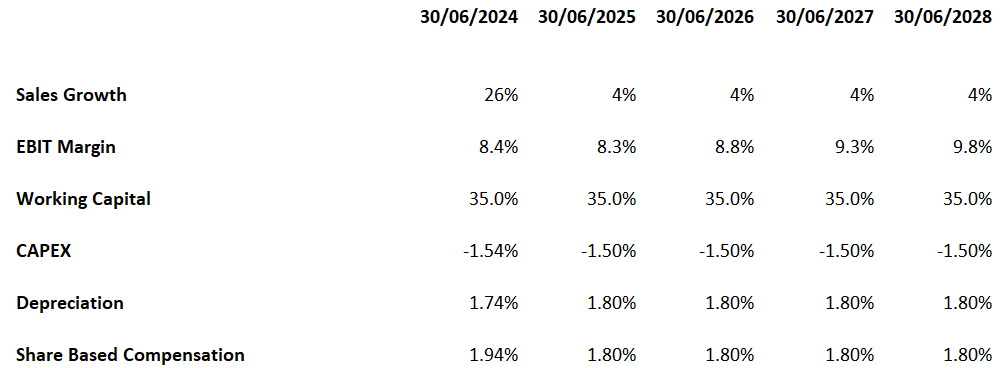

When valuing AVNW I have used a P/FCF multiple of 15x to get a share price target of $41 and an upside of 17% from today's price. I have sales growing 26% in the first year due to the NEC acquisition and then returning to the longer-term GDP growth rate of 4%, I believe this is conservative due to average organic growth of 12.7% over fiscal 2021 and 2022. I have EBIT Margins at 6.5% in 2024 and then growing to 8% by 2028, in line with company guidance of declining EBIT Margins due to the increasing integration costs, but longer-term outlook of 15% Adjusted EBITDA Margins. Finally, I have increased working capital to allow for the extra Accounts Receivable and Inventories after the acquisition.

Source: Author's calculations

If growth can stay above 8% that would be ground to use a higher multiple, something like 18x and that produces a share price target of $47.

The American Rescue Plan Act was signed into law on March 2021. Aimed at providing economic stimulus payments to individuals and allocating funds for critical areas such as infrastructure. Total allocated funds came to $1.9 trillion, with over $375 billion being designated to infrastructure related spending. A lot of the impact of APRA depends on AVNW's ability to leverage the relevant funding, but with a deadline of 2026, there is a significant short-term tailwind for the company going forward. In the longer-term, the company has the Infrastructure Investment and Jobs Act (BIL). Enacted to provide funding for long-term infrastructure jobs to address critical areas across the US economy, one of those areas being improvements in broadband and expanding high-speed internet access. In contrast, the BIL has no deadline, allowing for continued investment in the longer-term, that should allow AVNW to win business and keep investing.

I think AVNW will continue to benefit in the long-term growth of private networks, 5G rollout and the expansion of rural broadband. In Private Networks, I think demand will remain strong, which is important because it represents 50% of revenues, driven by the continued work on the large-scale statewide networks and the American Rescue Plan Act. As companies receive funds from the ARPA, I see a strong private network spending environment as the funds allocated by ARPA need to be used by 2026. In Rural Broadband, AVNW had record sales in the first half of fiscal 2024 from the Aviat store. I believe this is a good indication of healthy demand and expect it to remain strong in the quarters ahead. Finally, I think developing nation 5G spend is in front of AVNW, and they are well diversified, protecting the company against any slowdown in one country or region.

The main risk here is analyst's estimates of 2025 revenues. Growth is expected to be above 20% again and I can't see the company achieving this without another acquisition. So be aware that estimates might drop substantially, but I have that modelled into the valuation and there is still considerable upside.

I believe AVNW is on a promising trajectory. The company has previous years of strong organic growth, and the acquisitions allow AVNW to compete with bigger players in the industry. Despite a slight weakening of the Balance Sheet, debt remains at low levels relative to the industry and I think Free Cash Flow Margins could reach 7% by 2028. Furthermore, with funds being distributed for the ARPA, and with them needed to be utilized by 2026, I see a robust environment for private network that the company is now even better positioned for.