pcess609

pcess609

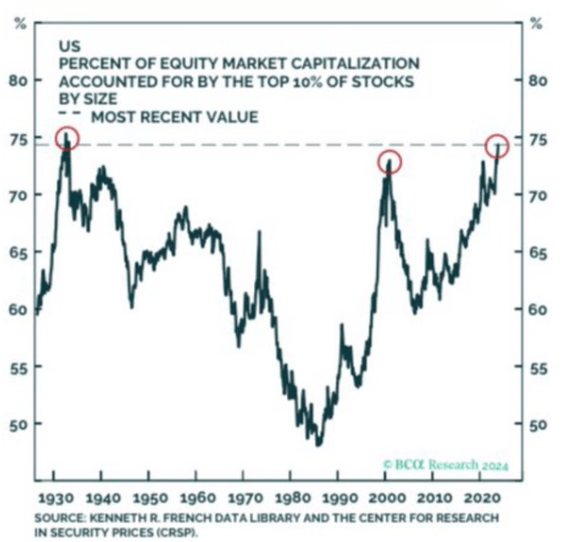

When the markets are experiencing euphoria, a retail investor should look at how to cut high beta investments rather than think about missing out on further gains. It now seems that semiconductors stocks are unstoppable, with new highs established every day. From market chatter, it looks like investors no longer look at fundamentals in this sub-sector, but are loath to miss out when they see others posting eye-watering gains on the respective names. While nobody can predict the future, history often repeats itself, and we are entering oddly familiar territory:

Concentration (KR French Data)

We are not calling for a market crash here, we just think history has a way of mirroring itself over long periods of time, just like it has in the rates space. We wrote a piece on the iShares 20+ Year Treasury Bond ETF (TLT) here, where we outlined the historic parallels for the current rates cycle, and our view regarding Fed actions based on those patterns. They have held up very well so far.

Despite some investors' views that 'this time it is different', the crude reality is that it is not. While artificial intelligence is the main driver behind the current exuberance, it represents just a factor. We have seen the same factors in the past, just under different names (Nifty Fifty, anything with *.com in their name).

In this article we are going to revisit the Advent Claymore Convertible Securities & Income Fund (NYSE:AVK), a name which we covered more than a year ago here. The vehicle is a closed end fund focused on high yield and convertible securities, and represents a high beta name in an investor's portfolio.

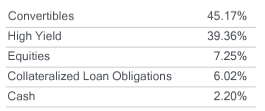

The fund contains a high equity delta, but also utilizes high yield for cash-flows:

Portfolio (Fund Fact Sheet)

The current composition utilizes convertibles and outright equities for the equity delta risk factor, while the high yield and CLO sleeves are used to support the dividend.

We have gone into detail in respect to convertible bonds in our initial coverage of the name, but a retail investor needs to understand that convertible bonds have equities as their main risk factor, followed by rates:

Holdings (Fund Fact Sheet)

The above table represents the fund's top holdings, where we can find a number of very large well-known names. Let us take Ford as an example to highlight the risk factors for convertibles:

DEARBORN, Mich., March 17, 2021 - Ford Motor Company today announced the pricing of $2.0 billion aggregate principal amount of 0% convertible senior notes due 2026 in a private placement to qualified institutional buyers pursuant to Rule 144A under the Securities Act of 1933. The initial conversion rate for the notes is 57.1886 shares of Ford's common stock per $1,000 principal amount of notes (which is equivalent to an initial conversion price of approximately $17.49 per share). Prior to the close of business on the business day immediately preceding Dec. 15, 2025, the notes will be convertible at the option of the noteholders only upon the satisfaction of specified conditions and during certain periods as set forth in the indenture for the notes.

The 2026 notes do not pay any interest, and are convertible at a price of $17.49 share. Given their lack of any interest cash-flow whatsoever, the main risk resides with the principal portion which is driven by Ford's (F) share price.

The fund does best in a cyclical bull market with low rates, like the one experienced in 2020/2021.

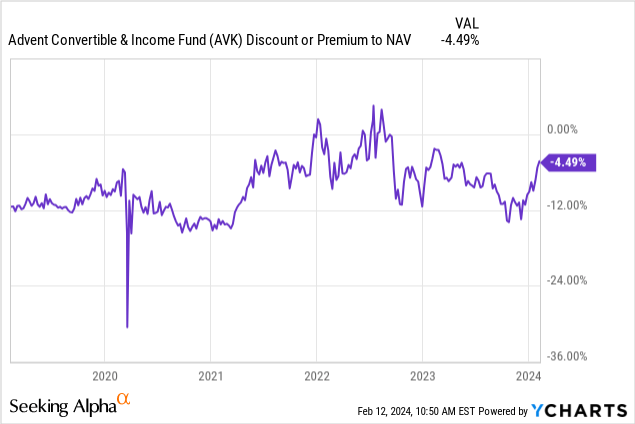

AVK is a CEF that has always traded at a discount in the past years:

The CEF usually sports a -10% to -12% discount, which only narrowed to flat to NAV on the back of the zero rates environment in 2021. This is a CEF which is very much tradable based on its discount, given its high beta.

The discount is now closing in on flat to NAV, given the overall risk-on mode in the market. Just like in the past, it won't last. We are penciling in a mean reversion in the discount during the next risk-off move, hence a -6% change on this risk factor.

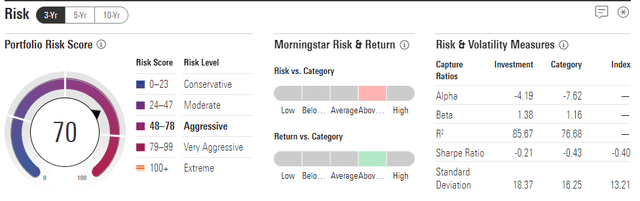

Beta is a cornerstone of portfolio management, and references the riskiness of a particular security:

Beta (β) is a measure of the volatility-or systematic risk-of a security or portfolio compared to the market as a whole (usually the S&P 500).

There are a number of sites which show beta, but we prefer Morningstar for CEFs:

Beta (Morningstar)

We can see the CEF with a very high beta of 1.38 in the above table. A beta of 1 means the security is following the market in lock-step, while a sub 1 beta means the underlying name is less volatile than the overall market. Conversely, high beta names exhibit a significant amount of volatility.

Morningstar has also recently introduced a portfolio risk score which they describe as follows:

MPRS measures the overall risk of a managed investment's portfolio. MPRS uses Morningstar Risk Model's holdings-based analysis to derive a risk estimate and score, and Morningstar's multi-asset Target Allocation Indexes to define the risk ranges.

AVK falls in the 'Aggressive' category, given its high beta and standard deviation. This will translate into the CEF exhibiting outsized moves versus the market, hence a risk-off mode will see a violent sell-off in the name.

The fund has a very high leverage ratio, which is partially responsible for the high beta:

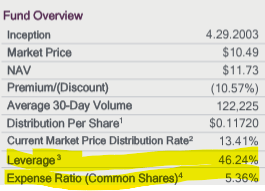

Leverage (Fact Sheet)

Currently the leverage ratio stands at 46%, with the associated expense ratio being very high given elevated SOFR levels.

Highly leveraged instruments are closely correlated with beta, with more leverage implying a high beta factor. Traditionally hedge funds were the first to use leverage to boost returns, but the feature has extended in time through the entire investment universe, retail investors now having access to it via CEFs such as AVK. Leverage is a high risk/high reward endeavor, and can really detract from performance during sell-offs.

AVK is a convertibles/high yield CEF with a high leverage ratio and beta factor. The fund has equities as its main risk factor, followed by credit spreads. The vehicle does best in a cyclical bull market with low rates, and we have seen it outperform during 2020/2021. The CEF has seen its discount to NAV narrow towards the top of its historic range on the back of the current risk-on environment, a level which we think will mean revert.

With significant euphoria in the market currently, we think we are due for a pull-back, with high beta names such as AVK set to sell off the most. The fund is extended from a discount to NAV perspective, and in our opinion a retail investor would do well to trim exposure to this highly leveraged name at this stage. We are a Sell at the current price-point.