guvendemir

guvendemir

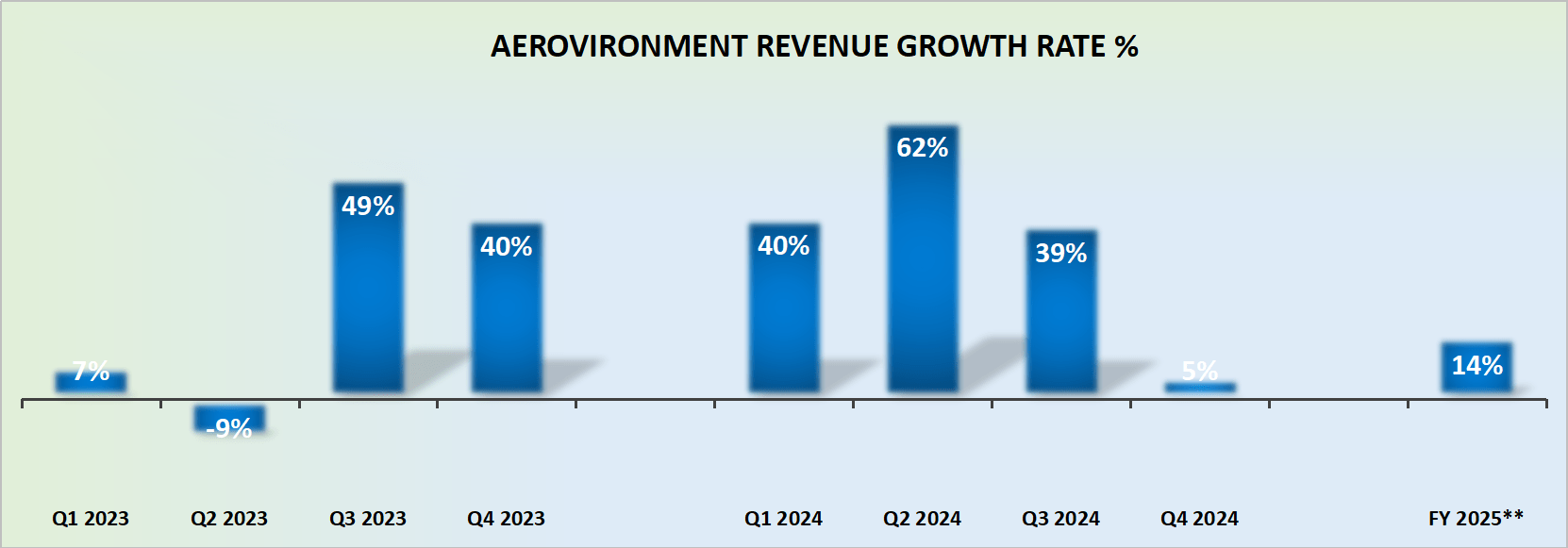

AeroVironment, Inc. (NASDAQ:AVAV) continues to delight investors with its three consecutive guidance raises this fiscal year. As we look ahead, management now guides for approximately 14% CAGR for the next fiscal year.

This investment thesis is not blemish-free, as you'll soon see. But according to my estimates, the stock is priced at 49x forward non-GAAP EPS, which strikes me as a reasonable entry point for investors.

AeroVironment specializes in creating advanced unmanned systems for defense purposes. They design and manufacture high-tech drones used by military and defense agencies.

AeroVironment's fiscal Q3 2024 results saw a record-breaking third-quarter revenue of $186.6 million (up 39% y/y), demonstrating its ability to capitalize on increasing demand for unmanned solutions.

Its Loitering Munition segment, in particular, more than doubled its revenue y/y, reaching $58 million. This surge is attributed to higher global demand and emerging programs of record, notably the Switchblade, which is in active negotiations with the U.S. government for a large multiyear sole source IDIQ contract.

Furthermore, AeroVironment's diversified portfolio, including Unmanned Systems and MacCready Works segments, contributed to the overall growth, with revenue for Unmanned Systems rising by 23% to approximately $113 million. The company is targeting multiple $1 billion programs and emerging unmanned solutions markets, positioning it for sustained double-digit revenue growth in fiscal year 2025.

However, despite these promising prospects, AeroVironment also faces headwinds. One of the primary challenges is the impact of delays related to the U.S. federal budget approval process. The company's MacCready Works segment experienced a slight decline in revenue due to program delays associated with the continuing resolution, resulting in reduced customer-funded R&D.

Moreover, fluctuations in working capital together with potential delays in government funding approvals may present short-term headwinds for AeroVironment.

Given this background, let's now discuss its fundamentals.

AVAV revenue growth rates

There's good news and bad news when it comes to AVAV's revenue growth rates. The bad news is that its growth rates are erratic and difficult to predict. Case in point, the first 9 months of fiscal 2024 saw AeroVironment deliver more than 40% CAGR, a terrific performance. Now, its guidance for fiscal Q4 is expected to be up a paltry 5% y/y.

Meanwhile, for fiscal Q3 2024, its funded backlog is up 9% y/y to $463 million, which is a deceleration from 26% y/y delivered in the previous quarter, fiscal Q2 2024.

This is not bad, in and of itself, but it does illustrate my contention that it's challenging to get a firm grasp on what AeroVironment's underlying growth rates could stabilize at in the near term.

Naturally, management is aware of investors' trepidation on this matter and sought to get ahead of any concerns by providing early guidance for fiscal 2025, which points to perhaps around 14% y/y CAGR.

This means that not only will AeroVironment exit fiscal 2024 with record revenues, but that looking ahead, there's still more good news to come. And on top of that, keep in mind that AeroVironment hasn't even started fiscal 2025, which begins in May of this year.

This means that there's even more scope for AeroVironment to raise this guidance further so that by the time fiscal 2025 is completed it could be higher by 20% y/y relative to fiscal 2024.

Given this context, let's now turn our focus to its valuation.

AeroVironment holds approximately $70 million of net cash. It has a stable balance sheet, but nothing out of the ordinary.

If we take AeroVironment's non-GAAP EPS guidance of $2.83 and presume that this figure grows by 20% y/y in fiscal 2025, this would leave the stock priced at 49x forward non-GAAP EPS.

This is a fair entry point for investors. It's not the cheapest of stocks, but it's far from shaking, too. And if AeroVironment were to be awarded one of its large programs in fiscal 2025, this valuation could become even cheaper than it appears right now.

In my view, AeroVironment offers an enticing investment proposition with three consecutive fiscal year guidance raises and a projected 14% CAGR for the upcoming fiscal year.

The recent fiscal Q3 2024 results, boasting a record-breaking $186.6 million in revenue up 39% y/y, demonstrate its financial strength.

Despite short-term challenges tied to budget delays, AVAV's stable balance sheet, backed by approximately $70 million in net cash, positions it well for the year ahead.

The current valuation at 49x forward non-GAAP EPS appears reasonable, presenting a fair entry point for investors. Anticipated fiscal 2025 growth adds to the optimism, making AeroVironment a financially sound and promising investment.