Scharfsinn86

Scharfsinn86

Based on my current outlook and analysis of Aurora Innovation, Inc. (NASDAQ:AUR), I recommend a buy rating. I believe AUR has a good chance to reach commercialization by the end of FY24, given the progress they have made so far in acquiring the required certifications, establishing partnerships, and getting commitments from potential customers. Assuming AUR were to trade at the same valuation that peers are trading today, based on FY27 revenue, I see an attractive upside to the stock.

AUR focuses on developing autonomous solutions (i.e., autonomous vehicles [AV]) for the transportation industry, specifically in the AV trucking market. AUR's business strategy is to partner with OEMs, fleet operators, and other third parties to commercialize its self-driving technology. As of today, the business is still in the research and development phase and is not generating any revenue. The balance sheet remains sound, exiting FY23 with ~$1.08 billion in net cash ($1.2 billion in gross cash).

Briefly touching on the 4Q23 results since it was released last week, AUR reported total OPEX of $198 million, a deceleration from the previous quarter of $207 million. On a cash basis, 4Q23 cash burn was $155 million after adjusting for stock-based compensation, depreciation, and amortization [D&A]. This puts AUR in a rather comfortable position from a balance sheet perspective, as the annual cash burn rate is around $600 million, which is easily covered by AUR's balance sheet for the next 2 years if the burn rate stays the same. On cash burn expectations, management guided a quarterly cash burn of ~$175 to $185 million on average in FY24.

I view AUR stock via a pragmatic lens, where I ask the question: when will AUR start to generate profits?

To answer this question, I have tracked the progress of AUR so far. Management is committed to completing the remaining Autonomy Readiness Measure [ARM] in order to enable Commercial Launch by the end of FY24, and they have reaffirmed their target for a commercial launch by the end of 2024. To be honest, based on how AUR has been executing, I believe there is a good chance for them to achieve the 2H25 timeline. On the progress in ARM, which I see as a major "test" of safety as it is a weighted measure of completeness across all claims of the Safety Case for the launch lane, AUR is already close to completing it as their results were up 900bps to 93% in mid-January 2024, vs 84% in 3Q23, this is within the timeline that management guided for last quarter where they had expected to achieve 95% of the ARM by end of 1Q24. Going forward, it appears that AUR is on pace to reach 100% ARM readiness by 1H24. Management has mentioned that they are collaborating with the truck platform to close the last 7% of the Safety Case, which will allow the launch at the end of this year on the last autonomy-enabled truck platform they anticipate receiving.

From an operational standpoint, AUR is also making encouraging progress by meeting its guided targets, in addition to certifications. With over 25,000 weekly commercial miles logged, AUR was able to autonomously haul 100 loads for its customers in 4Q23. As of 1/31/24, AUR has accumulated over 1 million commercial miles and autonomously delivered 4,300 loads (under supervision). This achievement, in my opinion, is more crucial than the ARM development since it provides AUR with a real data set to refine the product and make it launch-ready. To give you a perspective on how massive 1 million commercial miles is, trucker drivers typically only reach 1 million years after 8 years, and that distance is two trips to the moon and back. Notably, according to comments made by management, AUR accomplished all of this while maintaining nearly perfect on-time performance for its pilot customers, which included FedEx, Werner, Schneider, and Uber Freight.

Cumulative to date through January 31, we've autonomously delivered under the supervision of vehicle operators 4300 loads, driving more than a million commercial miles with nearly 100% on time performance for our pilot customers, including FedEx, Werner, Schneider, Hirschbach and Uber Freight among others. 4Q23 call

The last part of the commercialization plan-distribution-is something that I pay close attention to as well. Again, it was encouraging to learn that AUR is making strong progress in this area. Currently, AUR is in partnership with PACCAR and Volvo Trucks for trucks and with Continental for hardware kit manufacturing (i.e., hardware as a service).

Regarding the partnership with Volvo, during 4Q23, AUR successfully brought up the first Volvo trucks that were fully equipped for autonomous operation. In January, they started track-testing these trucks for autonomy. Plus, last month Volvo Trucks made public their Volvo VNL, the foundation for Volvo Autonomous Solutions' [VAS] Aurora driver-powered autonomous trucking product. As for PACCAR, a new fleet of PACCAR Peterbilt 579 trucks, equipped with the most recent generation of the commercial launch-ready Aurora Driver hardware kit, is progressing well in the buildup as well. The key takeaway from these two is that AUR is already helping its partners develop products for commercial use. I believe this suggests that the partners already know it is going to work-if not, why spend all the resources developing it?-and once AUR acquires the necessary certifications, the commercialization plan should not see any challenges from a product distribution perspective. Not only did AUR make strong commercial progress with these two partners, but it has also secured volume and pricing commitments for some of its capacity in 2024 and 2025, as well as a mechanism to transition to driverless operations, and a number of other contracts are almost ready to be executed.

Regarding Continental, AUR and Continental have an exclusive, long-term partnership to work together on the design, production, and support of Aurora Driver hardware upgrades. The next generation of Aurora Driver hardware, which will include a new backup system, has been finalized, according to a recent press release by Continental and AUR. Production of this hardware is scheduled to begin in 2027 by Continental. I like this partnership as it lightens the burden on the AUR balance sheet to spend on more research and development, pulling away resources from their core product. With the partnership model, Aurora will pay for the hardware based on the number of miles it covers. With this model, AUR could compete with conventional trucks in terms of price, with the cost of their autonomous trucks being comparable to that of conventional trucks.

That means we expect the cost to the customer to purchase an autonomous truck will be relatively in line with that of a traditional truck, thereby limiting the capital investment necessary to adopt autonomy in their operations. 4Q23 call

AUR

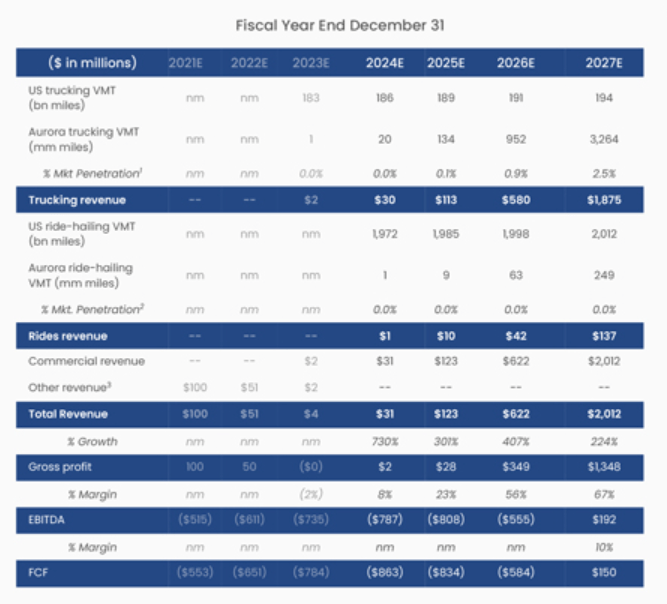

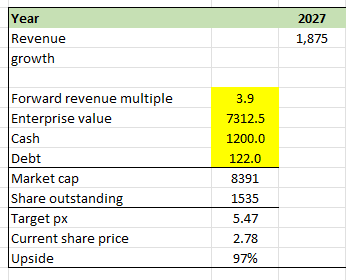

Given that AUR is not generating any revenue or profits today, the only possible way to maximize the upside is through management guidance. In the SPAC presentation, management guided for FY27 total revenue of $2 billion and EBITDA of $192 million. Based on AUR's current EV of $3.2 billion, the market is assuming AUR to trade at ~1.6x FY27 revenue, which is way lower than where peers are trading. My take on why this is the case is because AUR is not generating any revenue today, and it is still uncertain if they can actually reach commercialization by the end of this year, hence the discount. However, assuming it does take off, I believe the upside could be attractive if the market simply re-rates AUR to Lucid Group's (LCID) multiple of 3.9x. At 3.9x, this implies a FY27 share price of $5.47, ~100% upside.

Author's work Author's work

The risk of investing in AUR today is that they fail to achieve the necessary certifications (ARM, for instance), which leads to a delay in the commercialization plan. This will put a major dent in management creditability. Also, if any of the key partners were to stop the relationship, it would send a very big signal to the market that the underlying product might not be working as well as it should.

I recommend a buy rating for AUR. AUR should achieve ARM by the end of FY24, which coupled with strong operational achievements and partnerships, positions it well for the commercialization phase. AUR also has a robust balance sheet that reduces the risk of requiring additional capital injection. Assuming successful commercialization, I believe there is a significant upside potential, with a possible 100% increase based on peers' valuation multiples.