iQoncept

iQoncept

Aurinia Pharma (NASDAQ:AUPH) had been conducting a strategic review since June 2023. It turns out discussions didn't lead anywhere and the strategic review is complete. I rated AUPH a hold when I last wrote about it, noting the buyout thesis would be stronger if AUPH could produce a little more sales growth. Now the buyout thesis seems more or less dead. This article takes a look at where AUPH stands now.

AUPH had been conducting a strategic review, which as recently as January was still continuing. Unfortunately, with Q4'23 earnings we found out the review had concluded, and didn't result in a formal offer.

The Board initiated a robust strategic review at the end of June 2023 to review all strategic options for the Company. Together with management, JP Morgan, the Company’s financial advisor in the strategic review process, engaged with more than 60 parties, receiving only one non-binding expression of interest, which included a due diligence process, but did not result in a formal offer.

AUPH Q4'23 earnings press release, February 15, 2024.

The company also disclosed that under previous management, back in 2018 there had been another strategic review, that also didn't result in a formal offer, just a non-binding expression of interest and a due diligence process. There is nothing bullish about the fact that no one made a formal offer, in my opinion. All I can say is that if there were renewed sales growth, of course AUPH might have a chance of selling the company.

Another development I don't find bullish comes from another paragraph in the Q4'23 earnings press release.

Aurinia also explored potentially acquiring or licensing other entities or assets during this time. After assessing a range of alternatives over the last seven months, the Board elected to conclude Aurinia’s strategic review process. The Board ultimately determined that none of the explored opportunities that were available to it to pursue were in the best near-term interests of the Company to execute on, and that the best path forward is for management to streamline its operations as it announced today and focus on the Company’s commercial execution.

AUPH Q4'23 earnings press release, February 15, 2024.

The strategic review ran from June 2023 to January/February 2024, at a time where many biotechs were trading below cash, others were low on cash, trading at depressed valuations, but unable to raise the funds they needed. Despite that, the company couldn't find anything available to acquire or in-license that would be in the interest of the company? That does not inspire confidence in the company for me. AUPH's earnings call confirmed that acquisitions in the future are possible, but if they couldn't find a good deal in a beaten down biotech market, how would they do that now given biotech has rallied?

With Q4'23 earnings, AUPH has also noted it is discontinuing its development of AUR200 and AUR300, which had been its two developmental pipeline members. As recently as December 2023, the company had filed an Investigational New Drug (IND) application for AUR200 to enter the clinic. AUPH did note this change and prioritization of resource allocation would result in a one time charge in Q1'24 of $11M-$15M but savings of $50M-$55M a year. The savings are bullish in terms of pushing towards cash flow positivity, although AUPH does have a plan for its funds.

Of course, if you're ceasing development of two drugs in the pipeline, not acquiring on in-licensing anything from anyone else, you can buy back your own stock. I'm pretty cynical about this, in terms of the long term prospects of the company.

If investors just want the company to do what makes sense in terms of shareholder value, so if AUR200 and AUR300 aren't that, then fine, cease development. I have to wonder what changed though, since they filed an IND for AUR200 in December. I hope to see the company develop Lupkynis for other indications, or develop something else, but in the meantime it looks like they're going to focus on selling Lupkynis.

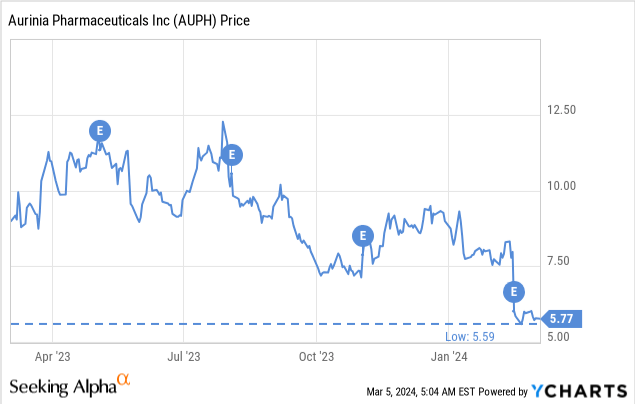

The buyback is for up to $150M worth of the company's common stock, pending the grant of exemptive relief from the Canadian securities regulators, that would allow AUPH to purchase up to 15% of the company stock in any 12-month period for 36 months. The approval of this application for exemptive relief is thus a potential near-term catalyst for AUPH, as otherwise the company could only buy back 5% of the company's stock. AUPH notes this 5% would be 7,230,888 shares. I note this is about $41.6M worth of stock, at $5.76 per share. Of course, if the stock ran up as AUPH bought in and the weighted average of the purchases ended up being, say $6, then this would be $43.4M of stock.

AUPH had net product revenue of $42.3M in Q4'23, and reaffirmed its 2024 guidance for net product revenue of $200M-$220M. Total net revenue was $45.1M in Q4'23. R&D expense was $10.2M in Q4'23 and SG&A expense was $50.1M in the same quarter. Net loss was $26.9M in Q4'23 and net cash used in operating activities was $33.5M in 2023. AUPH had cash, cash equivalents, restricted cash and investments of $350.7M at year-end 2023. Restricted cash was $0.12M at year-end 2023, so taking that out, and considering AUPH's net cash used in operating activities, the company could continue on for 10 years at the current rate without raising cash. Indeed, AUPH thinks it can fund its operations "for at least the next few years," according to its Q4'23 earnings press release. Further, the company talks about generating free cash flow by the end of 2024. That certainly sounds achievable due to the cost savings from streamlining its operations, although it will depend on how AUPH grows its revenues and how much it spends on the buyback.

As of February 14, 2024, there were 144,617,762 shares of AUPH's common stock outstanding. AUPH has a market cap of $833M ($5.76 per share). As of December 31, 2023, there were 11.56M stock options outstanding under the employee stock option plan with a weighted-average exercise price of $10.63. There were also 921K unvested performance awards and 6.89M unvested restricted stock units as of December 31, 2023.

There's nothing bullish, in my opinion, about ceasing development of a pipeline that you were incurring expenses on as recently as last quarter (such as with the IND filing for AUR200). Nor is there anything too exciting about the company finding no new assets available that they thought were worth acquiring.

On the other hand, while sales of Lupkynis have been flat for a few quarters, continuing to focus on selling the drug could drive new sales. Indeed, seasonality may have played a role in middling Q4'23 numbers.

Further, I don't find buying back stock isn't impressive from a business development perspective or a scientific perspective, but it does mean the share price could have support at low levels. Also, the 28% dip in the stock since my last article means the company now trades at a cheaper valuation, with revenue growth a real possibility. As such while I'm not that excited about the buyback, ditching AUR200/AUR300, and the strategic review turning up nothing, AUPH isn't at a terribly rich valuation and the possibility of sales growth is well intact. Overall then, I rate AUPH a hold, but I'd certainly consider rating it a buy if Q1'24 sales numbers impress.

There are risks to holding AUPH here, a few of which I'll mention. Firstly, if AUPH isn't granted exemptive relief to buyback up to 15% of its stock, then the stock could fall as the market knows AUPH's ability to support the share price is compromised. Secondly, if AUPH doesn't report strong sales numbers in Q1'24, it will look like a company with one drug that isn't growing, and no pipeline to look to for excitement. Lastly, AUPH is open to competition in Lupus Nephritis, I noted in my previous article that there are trials of other drugs underway. If AUPH is focusing of Lupkynis, it is a one drug company with nothing in the pipeline and so, with all its revenues coming from that drug for the foreseeable future, competition is certainly something to watch out for.