SOPA Images/LightRocket via Getty Images

SOPA Images/LightRocket via Getty Images![]()

Autohome (NYSE:ATHM) still remains a strong player in the automobile industry, despite recent macroeconomic headwinds that have brought the stock price down to relative lows. Despite lower ad spending, high unemployment among China's youth, and an uncertain regulatory environment, I believe Autohome still has a large role to play in facilitating China's automobile market. The company can leverage AI and machine learning to further improve the facilitation of automobile transactions on their platform, and the Chinese government's support of the NEV industry creates potential upside for the business. I think shares present a long-term buying opportunity to those who can wait out the economic fears and slowdowns.

Autohome operates a diverse business model that caters to several stakeholders in the Chinese automobile industry, ranging from car manufacturers, consumers, dealers, and advertisers. Investors may want to think of it as an online platform for all things regarding vehicles. They have professionally produced content that keeps consumers informed about news, models, prices, and other updates about their favorite cars. An extensive library of data, specs, vehicle parts, and comparisons to give people an exhaustive analysis of all kinds of automobiles. They also have new and used car listings so people can shop for the best prices and determine what vehicle fits their need.

autohome.com.cn

In my opinion, an online platform like this still holds tremendous value in China as younger generations are more attracted to the convenience, market data, and research they can do on a website like this. Far from being obsolete, I think Autohome represents the new future of how people will buy and sell cars in China.

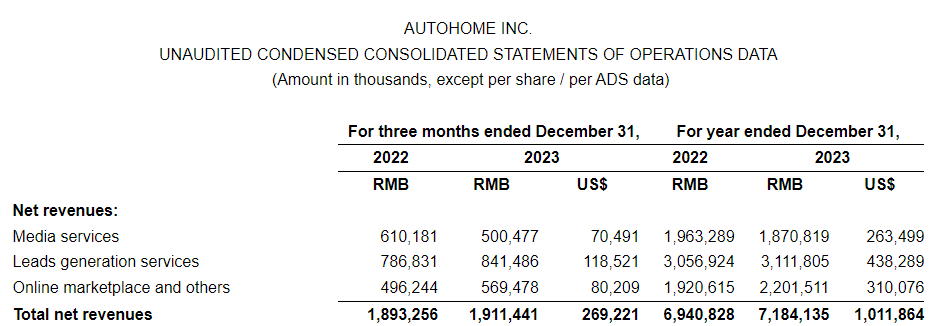

The company's revenues are split up into three segments: Media services, leads generation services, and online marketplace and other revenues.

According to the annual report, "through our media services, we provide automakers with targeted-marketing solutions in connection with brand promotion, new model release and sales promotion. Our large and engaged user base of automobile consumers provides a broad reach for automakers' marketing messages." Media services represented 26% of total revenue in 2023 according to the recent press release.

Leads generation services "enable our dealer subscribers to create their own online stores, list pricing and promotional information, provide dealer contact information, place advertisements and manage customer relationships to help them reach a broad set of potential customers and effectively market their automobiles to consumers online and ultimately generate sales leads." For 2023, leads generation services represented 43% of total revenue.

Finally, the online marketplace and other revenues refers to "focus on providing facilitation services for new and used vehicles transactions and other platform-based services for new and used car buyers and sellers." These services include auto financing, insurance, offering data analytics services to dealers, and inspection services. For 2023, online marketplace and other revenues made up the last 31% of revenue.

Q4 and Full Year Press Release

I believe the business has strong economics and characteristics that should allow the company to perform well long-term. First off, its network effect remains intact and can likely grow into the future. According to the investor fact sheet, 69 million mobile DAUs exist on the platform, and proves that Autohome holds the number one influence in the online auto marketplace with its comprehensive array of content. Because they are the leading online marketplace, they hold a strong dominant position because new auto consumers want to go to the largest site that has the most amount of content and value created. As more advertisers, dealers, users, and car experts fill the platform, the value created by Autohome trumps any other online marketplace from competitors.

The positive feedback loop still has a long runway to go, as 69 million users pales in comparison to the 250 million privately owned cars in China. The Chinese auto market is the world's largest by production, and Autohome still has untapped potential and can still grow to reach a larger younger audience in China who may be buying a car for the first time. Given the low penetration of automobiles in Chinese households of 51 cars per 100 households, assuming that number nears the US stat of 92 cars per 100 households, Autohome has significant long-term growth ahead of it.

Furthermore, the company has intangible assets, namely its proprietary data and high tech algorithms that allow it to efficiently match relevant stakeholders with each other. The company mentions in their annual report,

Leveraging the rich content and user data on our platform and our advanced AI and data technologies, we have developed a portfolio of intelligent tools to facilitate our users' potential vehicle purchases. For example, AskBob is a smart assistant tool empowered and enhanced by our rich data and unique algorithms and can generate customized purchase reports for users on the basis of each user's browsing records and other data."

This data cannot be replicated by competitors, as it is unique to only Autohome. Because Autohome has all the historical transactions, user data, market listings, and automobile specifications all one platform, they can become the most accurate and intelligent market platform that provides the best value to all stakeholders. Advertisers have all the data to create well-tailored, personalized ads to specific buyers. Consumers have all the market data and comparisons to make the best purchases. And, dealers have strong data as to what the car market is doing and how they should position themselves strategically. All in all, the technology that Autohome deploys is one of a kind and cannot be matched because Autohome has all the proprietary data that other platforms simply don't have.

Finally, the brand value that Autohome has allows people to trust the credibility and transactions that happen on the platform. No one wants to go on some shady website with no track record, as buying an automobile is a major high-ticket purchase. So, new entrants suffer high barriers to entry as nobody will trust them over the established, safe, and already existing Autohome. The brand serves as a trust factor, so that new buyers go to the place that is already working and has historical success for people.

As AI begins to take over our world, management has been using AI to create a more secure and efficient platform to facilitate its online auto marketplace. In the Q4 earnings call management says,

In 2023, we made breakthroughs in the application of AI and large language models and innovative new business model. We launched new AI-driven data products, deployed large language models in various business scenarios, and combined model-based decision-making with human expertise to enhance the service quality of our data products.

We also introduced applications based on large language models such as AITC and Operation Butlerhelping our dealer customer reduce overall cost and increase efficiency.

We launched products such as cloud smart selection and [indiscernible] which leverages our AI technology and big data capabilities to help dealers engage with high value users and manage instant messages with users in different scenarios.

These snippets show that management is very innovative and is using AI in creative ways to unlock value for stakeholders. Basically, they can use AI and large language models to make the platform more efficient and faster in facilitating secure transactions of automobiles. For instance, AI can do faster and more accurate risk assessments to assess creditworthiness for auto loans. It can create personalized recommendations for auto consumers based on historical user data to see what cars they want to buy. And, it can detect fraud, create chatbots and virtual assistants, and compile vast amounts of market data to highlight unique insights for users.

Far from facing regulatory risk, it seems to me that Autohome may actually benefit from the Chinese government through policy support for new electric vehicles. Given Autohome's new focus on NEV market, and their large market presence in used cars, I feel that the Chinese government may be indirectly helping a business like Autohome generate more revenue and gain market share.

In recent years the Chinese government has spent $57 billion to support the purchase of electric vehicles between 2016 and 2022, which is 5x the US government spends. It also heavily subsidizes the production of EVs, and the market for EVs in China is expected to grow at 17.15% CAGR for the next 5 years. This remarkable growth may actually stimulate Autohome's business, as they are heavily involved in the NEV space, "We also saw robust growth in our NEV business with revenues for the year increasing by over 80% year-over-year and accounting for nearly 18% of total revenue" (Q4 Earnings Transcript).

Autohome is heavily involved in monetizing this growth in NEVs, by offering a dedicated platform for buyers of NEVs. This platform includes listings, specs, comparisons, reviews and ratings, and more. They have recently launched a new breakthrough plan for NEV as mentioned in their earnings call,

In the fourth quarter we launched NEV Breakthrough Plan, a comprehensive evaluation program that assesses NEV's safety across the three dimensions: collusion, battery and intelligent driving, this program which aims to address user concerns and accelerate the decision-making process has received 325 million impressions and over 200 million views across the entire network. Additionally, we launched NEV Super Test, a program which carries out real-world evaluation of NEV performance over a period of two months. This initiative give us the opportunity to collaborate with other parties on developing a more consumer-centric vehicle evaluation system, promoting the overall NEV category and helping automotive brands develop strong products with a better user experience.

While markets are aware of the growth opportunity for EVs in China, they completely forgot about Autohome, the company instrumental in distributing, advertising, and facilitating transactions to end users for NEVs. I believe the growth of NEVs in China supported by the Chinese government may actually help Autohome grow its business.

Starting with TTM revenues of $1 billion, I believe the business can grow sales year over year by 5%. Most of this growth can come from the NEV business, increasing willingness to pay up for electric vehicles, as well as the increasing urbanization of China. The shift away from gas-guzzling cars to low-carbon, electric vehicles is likely a huge tailwind for Autohome, and the business should grow accordingly. Assuming a net margin of 30%, which is in line with the five year average, the profits will be around $330 million by 2027. Divide $330 million by shares outstanding of 123 million is $2.7 EPS in 2027.

I believe a fair earnings multiple should be around 10x, which is fair given the high quality business Autohome is. They have a lot of secular tailwinds behind them, ranging from rapid NEV growth to innovations in AI that can help them achieve higher earnings growth. This 10x earnings multiple is under the 5 year average of 18x, giving me a margin of safety in my assumptions (2.7 x 10 = ~27).

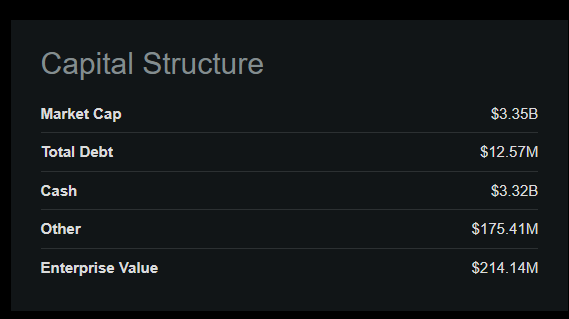

Then, I add net cash to my earnings based valuation to account for the entire capital structure. So, adding net cash of $27/share to my earnings based valuation of $27 gets me to a $54 fair value.

Seeking Alpha

Investors can see the mispricing easier if they account for the egregiously low EV/EBITDA ratio of ~1x, which is clearly a sign of undervaluation.

As a Chinese stock, the risks are the usual suspects. Government regulations could at any moment punish Chinese tech companies for monopolistic behavior. Although, it is worthy of mentioning Autohome has not received any fines, fees, or punishments from the PRC as of recently. I have searched high and low and have not found any punishment or penalty, so it seems unlikely that the Chinese government will ferociously attack Autohome out of nowhere. As far as I'm concerned, they are pleased with Autohome's efforts to spread NEVs across their country to meet low carbon emission efforts.

Shifts in government policies could threaten the thesis as NEVs may lose their subsidies or favorable position in the Chinese government's eyes. It could be that the PRC pulls back subsidizes for NEVs, or they switch their policy in some way that somehow hurts Autohome.

High unemployment in China among their youth remains a major headwind, as China's youth are most likely the ones buying new electric cars in China's economy. If China's new graduates don't have jobs, they obviously can't buy cars. So the economic slowdown in China is rather tough, which could slow down the purchase of NEVs by China's new jobless graduates.

Furthermore, automobiles are pretty cyclical and may have up and down markets in terms of demand. Thus, Autohome may see swings in its revenues as advertisers, dealers, and consumers cut back on spending and facilitating the transactions of automobiles on their platform. The correlation between GDP and auto sales in China is extremely high, and a weak economy could lower consumer confidence and cause people to cut back on vehicle spending.

The real-estate collapse can also decimate China household wealth, leaving them feeling poorer and unwilling to spend their money on high-ticket items such as automobiles.

Finally, competition from other online auto marketplaces could take market share and gain traction to build a more recognized brand.

I believe Autohome has a strong business model with secular tailwinds behind it. It will likely remain relevant and gain traction with the explosive growth of NEVs in China. Furthermore, the business is trading close to net cash, so investors are getting a very good deal on their shares. Its high margins, strong competitive advantages, and long runway for growth are all being undervalued by the market. At ~1x EV/EBITDA, it is too cheap to ignore. Put simply, I think it's a great business at a cheap price.