Miragest/iStock via Getty Images

Miragest/iStock via Getty Images

Ardmore Shipping (NYSE:ASC) is a global shipping company specializing in the ownership and operation of product and chemical tankers. ASC owns a fleet of 22 midsize eco product tankers, complemented by an additional 4 vessels through charter agreements. In a recent development, ASC has successfully finalized the acquisition of a 2017-MR vessel for $42 million and divested its oldest MR vessel, constructed in 2010, for $27.1 million.

I have covered Ardmore Shipping previously, investors should view this as an update to the previous article on the company, where I did an extensive Business Overview reviewing the capital allocation policy, management past actions and why it was an attractive investment.

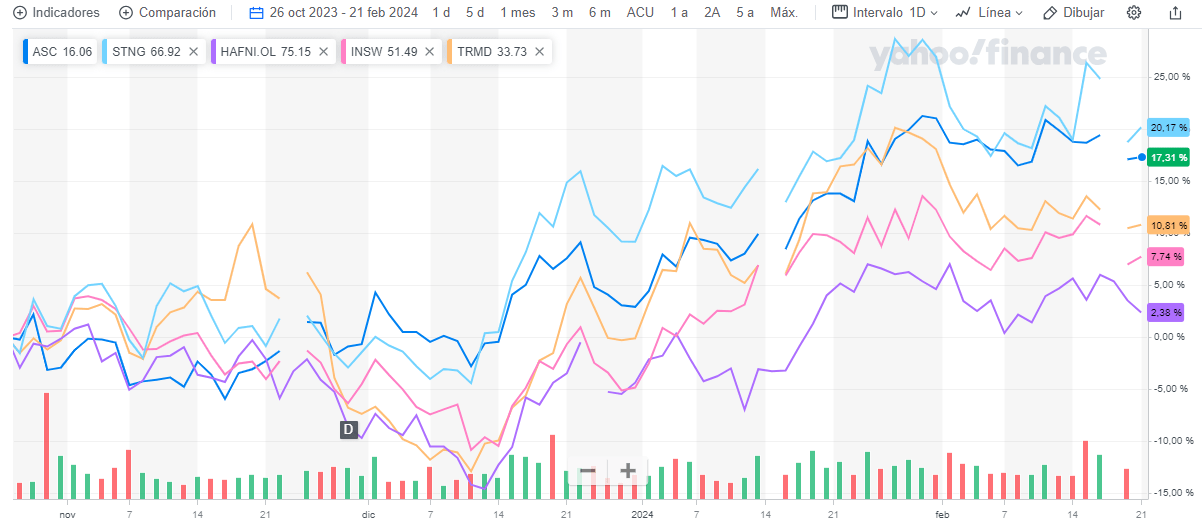

Indeed, the company has effectively closed the valuation gap, currently trading more in line with peers at approximately 0.85 times Net Asset Value (NAV), as illustrated in the valuation section. Furthermore, since the publication of the article, Ardmore Shipping stands as the second-best performer among product tanker companies.

Price evolution (Yahoo Finance)

In my previous article, I suggested three catalysts that could contribute to close the valuation gap:

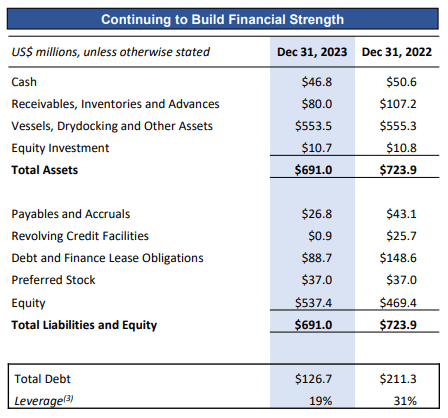

While the first two predictions proved accurate, I was wrong regarding the most important one for a long-term investment. In the latest Q4 results, the management reaffirmed their modest dividend policy despite having a nearly net cash position. As of December 31, 2023, Ardmore had $126.8 million in current assets (comprising cash and receivables) and $153.4 million in liabilities.

Balance Sheet (Ardmore Q4 Presentation)

Given the modest shareholder retribution program, which constitutes only 1/3 of the quarterly Earnings per Share (EPS), and considering that is trading in line or above certain peers, I decided to exit my long position. I have reallocated my investment into other opportunities, such as International Seaways (INSW) or d'Amico (OTCQX:DMCOF).

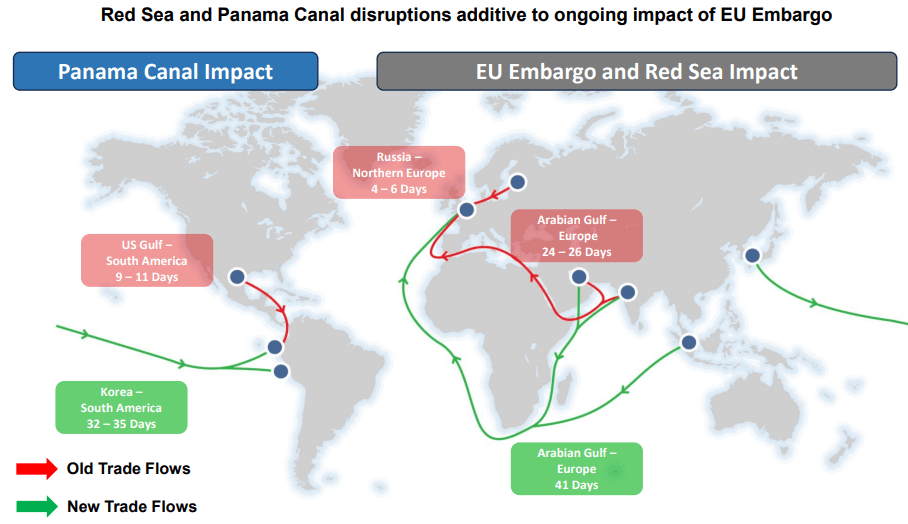

Following the release of the previous article, Houthi attacks on western vessels have resulted in a significant decrease in Suez Canal transits. Ardmore Q4 presentation has an extensive market outlook, where it can be seen that about 12% of all product tanker traffic typically moves through the Suez Canal, as Europe heavily depends on the Middle East for a significant portion of its consumption. According to Clarkson, there is a projected increase in global product tanker tonne-miles ranging from 6% to 12%.

Ardmore Q4 Presentation

To obtain those barrels, tankers now need to navigate around the Cape of Good Hope or consider alternative sources from America. Additionally, drought in Panama has resulted in a 40% reduction in product tankers transiting the Panama Canal. These disruptions have significantly extended average voyage lengths and increased demand for product tankers.

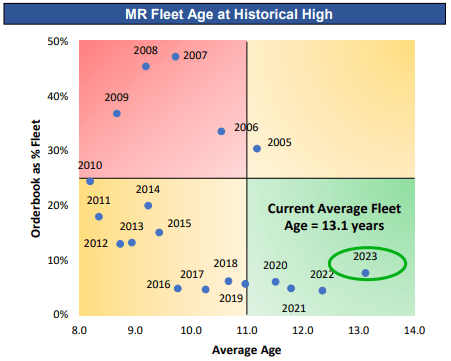

At the same time, the supply side is appealing, with the oldest MR fleet in history and a moderate order book at 7.7%. Looking ahead, in the next five years, around 47% of MR vessels will be older than 20 years.

Ardmore Q4 Presentation

In Q4, Ardmore reported adjusted earnings of $26.1 million, equivalent to $0.63 per share, with a fleet average TCE of $29.7k per day. Following their dividend policy, one-third of EPS, the company declared a $0.21 per share dividend, a 31% increase respect Q3. However, this increase was due to better results in Q4 and not to the improved dividend policy that I was expecting.

The Q1 guidance presents an outstanding outlook, projecting a fleet average TCE of $32.4k per day. Notably, 60% of MR vessels were booked at $35.4k per day, and 70% of chemical tankers were secured at $30.1k per day. For comparison, Scorpio Tankers (STNG), with a more modern fleet, fixed 59% of spot MR days at $34.5k per day, worst rates despite better fleet.

If those rates are sustained, Ardmore could potentially achieve around $1 EPS in Q1, implying a dividend of $0.33 per share and a low 8% yield. Taking in consideration that Ardmore will be net cash in Q1 and has a young fleet, if management had improved the dividend policy to 3/4 EPS, that would imply a 19% yield and a re-rate in stock valuation. However, with recent actions, this scenario is highly unlikely.

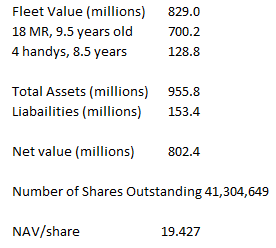

With Q4 figures and Arctic asset values, year-end NAV can be estimated easily:

NAV Calculation (Author)

Year end NAV, considering current asset values, stands at $19.4 per share, implying that the stock is currently trading at 0.85 times NAV. This aligns with the year end NAV projected in the previous article. This valuation is similar to peers trading between 0.8 and 0.9 times NAV as Scorpio Tankers, International Seaways, and d'Amico. I, personally, believe that the latter two are better managed and have a stronger alignment with shareholders than both Ardmore and Scorpio Tankers, which is why I have chosen to no longer maintain a long position in ASC.

Given current sentiment and lack of ceasefire in Gaza, there is a possibility for the stock to further reduce the valuation gap and trade around NAV. However, considering the existing shareholder returns and the apparent lack of interest in improvement, a discount of 15-20% to NAV is reasonable. This suggests that the stock is fully valued, and only modest returns should be expected if the strong sentiment persists.

While it's premature to provide an exact year-end NAV estimate for 2024, I expect it to be approximately $22.5 per share, applying a 15% discount to NAV, fair value would be $19 per share, a potential 15% upside.

Improved Shareholder Policy: Together with Q4 results, Ardmore did their investor day, where they reiterated their dividend policy. Given they already did the investors' day, I don't anticipate an immediate improvement in shareholder returns over the next few quarters, however there is a possibility that the company may consider issuing a special dividend, which could be well-received by the market. Moreover, if rates persist at current levels, Q1 dividend will be higher than Q4.

New disruptions: An increase in disruptions or congestion could lead to a tighter supply of vessels and higher rates.

Ceasefire in Gaza: While a temporary ceasefire doesn't mean the return of ships at the red sea, it will generate negative sentiment. Ceasefire rumors already reversed positive momentum, if a ceasefire is announced, share prices can experience a huge selloff.

Resumption of transit in Red Sea: Before tankers resume transits in the Red Sea, a permanent ceasefire should be agreed. If that happens, will reduce tanker demand to last year levels, resulting in lower base rates.

Desire to Grow: One of the four objectives of Ardmore capital allocation policy is "Well-Timed Accretive Growth". While management has primarily focused on fleet renewal, as proved by the 2017-MR acquisition and 2010-MR divestment, at some point they will start with fleet growth.

Ardmore Shipping has a solid financial position, ending 2023 with just $26.6 million in net debt and will be net cash in Q1. However, despite this strength and modern fleet, the company continues to ignore shareholders distributing just one-third of quarterly EPS and building an unnecessary cash position.

Ardmore has successfully closed the valuation gap and now trades around 0.85 times NAV, more in line with peers. Taking these factors into account, I've closed my position and downgraded the recommendation to hold, as stock potential appreciation is limited. I haven't downgraded it to sell because the stock isn't overvalued.

Q1 results will be outstanding and if rates remain strong NAV should continue trending higher. However, current risk/reward is less appealing than before, and other stocks have more potential. While the stock might continue to climb as long as the overall sentiment in the sector stays positive, it is no longer an interesting buy.