Pitris

Pitris

Array Technologies (NASDAQ:ARRY) is one of the leading investments in solar tracking technology. However, I consider the short-to-medium-term risks worth heavily weighing against the long-term prospects provided by solar market growth. The company has a lack of constant net income and a balance sheet that could be improved. Based on the risk associated with earnings estimate revisions at this time, I consider the stock fairly valued, with no margin of safety in price.

Array is a global provider of solar tracking solutions and services for large-scale power plants. It designs, manufactures, and supplies systems that increase the efficiency of these solar energy projects. Its tracking systems adjust the angles of solar panels to follow the sun's path during the day, which maximizes energy capture, offering a significant improvement to fixed-tilt installations.

The company had its IPO in October 2020, and it was founded in 1989. Array's operating revenue is composed of 78.5% from the US, 8.8% from Brazil, 7.9% from Spain, and 4.8% from the rest of the world. Array acquired STI Norland for around $652 million in a combination of cash and stock in 2022, positioning it as one of the largest solar tracking companies in the world. Now, 77.4% of its operating revenue comes from Array Legacy operations, and 22.6% comes from STI Norland operations.

According to Mordor Intelligence, the Solar Tracker Market size is estimated at $36.62 billion in 2024, and it is projected to reach $100.51 billion by 2029, growing at a CAGR of 22.38% over the period. This is part of a broader trend in the energy sector, where solar power is becoming an increasingly significant contributor to global electricity generation. The World Economic Forum considers solar to be growing faster than any other energy technology in history.

There are three main renewable energy competitors to solar:

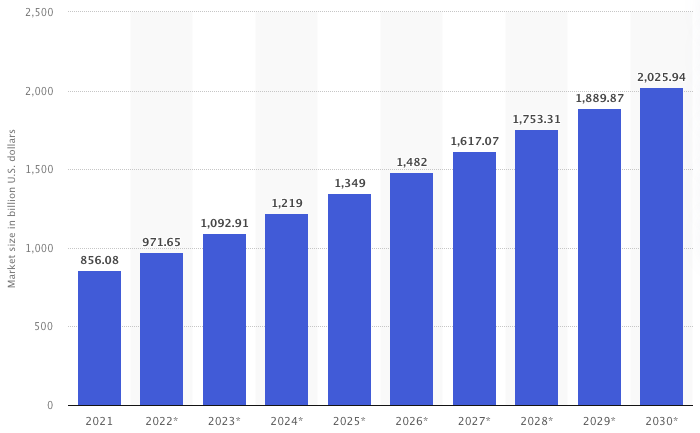

These renewable energy providers are the most significant contributors to the renewable energy market size, forecasted by Next Move Strategy Consulting to reach $2,025.94 billion in 2030.

Global Renewable Energy Market Size 2021-2030 (Statista)

Array has four major competitors that I have identified, independent of its market cap, and only one of these is publicly listed:

Based on a similar market cap, we can also include Shoals (SHLS) and Sunrun (RUN).

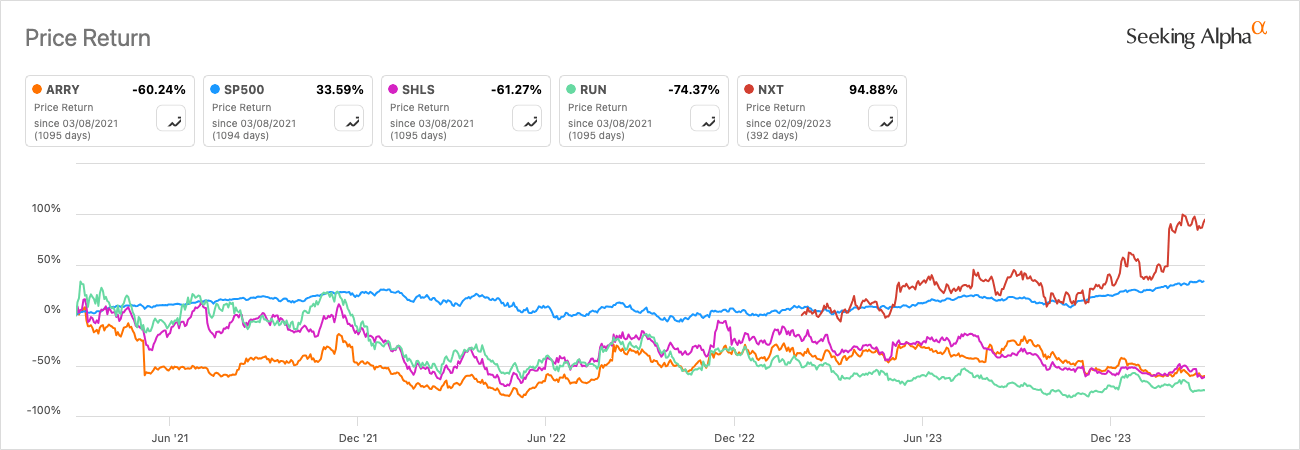

It is worth noting that compared to the S&P 500, Array has significantly underperformed over the past three years, which is a general trend in the solar energy markets at this time:

Author, Using Seeking Alpha

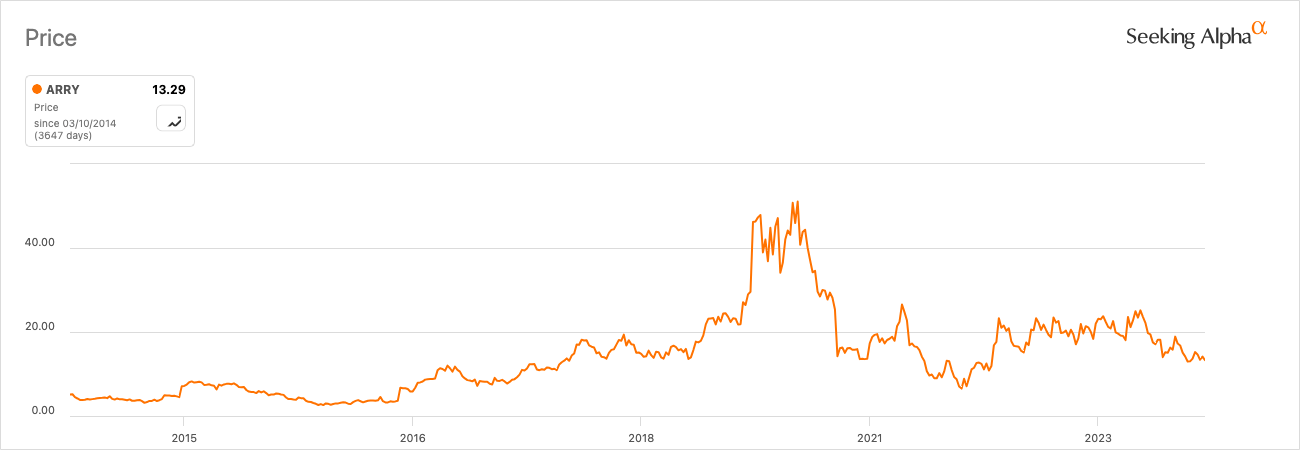

As I mentioned earlier, Array had its IPO in 2020, and its price rose significantly leading up to this, now returning to what I consider a more moderate valuation, in part due to a general slowdown in demand for solar energy in the US, Array's core market, at the moment. However, I also attribute it to what I consider to be too-high expectations and an overvaluation leading up to its IPO by excessive market sentiment.

Part of the instability that comes with investing in Array is that even though the company was founded in 1989, it has had continued periods of net loss as recent as since 2018 and 2021:

Seeking Alpha

Its 2021/2022 loss was impacted by challenges from an Anti-Dumping/Countervailing Duty investigation, which impacted Array's ability to forecast its 2022 estimates accurately. Projects of around $250 million of revenue were delayed, affecting the firm's financials. Additionally, CEO Kevin Hostetler noted:

Many things outside of our control, like the AD/CVD investigation, the conflict in Ukraine, and the continued commodity and logistics volatility will create a difficult overhang for the remainder of the year [2022].

The balance sheet could be a lot stronger, as its equity-to-asset ratio is 0.36, and its debt-to-equity ratio is 1.2. Compare this to the three publicly listed peers I have used for competitive analysis:

Evidently, Shoals comes out on top based on the balance sheet, and both Sunrun and Array have significant debts to pay off, which could inhibit future growth. Nextracker falls slightly outside of the competitive analysis framework, as it had its IPO in 2023 and was founded in 2013, so it is the newest of the four peers, and its balance sheet is anomalously weak.

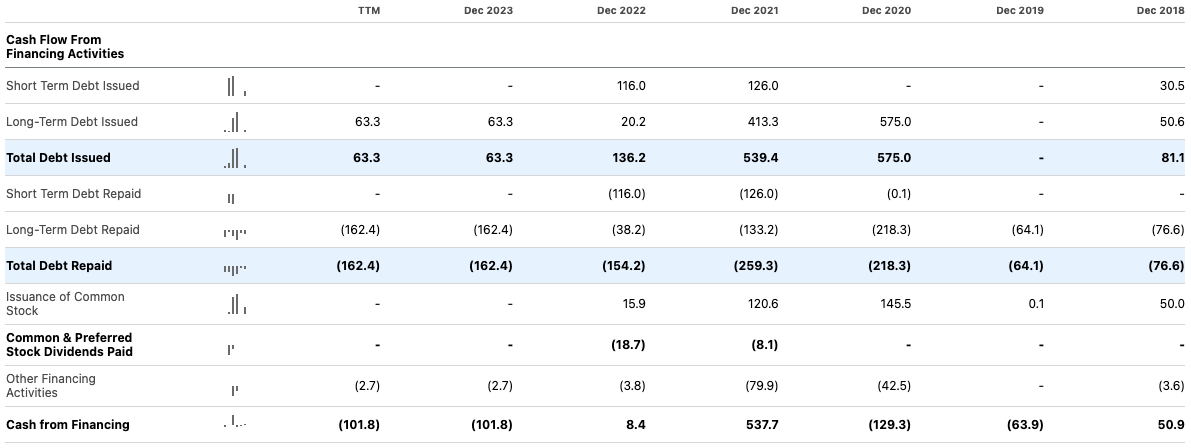

Notably, Array doesn't repurchase common stock, and its cash flow statement shows a high level of debt issued since 2018, with the most significant contributions being $575 million issued in 2020 and $539.4 million issued in 2021. However, it is paying this off in large amounts every year, which is prudent considering the need for a better balance sheet in general at this time.

Seeking Alpha

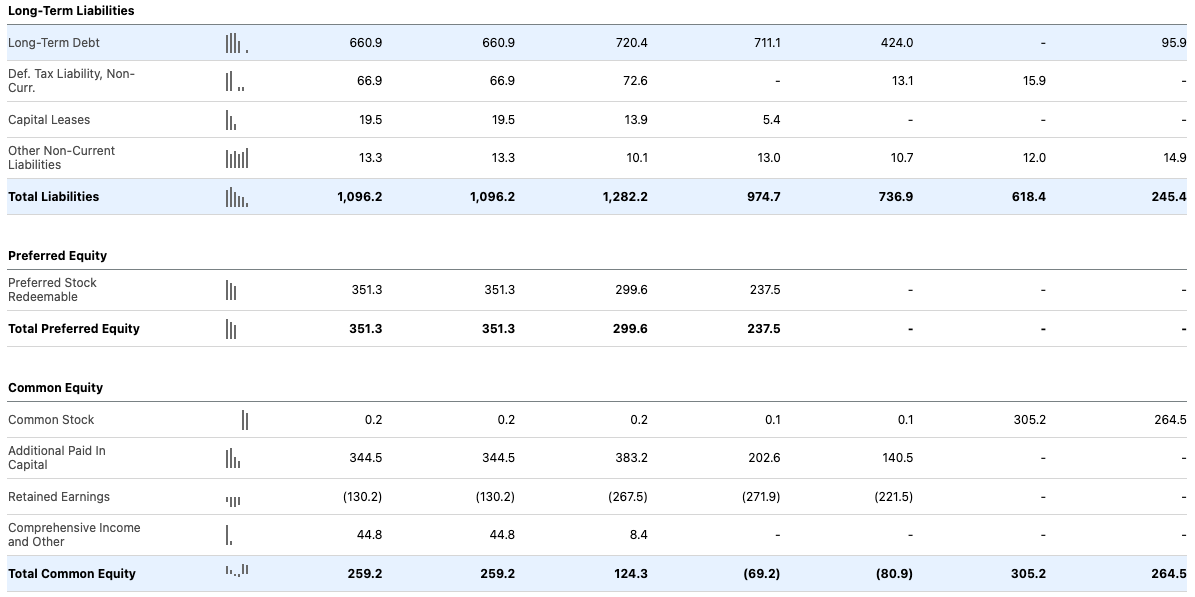

On the balance sheet, we can see that a significant amount of its total liabilities of $1,096.2 million at this time is made up of said long-term debt, specifically $660.9 million. But also, we can see the negative impact of retained earnings, which is significantly bolstered by additional paid in capital of $344.5 million. The balance sheet also shows further evidence of outlined earnings instabilities, with 2020 and 2021 showing negative equity:

Seeking Alpha

I consider Array's balance sheet a significant risk, and I believe there are better solar energy investments available on the market, particularly in China, including LONGi, which has an equity-to-asset ratio of 0.44 and significantly stronger growth prospects.

I consider Array fairly undervalued right now based on long-term earnings estimates. The semiconductor sector median for TTM P/E GAAP ratio is around 24.5, and Array is selling at a ratio of around 25. Array's forward P/E GAAP ratio is around 23. Compared to its peers, Array looks promising:

Array's earnings estimates for fiscal 2024 show a moderate normalized actual EPS contraction of -5.18% but 40.49% YoY growth for fiscal 2025 following this. This then reduces to a more moderate 3% YoY growth for fiscal 2026.

Seeking Alpha

Therefore, I believe it is clear there will be some volatility in the next few years, but now does not seem to be a bad time to buy in based on Array's price history.

Seeking Alpha

Considering higher growth in fiscal 2025 expected on consensus, usually, I would suggest that the shares are undervalued at this time, based on the following calculation:

However, as we will see, the revisions risk outlined next reveals why my estimate is caveated by short-term downside expected.

Over the past year, Array has depreciated in price by 35.12%, and over the past six months, it has depreciated in price by 46.61%. This outlines the significant short-to-medium-term danger of an investment in Array at this time, and I believe investors should have the stomach to weather the downside that could come if buying in now.

There is further evidence of long-term returns being less than currently expected, based on its EPS revisions having predominantly downtrends. December 2025, the year meant to be important for investors who buy in at the present valuation, has a -18.16% six-month trend in earnings estimate revisions. That indicates lower-than-expected returns for long-term-oriented investors. I believe this risk significantly outweighs some of the market forecasts I have outlined above, but I also think that sentiment may change once the global economy shifts back into a growth phase and renewable energy becomes more of a dominant spend in government and commercial budgets.

There are short-to-medium term downside risks with this investment, but I see a long-term future for the stock that is bright. However, I do not see evidence that this is one of the solar energy investments that will significantly outperform the S&P 500 over the long term, and I believe its balance sheet is one of the core areas of improvement that needs to be addressed, as well as its net income instabilities. Additionally, I believe that as the solar market proliferates and AI is introduced more powerfully into solar technologies, Array may face competition that could reduce its market share. My analyst rating for the stock is a Hold.