ferrantraite

ferrantraite

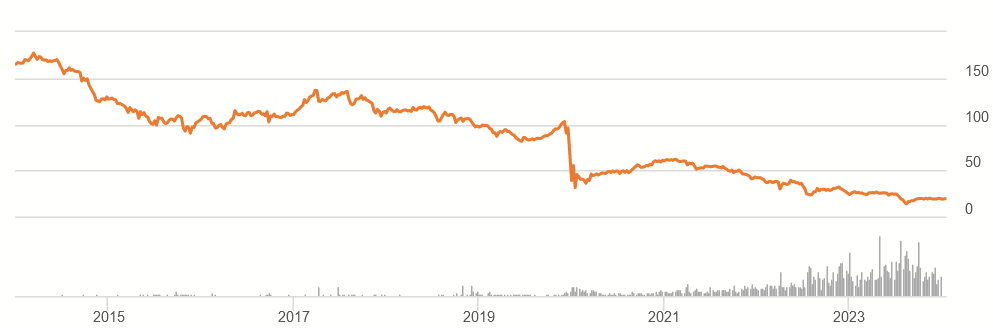

ARMOUR Residential REIT (NYSE:ARR) share prices had a tough year in 2023 and over the past decade.

ARR Price History (Seeking Alpha)

In spite of this, the shares currently boast a near-15% dividend yield. With FY 2023 results out through their latest 10-K and announcements last week of leadership changes, it seemed a good time for a more up-to-date look at the shares.

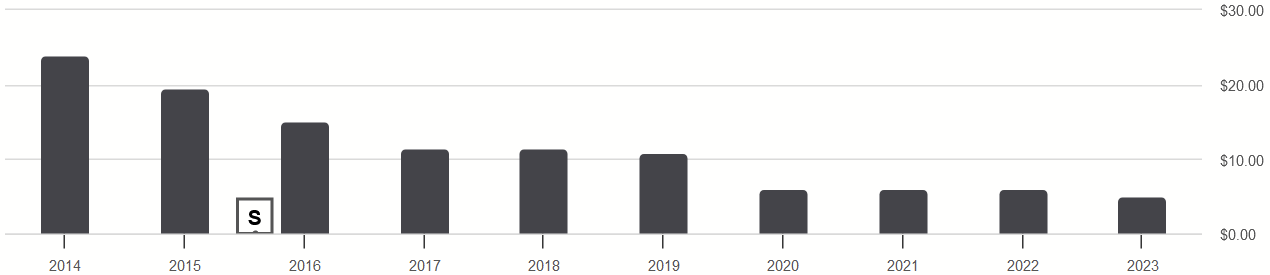

Being a REIT, ARMOUR's main draw for investors is the dividend income its shares provide. This is provided by primarily investing in residential mortgage-backed securities from the likes of Fannie Mae or Freddie Mac. Over the past decade, the results for that have been disappointing.

Dividend History (Seeking Alpha)

Adjusted for splits, the annual dividend has fallen from $24 per share in 2014 to $5 in 2023. What are the trends that followed this?

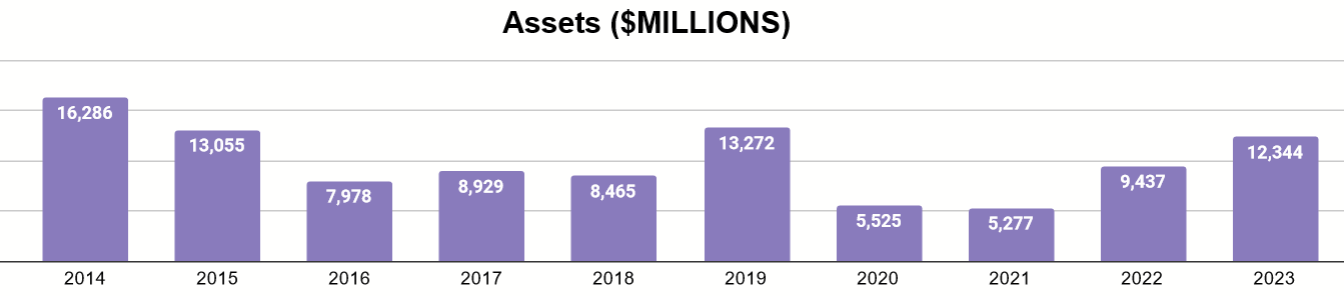

Author's display of 10K data

We see a declining asset book over time, with the occasional spike as new capital is raised, marked by sharp declines thereafter.

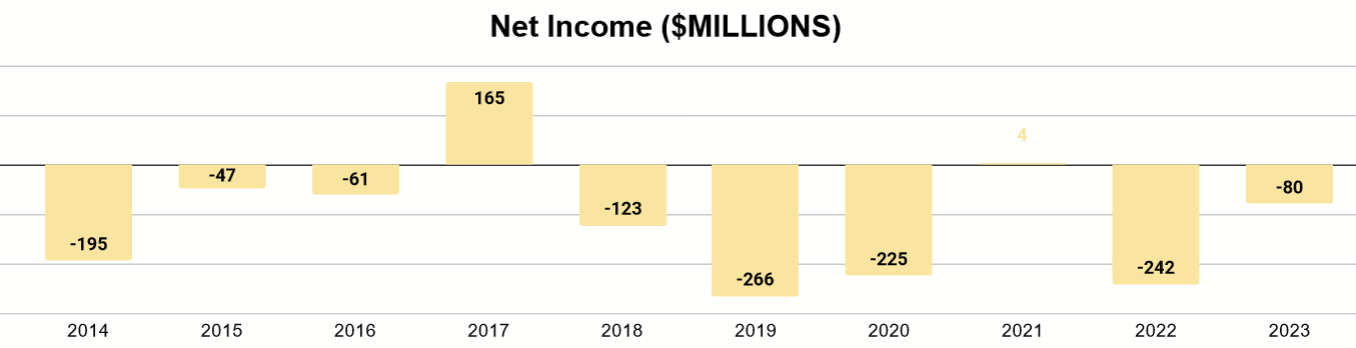

Author's display of 10K data

Unsurprisingly, the chart above shows that some of this is due to mostly negative earnings over the last decade. This means that distributions have occurred even as the company hasn't made any money. Yet, total dividends paid never exceeded $250M during this period and were sometimes as low as $100M. What else explains the declining assets?

Well, ARR relies on leverage to build their portfolio. In their 2023 Form 10K (pg. 1), the company notes:

Our borrowings (on a recourse basis) are generally between six and ten times the amount of our total stockholders' equity, but we are not limited to that range.

Later on (pg. 12), they note the risks associated with this.

Our lenders are contractually entitled to adjust margin requirements on relatively short notice and collateral values as frequently as daily. Depending on the duration and severity of the market distress, ARMOUR has sold, and may in the future need to sell, MBS at prices significantly below their long-term value in order to meet lender margin calls. We may not be able to participate in any potential market recovery and the resulting losses may permanently and materially reduce our equity.

Federally guaranteed assets like their residential MBS issues are often considered "safe" investments in terms of creditworthiness. Yet, because of their long maturities (between 10 and 30 years), their market prices are the most volatile in response to changes, one of the most important being interest rate fluctuations. Making them subject to margin calls based on changing valuations has the effect of negating the credit advantage offered by these MBS assets.

Seeking Alpha

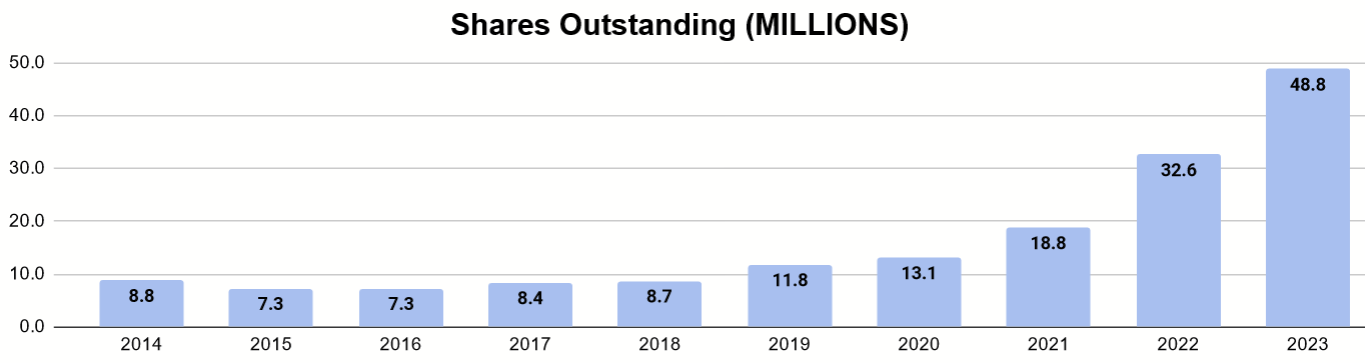

The last thing to consider for the declining dividend has been the issuance of new equity in order to raise more capital against losses. Adjusted for splits, the total shares outstanding are more than five times where they were a decade ago. Most of this occurred in the last three years, with $1.9 billion raised. A larger number of shares makes the same dividend harder to maintain. This contributed to a sharp dividend cut in December.

The company announced on March 15 that Jeffrey Zimmer would be stepping down as co-CEO, President, Vice Chair and director. This leaves Scott Ulm as the sole CEO. Zimmer had to say:

I have the utmost confidence in Scott's leadership and ability to capture the significant growth potential for the business...

Two days before that, it was announced that Gordon Harper would succeed James Mountain as CFO. On March 18, ARMOUR announced that Sergey Losyev and Desmond Macauley had become co-Chief Investment Officers. The timing of these changes is likely not coincidental, and so one has to wonder what growth lies ahead for this team.

It's important to ask because each of them already has many years with ARMOUR already, spanning the financial history I just discussed. I think it's unlikely that they would radically change much, so what else is there?

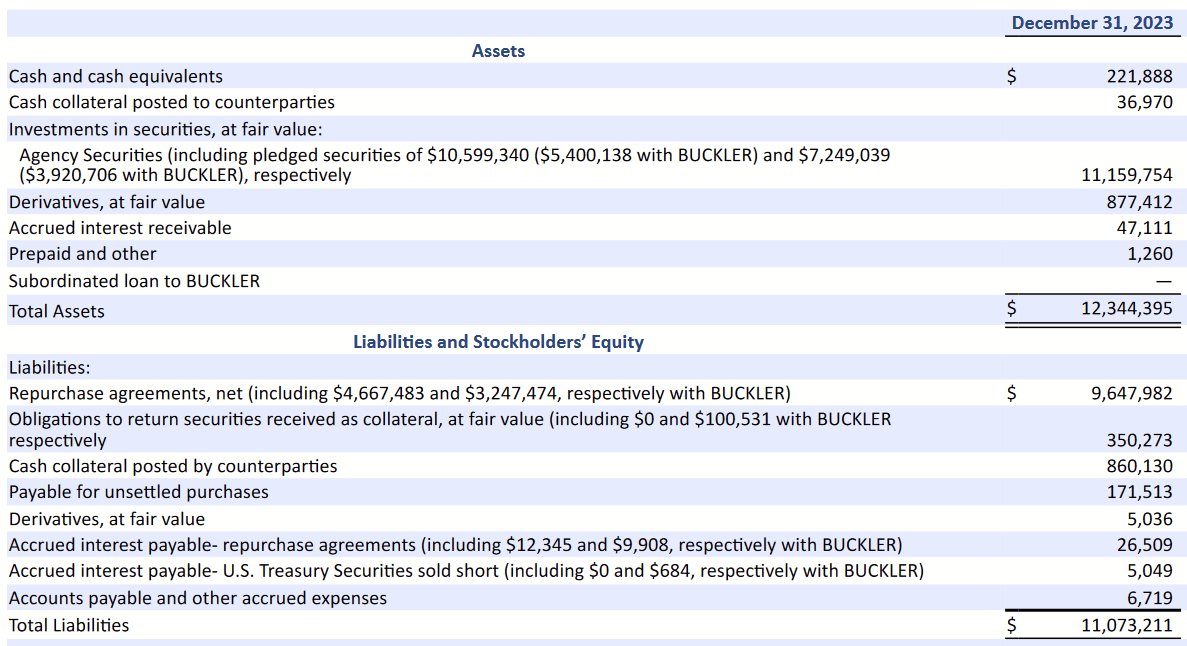

Balance Sheet (2023 Form 10K)

Looking at the balance sheet, what is there to change? An mREIT like ARMOUR has a pretty simple model: buy a portfolio of Agency securities, leverage some of these buys with repurchase agreements, buy derivatives to try and hedge against interest rate fluctuations, and hope it all goes well.

Zimmer may have been speaking to his belief that interest rates will soon decline, pushing up the value of their assets and creating ground for more mortgage origination in the country. This could create the first truly good year for ARMOUR in a long time. This reflects the Fed's expectations that there will be three rate cuts this year, which they reaffirmed just days after Zimmer's remarks.

Yes, this requires a bit of mind-reading, and it's not helped by the fact that management skipped out on an earnings call for Q4 and FY 2023 results.

Company Website

Generally, when a company skips the earnings call or even omits the Q&A portion, I take that as a sign that management is not comfortable about something. I find it strange when Q4's results had some positives to them, and these calls are often good "handing the torch" moments for leadership.

All things considered, even with the prospects of a decent year ahead, I do not consider the shares worth buying. ARMOUR does not have a significantly different approach from that of Annaly (NLY) or AGNC (AGNC), both of which I've covered before (1, 2). I see similar problems with those, but ARMOUR has a much worse record of results. If I want to take a dive into the Agency mREITs, they seem like the better choices.

Yet, I am not taking that dive. I continue to believe that purchasing these shares proves to be a better deal for the lenders whose margin call provisions allow them to seize the common shareholders' quality assets at distressed prices. Moreover, the business is largely at the mercy of the interest cycle and, with no hand in loan origination itself, doesn't have an operation that makes room for innovation or a competitive edge.

I would need a steeper discount in the share price or a stronger indication that new leadership will come with swift improvements. Until then, I don't consider these shares a reasonable Buy for the long-term investor.