Chun han

Chun han

CONSOL Energy Inc. (NYSE:CEIX) is a U.S. based coal producer with a market cap of ~ $2.5 billion. Since it operates in the coal space, it's not that surprising that the underlying valuations are extremely cheap and clearly in deep value territory.

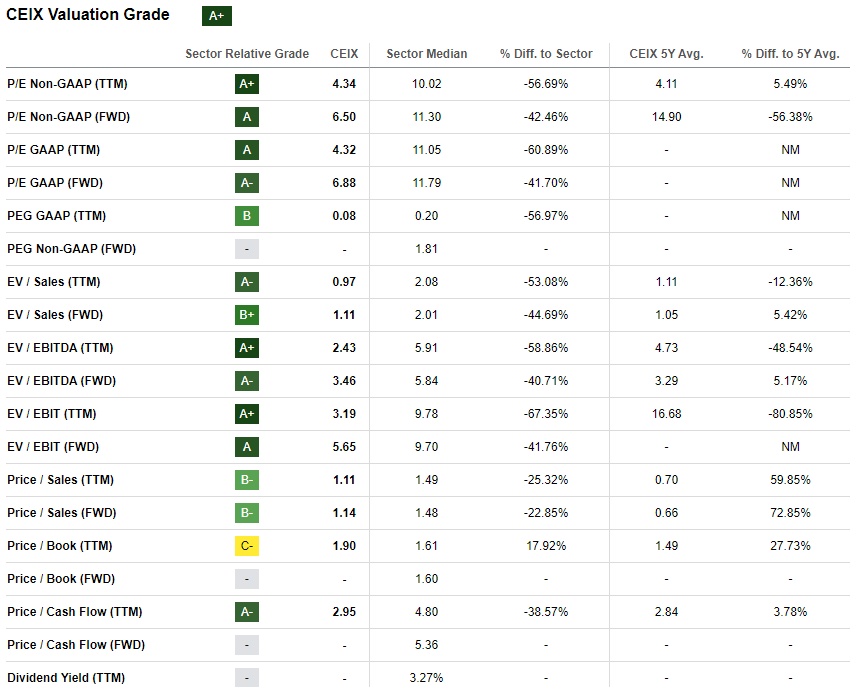

Just to give you a flavor of how cheap CEIX really is:

Also, if we compare the current valuations with the sector average (which includes other energy producers as well) and CEIX's historical levels, the picture does indeed look very attractive.

Seeking Alpha

Having said that, there are two aspects to consider when speaking about the relative and absolute cheapness of CEIX:

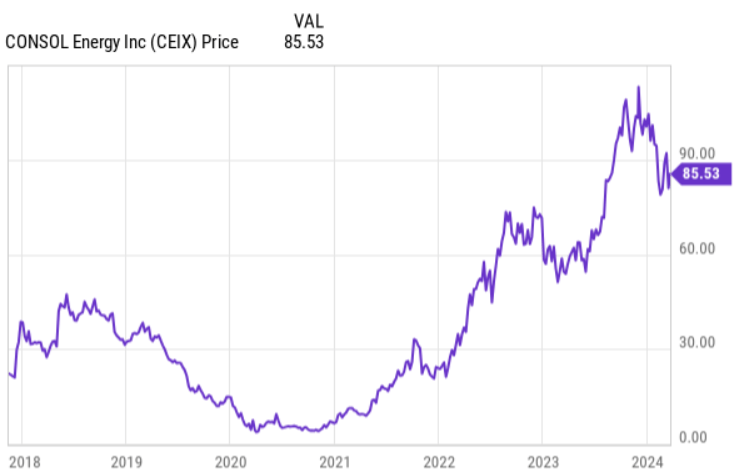

Ycharts

Let's now take a look at the underlying fundamentals of CEIX and determine whether the stock is a buy at these optically cheap valuation levels.

In the coal sector, the prevailing dynamics are favorable for export-oriented coal producers as U.S. demand has for several years in a row stagnated, gradually assuming a negative trajectory. Yet, in markets such as China, India and Africa, the demand for coal is not only there but also growing.

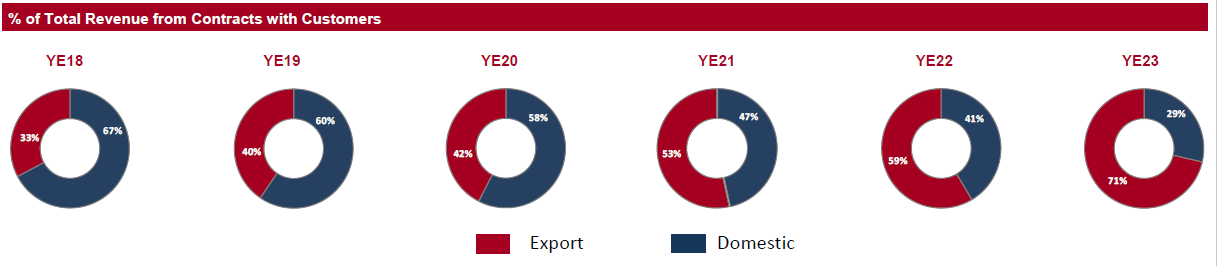

In this context, CEIX looks well positioned as it has dedicated consistent efforts in diversifying away from the notable exposure toward U.S.-based demand/revenues. For instance, as of now, the U.S. accounts only for less than one-third of the total revenue mix, while in 2018 the situation was the opposite.

CONSOL Energy Investor Presentation

While all of this is theoretically positive, there are, however, some drawbacks that are associated with foreign exposure. In my recent article on CEIX's peer - Alliance Resource Partners, L.P. (ARLP), which has almost zero sales to foreign customers - I elaborated on this quite a lot.

Some of the drawbacks:

Yet, all in all, the fact that CEIX carries an exposure toward structurally growing markets in terms of coal consumption is beneficial for the future cash generation profile.

Now if we assess the underlying financials of CEIX, the story gets even more enticing.

For instance, in the year 2023, CEIX delivered a net income of $656 million and adjusted EBITDA of $1.05 billion. Factoring in the capex spend, the free cash flow figure for 2023 landed at 687 million. Of this $687 million FCF result, circa 30% was directed toward de-risking of balance sheet and the remaining chunk was distributed to the shareholders.

These are very strong figures even considering the fact that 2023 was associated with milder domestic weather conditions.

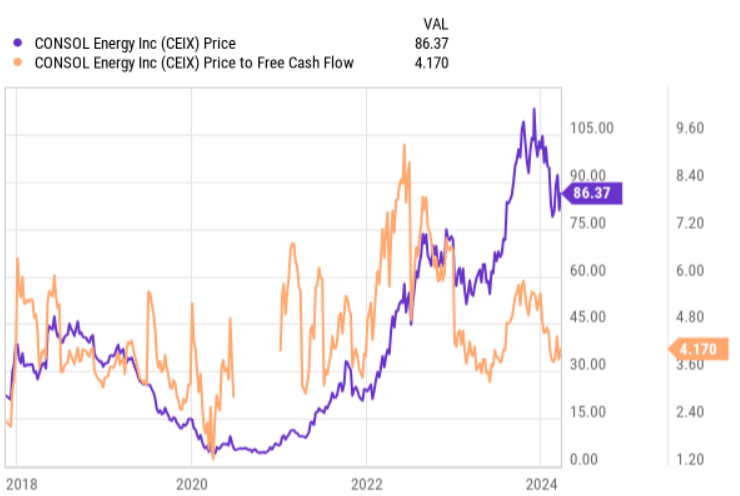

The chart below depicts nicely how CEIX has actually benefited from this robust cash generation (really starting all the way from 2022).

Ycharts

We can see that, while the stock price has surged higher, the multiple has remained the same or even decreased a bit. This means that the entire chunk of the positive total return performance has been attributable to the underlying fundamentals (i.e., strong FCF generation).

Moreover, it seems that even the massive efforts in debt reduction (where CEIX now has a negative net debt) have not helped the multiple to expand.

CONSOL Energy Investor Presentation

Finally, what's rather surprising for me is that there has not been a positive push at the multiple fronts even as the near to medium-term outlook for coal demand has improved:

Mitesh Thakkar - President and CFO - in the recent earnings call provided a nice color on this dynamic:

Moving forward to 2024, we expect to follow a similar playbook by building upon our structural export market shift, while maintaining a stable book of domestic fixed price business. There are several tailwinds in the US coal market that give us confidence in our ability to continue to contract future domestic business.

The increasing demand for data centers due to the deployment of AI technologies, growth of commercial factories, and EVs is causing electricity usage to soar across the United States. As such, utilities and grid operators are increasing their forecast for US electricity growth for the next five years, well above historical demand trends.

Plus, when speaking of the CEIX's financial prospects for the remainder of this year, we have to factor into our analysis the fact that almost 85% of the production has already been contracted. This provides the necessary cash flow visibility while leaving some room open for executing opportunistic sales in the spot market that have been rather elevated.

Finally, if we sum all of these pieces together - negative net debt, growing FCF that is already largely contracted for this year, exposure to favorable markets, and, most importantly, dirt cheap multiple - CEIX truly seems like a bargain.

At a P/FCF of ~ 4.1x and a target FCF distribution policy of 75% in the form of share buybacks Consol Energy looks like a very enticing buy.

Usually, whenever a company trades at so depressed multiple, there should be a meaningful probability of financial distress or the company going belly up.

However, in this case, the financial risk is almost non-existent given the negative net debt metric. The cash flows are growing for several quarters in a row with 85% of 2024 volumes already contracted. Plus, the exposure to growing market segments introduces certainty around the demand for CEIX's production going forward.

This combination of an extremely low multiple and growing cash flows has allowed the management to repurchase ~16% of the free float since late 2022 when the share buyback policy was initiated. The stock price has reacted accordingly.

Granted, there are still tangible risks in the "system" such as dependency on emerging markets and operations in the coal segment, which is constantly subject to potentially detrimental regulation.

However, at this multiple and at these fundamental characteristics, Consol Energy is a buy for me.