TonyBaggett

TonyBaggett

Arcos Dorados Holdings Inc. (NYSE:ARCO) owns the master franchise of McDonald’s Restaurants in 20 countries in Latin America and the Caribbean. With its vast market presence and capacity to serve over four million customers daily, ARCO is the largest quick-service restaurant (QSR) chain in the region. It is based in Montevideo, Uruguay and operates across South America and some parts of North America.

ARCO demonstrated a robust performance in FY23 amid the unfavorable impact of inflationary headwinds. It capitalized mainly on expansion to sustain its double-digit revenue growth. It also improved efficiency as margins have expanded in the past year. Even better, the company shows improving liquidity levels, although it still has to watch out for its borrowings. Its adequate cash levels amid its robust restaurant openings will allow it to sustain its larger operating capacity, repay short-term borrowings, and distribute dividends. This will be supported by improving macroeconomic indicators that may stimulate discretionary spending.

As such, the stock price uptrend remains reasonable. There is a decent upside potential, which can be supported by its solid performance. I recommend ARCO as a buy.

Two weeks before Arcos Dorados's earnings release, we already have a glimpse of its 4Q23 performance. The data for the fourth quarter may be limited, but that is enough to know it sustained its robust topline growth.

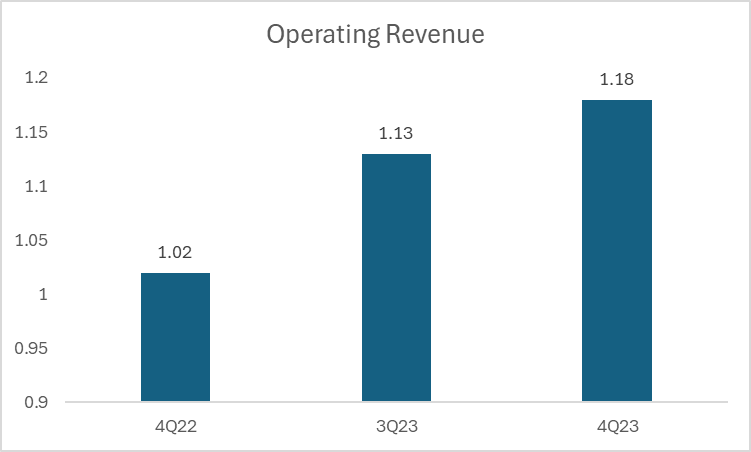

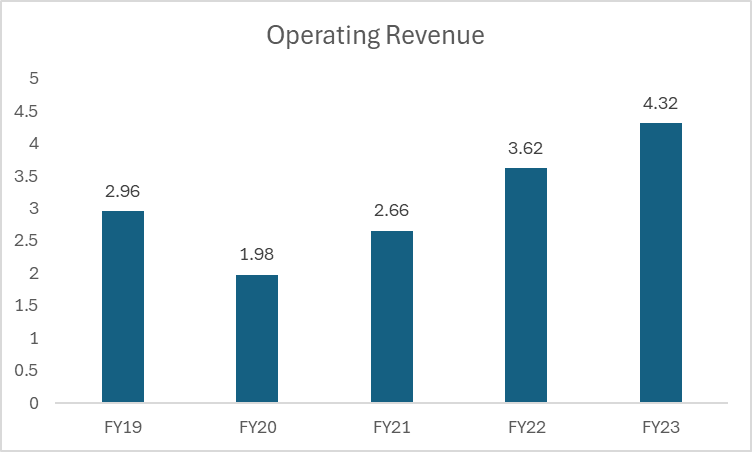

Based on the release, the 4Q23 operating revenue rose by 15.4% YoY. So, it was equivalent to $1.18B. More interestingly, the YoY growth every quarter has been uninterrupted since it started rebounding from the pandemic recession. And using the derived 4Q23 revenue, we can now derive the full-year value of $4.32B. It was 19% from FY22. Even better, the value has consistently increased since its rebound from the pandemic recession.

Operating Revenue (ARCO Earnings Release)

Operating Revenue (ARCO Earnings Release)

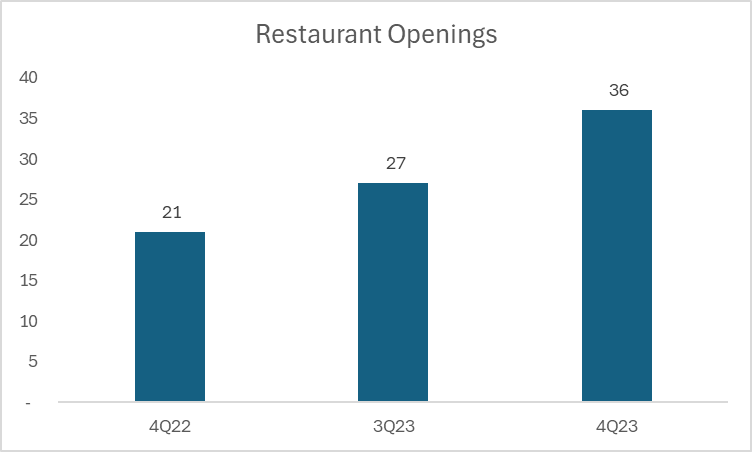

A lot of things contributed to its impeccable performance. First, the company capitalized on continued expansion. It opened 81 new restaurants the whole year, including 72 free-standing ones. The number of restaurant openings is much higher than in 2022 with 66, so ARCO reached its target. In addition, the number of restaurant openings has consistently increased from 1Q23 to 4Q23. During the first half, the combined number was only 18. In 3Q, it rose to 27. And in 4Q, it reached 36, one of the largest number of openings in a single quarter. It's no surprise that revenue growth was still substantial in the second half.

Restaurant Openings (ARCO Presentation)

Second, the company leveraged its digital capabilities. Digital channels accounted for 53% of systemwide sales versus 52% in the previous year. Its continued innovation helped it cope with the digital revolution. In-app delivery purchases and digital takeaways helped streamline and speed up order processes. This allowed the company to cater to more customers at a faster pace as it opened more restaurants across Latin America and the Caribbean. As of the recent report, it has over three million digital subscribers and serves over four million customers daily.

The decreasing inflation in the region also help increased consumer confidence to stimulate discretionary spending.

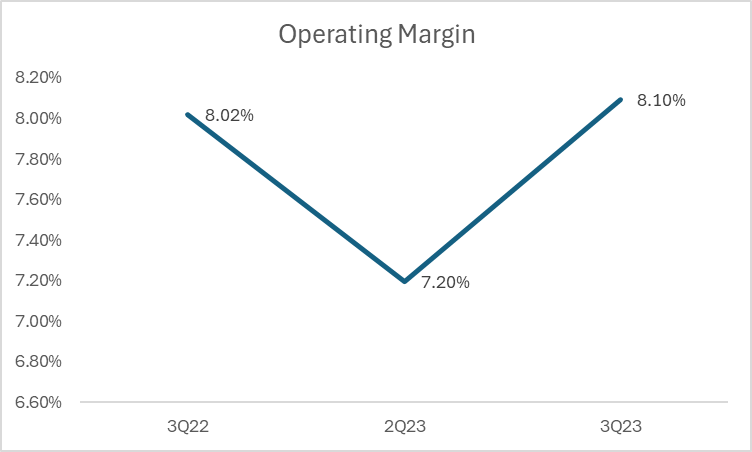

Meanwhile, its 3Q performance showed it achieved its goal of remaining efficient while expanding. Its operating costs and expenses rose as ARCO raised its operating capacity. Yet, sales growth still outpaced them. Indeed, the continued expansion and digital innovation helped the company to achieve economies of scale. As of 3Q23, the operating margin was already 8.10%, higher than 3Q22 and 2Q23 at 8.02% and 7.20%, respectively.

Operating Margin (ARCO Earnings Release)

Looking ahead into FY24, the company still shows solid growth prospects. Its plan to open new restaurants will help it sustain its already impressive topline growth. The improving external factors and adequate financial capacity of the company can support it.

These are the factors to like about ARCO.

ARCO holds the master franchise of McDonald's in the region, making it one of the largest franchisees globally. MCD is already an established name, given its ubiquity, size, and high demand. This gives ARCO an advantage over its competitors in the region. And since it holds the master franchise, it doesn't have a direct competitor in the form of other MCD franchisees. Also, there is little threat to its operations, especially now it plans to open more MCD restaurants this FY24.

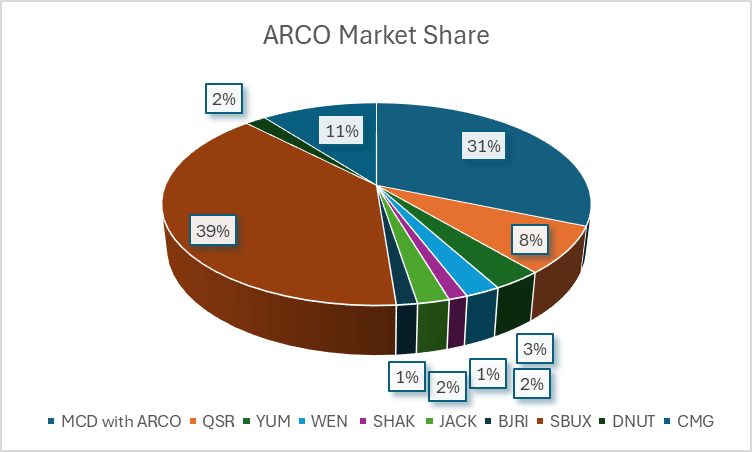

Even better, MCD continues to be one of the leaders in the restaurant in the industry. Among its close peers that had already released the 4Q23 report, it had the second-largest market share.

Market Share (Manual Data Gathering of Revenue Via Seeking Alpha)

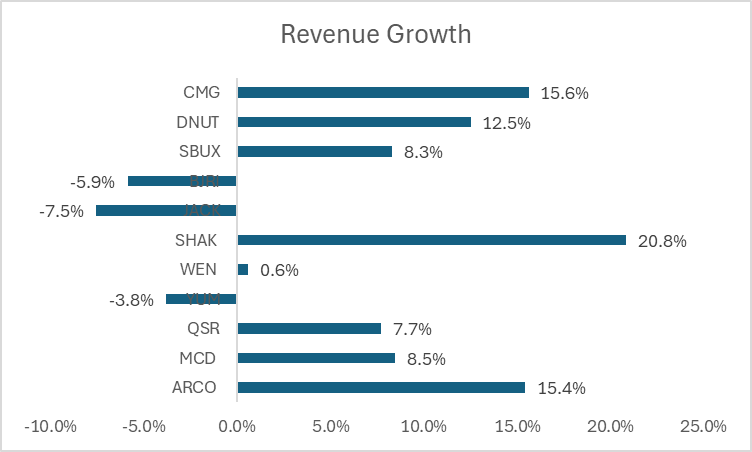

Also, MCD and ARCO both sustained revenue growth. ARCO had the second-highest revenue growth.

Revenue Growth (Individually From Seeking Alpha)

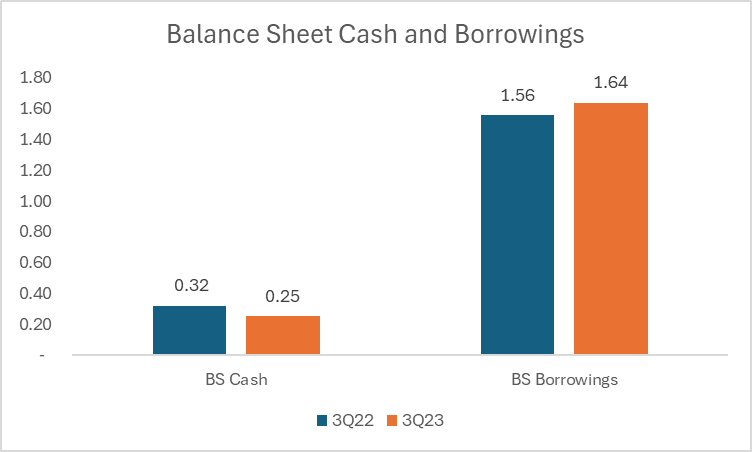

We still don't see the 4Q23 Balance Sheet, but from the looks of the 3Q23 report, everything is going well for the company. Cash and cash equivalents decreased from $319M to $251M, while borrowings increased by 5%. Even so, we can attribute these changes to the massive expansion of ARCO. Note that it opened 27 restaurants in a single quarter. This is much higher than in the previous year, which was only 15. Most importantly, the substantial increase in the income statement showed sound fundamentals. In fact, its EBITDA rose by 25.8% to $129M. With that, its Net Debt/EBITDA decreased from 3.24x to 3.22x. This is still lower than the maximum range of 4.0x. This is an essential metric to determine if ARCO can burn more cash or increase its borrowings to sustain its expansion through restaurant openings. The ratio shows that ARCO has a financial capacity of three years to pay all borrowings. As a capital-intensive company, ARCO maintains decent liquidity levels.

Cash and Borrowings (ARCO Earnings Release)

Risk factors of ARCO come mainly from external forces. Although its growth remained impeccable, it must watch out for its closest competitors, which also show increasing sales. Given this, the sustained expansion and restaurant openings of ARCO will be a primary driving force to propel its growth in the region.

These are some potential growth drivers of ARCO.

Restaurant openings and digital innovation have always been integral to ARCO's growth over the years. But the number has substantially increased in the past year, allowing it to capture more demand.

This year, it plans to open about 80-90 restaurants. And given its decent liquidity and viability, it can cover this expansion.

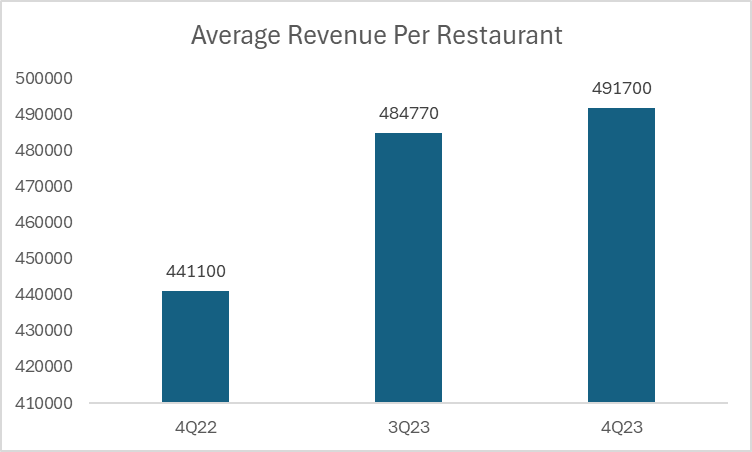

Note that as of 4Q23, it already has 2,400 restaurants. If we divide the operating revenue by the total number of restaurants, the average 4Q23 and full-year 2023 values are $491,700 and $1.8M, respectively. This is much higher than in 4Q22 with $441,100 and full-year 2022 with $1.6M. This shows that the 81 new restaurants brought an additional revenue of about $200,000 per restaurant. And from 3Q23 to 4Q23, the 36 new restaurants brought an additional average revenue of $60,000 per restaurant.

Average Revenue Per Restaurant (Author's Computation (Sales/Total Number of Restaurants))

Given the current trajectory, sales may still have a double-digit increase rate. To be more conservative, we are only setting it at 10%. And if the company achieves its number of restaurants, the average sales will be about $1.9M per restaurant. Even if the company only grows by 5%, the average revenue will still be higher than in 2023 at $1.82M. Indeed, the company has more room for growth, allowing it to capitalize on expansion and digitalization to get more customers.

Inflation has posed some challenges to the company in the past two years. But the stable core operations proved ARCO's resilience. And given the decreasing inflation, the price increase may become more manageable. In Uruguay and Brazil, inflation has already decreased to 5.09% and 4.51%, respectively. This can increase consumer spending. This can also help the company make price adjustments to increase sales and margins. And with the potential interest rate cut, increasing the borrowings and paying the current ones will become less expensive. Given this, the improving macroeconomic indicators can help ARCO maintain its growth, viability, and liquidity.

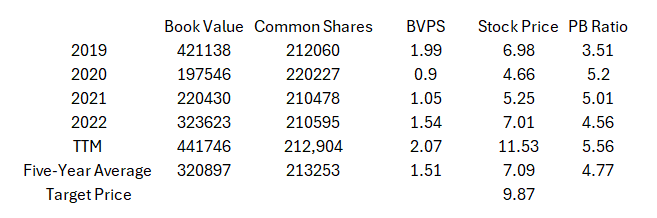

The stock price of ARCO has been in an uptrend since its rebound from the pandemic shock in 2020. The increase has sped up in the past year, mainly due to its continued expansion and solid revenue growth. More interestingly, its Book Value shows the largest influence on stock price changes. Take the historical five-year stock price trend and compare it to the book value in every year. In 2019, BVPS was $1.99, while the average stock price was $6.25. When BVPS dropped to $0.9 in 2020, the average stock price decreased to $4.66. When BVPS bounced back in 2021, the stock price followed. And when BVPS decreased again in 2022, the stock price went in the same direction. As of 3Q23, ARCO has a BVPS of $2.07. It’s no wonder the stock price has already risen to $11.53. Given this, the stock price uptrend can be supported by the increasing sales and book value of the company. However, if we try to use the PB Ratio to value the stock, ARCO appears to be undervalued by 14%.

Book Value, PB Ratio (Author's Computation)

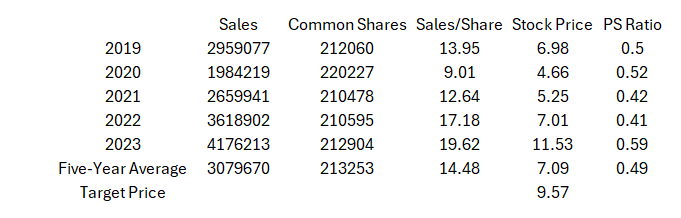

The same goes for the PS Ratio, which shows a 17% overvaluation of ARCO.

Price/Sales Ratio (Author's Computation)

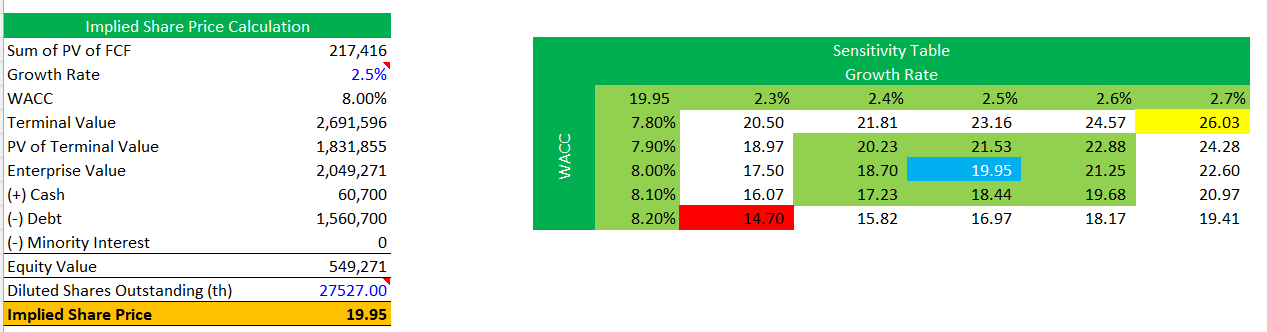

Even so, we can infer that the uptrend can be supported as long as sales and book value keep increasing. So, we will use the DCF Model to assess the stock price. It is a more precise valuation method, especially since ARCO is a capital-intensive company.

DCF Model (Author's Computation)

Apparently, the DCF Model contrasts the valuation using the two price metrics. After all, this is more forward-looking than the other two. It shows a 73% upside potential, which I still find reasonable since ARCO is still expanding despite its already huge exposure to Latin America and the Caribbean. It continues to dominate the market with its sustained restaurant openings and digitalization. And it still pays off, given the double-digit increase in sales and rising margins. Also, its increasing book value shows its high sustainability despite its high borrowing levels. It has adequate resources to sustain its increasing operating capacity, pay borrowings on time, and distribute dividends. As such, it should not be surprising that the increasing sales and book value support the price uptrend.

As we can see, I only used a 2.5% perpetual growth rate to remain consistent with the target inflation of 2.0-2.5% this FY. Meanwhile, WACC was derived using CAPM.

I also want to reiterate that ARCO holds the master franchise of MCD in the region. This makes it one of the largest franchisees globally. Hence, it should be logical to expect that the price is still lower than the intrinsic value.

Arcos Dorados is a solid company with impeccable topline growth and decent liquidity. It has adequate earnings to sustain its expansion and pay borrowings on time. We can see it in the increasing book value and decreasing Net Debt/EBITDA Ratio. Both ratios show that the company remains viable and sustainable to continue supporting its robust stock price performance. Hence, I am recommending ARCO as a buy.