bjdlzx

bjdlzx

EQT (NYSE:EQT) has made an offer for Equitrans Midstream (ETRN). It's an all-stock deal where EQT will issue .3504 shares of its common for each share of the midstream stock. As management shows in their acquisition presentation, EQT has been building a midstream network for some time. Only this time, the midstream operation is the sole reason for the acquisition. By waiting until the major Equitrans Midstream construction project (the Mountain Valley Pipeline) was done before buying Equitrans Midstream, management avoided major (and complicated) management headaches as well as cost overruns. This will save shareholders a lot of money while continuing the management midstream strategy.

The last article told the story of this acquisition from the Equitrans side. But there are two sides to any acquisition story. This article will cover the EQT side of the acquisition offer.

Back when I first covered EQT, the company "dumped" the production into the oversupplied Marcellus area. Management had limited options, combined with long-term contracts, to change the situation to get better commodity pricing for the production. The acquisition process has sped up that change considerably. This should lead to greater profitability from better sales pricing sooner rather than later.

This management is actually reproducing the Canadian model of doing business because it's often seen in Canadian companies. Generally, only the largest American companies own an extensive midstream business as is seen here. Some small and mid-sized companies actually sell any significant midstream operations because these are viewed as lower profit than the upstream.

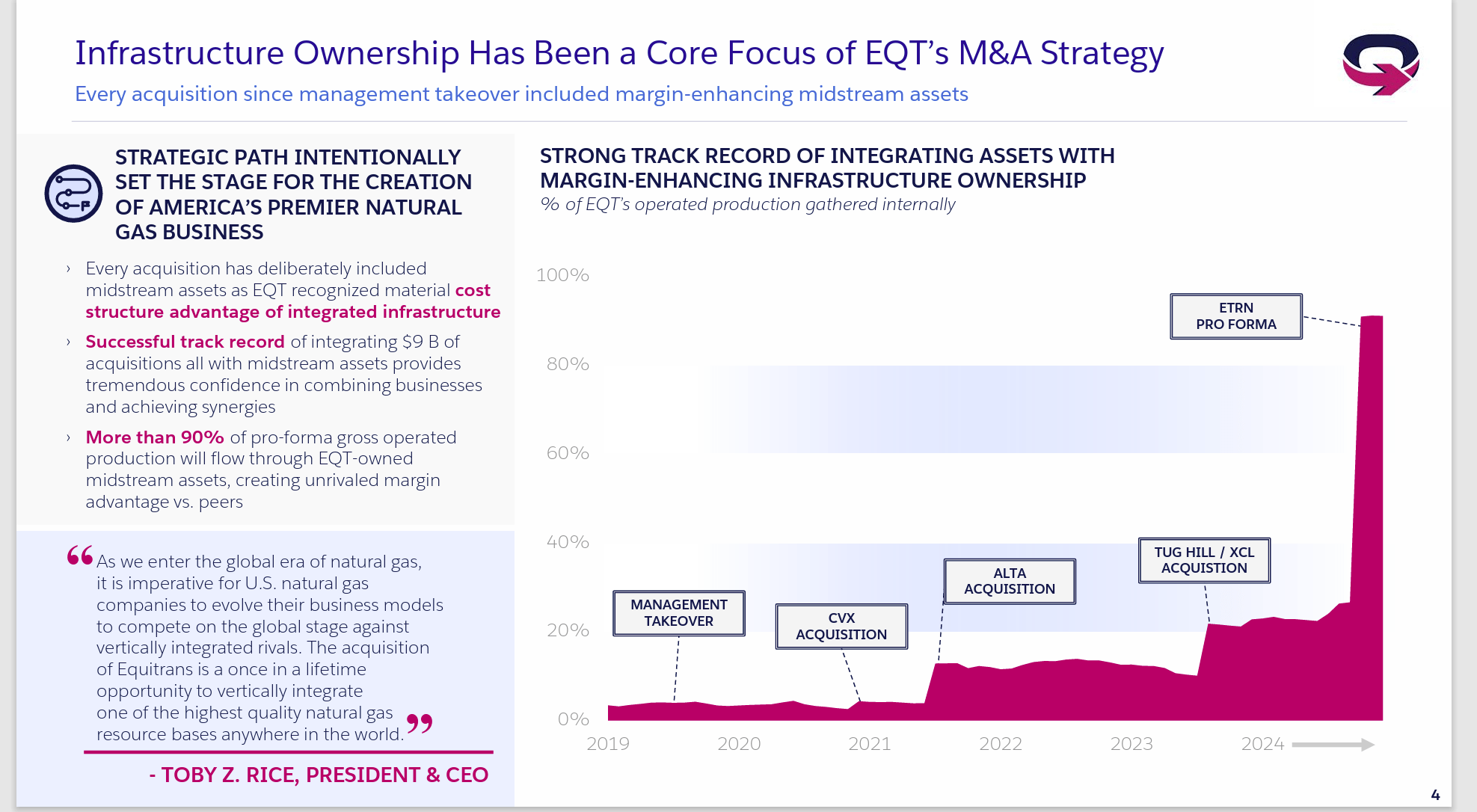

EQT Midstream Acquisition Strategy (EQT Equitrans Midstream Acquisition Presentation March 2024)

The thing to remember here is that the Rice Brothers merged their company into EQT and then after that the midstream split from the upstream operations. When the current administration took over a few years back, they found that the company had few options for selling its production. That lack of options often meant the sales price had a sizable discount to the related benchmark.

What's happening above is management is developing more options to move the production to stronger pricing markets. This strategy should minimize or eliminate the discount to the relevant benchmark.

This is a way to solve the "low price" issue somewhat that was covered under the last article due to a lot of natural gas in storage. It's not a real common way to resolve the issue either.

Antero Resources (AR) has long explained (as they do in the latest presentation) how they have the midstream options to get their production to stronger markets. This has long resulted in Antero Resources getting the best pricing for its natural gas in the Marcellus Basin (and the associated products as well).

Clearly EQT management wants a similar model to achieve better pricing than the oversupplied Marcellus Basin pricing. But waiting for long-term midstream agreements to expire would have been a very slow process. Carrying extra midstream capacity is often a far lower cost than the potential premium pricing obtained by getting the natural gas to stronger priced markets. Antero Resources has been demonstrating this for years. EQT management is rapidly moving the company into position to join that same strategy.

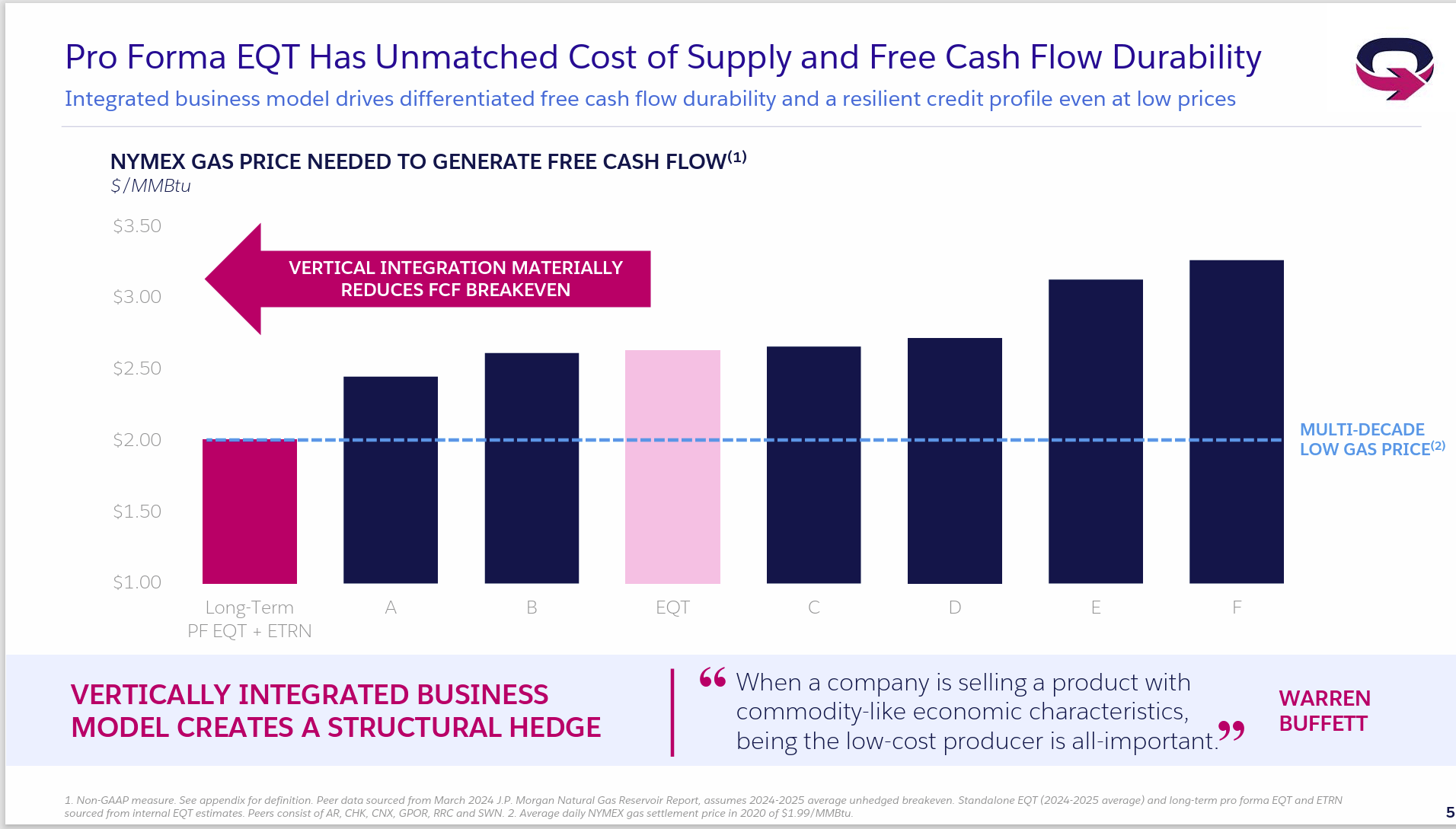

A well-run vertical integration system can have some significant (even major) cost implications. A key risk factor is that with vertical integration, every part of that integration must run optimally. Otherwise, the case for vertical integration falls apart.

EQT Discussion Of Merger Effect On Lowering Costs (EQT Corporation Presentation Of Equitrans Midstream March 2024)

In effect, Antero Resources did this by constantly obtaining a premium price compared to others in the basin. But that lowered the NYMEX price needed because that premium pricing was obtained. There's likely to be a similar effect for EQT.

But there's also a benefit to controlling as much of the sales process as possible in that the company makes money every step of the way. The midstream business is a steady business where cash flow basically does not follow the upstream business conditions. This is because the midstream business is a transportation business. Therefore, commodity prices do not matter. The result for EQT is likely to be lower earnings volatility due to the presence of that midstream business.

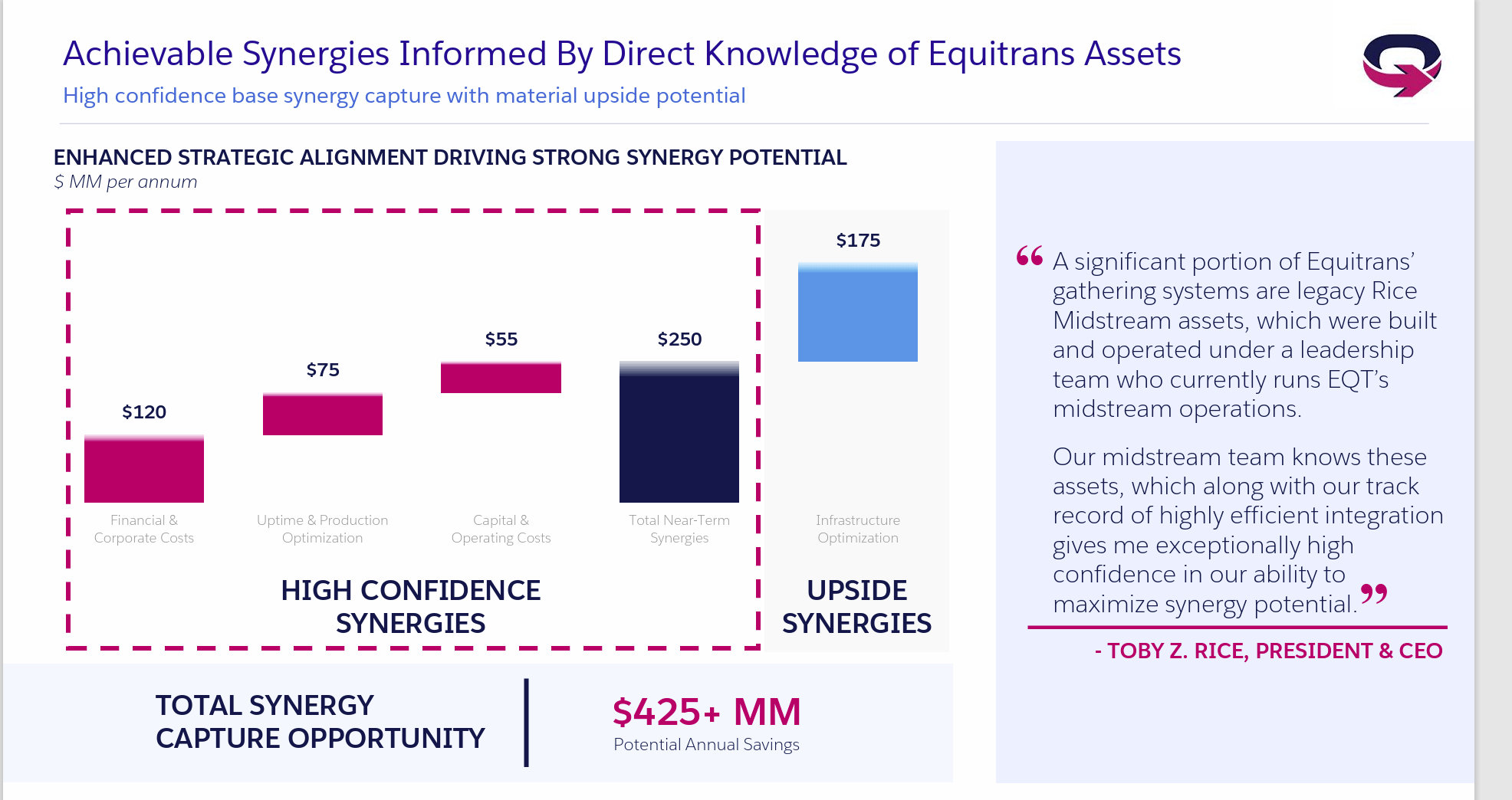

The company employees are unusually familiar with a significant portion of the Equitrans assets because they ran the assets before Rice Energy merged with EQT. That's an unusual situation that will reduce assimilation risk.

EQT Merger Synergy Guidance (EQT Corporate Presentation For Equitrans Midstream Merger)

Admittedly the Mountain Valley Pipeline project will be a new asset addition that EQT employees did not manage before the merger and spinoff. However, any familiarity makes the chances of merger success climb.

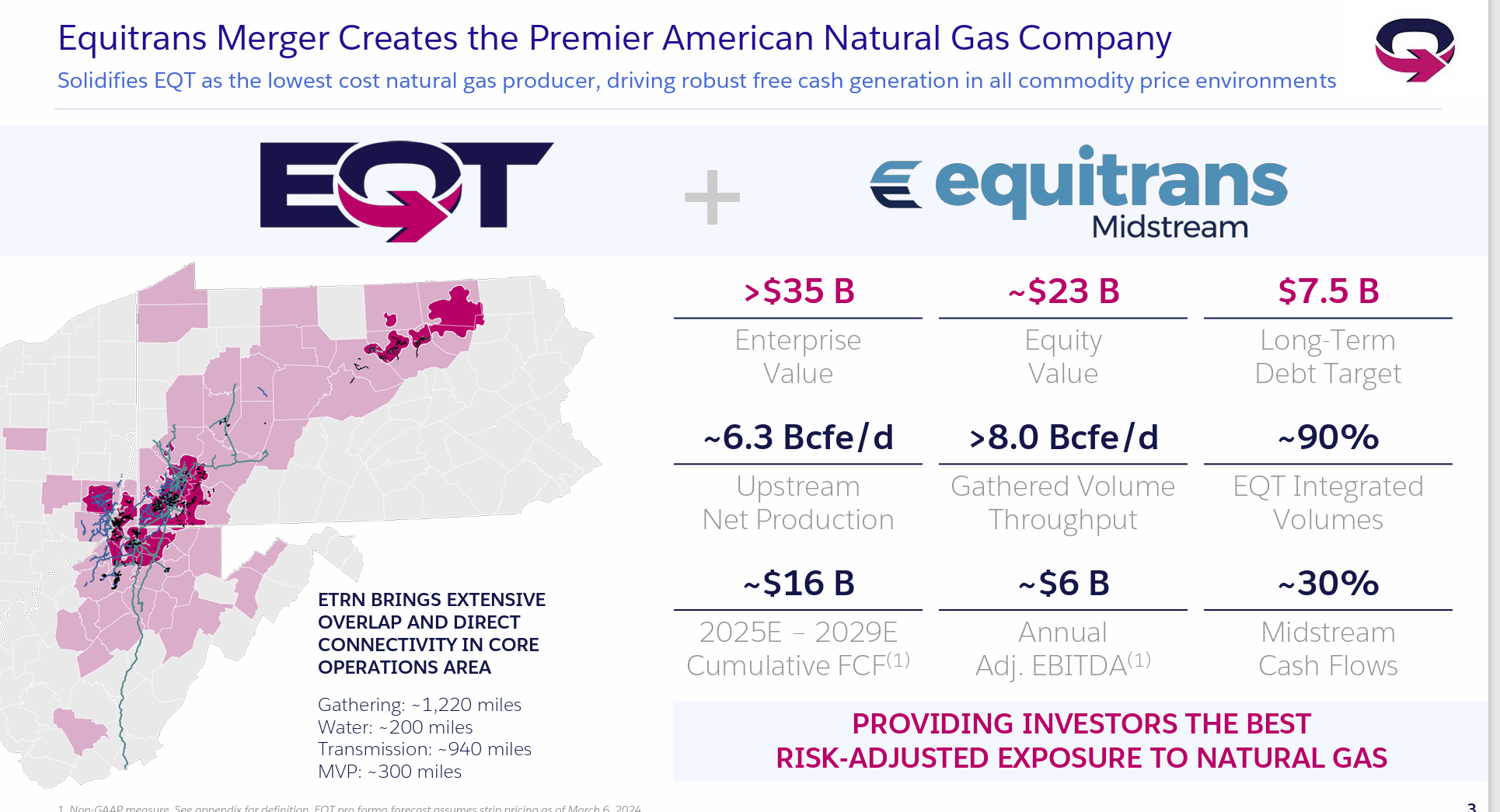

The combined company map of operations does have some overlap. Management will have to decide if they can take advantage of the overlap. Managements often move assets like natural gas processing equipment to places needed when there is some idle capacity.

EQT Post-Merger Combined Company Map Of Operations (EQT Corporate Presentation Equitrans Midstream Merger Proposal March 2024)

Probably the largest market worry is all of the Equitrans Midstream debt that the combined company will have to deal with. But as is shown above, management will likely be able to quickly reduce debt as Equitrans Midstream as a private company will have no commitment to a level or steadily increasing dividend.

Therefore, the Equitrans Midstream debt can be rapidly repaid first and then dividends from a much financially stronger private company can be distributed to the major holders.

That's likely to work out far better than the current market demands for a return of capital to shareholders that likely constrains the Equitrans Midstream stock price. In fact, that market demand for shareholder returns could relegate debt payments at a slower pace that could last for years with no dividend increase should it remain public.

That could very well mean that Equitrans Midstream has more value as a private company than it does as a public company due to the debt load.

EQT management has come up with a significant way to "move the needle" in terms of company earnings faster than the company can grow while meeting market demands for shareholder returns. It's doing it by acquiring a debt laden company that dealt with cost overruns to build a new interstate pipeline.

Management no longer has to deal with court cases and work stoppages on the major construction project because operations of the pipeline will have begun before the merger completes. That's going to be a major cost advantage that greatly simplifies the management tasks going forward.

Cost reductions and the benefits of vertical integration are essentially "icing on the cake" compared to avoiding a fair amount of the cost overruns constructing the pipeline.

EQT also is making a major advance to the goal of getting better pricing for its production. Most managements I follow dump their production locally without a thought about prices received. Instead, they just take what they can get. Management is taking the pricing a few steps further to get better pricing that more than offsets transportation costs.

EQT remains a strong buy on the acceleration of a long-executed strategy to get production out of an oversupplied basin to stronger markets. The change with this merger will be significant in the form of increasing profitability at a rate faster than production growth for a few years.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.