phototechno

phototechno

This is my first take on AquaBounty (NASDAQ:AQB) a different type of biotech company. It is an innovative company that is carving a niche for itself in the developing field of aquaculture.

As we begin calendar year 2023, AquaBounty Technologies can take pride that it has come a long way since its founding in 1991. The initial spark that started its long trek was a breakthrough in genetic engineering for the development of Atlantic salmon at Memorial University in Newfoundland Canada.

AquaBounty can never be accused of having small ambitions. Its 09/2022 Analyst Day slide presentation (the "Presentation") opens with the following introductory slide:

seekingalpha.com

Feeding the world with genetically engineered protein, slaying the dragons of political, regulatory and perceptual hurdles. My, it is strutting its stuff. This is a $64 million market cap company which has ambitions of punching far above its weight class.

Beginning with an initial study submitted in 2003, AquaBounty has been working with the FDA to secure approval of its GMO AquAdvantage Salmon and its farms ever since. In other words AquaBounty operates in a similar rigorous FDA regulatory environment as more traditional biotech companies.

In the transcript (the "Transcript") that goes with the Presentation, CEO Wulf sets out its competitive environment as:

...a very fragmented industry. There are a lot of new players coming into this space. You see new folks coming in on the technology side, you see new folks coming in on the growing side. There's also some consolidation taking place on the supply side, so I think one of our benefits there is that we are vertically integrated, we are our own source of eggs. Other land-based RAS farms don't have that capability, which is why some of them are talking to us about being their supplier for eggs.

AquaBounty has two operating farms that are producing product, its Rollo Bay farm on Prince Edward Island in Canada and its farm in Albany Indiana. It is currently in initial site construction activities for its Pioneer Ohio farm. Its ambitious goal is to build out a new farm every two years.

Per slide 31 of the Presentation its primary focus is to have 4-5 new farms producing at capacity by 2030. It anticipates reaching capacity of 50,000 metric tons. It is also looking for partners to expand internationally. Initially it is looking at China, Israel, Argentina, and Brazil.

In its 10-Q (pps. 31-32) AquaBounty notes the uncertainties inherent in its expansion plans particularly in the current inflationary environment. Among the litany of issues it cites as potential drivers of cost increase as it completes its pioneering, cutting edge RAS installations are some combination of:

These issues are intersecting with the sizable economic commitments inherent in building out AquaBounty's production facilities. For example it initially pegged its Ohio farm as a $320 million commitment. Its latest press release, its Q3, 2022 earnings release (the Release") dated 11/08/2022, describes its increased bond financing authority for $425 million.

The Release anticipated closing the bond financing by Q1, 2023. As I write on 02/13/2022 there is no news of any developments. The bond issuer is just one part of the financing puzzle. The tougher part is finding buyers for the bonds who are willing to take on its financial risks. This should be reported soon if it meets Q1 target.

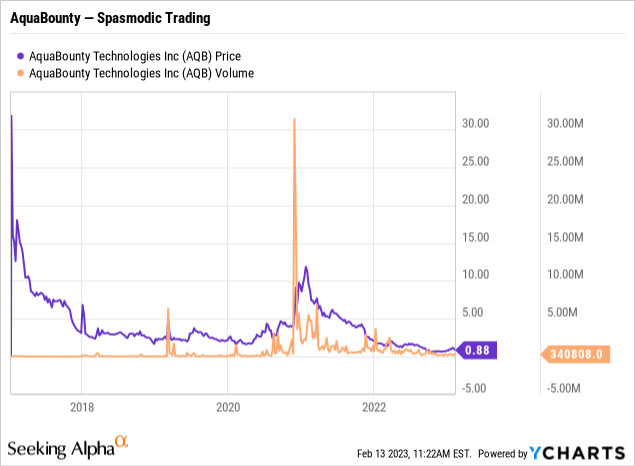

AquaBounty has been laboring to develop its vision over the last >three decades. It has been publicly traded since its IPO in early 2017 with shares priced at $1.50. As shown by its chart below its initial trading started with a bang:

Its initial enthusiastic trades were on low volume. Its Seeking Alpha news feed over it life as a public company has mainly reflected its quarterly earnings releases. These releases reflected ongoing losses as it built its current ~$187 million accumulated deficit. Its news feed also included periodic reports of share transactions leading to its latest reported ~71 million shares outstanding.

AquaBounty provides no quarterly earnings conference calls. Its quarterly earnings press releases provide basic information. Its latest reported revenues are definitely small beer:

...$653 thousand in product revenue in the third quarter, a year-over-year increase of 44% as compared to $455 thousand in the third quarter of 2021. In the nine-month period ended September 30, 2022, product revenue totaled $2.7 million, a year-over-year increase of 255% as compared to $0.8 million in 2021.

For 2022 its expenses through Q3, 2022 ran at ~$19 million. It closed Q3, 2022 with cash, cash equivalents, marketable securities and restricted cash of $128.0 million, down from $191.2 million as of December 31, 2021.

So far it has had no problem selling the salmon that it produces. Its Indiana farm, which is its principle source of salmon has a capacity of 1,200 metric tons. Once it gets its Ohio farm up and running, it will ramp up its production by at least ~10,000 metric tons.

This should help towards meeting its initial production challenges. In the Transcript, CEO Wulf discusses how customers embrace its product; however it has inadequate supply for larger customers with whom it might negotiate long term contracts. Even 11,200 metric tons would not register it as a major producer; it is just a drop in the bucket compared to the big boys. Mowi ASA (OTCPK:MHGVY) produced 2.6 million metric tons of salmon in 2021.

AquaBounty is an admirable company working to become a force in providing sustainable nutrition in an environmentally responsible fashion. From an investment standpoint it is often best to disregard such feel good sentiment and stick to the known financial metrics that can support future performance.

With AquaBounty these are precious few. Its farms are being designed to meet the highest standards of performance, but it has limited experience upon which to base such decisions. As is clear from Presentation slides 20 -22 described below its farms are working experiments:

It has no reliable data upon which to base either operational income or costs and expenses. Investment success will not only require that it be able to successfully scale and operate its farms, it will also require that establish effective channels for selling and shipping its product.

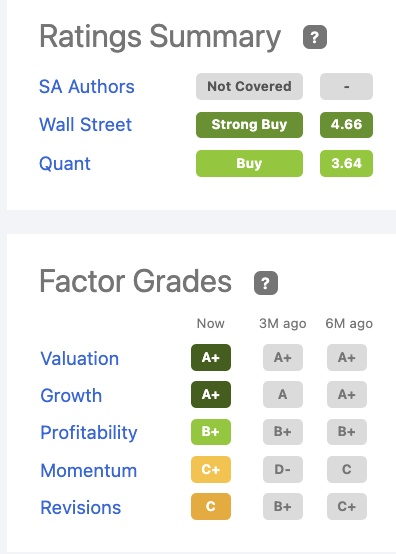

I am keenly aware that Seeking Alpha's ratings panel for AquaBounty shows a strong report as follows:

seekingalpha.com

In this case I was more mindful of its quant rating of "buy" than its Wall Street "strong buy". AquaBounty is just the sort of story stock that brokers can use to pitch to a client. Quant ratings on the other had are based on financial metrics.

Its quant profitability rating is the one that I question. Although AquaBounty has been operating for a lengthy time, I judge its operations as insufficiently mature to assess them as profitable. Consider the following from its latest 10-Q (p. 8):

...the Company has experienced net losses and negative cash flows from operations since inception,..., until such time as the Company reaches profitability, it will require additional financing to fund its operations and execute its business plan.

Accordingly quant's "B+" for profitability must be attributable to the universe by which it is measured, rather than by the plain fact that it has never made a profit.

In sum I rate AQB stock as a hold. I wish it and all of its investors the best of luck. This is one where I am taking a pass.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.