Supertruper

Supertruper

Hotel REITs have had quite the ride over the past 5 years, from market fears in 2020 during the pandemic to optimism around a travel rebound, and back to fear again due to higher interest rates and economic uncertainty.

This is reflected by the share price performance of Chatham Lodging Trust (NYSE:CLDT), which as shown below, is again trading at the low end of its 5-year trading range outside of the 2020 timeframe.

CLDT Stock 5-Yr Trend (Seeking Alpha)

I last covered CLDT back in April of last year, noting the impressive turnaround in its operating metrics and undervalued share price. While the stock has seen its ups and downs since then, CLDT has declined by just 1.8% since my last piece (0.3% total return including dividends).

In this article, I revisit the stock including key updates on operating fundamentals over the past year, and discuss why CLDT remains a good bargain for those willing to go against the grain, so let’s get started!

Chatham Lodging Trust is a Hotel REIT that focuses on upscale, extended-stay and select-service hotels. At present, it owns 38 hotels covering 5,735 rooms in 16 U.S. states and Washington D.C.

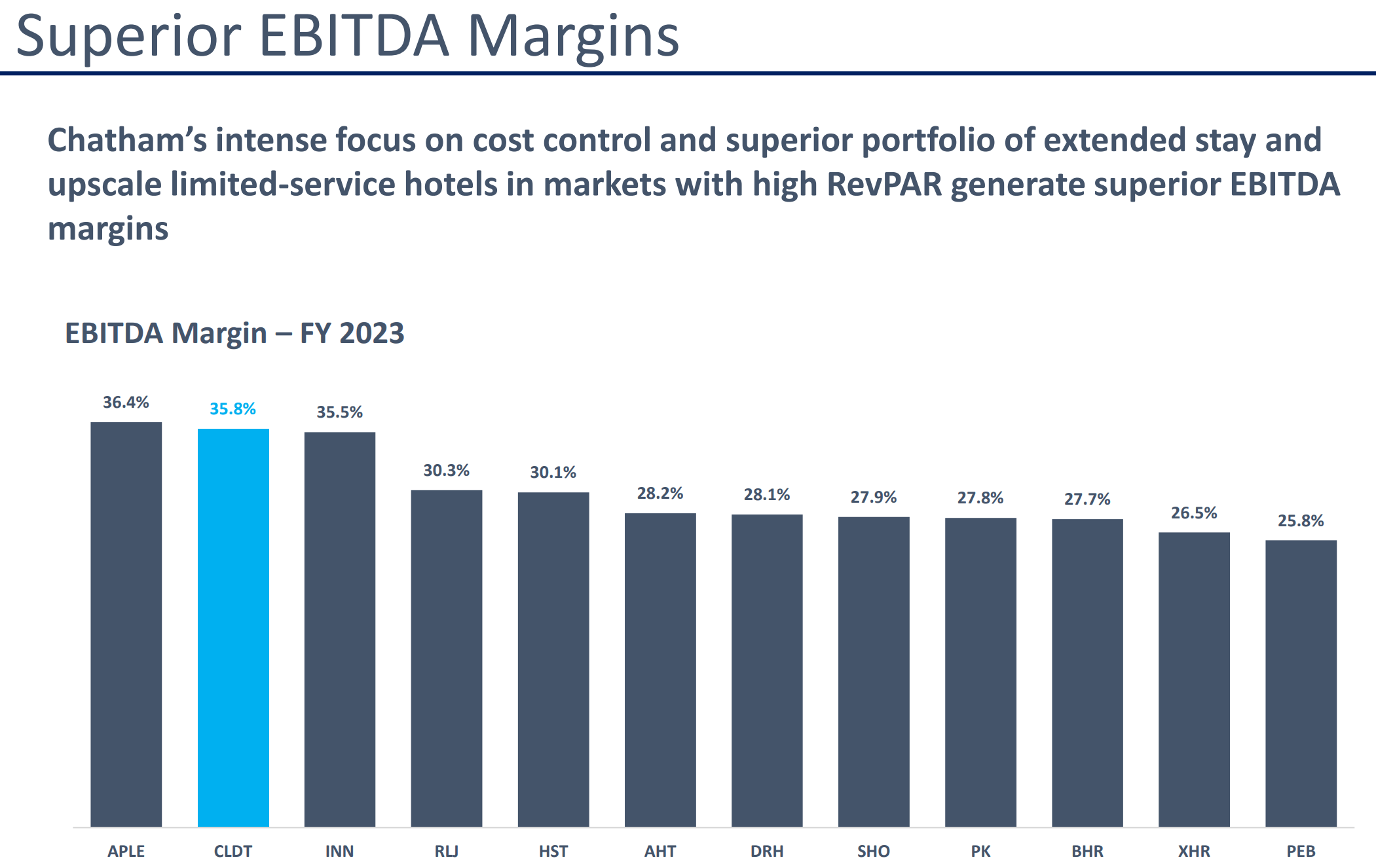

CLDT’s focus on select-service hotels enables it to achieve higher margins than most of its peers, due to lower operational costs. As shown below, CLDT boasts a superior Hotel EBITDA margin of 35.8%, comparing favorably to its two peers Apple Hospitality (APLE) and Summit Hotel Properties (INN) and sitting higher than the rest of the industry average.

Investor Presentation

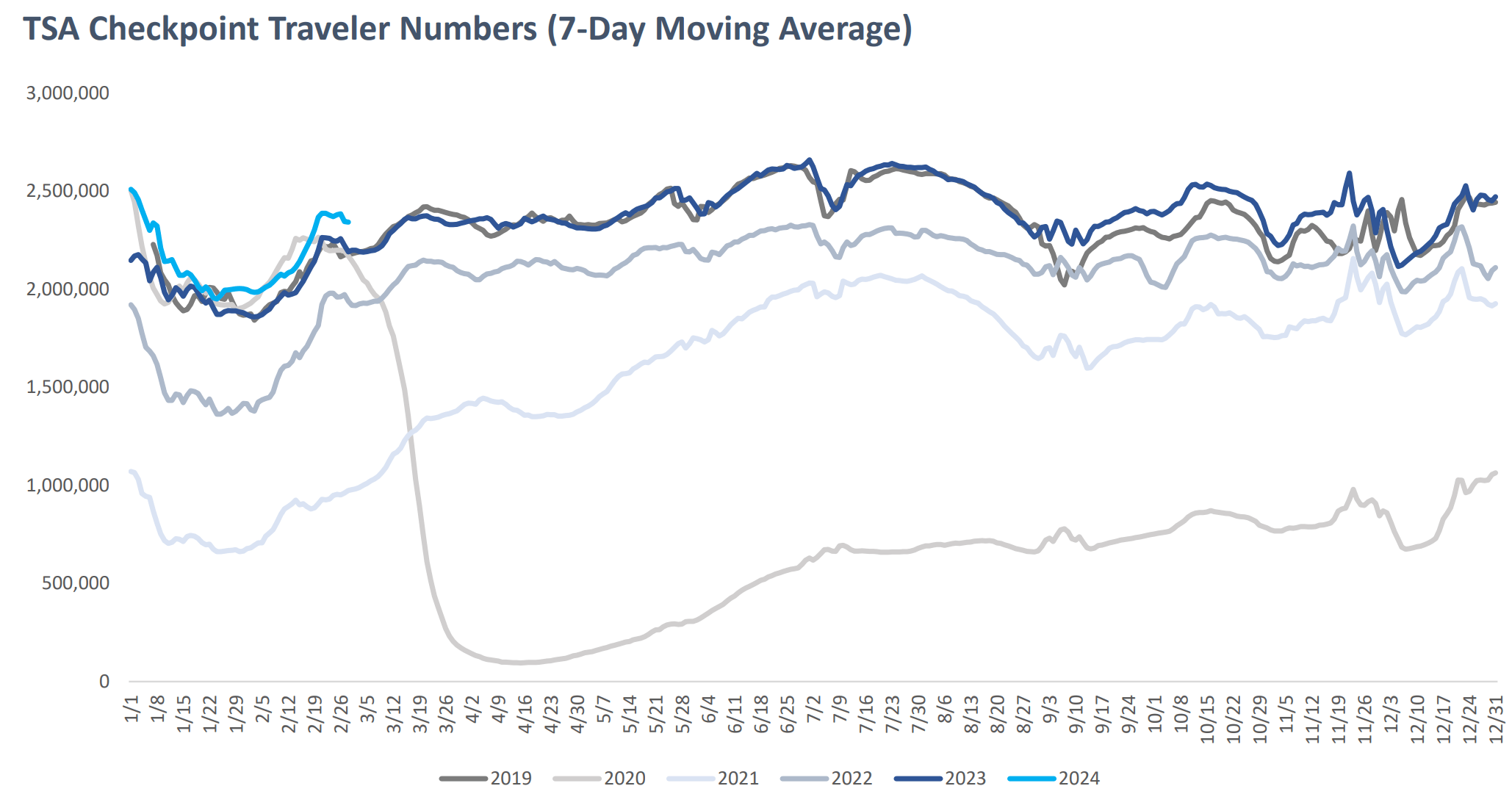

One of the top things in mind for any investor in Hotel REITs should be to see how travel is trending, and early numbers for 2024 are encouraging. This is supported by the following TSA Checkpoint Numbers, which shows the 2024 travel figures (blue line), particularly in early March, as being meaningfully higher than where it was in prior years including 2019 (pre-pandemic), as shown below.

Investor Presentation

CLDT’s Q4 2023 earnings, released on February 27th, indicate steadily improving operating metrics at its properties. This includes RevPAR (revenue per available room) rising by 2.5% YoY to $121, and this growth was almost double that of the hotel industry.

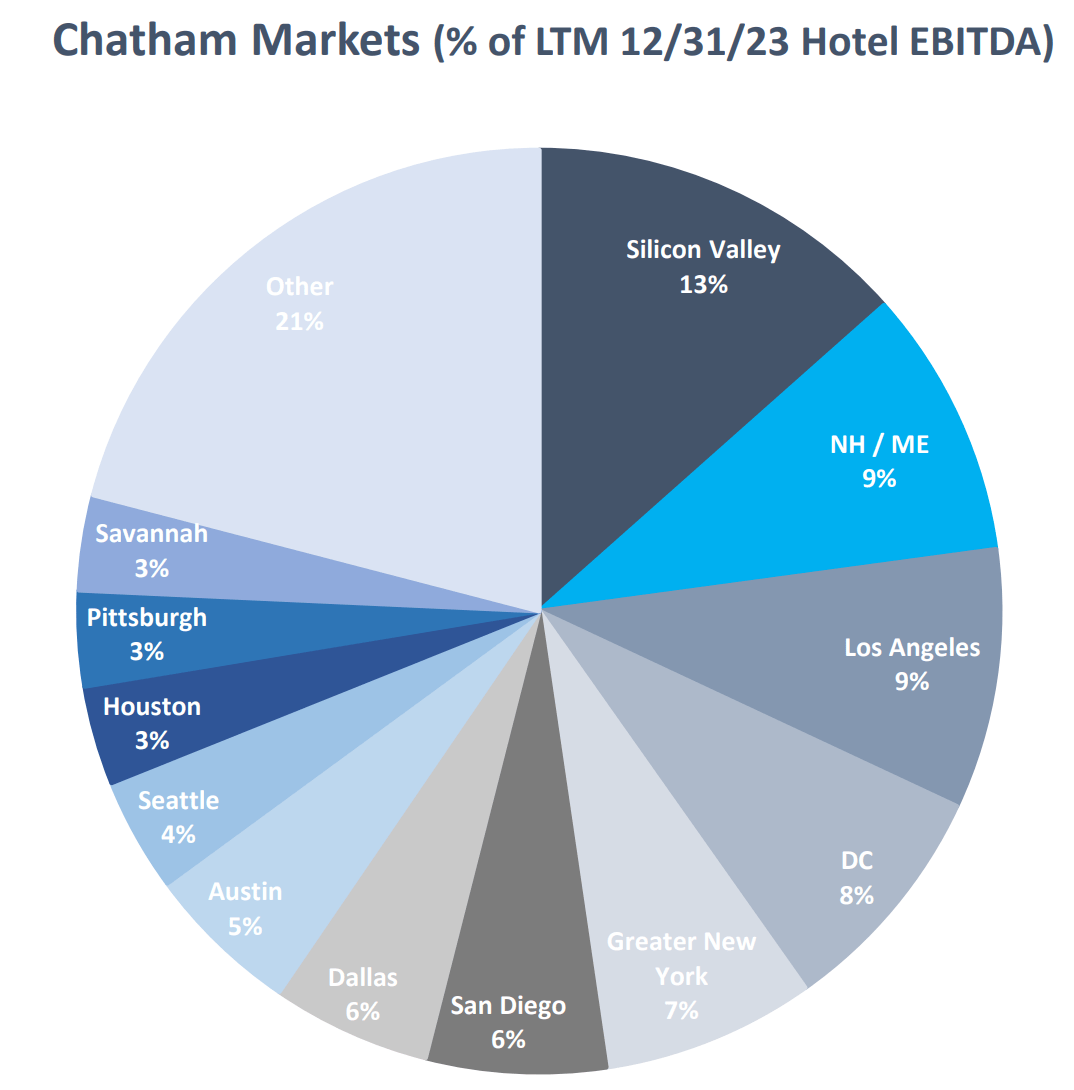

This was driven in large part by CLDT’s exposure to the technology industry with its properties in Silicon Valley and Seattle markets, as AI technology has been a key growth driver of the economy and the market this year. RevPAR growth for CLDT’s Silicon Valley and Bellevue properties grew by an impressive 14% YoY during Q4. As shown below, Silicon Valley and Seattle represents 17% of CLDT’s Hotel EBITDA.

Investor Presentation

For the full year 2023, CLDT saw a solid 6.1% YoY increase in RevPAR, which exceeded industry RevPAR performance by 25%. This was driven by all RevPAR growth in all but one of CLDT’s top markets. Notably, last year started off bumpy for the tech industry as a whole, as it was still reeling from layoffs from 2022 that spilled over into 2023, but the second half was driven by a very strong rebound due to AI-related companies such as Nvidia (NVDA) making huge gains operationally.

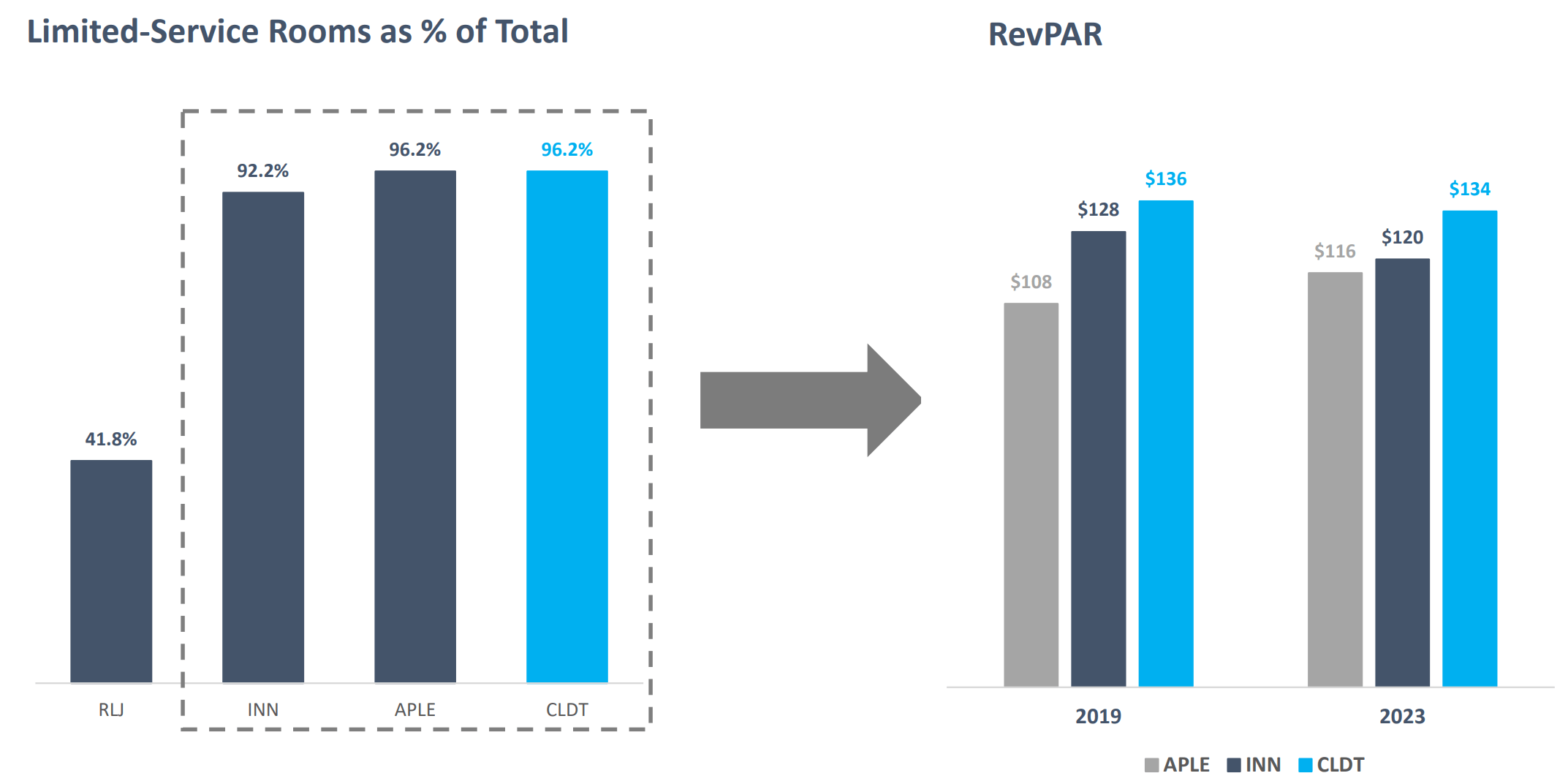

CLDT has benefited from this trend as its hotels are well-suited for business travel, given that has the highest exposure to extended stay rooms, representing 63% of total rooms. This compares favorably to the next closest peer, APLE, which has 32% extended stay. Plus, as shown below, CLDT’s 2023 RevPAR of $134 sits just shy of the $136 from 2019, representing faster recovery compared to its two closest peers, APLE and INN, due to CLDT’s higher exposure to tech-related markets.

Investor Presentation

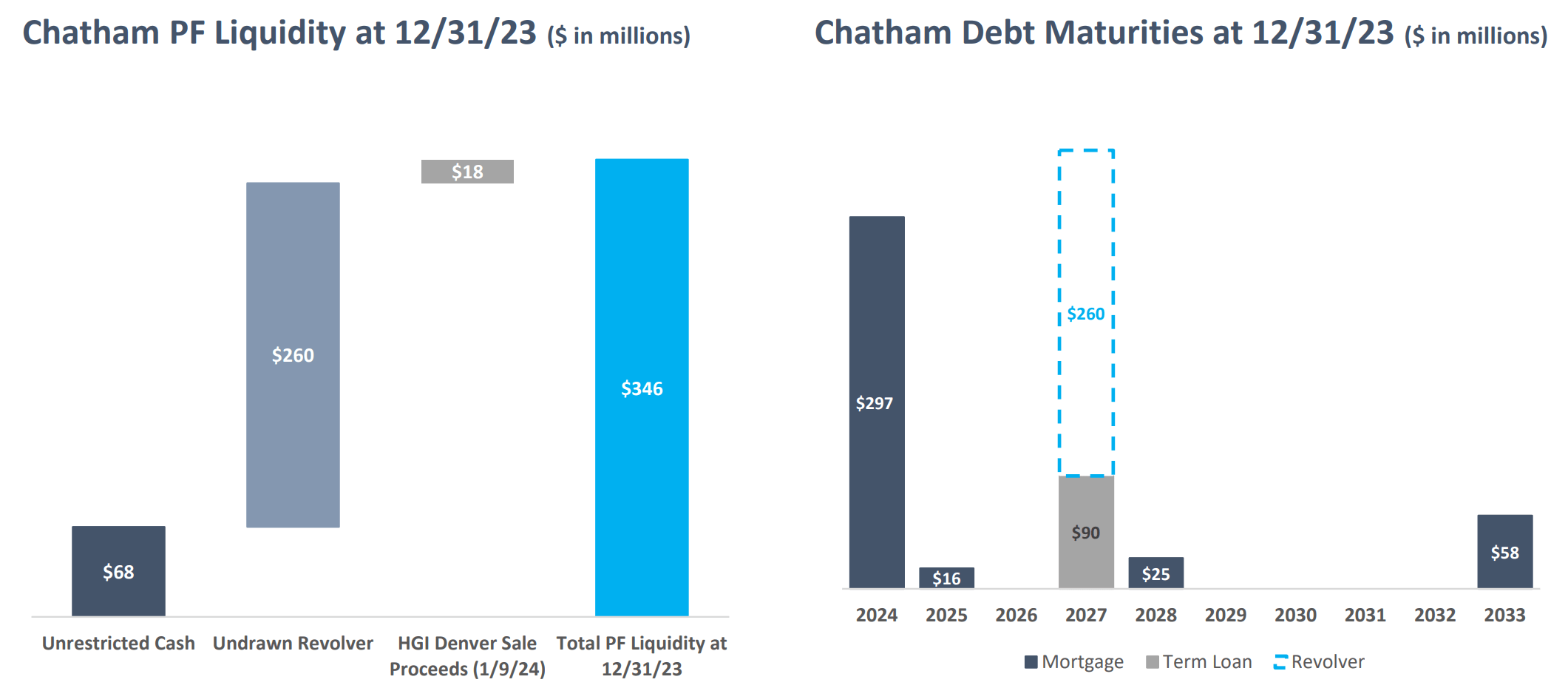

Moreover, CLDT also took steps to deleverage its balance sheet, as it reduced net debt by $26 million in 2023. It now carries a net debt-to-enterprise value of 40%, which sits below the 50% level that I generally consider to be safe for REITs, and carries a safe net debt-to-EBITDA ratio of 4.1x, sitting well below the 6.0x level generally considered to be safe for REITs.

It also has $346 million of liquidity, which more than covers the $297 million worth of debt maturities this year. As shown below, CLDT has low maturities in 2025 and no debt maturing in 2026, thereby giving it some breathing room with potential for interest rates to decline over the next couple of years.

Investor Presentation

Looking ahead, I would look for the health of the tech industry to continue to be bolstered by AI trends, as that would help CLDT’s exposure in Silicon Valley. Plus, return to the office also presents a potential tailwind for CLDT, as increased face-to-face engagement would likely result in higher business travel as well. Moreover, recent moves by big tech companies to expand their footprints could also serve as a catalyst, as noted during the recent conference call:

With AI driving a surge in tech investment, travel demand is building. Sunnyvale is becoming the epicenter of AI development. As previously disclosed, Applied Materials, which has forever been one of our top accounts in Sunnyvale, announced plans to build the EPIC Center.

That's the equipment and process innovation and commercialization center, which is a $4 billion, 180,000 square foot R&D facility only blocks away from our two Sunnyvale residence inns. Google's expansion into San Jose Downtown was delayed, but we're benefiting as they continue to expand their Caribbean campus as they call it in Sunnyvale.

Risks to CLDT include potential for a higher for longer interest rate environment, which raises long-term interest expense. Other risks include the cyclical nature of the hotel industry, which is sensitive to macroeconomic downturns. Businesses could pull back on travel spending should higher interest rates result in a pullback in consumer spending.

Importantly for income investors, CLDT currently yields 2.7% and the dividend is well-covered by a 24% payout ratio. CLDT’s quarterly dividend rate of $0.07 remains the same as when it reinstituted the dividend in Q4 of 2022. While CLDT’s current dividend rate is a far cry from its pre-pandemic rate there is potential for growth should interest rates stabilize or decline and with continued strength in the portfolio.

For those investors who prize a higher starting yield, CLDT’s Preferred Series A (NYSE:CLDT.PR.A) may be a better option, as it currently yields 7.7%. This series is cumulative, which means that missed dividend payments must be made up unless if CLDT becomes insolvent. At the current price of $21.52, this preferred stock also trades at a 14% discount to par value thereby giving it upside potential and call protection. Speaking of which, CLDT.PR.A’s call date is 6/30/2026, giving investors a long window to collect the dividends until then or even beyond, should interest rates remain elevated.

Turning to valuation, I continue to see value in CLDT at the current price of $10.21 with forward P/FFO of 9.1. At this valuation, CLDT is priced for low or no growth, which I don’t believe to be the case. While I wouldn’t expect bottom line growth this year, considering that material debt refinancing this year and higher interest rates, I believe CLDT is set up for long-term mid-single digit FFO/share growth as a base case scenario, considering its high margin profile and aforementioned catalysts in tech-driven economies. As such, I believe a P/FFO of at least 10x is fair, considering both catalysts and risks, thereby giving CLDT meaningful upside potential.

In summary, CLDT has shown strong performance over the past 12 reported months, particularly in the tech-driven markets of Silicon Valley and Seattle, thanks to its well-suited extended stay hotels and higher margin profile compared to peers. The company has also taken steps to strengthen its balance sheet and maintain a healthy liquidity position.

Looking ahead, the rise of AI trends and potential return to office could continue to benefit CLDT's exposure in these markets. While the dividend yield on the common stock isn't high, it does have meaningful upside potential due to the low payout ratio. Investors seeking an immediate high yield ought to consider the preferred stock, which trades below par value. Considering all the above, I view both the common and preferred series as good options for income investors in a well-diversified portfolio, and maintain a 'Buy' rating on both.