Bjoern Wylezich/iStock Editorial via Getty Images

Bjoern Wylezich/iStock Editorial via Getty Images

One sector that I lack exposure to is the basic materials sector. While I have adequate exposure to the energy sector, the basic materials remain elusive. As companies in the sector tend to be sensitive to price changes of commodities, most of them are unsuitable for dividend growth investors seeking reliable growth in sales and EPS. In this article, I will analyze Air Products and Chemicals (NYSE:APD), a leading dividend aristocrat in the sector.

I analyzed the company last year and found it to be a hold on valuation as the shares were trading for more than 24 times earnings. A year later, I am revisiting the company as I look for a market leader. This article will explain my BUY thesis for the company based on its better valuation and excellent growth opportunities in line with mega trends in the economy, mainly energy transition.

Seeking Alpha's company overview shows that:

Air Products and Chemicals provides atmospheric gases, process and specialty gases, equipment, and related services in the Americas, Asia, Europe, the Middle East, India, and internationally. The company produces atmospheric gases, including oxygen, nitrogen, and argon. Process gases, such as hydrogen, helium, carbon dioxide, carbon monoxide, syngas, and specialty gases for customers in various industries, including refining, chemical, manufacturing, electronics, energy production, medical, food, and metals. It also designs and manufactures equipment for air separation, hydrocarbon recovery and purification, natural gas liquefaction, and liquid helium and liquid hydrogen transport and storage.

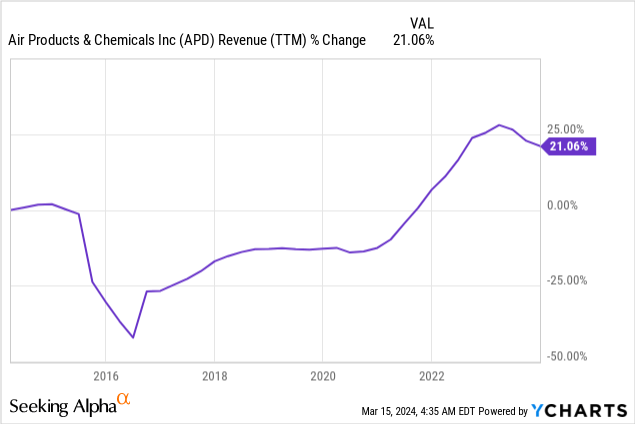

The revenues of Air Products and Chemicals are up only 21% over the last decade. The company has been realigning its portfolio over the previous several years to accommodate clients' needs better. It has been growing mainly organically and has also used some acquisitions to increase its global presence, mainly in Latin America. To focus on gases with high demand, the company also sold other divisions, such as its electronic materials. Therefore, while the sales grew slowly, the result is a much more focused company with higher margins. In the future, as seen on Seeking Alpha, the analyst consensus expects Air Products and Chemicals to keep growing sales at an annual rate of ~6% in the medium term.

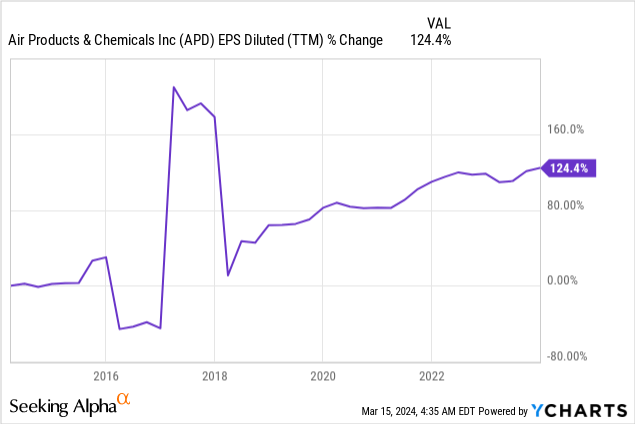

The EPS (earnings per share) of Air Products and Chemicals has grown at a much faster pace during that decade. With EPS up 124%, investors can see the success of the company's realignment. It did this by strategically focusing on gases, and it did it even with the share count being higher than it was a decade ago. The strategic shift allowed the company to focus on its core business, which enjoys higher margins. In the medium term, as shown on Seeking Alpha, the analyst consensus expects Air Products and Chemicals to keep growing EPS at an annual rate of ~9% in the coming years.

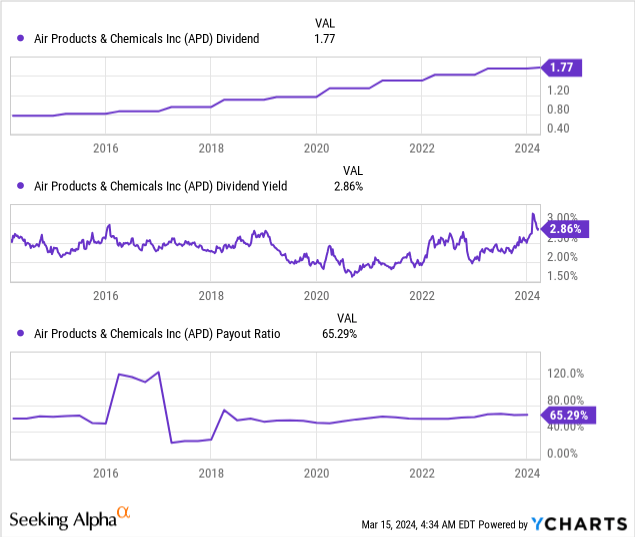

The company is leveraging its EPS growth to reward shareholders with a growing dividend. Air Products and Chemicals is a dividend aristocrat who has increased the dividend payment annually for 41 years. The latest increase was a 1% increase in January, which was smaller than the usual 9% average dividend increase it offered over the last decade. The company's payout ratio stands at 65%. Therefore, investors should expect mid-single-digit increases as the company lowers the payout ratio while investing heavily in new plants and projects.

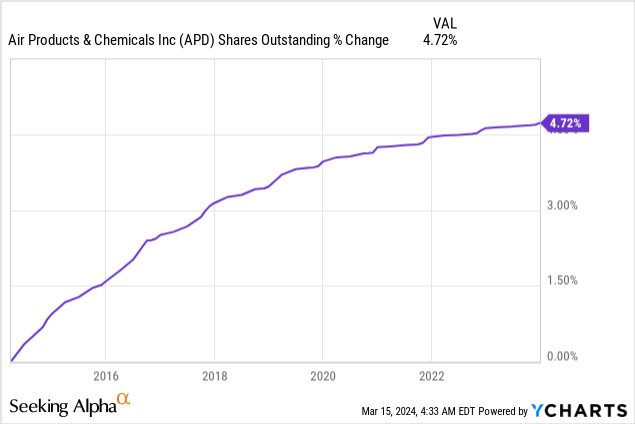

In addition to dividends, I always check whether companies return capital to shareholders via buybacks. Buybacks are an efficient way to return capital by supporting EPS growth. The EPS growth happens as the company decreases the number of outstanding shares. In this case, the company is not buying back shares, and the share count has increased by 4% over the last decade. This is not dilutive, primarily as the EPS has grown despite the share count increase. I hope the company will consider buying back shares when the valuation is attractive.

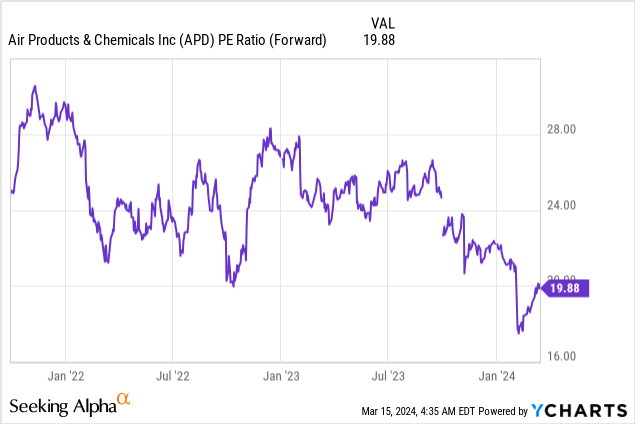

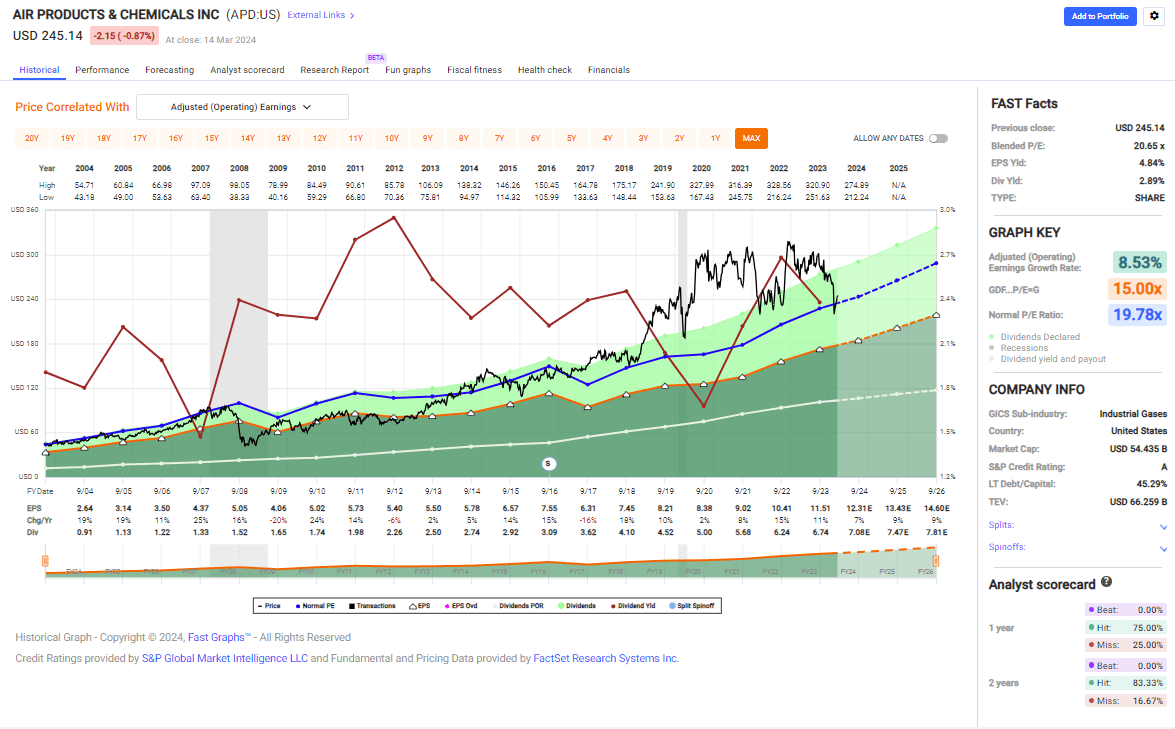

The P/E ratio of the company stands at 20 when using the 2024 EPS estimates. This is not a low valuation, especially in the current interest rate environment. However, this is almost the lowest valuation we have seen over the last twelve months. It is also 20% lower than the valuation I saw when I analyzed the company last year. I believe that since the company is a leading blue-chip in the sector, it deserves a rich valuation, and while the price is not cheap, it is decent.

The graph from Fast Graphs also shows that the company is currently fairly valued. The average P/E ratio of the company over the last two decades stands at 20, and the current one is also 20. The company's growth rate over the same period stands at 8.5%, which aligns well with the current forecasts for a 9% growth rate in the medium term. Therefore, investors have a decent and fair entry opportunity to a company that has been on the expensive side for more than five years in a row.

Fast Graphs

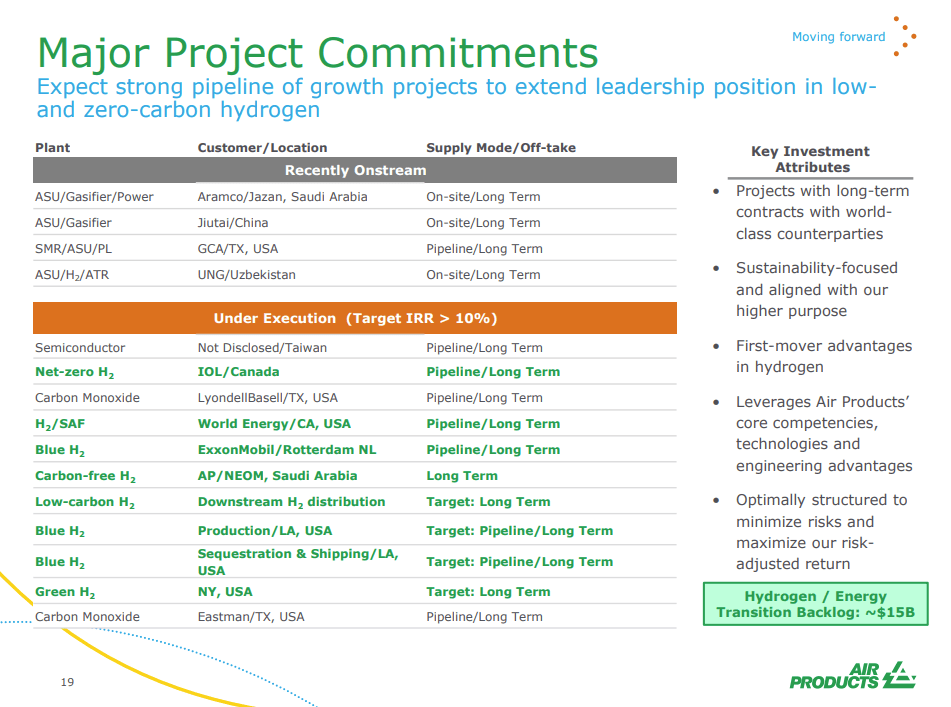

The company's most significant growth opportunity beyond its core is hydrogen and carbon capture expansion. Green hydrogen is the cleanest version of hydrogen, made of water. Blue hydrogen is made of natural gas and thus requires carbon capture to avoid emissions of greenhouse gases, mainly CO2. The company is active in these fields and the sustainable aviation fuel. It operates for companies such as Exxon Mobil's hydrogen projects as the world is transitioning into a greener period in terms of energy sources. The current hydrogen and energy transition backlog stands at $15B.

"Air Products is pursuing a first mover growth strategy with our core industrial gases business as the first pillar and our blue and green hydrogen projects as the second pillar."

(Seifi Ghasemi, Chairman, President and Chief Executive Officer, Q1 2024 conference call)

Air Products and Chemicals

The second growth opportunity for the company is that Western countries wish to keep the supply chain in their territories. So not only do they invest in new and renewable fuels such as hydrogen, but they also build new plants in Europe and North America. Therefore, we see a 28% increase in adjusted EBITDA in Europe. As developed markets invest heavily in the energy industries in their territory, Air Products and Chemicals will benefit. The chart above also emphasizes the number of new projects in the U.S., Canada, and Europe.

"Our results in Europe are excellent, the margins are up 1,000 basis points, and that is because people have done a good job hanging on to the price while energy prices are going down."

(Seifi Ghasemi, Chairman, President and Chief Executive Officer, Q1 2024 conference call)

The last growth opportunity is the strict capital allocation policy that the company adopted. The company focuses on core gases and hydrogen, so it doesn't take any project. It focuses on the ROI (return on investment), and that's how it managed to increase the EPS by 120%+ while the sales were up only 21%. This strategy allowed the company to initiate various new projects simultaneously while also returning capital in terms of dividends. The company managed to more than double its capex to create future cash flow while maintaining growth of EPS and dividends.

"Creating Shareholder Value: cash is king; long-term increase in per share value of our stock; capital allocation is the most important job of the CEO"

(Investor presentation, Q1 2024 conference call)

"We expect to return approximately $1.6 billion to our shareholders in 2024, while continuing to execute hard return industrial gas and clean hydrogen projects."

(Seifi Ghasemi, Chairman, President and Chief Executive Officer, Q1 2024 conference call)

While there are some up-and-coming growth opportunities in developed markets, primarily based on hydrogen and energy transition, there are also risks to the investment thesis in Air Products and Chemicals. The company is facing some severe headwinds in China and the Asian markets in general. This is the result of slower economic growth in China. China is a leader in energy transition and invests heavily in hydrogen. If its growth slows, it may hinder the company's growth rate.

"These factors that affected our guidance are: number one, larger than anticipated volume headwinds from weak economic growth in China."

(Seifi Ghasemi, Chairman, President and Chief Executive Officer, Q1 2024 conference call)

Moreover, the company sees some weakness in its core gases core business. The weakness is seen mainly in Helium, where the company suffers from a decrease in volume due to lower demand from the global electronics market. This weakness has caused the company to initiate a weaker-than-anticipated guidance. If it continues, the growth rate may slow, making it harder to justify the current valuation.

"Lower helium demand in electronics especially across the world."

(Seifi Ghasemi, Chairman, President and Chief Executive Officer, Q1 2024 conference call)

To conclude, Air Products and Chemicals is one of just a few dividend aristocrats in the primary materials sector. This is a highly volatile sector. Therefore, building a long track record of dividend growth is complex here. The company offers strong fundamentals with sales and EPS growth, fueling dividend growth for over 40 years. These great fundamentals come with some very promising growth opportunities for the company. It seeks growth by leveraging the megatrend of energy transition that we see across the globe.

The growth initiatives are focused on developed markets, mainly around hydrogen (green and blue). There are risks to the thesis, primarily weaknesses in China that affect the entire Asia area. However, I believe that the company is trading for a fair valuation, and while the margin of safety is not comprehensive, it is enough to initiate a position. Therefore, I believe that Air Products and Chemicals is a BUY. More cautious investors may want to consider buying shares gradually over the next several months if the share price drops.