onurdongel

onurdongel

There is nothing better than having a number of stocks in your portfolio that increase their dividend like clockwork. There are plenty of people who don't invest in boring stocks, while I think we should embrace boring sometimes. Companies that are dominant in their sector and have a proven business model. These companies keep growing earnings and can almost guarantee dividend increases despite the influence of the economic cycle.

One of my own top 5 holdings is A. O. Smith Corporation (NYSE:AOS). The company doesn't get the attention it deserves. In my view this is unjustified, because the long-term results are exciting.

AOS total return (YCharts)

For the dividend growth investors who have a lot of time on their side, there is a lot to like as well. The dividend yield is "just" 1.49% at the moment but that's just because of its share price appreciation.

AOS dividend summary (Seeking Alpha)

With a 5Y dividend growth CAGR of 9% and a healthy pay-out ratio of 31.9% there is no sign of weakness. I even think the company has serious dividend king potential.

Today I want to update my investment thesis for the company using the latest information.

Why invest in AOS? I will give you a summary of why you should take a look at the company. For people who are interested in additional information about AOS, you can read my previous article via this link.

AOS strategy (AOS investor day presentation)

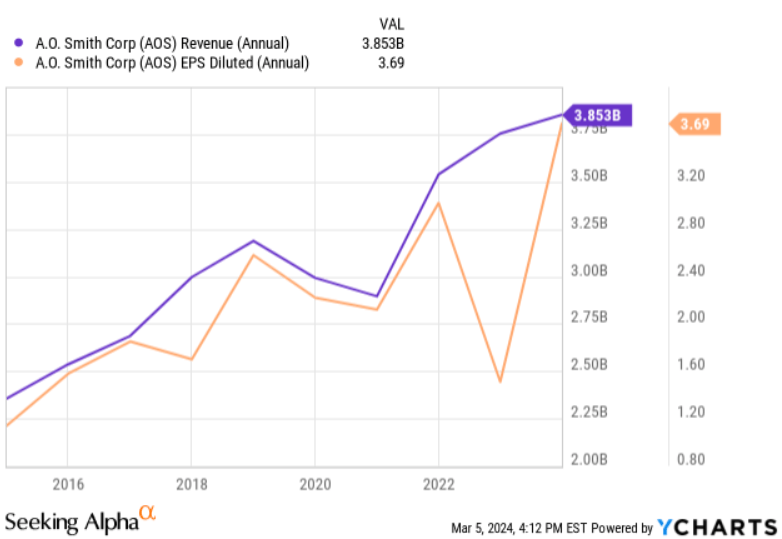

Revenue and EPS development (YCharts)

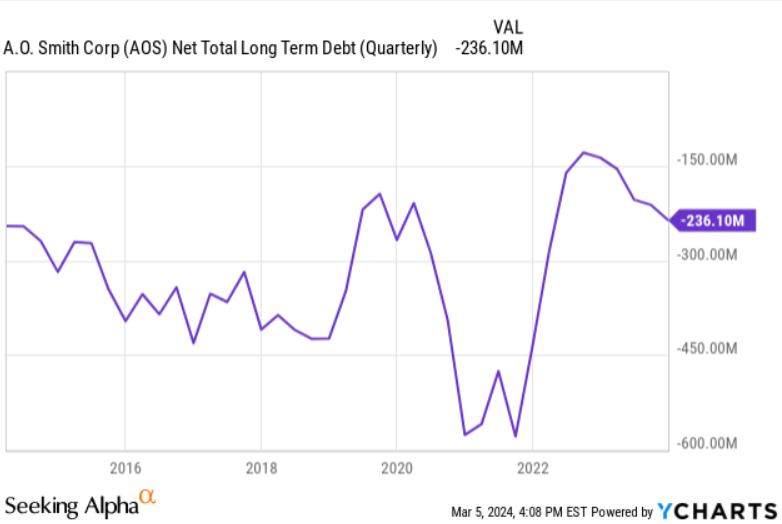

AOS net debt development (YCharts)

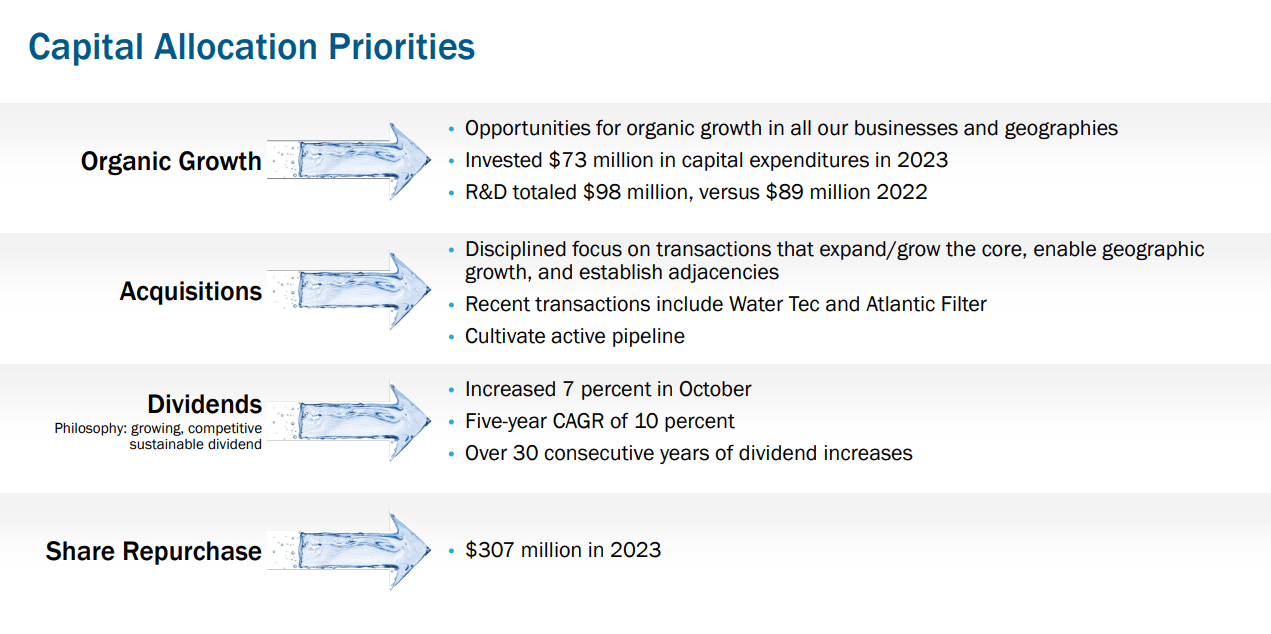

AOS capital allocation (Investor day presentation)

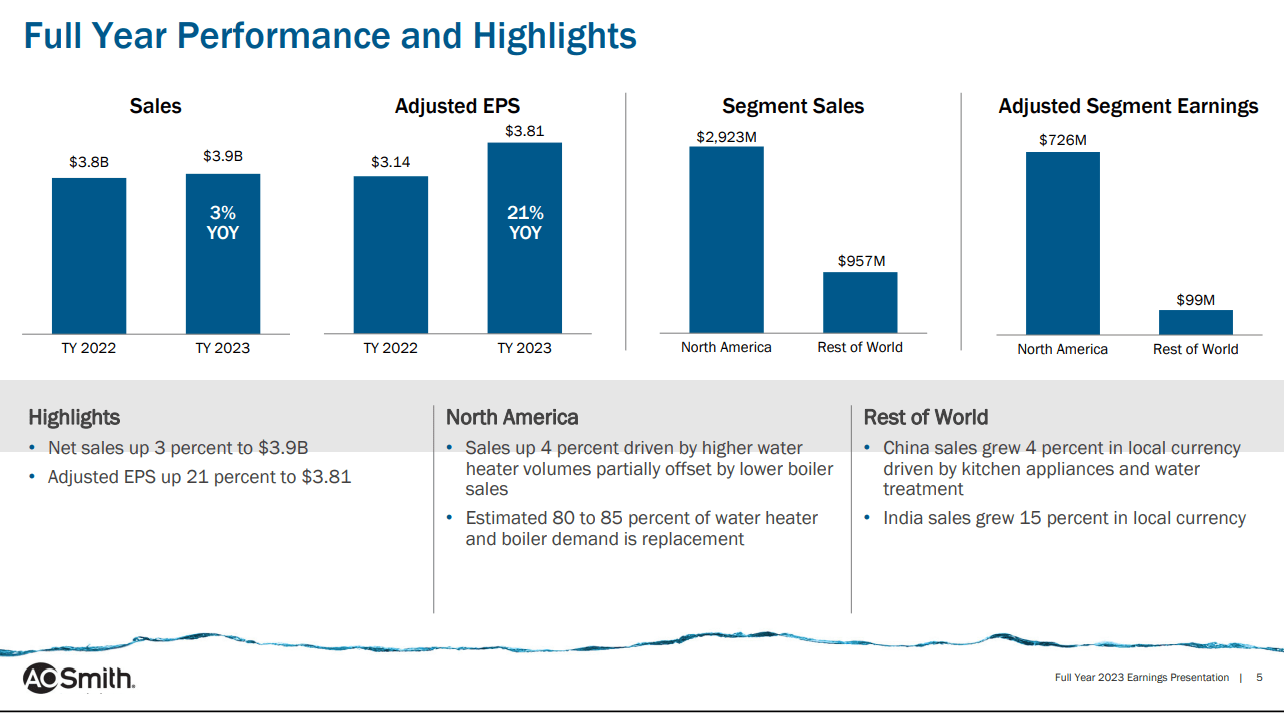

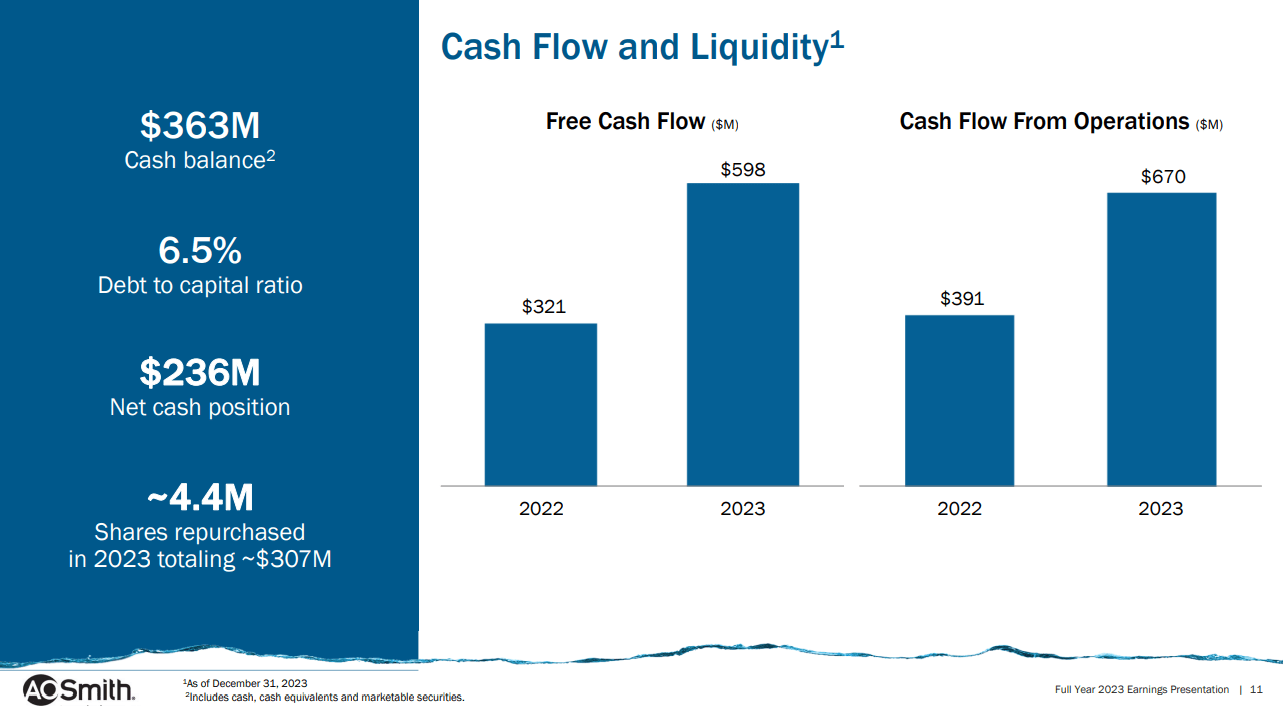

AOS has managed to deliver excellent full year results.

AOS FY 2023 performance (Q4 2023 presentation)

In FY 2023 the total sales increased 3% and their margins increased as well due to an improved price cost relationship. The North America segment increased 4% YOY, because of higher volumes in water heaters. The "Rest of the world segment" went down 1% due to currency headwinds, this was mostly China-related. Despite a weak economy in China, AOS is growing sales again with 4% in local currency. New kitchen products in China were received very well. Sales in India are growing fast, 15% in local currency. This growth is equivalent to 3x the market.

EPS is also growing rapidly, the adjusted EPS was a whopping 21% higher compared to FY 2022.

What is also remarkable is AOS's FCF growth, which is significantly higher compared to FY 2022 due to higher profitability.

Free cash flow (Q4 2023 investor presentation)

This allows them to continue what they do so well, namely investing in further growth, buying back shares and growing their dividend in a sustainable way.

For FY 2024, AOS predicts sales growth of North America water treatment products to increase approximately 10% to 12%. They are planning to do some price increases in water heaters. This is around 8% and will be effective in Q1. AOS is also expecting new growth in their North America boiler business of 8-10%.

They also expect 3-5% growth in China, due to resilient replacement demand and their success in their water treatment- and kitchen products. Growth in India remains good and growth of 15% is expected for the coming year.

However, they expect a lower amount of FCF compared to FY 2023 ($598 million vs $525-$575 million). This is based on the fact that steel prices are likely to be higher in FY 2024. Also CapEx will be higher compared to FY 2023, which impacts FCF as well ($65 million vs $105-115 million).

AOS does expect to repurchase $300 million of its own shares and it is expected that the dividend will be increased again.

FY 2024 outlook (Q4 2023 presentation)

In other words, next year will be looking very similar compared to FY 2023. From an FCF point of view, things are looking a little bit less attractive.

What consequences does this have when it comes to the valuation of AOS?

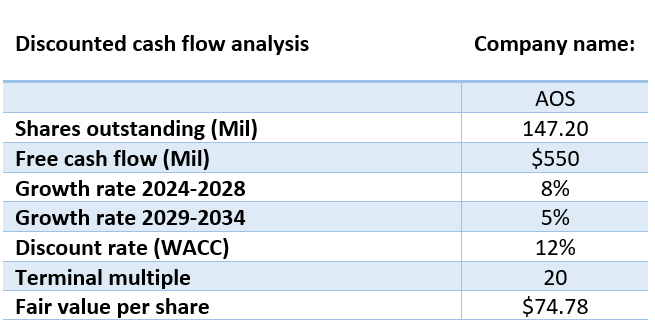

To calculate the intrinsic value of AOS, I used discounted cash flow analysis. The expected FCF for FY 2024 should be in the $525-$575 million range. I have confidence in management, and I used $550 million for my calculations.

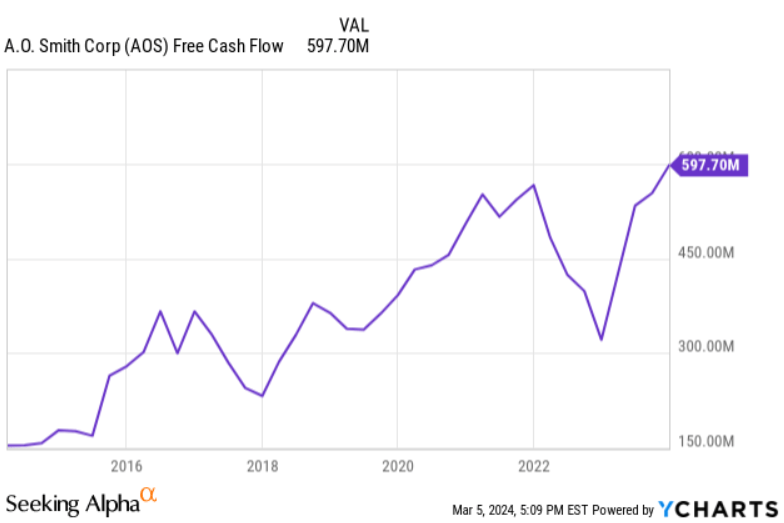

FCF development (YCharts)

As you can see from the chart, AOS's growth in FCF is lumpy, but over the long term, they show healthy growth. The company achieved a 5Y FCF per share CAGR of 10.9% and 10Y CAGR of 14.9%. FCF will drop a bit next year but growth prospects are still strong. I think a 5Y free cash flow growth assumption of 8% is reasonable and 5% for the 5 years thereafter, because it is more difficult to make assumptions further into the future.

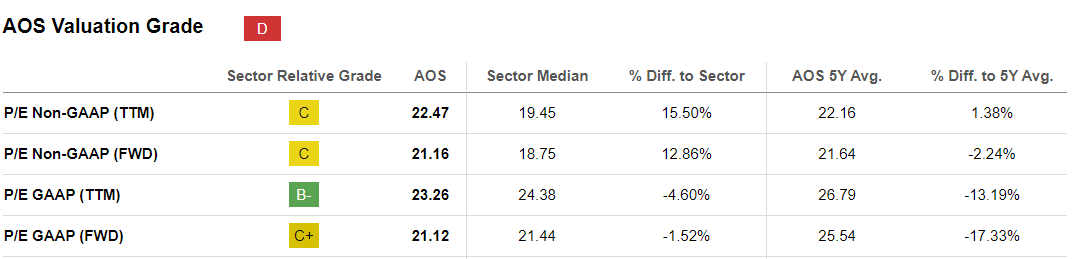

At the moment, AOS has a PE non-GAAP of 22.47, which is still a bit above its 5Y average of 22.16. From a PE GAAP point of view, the company trades below its 5Y average.

Valuation metrics (Seeking Alpha)

I used a PE of 20 as a terminal multiple, because AOS is a high-quality business where I think this multiple can be justified. Finally, I used a discount rate of 12% as a minimum rate of return.

DCF (Google spreadsheets)

If we do the math, this comes to a fair value of $74.78 per share. Comparing it to the current share price of $85.82 it is 14.7% overvalued.

AOS is a quality company and continues to do what they have been doing for decades. The company has done well over the past year and its free cash flow is currently at a record high. They will continue to invest in new growth, but will have sufficient capital to continue to buy back shares and increase the dividend. The last dividend increase of 7% was on the conservative side, but from a dividend growth investment point of view, this is in my opinion a SWAN stock. Free cash flow isn't likely to grow much in FY 2024, but with a long-term mindset, there are plenty of opportunities for AOS to continue to grow.

In my opinion, the stock is currently overvalued, but it's definitely worth putting the company on your watchlist. It is always possible that market sentiment may change or AOS may disappoint in the short term. AOS has shown in the past that it can be very volatile. In 2022, it already stood at $80, but has since fallen below $50 dollars per share.

AOS Share price volatility (Seeking Alpha)

It is therefore possible that AOS could fall significantly below my calculated fair value. These are usually opportunities to add these types of stocks to your portfolio.

Of course, there are also several investment risks to mention. AOS needs to keep innovating and investing to maintain its dominant position. Competition that can possibly make better use of the most up-to-date technology can have a negative impact on the position of AOS. When it comes to profitability, AOS is dependent on the steel price. If this rises sharply, this could have a significant impact on profits. Doing business in China can be both an opportunity and a threat. Geopolitical tension between America and China can complicate activities and impact profitability. In addition to this, AOS has a goal of achieving margins of 14-15% in the "rest of the world" segment, which is currently 10-11%. China has the biggest impact on this (22% of total sales in FY 2023), but the current economic condition is disappointing to say the least. There is still turmoil in the Chinese real estate sector, which could mean that people might invest less in AOS's products or choose other, more cheap alternatives. The company is therefore really dependent on economic recovery, and this could make the margin expansion too ambitious.

At this point in time, I give AOS a "HOLD", but it wouldn't surprise me if AOS falls closer to or below my calculated fair value in the event of a setback. This would be an excellent time for the dividend growth investor with a long-time horizon to add to his position.