gorodenkoff/iStock via Getty Images

gorodenkoff/iStock via Getty Images

Hewlett Packard Enterprise Company (NYSE:HPE) reported a relatively lackluster start to FY24 as the firm remains on the sidelines as a result of customers not having their data centers prepared for the new infrastructure purchased throughout FY23. This posed a major challenge to revenue growth that management expects to continue through the duration of 1h24. Despite the second half of the year being the typical swing to higher cash generation for HPE, I anticipate eFY24 to be underwhelming to management's expectations with eFY25 continuing a less optimistic course. I provide HPE shares a SELL recommendation with a price target of $14.38/share at 3.38x eFY25 EV/aEBITDA.

HPE is currently experiencing a significant tailwind as a result of AI adoption as seen across competing server manufacturers and GPU designers alike. HPE faced a significant amount of challenges in q1'24 as the firm worked through the heightened interest for AI-enabling infrastructure. One of the challenges involved sourcing Nvidia GPUs as the semiconductor designer experienced exceptionally strong demand for higher compute speeds. This is a matter that Taiwan Semiconductor (TSM) is addressing by doubling their CoWoS capacity to cater to this heightened demand. Another challenge was implementation preparedness in which customers didn't have the proper infrastructure in place to begin utilizing these high-performance server racks. This is something that has been addressed by Super Micro Computer (SMCI) in their q2'24 earnings report as the firm is being faced with scaling challenges and will be expanding and building new facilities to resolve these bottlenecks. These challenges aren't necessarily something new as the infrastructure purchases had occurred in q1'23. The purchases and constraints may create additional pressure to HPE's growth as refresh cycles will now be further pushed back, resulting in potentially softer demand in the coming quarters and possibly through e1h25. Many of these constraints have led to HPE building a $3b backlog that the firm will be converting into revenue throughout eFY24 & eFY25.

Another challenge HPE faced in q1'24 was a softer market for networking equipment. This isn't an isolated instance as many chip designers such as Marvell Technology (MRVL) have voiced similar headwinds. Contrary to HPE's networking challenges, companies like Broadcom (AVGO) and Arista Networks (ANET) posted strong q4'23 growth, which may suggest that there is demand for networking infrastructure; it just has to be the right technology. Gartner's CY24 forecast called for a modest 3.3% growth in communications services and 9.5% growth across data center systems, which makes me believe that there may be some shift in networking equipment from more traditional to AI-enabled and the software-defined networking equipment that Arista has to offer. The research firm suggested that CIOs will focus on short-cycled, cost-cutting projects, which I believe will be mostly focused more on software and infrastructure additions rather than replacements. Considering that the majority of HPE's revenue growth challenges were the result of their customers' ability to source and implement vs. the sales cycle, I have reason to believe that these challenges may persist for longer than another quarter.

Despite the growth challenges, HPE did experience some operational tailwinds as a result of cost management and ARR improvements. Though the firm gained some ground in margins in q1'24, management hinted that q2'24 may not experience the same benefits and that margins may be pressured resulting from cost-reducing programs taking longer to circumvent. Management anticipates OPEX headwinds in the range of $200-250mm, significantly lower than their original forecast of $300mm. Though optimistic, I believe management is too ambitious on their topline forecast in which the GPU bottleneck shouldn't be expected to be resolved until the end of CY24, as discussed in my report covering Nvidia.

Management anticipates generating at least $1.9b in free cash flow for eFY24, which, considering their current trajectory, is very feasible. As management had alluded to in their q1'24 earnings call, the second half of the year is the primary time for positive free cash flow generation with q4 expected to be the bulk of cash generation. Modeling this out, I anticipate a deeper sequential use of cash for eq2'24 with a gradual turn in eq3'24 and a greater impact in eq4'24. I anticipate eq3'24 to remain constrained when compared to the previous year's period with stronger cash generation in eq4'24 as I anticipate many of the exogenous bottlenecks should be resolved.

Corporate Reports

Looking forward, management anticipates stronger margins as more of the revenue mix is derived from their as-a-service offerings. Much of this will be captured through their cloud-native offerings and AI applications, which I believe will drive significant revenue growth while being offset by legacy hardware across compute and storage. As more firms turn to a consumption-based model for AI/ML hosting, I believe there can be some tailwinds as demand for more compute speeds and power are necessary.

Corporate Reports

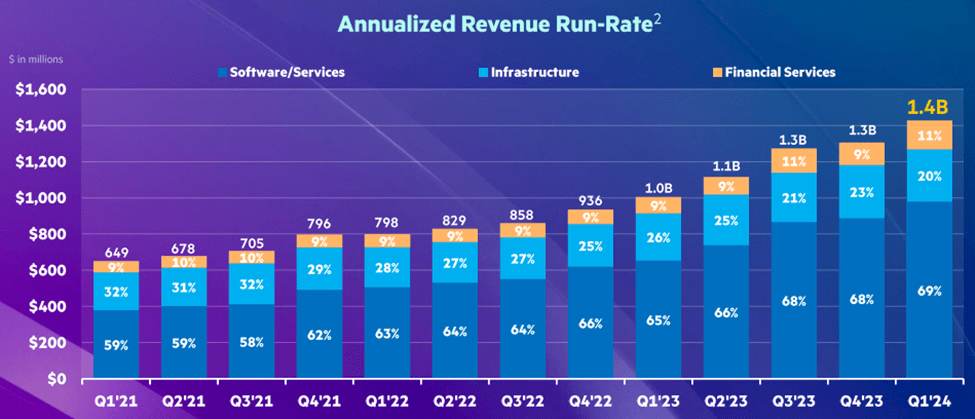

Management forecasts significant ARR growth with an expected 35-45% CAGR. This should be highly accretive for HPE's margins going forward as software services tend to be paired with lower operating costs. I do anticipate this to be somewhat cannibalistic to other offerings, however, as customers shift product mix into that more consumption-oriented offering.

Across HPE's segments, Server experienced the most severe decline in revenue as customers face slower implementation rates. The segment's revenue declined by -23% from the previous year. I anticipate that Server may remain a laggard for the duration of eFY24. Intelligent Edge grew by 2% with ARR increasing 77% y/y. This segment should drive margin expansion going forward as more customers turn their attention to utilizing AI/ML across their enterprises. Hybrid Cloud declined by 10% y/y with a 200bps decline in operating margin. This segment is expected to experience some tailwinds with their new hyperscaler customer choosing to use their HPE GreenLake offering. Financial Services experienced a 2% decline in the quarter as customers face higher financing costs. This factor plagued Palo Alto Networks (PANW) in their q2'24 earnings release as customers opted for shorter-duration contracts or creative financing solutions. These same factors may impact HPE in eFY24 as well as customers remaining sluggish to refresh their infrastructure.

Despite my bearish sentiment towards operations, there may be some positive catalysts on the horizon to take into consideration, including the debottlenecking of Nvidia's GPU manufacturing by TSM, exceptional interest in building out infrastructure capabilities to support AI/ML applications, and the merger with Juniper (JNPR) that may bring in stronger networking and cybersecurity capabilities to HPE.

Corporate Reports

HPE shares currently trade at 3.41x TTM EV/aEBITDA, falling towards the top end of their historical trading range. Given my expectations for some operating metrics to fall short of expectations, I believe HPE shares are relatively overpriced and will experience a further pullback.

HPE does pay a quarterly dividend, annualized at $0.52/share. In total, HPE returned $172mm in the form of dividends and share repurchases in q1'24. This breaks down to $3mm in repurchases and $169mm in dividends. Given my expectations for future cash flow generation, I do not anticipate HPE to make major strides in share repurchases in the coming year. Compared to q1'23, HPE's repurchase allocation declined by 96% from $73mm.

Corporate Reports

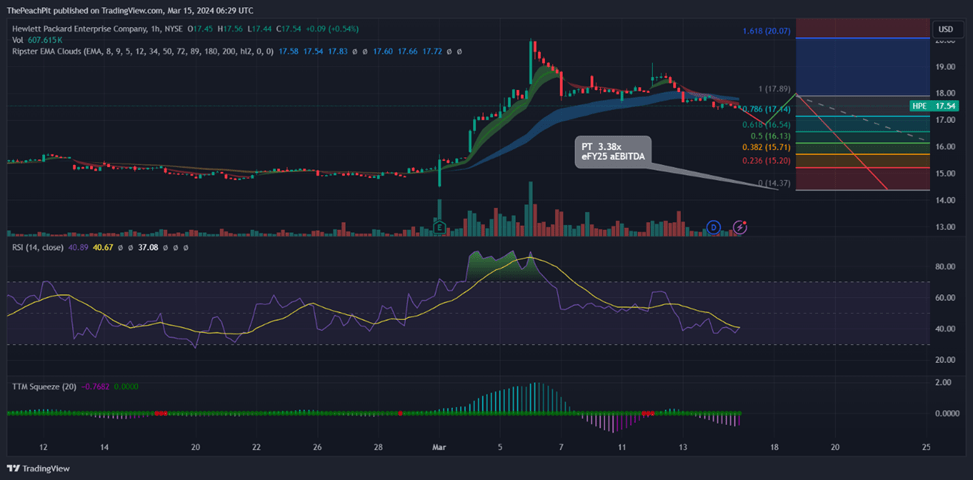

Charting out the share price out, we may experience an additional swing before shares route course for my bearish price target of $14.38/share. Considering the Ripster EMA Clouds, HPE shares appear to be entering a bearish trend. With the expectations that HPE underwhelms the market in future periods, I provide HPE shares a SELL recommendation with a price target of $14.38/share at 3.38x eFY25 aEBITDA.

TradingView