Luke Sharrett/Getty Images News

Luke Sharrett/Getty Images News

Alpha Metallurgical Resources, Inc. (NYSE:AMR) is a leading U.S. met coal producer. According to Alpha, AMR accounts for 20% of total U.S. metallurgical coal production. It exports more than 70% of its production, making Alpha a crucial partner for its customers in more than 25 countries worldwide.

Keen AMR followers should be aware of the differences between thermal coal producers and met coal leaders like Alpha. While Alpha has thermal coal production in its portfolio, met coal is the most significant growth driver in Alpha's shipments. Therefore, the company is mainly exposed to the steelmaking industry, which plays a pivotal role in supporting the renewable energy players. As a result, Alpha is well positioned to leverage its scale and market leadership to exploit the long-term secular demand dynamics in met coal.

Accordingly, Alpha guided for total met coal shipments of between 16.4M and 17.8M tons for FY24. In addition, Alpha telegraphed that it had received a rice commitment comprising 35% of its met coal based on an average price of $171.33 per ton. With costs between $110 and $116 per ton, Alpha seems well-placed to continue raking in solid profitability, notwithstanding recent weaker sentiments.

Accordingly, AMR surged to an all-time high at the $452 level as Alpha posted its fourth-quarter earnings release and forward guidance at the end of February 2024. That proved to be a "sell the rip" opportunity, as AMR has since plunged into a bear market, falling more than 35% through last week's lows. As a result, I believe it's timely for Alpha investors to reassess whether the recent bear market offers an opportune moment to capitalize on weakness before it resumes its rally.

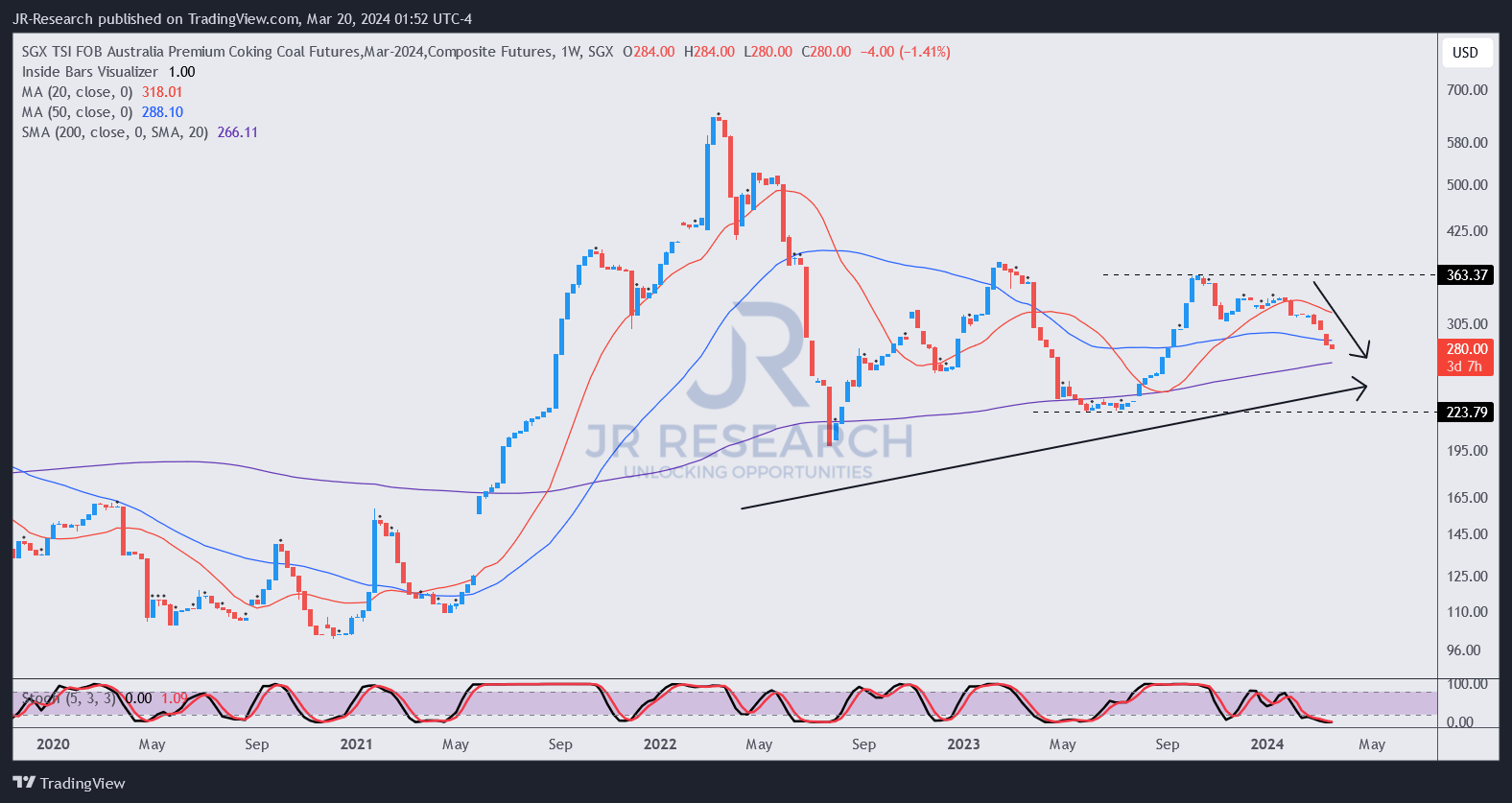

Australia premium coking coal futures price chart (weekly, medium-term) (TradingView)

As seen above, the market dynamics gleaned from the Australia premium coking coal futures price chart remain constructive. While volatile, the market remains in a medium-term uptrend. However, there's a clear pullback from its October 2023 highs, although AMR only observed significant downside volatility over the past month. Despite that, I have not observed the need to be unduly worried about the growth normalization as Alpha prepares for more challenges ahead.

One of the critical drivers of Alpha's shareholder value over the past two years is its generous buyback program. Considering its market cap of just under $4B currently, Alpha has repurchased about $1.1B in shares since its program inception in March 2022. With slightly above $400M left in its current authorization, the company indicates in its FQ4 earnings that Alpha will "reduce the cadence of share buybacks over the next few months." Alpha management highlighted its priority to "build cash balances back to targeted levels."

I believe the caution then is apt, as Alpha needs to be cautious about buying back shares unless a highly attractive opportunity presents itself. Alpha also indicated that it remains flexible in its capital allocation when deploying its cash for buybacks, "subject to cash levels and market conditions."

However, as a commodity producer, Alpha must balance that need with the current opportunities and challenges in the underlying market. Management believes that demand dynamics for met coal remain favorable, suggesting "global demand for coal used in high-quality steel production is expected to exceed supply."

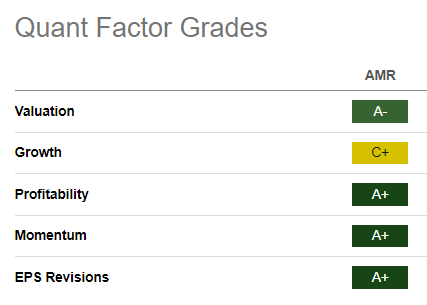

AMR Quant Grades (Seeking Alpha)

Notwithstanding the recent caution, AMR's Quant Grades remain highly favorable, supporting robust buying sentiments. Its valuation grade corroborates my observation of solid buying support at the $290 level as AMR plunged from its February 2024 highs.

With $400M remaining in its authorization, I would be pleased if Alpha management capitalized on the recent bear market to execute more buybacks to benefit shareholders. Despite that, Alpha's growth opportunities as a key producer and supplier of met coal to the steelmaking industry are expected to remain robust.

Rating: Initiate Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!