Diy13

Diy13

Antero Midstream (NYSE:AM) expects to generate approximately $690 million in free cash flow before dividends and $255 million in free cash flow after dividends for 2024. This is a bit better than what I previously expected in November 2023 and is also better than the $155 million in free cash flow after dividends that it reported in 2023.

The increase in free cash flow is driven by a combination of reduced capex, fee adjustments due to inflation and the end of the fee rebate program with Antero Resources.

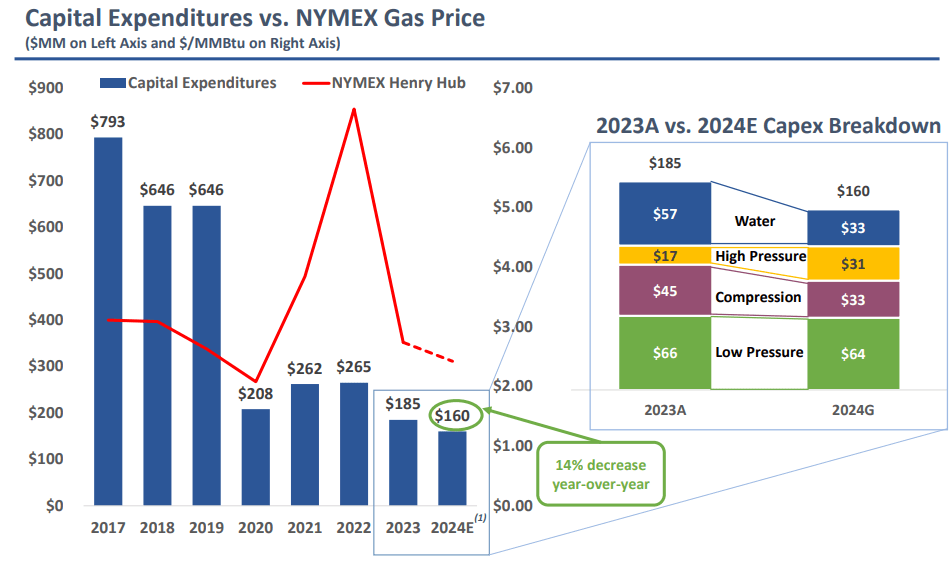

Antero Midstream expects roughly $160 million in capex during 2024, down 14% compared to 2023. Antero Midstream is past its period of heavy capital investments (after spending $600+ million per year from 2017 to 2019).

I now estimate Antero Midstream's value at $14.35 per share. This includes a base $14.00 per share value (not including the potential Veolia proceeds), which is a $0.25 per share increase from my November 2023 base value estimates. This increase reflects Antero Midstream's slightly better than expected guidance for 2024.

I've also included $0.35 per share for the potential Veolia proceeds, assuming a generic 75% chance of the judgment being upheld and discounting the future proceeds to get to present value.

In January 2024, Antero Midstream issued $600 million in 6.625% unsecured notes due 2032 and used the proceeds from the notes to pay down its outstanding credit facility debt. Antero Midstream had $630 million in outstanding credit facility debt at the end of 2023.

Antero Midstream's credit facility debt had a weighted average interest rate of 7.08% at the end of 2023. Thus the new unsecured notes have a slightly lower interest rate which results in a minor amount (such as $3 million per year) in near-term interest savings.

Antero Midstream's credit facility debt has a variable interest rate, so the credit facility debt (if any) could still end up with a lower interest rate than Antero Midstream's new notes in the future.

Antero Midstream is currently projecting adjusted EBITDA of $1.02 billion to $1.06 billion for 2024, which involves a 5% increase compared to 2023 based on the guidance midpoint of $1.04 billion. This includes expectations for 2024 throughput growth in the flat-to-low single digit range.

Antero Resources expects a slight decline in production in 2024, but the drilling partnership with QL Capital adds a bit to Antero Midstream's throughput volumes. QL Capital is expected to fund 20% of the development capital for wells that Antero Resources spuds in 2024, gaining a similar working interest percentage.

Antero Midstream's adjusted EBITDA also benefits from the fee rebate program with Antero Resources ending as scheduled at the end of 2023. Antero Resources received $52 million in fee rebates from Antero Midstream in 2023.

Antero Midstream's Capex (anteromidstream.com (Q4 2023 Earnings Presentation))

Antero Midstream also expects its capex budget to be $150 million to $170 million, which represents a 14% decrease in capex compared to 2023 at the guidance midpoint of $160 million, and is also a bit lower than prior expectations.

Antero Midstream estimates its interest expense to be around $185 million to $195 million during 2024. However, Antero Midstream's outstanding notes appear to have combined interest costs of nearly $200 million per year and that doesn't include any credit facility interest costs. Antero Midstream's 2024 free cash flow may benefit a bit from its new 6.625% notes due 2032 only making one interest payment during 2024.

| In $ Millions (Except for Daily Production) | ||

| AR's 2024 Daily Production | My Prior Estimate | 2024 Guidance |

| Adjusted EBITDA | $1,035 | $1,040 |

| Capital Expenditures | $175 | $160 |

| Interest Expense | $205 | $190 |

| FCF Before Dividends | $655 | $690 |

| Dividends | $430 | $435 |

| FCF After Dividends | $225 | $255 |

The above table compares Antero Midstream's guidance versus my earlier estimates. Antero Midstream is now expected to generate $255 million in free cash flow after dividends in 2024, around $30 million more than my prior estimate.

Antero Midstream instituted a $500 million share repurchase program in February 2024. It could theoretically put much of its free cash flow after dividends towards share repurchases in 2024 as its credit facility balance should be pretty minimal, proforma for its 2032 note offering.

Antero Midstream may also look to redeem some of its $550 million outstanding 7.875% unsecured notes due 2026 due to the relatively high interest rate on those notes, but it will need to wait until May 2025 if it wants to redeem those notes at 100% of par with no premium.

Antero Midstream ended 2023 with $3.23 billion in net debt. If it doesn't do any share repurchases, it should be able to reduce its net debt to a bit under $3 billion by the end of 2024, giving it leverage of 2.9x.

Veolia Lawsuit (anteromidstream.com (2023 10-K))

The Veolia lawsuit appeals are still being dealt with at the Colorado Court Of Appeals. This process can take a while, so I believe that the results can be expected in late 2024 or 2025. Antero wanted Veolia to post more than a $25 million appeal bond, but the courts decided that the $25 million bond was sufficient based on Colorado statutes and the guarantees from Veolia France.

My base estimate of Antero Midstream's value has increased by $0.25 per share to $14.00 per share. This is before potential proceeds from the Veolia lawsuit.

Antero Midstream may see around $280 million in proceeds from Veolia if the judgment is upheld. The chance of a generic civil appeal being successful is estimated at around 25%. So using that generic number and also discounting the proceeds by around 20% to account for a potential 2026 payment date results in a present value of around $168 million or $0.35 per share.

Thus I'd value Antero Midstream at approximately $14.35 per share currently.

Antero Midstream's 2024 free cash flow after dividends is expected to improve by roughly $100 million compared to 2023. This is driven by lower capex and items such as the end of the fee rebate program with Antero Resources. Although Antero Resources expects a slight net production decline in 2024, the production attributable to QL Capital is expected to at least keep Antero Midstream's throughput volumes flat, and may result in a slight amount of growth.

The increased free cash flow guidance (slightly better than my expectations) helps improves Antero Midstream's value a bit, and I now value it at $14.35 per share.