grandriver

grandriver

Readers may find my previous coverage via this link. My previous rating was a buy, as I believed Allison Transmission Holdings (NYSE:ALSN) would be able to beat its FY23 guidance, driven by the positive pricing and demand environment. Indeed, ALSN beat its own guidance, and it did it spectacularly, resulting in a strong share price rally to the current level of ~$76. I am reiterating my buy rating as I, once again, expect ALSN to beat its FY24 guidance. In my opinion, FY24 guidance seems to be too conservative considering the demand and pricing outlook.

ALSN posted 4Q23 net sales growth of 8% to $775 million, beating its own guidance of $740 million at the midpoint. Gross margin also improved by 80bps to 47.9%, leading to a guidance beat in adj. EBITDA. Adj EBITDA was reported at $277 million, implying a margin expansion of 160bps to 35.7%, beating management guidance of $249 million and a 33.6% margin. Looking ahead, management guided FY24 sales in the range of $3.05 to $3.15 billion and adj. EBITDA of $1.07 to 1.13 billion, implying a margin of 35.5% (stable from 4Q23 levels).

Based on author's own math

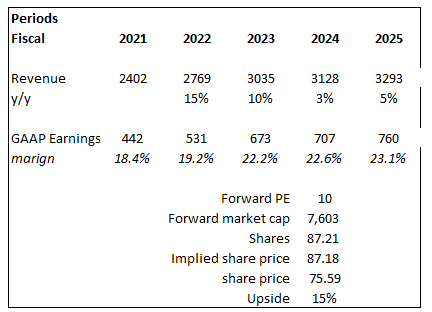

Based on my view of the business, ALSN should beat management guidance and consensus estimates, given that the demand and pricing environment remain favorable. To reflect my view, I used consensus estimates as a benchmark, followed by adding a premium to these estimates based on the ALSN historical beat. On average, over the past 7 years, ALSN has almost always beaten consensus estimates (except for FY20, which is mainly due to COVID) by 1% for revenue and ~8% for GAAP earnings. What this tells us is that consensus tends to be right on revenue but underestimates GAAP earnings. After adjusting consensus estimates, I expect ALSN to grow revenue by 3/5% and GAAP earnings to reach $707/760 million in FY24/25. However, I remain conservative on the valuation multiple that ALSN should trade at. I simply assume that ALSN will continue to trade at the current average level of 10x forward PE. But I do note that multiples could go higher if ALSN beat estimates by a bigger than expected margin.

My outlook for ALSN remains very bullish, as the underlying demand is still very robust. Take North America on-highway, for instance. The strength of Class 8 vocational demand continues to be supported by infrastructure spending. While management guided for revenue on this end to be down 2% at the midpoint, I point out that this is not due to a lack of demand; rather, it is due to supply constraints (this shows how strong the demand is). Specifically, they flagged the possibility of the supply base being unable to deliver sufficient components to the OEMs to meet the strong demand, which could potentially drive weakness in 2024. As such, once again, this puts ALSN in a position where I think they could easily beat guidance again. Since this is a supply issue, ALSN just needs to increase capacity; this depends on the execution and availability of materials, but looking at how management provided this guide, it seems like they are staying on the conservative end of the spectrum. Additionally, another upside catalyst is the ~$100 million incremental annual revenue opportunity in Class 8 regional haul and day cabs, which continues to make progress. Again, depending on how much traction this partnership brings, it could drive additional upside to the guide.

We're still in this situation where can the entire vehicle supply chain get the proper parts to the OEMs to build? Clearly, they're building less over-the-road tractors and are focused on building where they have strong demand, which, fortunate for us, is right in the middle of our core addressable market, medium duty, Class 8 stray truck.

First, we were pleased to announce that our $100 million incremental annual revenue opportunity in the Class 8 Regional Haul and Day Cab market continues to progress as one of the largest global logistics and delivery companies has specified Allison's 3414 Regional Haul Series as the propulsion solution of choice. Source: 4Q23 earnings

Even outside of North America on-highway, those segments are also expected to grow mid-teens percentage in 2024 driven by several growth initiatives. So, for example, Allison stands to gain around $100 million in yearly revenue from their collaboration with SANY on wide body mining dump trucks. In spite of geopolitical uncertainties, the defense segment is projected to grow at a rate of 34% thanks to rising demand on a global upcycle, opportunities at home with US modernization programs, and higher sales to the US Military. Management has also guided for a 20% growth in the energy mining and construction segment, which should be accompanied by a recovery in demand (after the challenging 2H23 caused by OEM tenders). (Guidance is from transcript)

Another positive indicator of demand is that pricing traction remains strong, up 540bps in FY23, outpacing management initial expectations of 400bps. Readers should be reminded that over 90% of ALSN's NA on-highway business is covered by long-term agreements with defined pricing, so the expected moderation in pricing growth will not have less of an impact. In fact, considering ALSN's value proposition—which promotes energy efficiency, ease of driving, and reduced downtime—I anticipate ALSN to continue realizing better than average (i.e., the 200bps) pricing.

Looking at how the stock has reacted to the recent results, I think the investment risk is more of an expectation risk, where the stock is now embedding more optimism. While I believe ALSN can beat its FY24 guidance, any sign of weakness could cause investors to cut back on their position to lock in profits. On a fundamental basis, if the macro situation turns for the worst (for any reason), ALSN will suffer one way or another as the overall economy slows further.

In conclusion, I maintain a bullish outlook on ALSN, reiterating a buy rating after its impressive FY23 performance and guidance beat. With robust demand in North America and growth initiatives in various segments, I believe ALSN is well-positioned to exceed FY24 guidance. Supply constraints, rather than lack of demand, pose a temporary challenge in the on-highway segment, but it is not unsolvable. The $100 million incremental revenue opportunity in Class 8 regional haul and day cabs further adds to the positive outlook. Pricing traction also remains strong, supported by long-term agreements, and I anticipate ALSN to sustain above-average pricing. However, investors should be mindful of optimism embedded in the stock, posing an expectation risk. Any signs of weakness or macroeconomic downturn could also impact ALSN's performance.