RichLegg

RichLegg

Align Technology (NASDAQ:ALGN) is a medical device company that is famously known for its Invisalign product. The stock has had a rough patch since September 2021. After falling 75% from its all-time high, the stock has recovered 69% from its trough and is currently trading at $302. While the company is showing signs of recovering revenue growth given its focus on R&D to continually innovate its products to maintain its competitive edge, its operating margin has been steadily declining, which is a cause for worry.

At the same time, should global macroeconomic conditions worsen, we may see further volatility in the stock price. While the company could stand to gain long-term if revenue growth returns to the low teens along with expanding margins, I will choose to stay on the sidelines until I see evidence of a material improvement in both the top and bottom lines in the coming quarter(s). As a result, I will rate the company a Hold at the moment.

Align is a global medical device company that designs, manufactures, and markets orthodontic, restorative, and aesthetic dentistry products.

The company operates through two operating systems:

Clear Aligner: This segment consists of the company’s core product, which is its Invisalign clear aligners that treat dental misalignment and malocclusions. In 2023, the company’s Clear Aligner segment contributed 83% of the company’s total revenue.

Imaging Systems and CAD/CAM Services: This segment includes its scanning system, iTero, as well as exocad, which is software that aids in computer-aided design and manufacturing and is used by dental professionals to perform implant and restorative surgeries.

In terms of its business model, the company sells its products primarily to orthodontists, GPs, and dental laboratories, leveraging its specialized sales force. The company generates its revenue through a combination of subscription-based pricing for its Invisalign product, as well as fees charged for the series of aligners provided to the patient over the course of their treatment.

In Q4 FY23, Align managed to beat revenue and earnings expectations by 2.5% and 11.5%, respectively. Revenue for Q4 grew 6.1% YoY to $956M, driven by faster growth in the Clear Aligner segment, which grew 6.9% YoY in Q4 to $781M.

During the earnings call, the management indicated that the faster growth in Clear Aligner revenue was partly due to a higher Average Selling Price (ASP). At the same time, the company’s teen cohort saw 197,000 teens and younger patients that started treatment, which increased 6% YoY in Q4, along with a record number of Clear Aligner shipments for teens up 8% YoY to 809,000 in FY23, which I believe helped boost the topline.

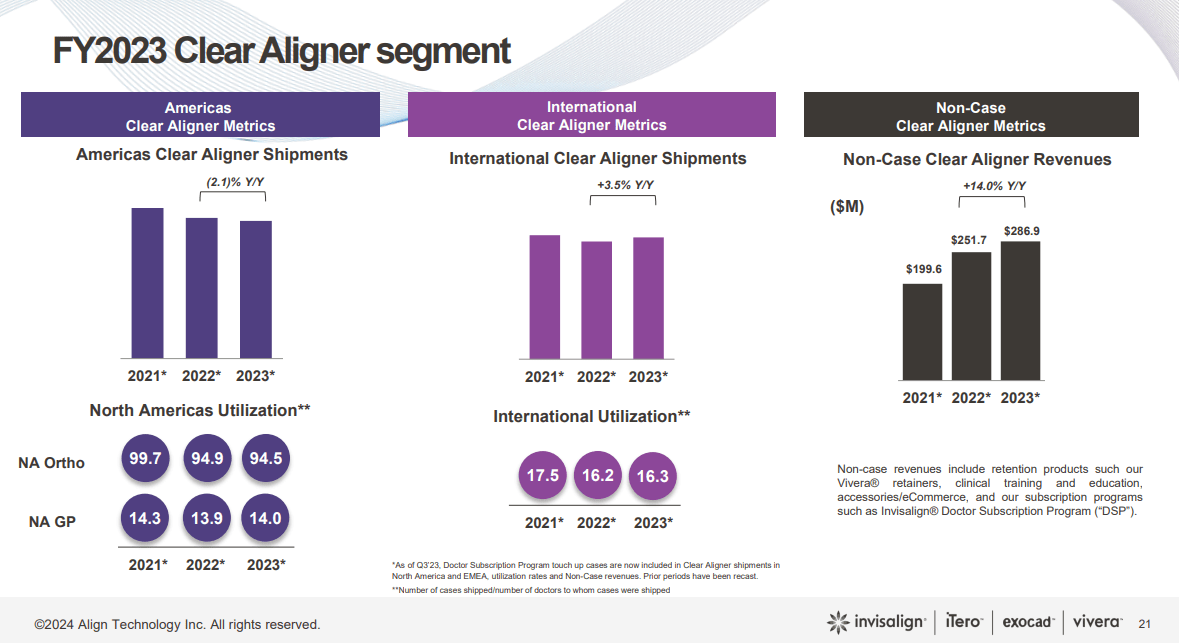

For the full FY23, Clear Aligner revenues grew at 4.1% YoY to $3.2B, mostly driven by faster growth in its International Markets which now contribute 38% of Total Revenue, compared to 36% in the prior year. In FY22, Clear Aligner revenue declined (5.4%) YoY. For context, over the last 10 years, the company has grown its Clear Aligner revenue at a compounded annual growth rate (CAGR) of 20%, so this is a marked slowdown from its prior growth levels.

Q4 FY23 Earnings slides: Align's Clear Aligner Segment Revenue

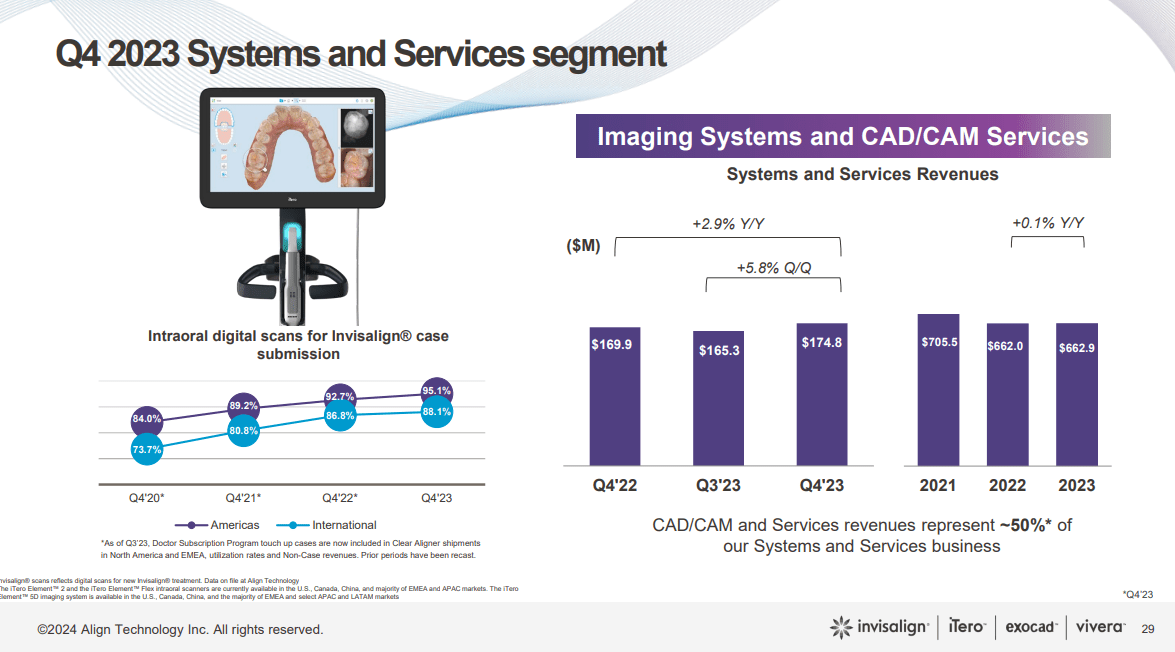

Meanwhile, the company’s revenue performance in its Systems & Services segment has been lackluster, growing at 0.9% YoY to $662M. I believe this could be attributed to reduced capital expenditure, as dentists anticipated a slowdown in their businesses from a tough macroeconomic environment of high inflation and interest rates.

Q4 FY23 Earnings slides: Align's Systems and Services Revenue

In FY24, the company expects total revenues to grow in the mid-single digits, a marked slowdown from its previous growth range, as the company remains cautious about the uncertainties prevailing in the overall macroeconomic environment.

In terms of product innovation, the company introduced its latest iTero Lumina inter-oral scanner, which has a 3x wider field of capture and a 50% smaller wand that delivers faster and more accurate scanning, improving overall practice efficiency. Furthermore, Joseph Hogan, CEO of Align, mentioned that initial doctor feedback has been positive. I believe this emphasizes that the company is on the right track with its product innovation pipeline.

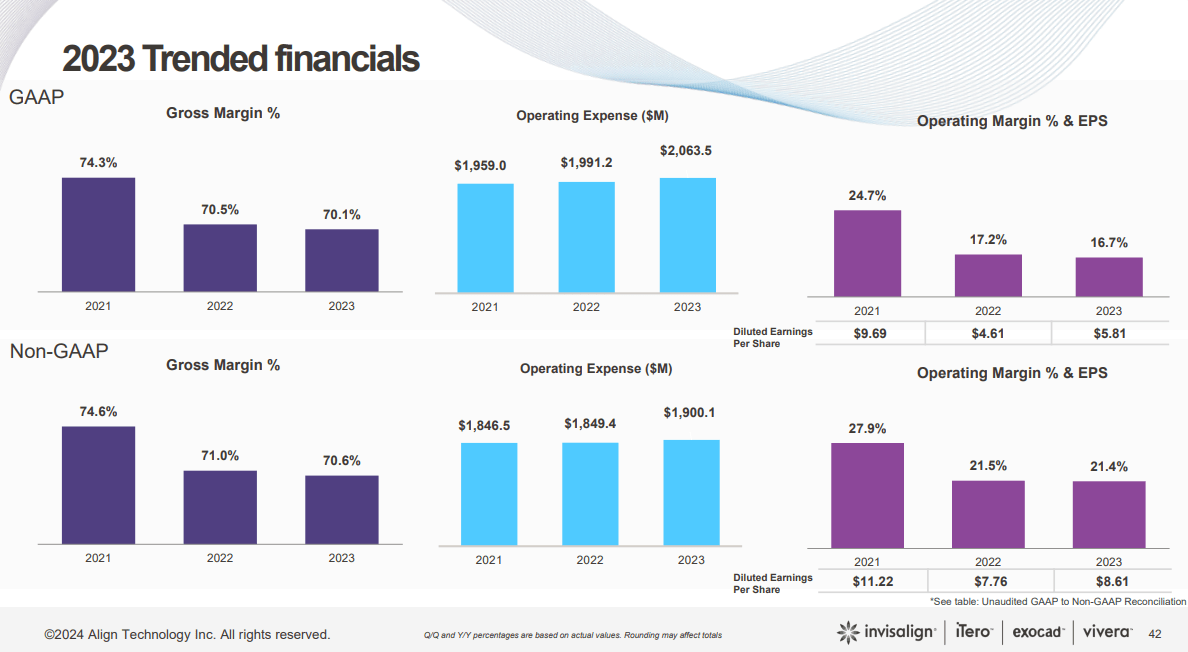

Shifting gears to operating profitability, Align reported a non-GAAP operating margin of 21.4% for FY23, which remained flat YoY. However, in GAAP terms, GAAP operating margin grew to 16.7% in FY23, down from 17.2% in FY22. Compared to FY21, GAAP operating margin has dropped 800 basis points ((b.p.)) as the company has continued to invest in its R&D, which increased 13% YoY, while total revenues just grew 3.4% YoY.

At the same time, the company has not been able to streamline its Sales & Marketing spend as it continues to focus its efforts on international expansion in order to maintain its competitive positioning.

Q4 FY23 Earnings Slides: Align's Profitability

Moving forward, the management projected its operating margins to slightly improve from their FY23 levels on both a GAAP and non-GAAP basis. On the one hand, the company is sacrificing its profitability to invest in its R&D in order to counteract the impact of competition, while also offering discount programs to dentists to incentivize them to push Align products, which could boost the top line and create a loyal customer base. On the other hand, the narrowing of profitability in the short term will turn out to be a bigger problem if we see a global macroeconomic slowdown.

We have already seen many Euro countries, such as the UK and Germany, enter a recession, as well as Japan. At the same time, with inflation not decelerating at the pace the Fed would like, there is a growing probability of interest rates remaining higher for longer. I believe this will increasingly squeeze consumer discretionary spending, as the costs of borrowing remain elevated, coupled with the prospect of a weakening job market. This in turn may continue to put downward pressure on Align’s growth prospects, and given the company’s robust R&D spending at the moment, it would likely drive away investor optimism, in my opinion.

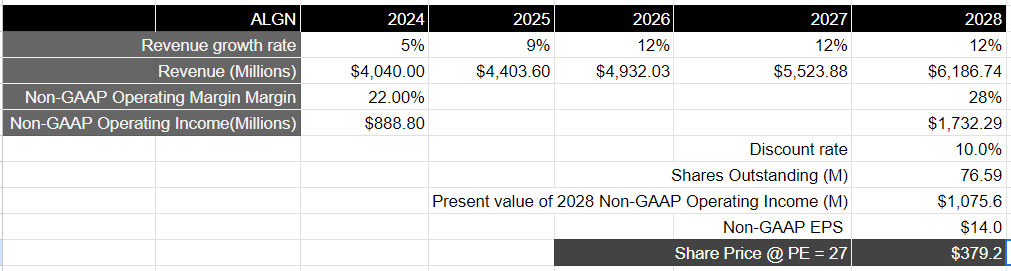

Align’s management has guided revenue to grow in the mid-single digit in FY24, with operating margins slightly improving compared to FY23. Looking over a 5-year investment horizon, should we expect the company to return to its low-teens growth rate, as the company rapidly innovates on its product pipeline with a robust R&D spend coupled with international expansion, the company should generate around $6.2B in FY28. Assuming that the company’s management re-focuses its priorities to improve operating efficiencies by growing its non-GAAP operating margin from 22% in FY24 to 28% in FY28, the company should produce a total non-GAAP operating income of $1.7B in FY28, which will translate to a present value of $1.075B when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies have grown their earnings by 8% on average over a 10-year period with a forward price-to-earning ratio of 15–18, Align should trade at approximately 1.8x the forward multiple, given that earnings grow 14–15% annually every year over the next 5 years. This would translate to a forward price-to-earning multiple of 27, which would mean that there is approximately 25% upside for the stock at the moment.

Author's Valuation Model

However, I would be cautious at the same time, as the company has not yet shown any material sign of improvement on either the revenue or the operating margin front. Coupled with that, macroeconomic risks are a sizable concern, in my opinion. This may cause significant short-term volatility for the stock as the company navigates forward. As a result, I will rate the company a Hold at the moment.

While Align’s improving revenue growth is definitely a bright spot, I believe that the stock will be subject to significant short-term volatility until it shows evidence that it has navigated clear of the storm. As a result, I will rate the stock a Hold until management provides further guidance on its plan to reaccelerate growth and profitability.