Avalon_Studio/E+ via Getty Images

Avalon_Studio/E+ via Getty Images

Alamo Group Inc. (NYSE:ALG) is a manufacturer and distributor of industrial and vegetation management equipment. With a recent miss in earnings during the company's quarter, I think Alamo's current valuation has presented an opportunity to buy a steady grower in the Industrials sector. In this article, I'll discuss the latest results and outline the bullish case for the company and why I'm a buyer of the company's shares today.

Alamo Group operates two primary segments. In Vegetation Management, the company's largest segment at 58% of revenues, the company sells heavy duty machinery and hydraulically-powered equipment like tractors, truck-mounted mowing equipment, and all of the related replacement parts for these products. Most of this equipment is used on farms and for agricultural applications to cut grass, clear land, plant fertilizer, and plant, trim, and remove plants, crops, and trees, but it also does wetland management and forestry and recycling work. In recent years, this has been the faster growing segment for Alamo Group, having doubled in size over the last five years and overtaking the Industrial segment in terms of total sales in 2020 (source: S&P Capital IQ).

In the Industrial segment, Alamo also sells heavy duty machinery and equipment, but these have more applications towards contractor and municipal infrastructure projects. Since agriculture can be a bit seasonal, this segment helps to smooth out the seasonality of revenues and focuses on the year-around maintenance projects that keep cities running, like cleaning sewers, removing snow, cleaning up roadway debris, and repairing potholes. As a slower growing segment, the Industrial segment grows roughly in line with inflation and makes up 42% of revenues.

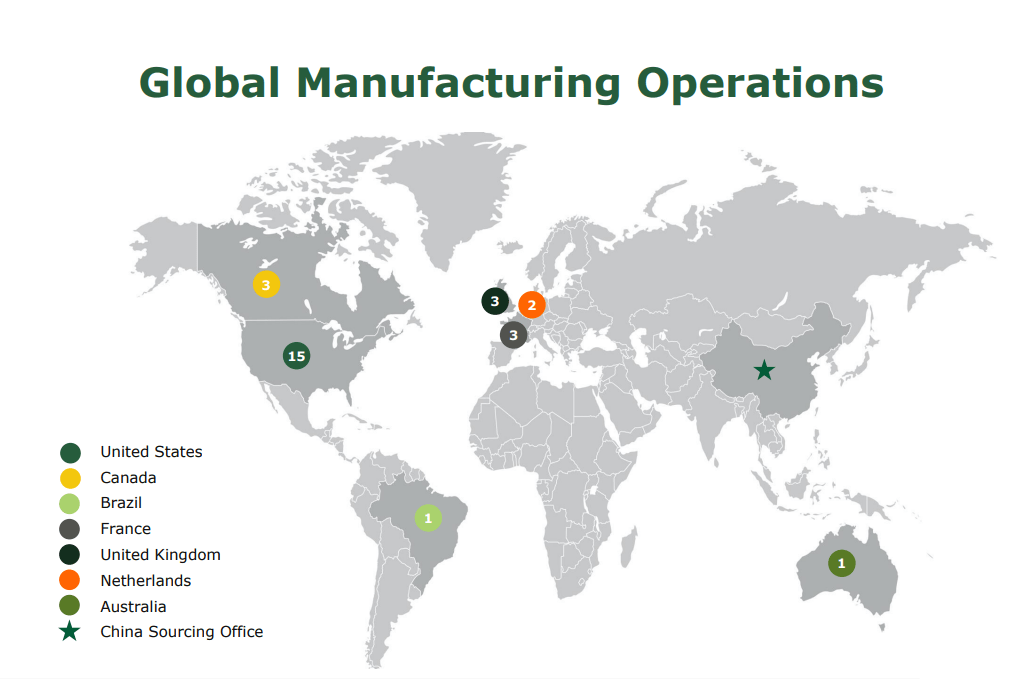

Geographically, Alamo Group derives most of its revenues from the United States (71%), but it also has manufacturing operations in Canada, France, the Netherlands, the U.K., Brazil, and Australia. With Alamo as its flagship and primary brand, it also has 40+ other banners it sells under.

Investor Presentation

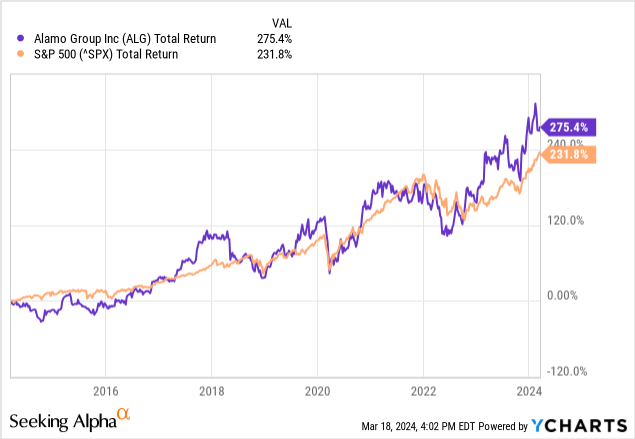

Shares have Alamo Group have been a steady outperformer over the last 3, 5, 10, and 20 years, consistently outpacing the total return of the S&P500 over the respective time periods. For example, in the last decade, shares of Alamo Group have returned 275.4% compared to the S&P500's return of just 231.8%. This equates to a CAGR of 14.1% which would mean that shares of Alamo have effectively doubled every 5 years.

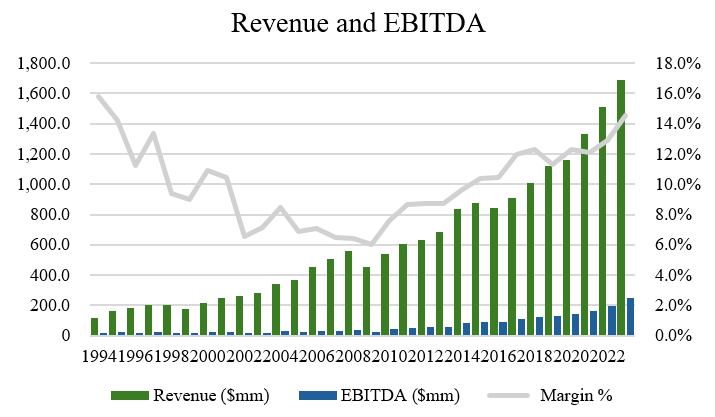

When looking at the historical financials for Alamo Group, the company has been compounding its sales and profitability at high rates of return. Over the last 20 years, the company has compounded revenues and EBITDA at CAGRs of 9.4% and 13.4%, respectively. In the last decade, the company's growth rate has not slowed down, compounding revenues and EBITDA at CAGRs of 9.5% and 15.2%, respectively (source: S&P Capital IQ).

Author, based on data from S&P Capital IQ

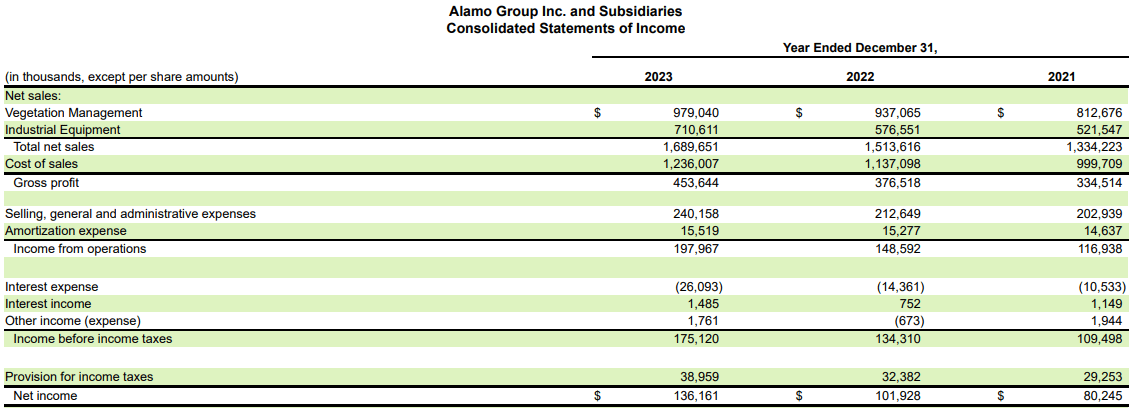

When looking at the recent Q4 and full year 2023 results that were announced last month for Alamo Group, the company reported a miss on both revenues and earnings per share. During the quarter, the company reported revenue of $417.5 million which was up 8.0% on a year over year basis but missed analysts' estimates slightly by $1.9 million. EPS came in at $2.63 for the quarter missing the consensus estimate of $2.68 by 5 cents. For the full year, revenue clocked in at $1.69 billion, which was up 11.6% on a year over year basis.

Overall, despite the small miss on both the revenue and EPS front, this was a good quarter for Alamo Group. For one thing, the company hit a record sales figure for 2023 with both of the company's revenue segments higher than their 2022 levels. Despite the miss on EPS, the company had some gross margin expansion of 190 basis points for the full year and 80 basis points for the quarter, driven by cost efficiencies, higher volumes, price increases across the product portfolio.

Moving down the income statement, operating income was up modestly at 5% as the SG&A as a percent of revenue as unchanged. For the full year, net income as a percent of revenue was 8.1% compared to 6.7% in 2022.

Financial Results (Company Filings)

I see positive developments ahead for Alamo Group which leave me pretty optimistic about the company. Firstly, while management didn't provide guidance for 2024, the 18% dividend increase from $0.22 per quarter to $0.26 per quarter should be a testament to their confidence in the business going forward, especially after 9 consecutively higher quarters on both revenue and earnings per share.

When we look at state rainy day funds, they're about at the highest level they've ever been and twice as high as they were five years ago in 2019. So when we infer what state and municipal spending will look like down the road, it seems that their spending has kept pace with Alamo Group's growth rate. Alamo Group's services to municipalities are essential services in many ways. For example, you're not going to wait a couple years before replacing a pothole or cleaning a city's sewers. From that perspective, the Industrial Segment's revenues being tied to government spending has its advantages by being both predictable and steady over time.

As for the company's backlog, the Industrial segment's backlog is strong at about nine months of sales. During the quarter, there was also over $45 million of revenue recognized from the acquisition of Royal Truck and so there was a bit of revenue and EBITDA contribution there for the segment. There's likely more room for small tuck-in acquisitions like Royal Truck in the highway infrastructure and traffic control market, considering its fragmented nature. With debt reduced by $67 million for the full year, the company's total debt to EBITDA ratio is sitting at 1.0x, which is at the lowest level it's been in some time. So should there be opportunities ahead, Alamo Group seems to be in a very favorable position to take advantage given its flexible balance sheet.

On the vegetation management side, my confidence is a bit more muted, considering that U.S. farmer sentiment has not been increasing. On the company conference call, management noted that the company's Q4 2023 new order bookings was down 34% compared to the Q4 2022 and there seems to be a bit of destocking that's persisting.

While the pace of cancellations in Q4 was lower than in Q3, this doesn't exactly inspire a ton of confidence despite the fact that revenues are increasing for the segment. One catalyst I foresee is that once interests rates normalize, it's likely that agricultural spending could pick up. Headline inflation is still around 3.2% with core inflation at 3.8% and once we get closer to the 2% target the Fed is likely to cut interest rates, which would be a positive factor for spending in the vegetation management segment. I don't like to speculate on macro bets but it seems the risk is to the upside and that this is a potential source of catalyst. Given the seasonality of the business (and typically weaker period of Q4), I'll particularly be watching what happens in Q1 and the Spring season to better assess how long we can expect this to continue.

Alamo Group has 3 analysts covering its stock who all have 'buy' ratings on the stock. Collectively, the average price target of the group is $235.67, with a high estimate of $265.00 and low estimate of $207.00 (source: TD Securities). From the current price to the average price target one year out, this implies potential upside of 16.6%, not including the 0.5% dividend yield.

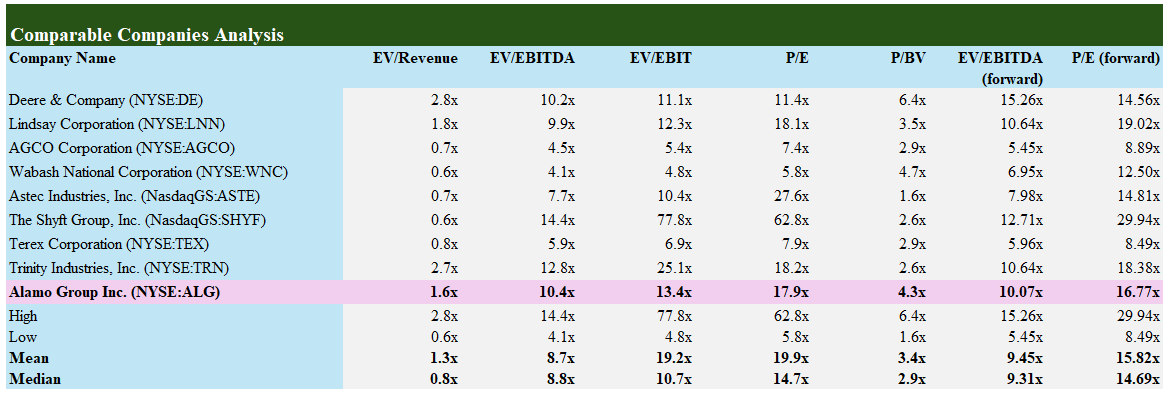

When looking at the peer group for Alamo Group, the company trades at 10.4x EV/EBITDA compared to the peer group multiple of 8.7x. On a P/E basis, the company trades for 17.9x P/E which is at a slight discount compared to the peer group at 19.9x P/E. Overall, I think Alamo Group is deserving of its multiple and could in fact trade at a much higher valuation. Why? Due to the company's track record, higher returns on equity, higher growth rates, and more stable and re-occurring revenues as a result of having several contracts with municipalities and states, I don't think it's unreasonable for the company to trade closer to 12.0x on an EV/EBITDA basis or around 20.0x on a P/E basis. At these valuation multiples, the stock should be closer to the $225-$230 range.

Author, based on data from S&P Capital IQ

Alamo Group has proven itself as a steady performer in the industrial and vegetation management equipment sector, with a diversified revenue stream spanning agricultural and infrastructure projects. Despite a minor miss in recent earnings, the company has showcased a great track record of growth through its financials, marked by record sales figures in recent years and gross margin expansion. With a strong backlog, reduced debt, and strategic acquisitions, I believe the outlook for Alamo Group looks promising. While challenges in the agriculture sector persist, potential catalysts such as interest rate normalization offer upside possibilities and the valuation seems reasonable. Given its track record, superior returns, and stable revenue streams, I think Alamo Group's current valuation may even underestimate its true worth, suggesting room for further price appreciation. For these reasons, I'm bullish on shares of Alamo Group.