Jorgefontestad/iStock via Getty Images

Jorgefontestad/iStock via Getty Images

I wrote my very first Seeking Alpha article this past June on Alico (NASDAQ:ALCO) and I am very excited to be able to touch back on one of my previous analyses and see what developments the company has made since I had last written about them. Alico happens to be in an interesting spot currently. In September of 2022 Hurricane Ian's high winds had damaged some of Alico's trees and caused fruit to drop from them prematurely at the start of their 2022-2023 harvest season. This left Alico with an absolutely terrible year last year. Last week, however, Alico just released its financial statements for Q1, which runs through the beginning of Alico's harvest season (Oct-Dec). Now with Alico's Hurricane Ian season finally behind it, will things begin to turn around one of America's largest citrus producers?

Before we begin, I will leave my first Seeking Alpha article on Alico here for anyone that needs a detailed crash course on Alico's previous business adversities before jumping into Alico's current business happenings and future expectations for the stock.

I am retaining my buy rating for Alico because I believe the company is just beginning its recovery from Hurricane Ian, which struck Florida in September of 2022 and was the second deadliest storm to hit the continental United States. Alico could and will likely receive a large chunk of cash for relief from Hurricane Ian from a Consolidated Appropriations Act that was signed into law in December of 2022. The company had also planted 2.2 million citrus trees in 2017 that take six to seven years to reach full maturity. These trees reaching maturity right now, once fully recovered from Hurricane Ian, have the potential to significantly improve Alico's boxed fruit production.

All of these developments should see Alico's stock price climb back to its historically normal, pre Hurricane Ian levels, however my buy rating for Alico is heavily influenced by its asset valuation versus the business's current stock price. I believe when you buy ALICO you are buying $33.19 worth of a company per share and as the stock is hovering around the $28.00-$29.00 range, right now may be the perfect time to scoop up a couple of shares for yourself.

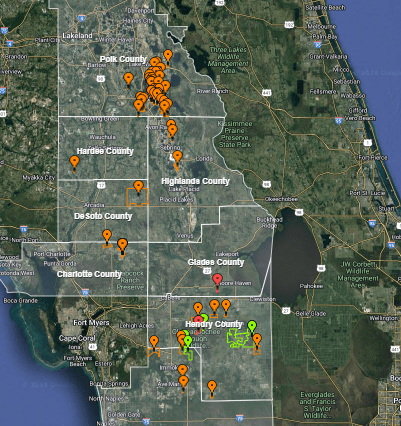

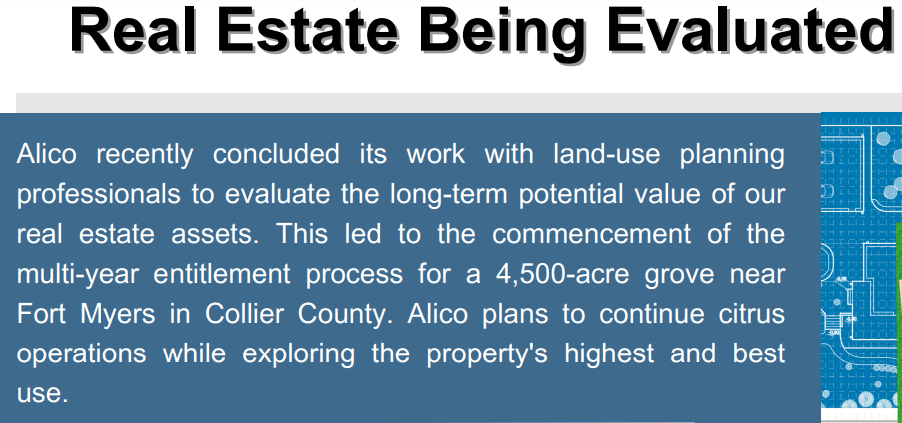

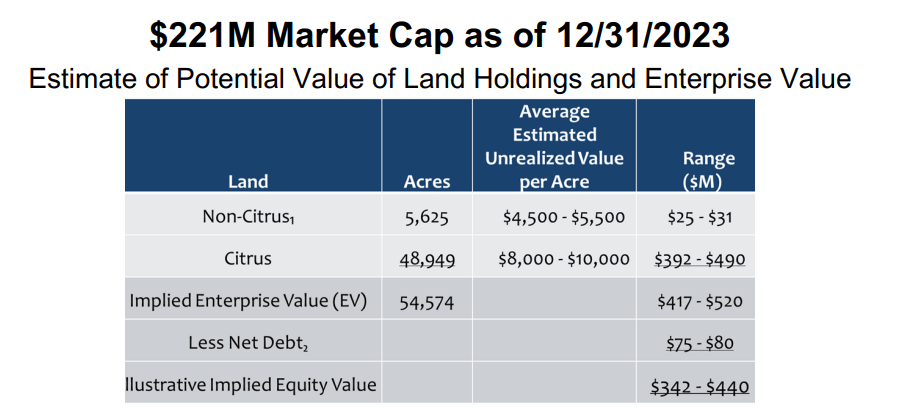

Alico is one of the nation's largest citrus producers, and 81.3% of Alico's consolidated revenues in its fiscal year 2023 came from Tropicana. The company is located in Florida and owns 54,574 acres of land, holding mineral rights on substantially all of it. This land is located in Charlotte, Collier, DeSoto, Glades, Hardee, Hendry, Highlands and Polk counties. 48,949 acres of this land is citrus groves and 5,625 acres is non-citrus producing acreage. Alico has recently been selling off its non-citrus producing property and had recently just sold off over 17,000 acres of ranch land to the state of Florida. Alico has also been consulting land use professionals to figure out what the most profitable use of its lands will be going forward and has recently completed a multi-year entitlement process for 4,500 acres of grove in Collier County near Fort Myers.

Map of Alico's Properties (Alico and Google Earth) Map Legend of Alico's Properties (Google Earth and Alico)

As mentioned in my first article written on Alico, Hurricane Ian wreaked havoc on the company's citrus groves at the beginning of their 2022-2023 season. This caused fruit drop as well as damage to their trees. Initial estimates shortly after Ian had struck suggested that it would take up to two full seasons before Alico's groves would fully recover.

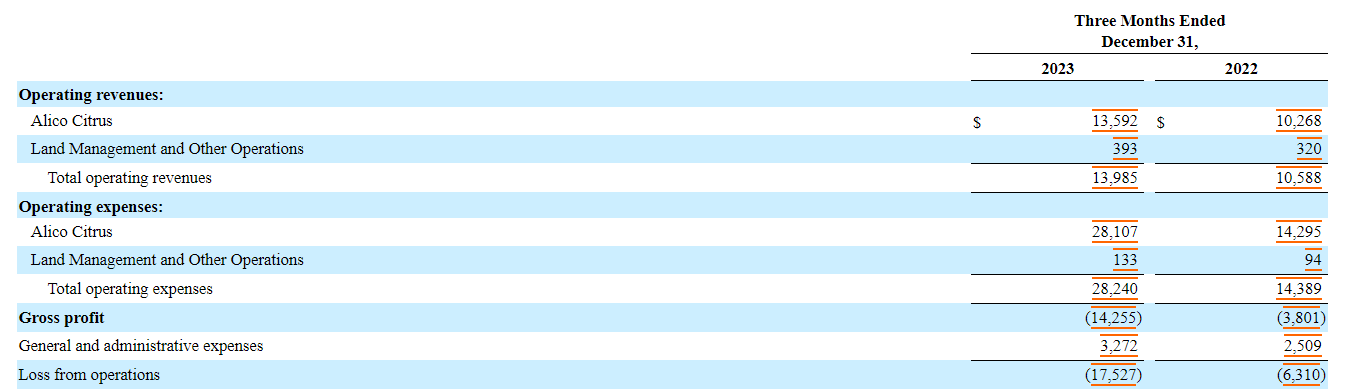

Currently, Alico is beginning its second season after Ian and while Alico's production is improving greatly over last year, the effects of Hurricane Ian are still leaving their mark on Alico's income statement. While Alico saw a 30.1% increase in its processed box fruit production in this 2023-2024 season over the first three months of its 2022-2023 season and a $3.32 million increase in revenue over the same period the company actually shows a gross profit loss of $17.53 million versus a gross profit loss of $6.31 million between the two seasons.

Alico's Operations Revenue (Alico's Q-1 10-Q for the 3 Months Ending December 31st, 2023)

This loss of gross profit despite having an increase in revenue can be largely attributed to a $10.8 million write-down on inventory off of Alico's balance sheet for overestimations made on their 2023-2024 season crop. While this reduction in inventory does have to be accounted for as a loss, it's not really an expense to the company in the same way that paying for labor, machinery, and transportation would be. Alico has to estimate its citrus inventory before harvest every year and if their inventory estimation and actual realizable inventory levels are different, they have to take an expense write down for the difference between the two figures to account for the full actual realizable value of their inventories. When taking out this inventory reduction write down of $10.8 million, Alico only lost $6.73 million in Q1 of its 2023-2024 seasons versus a $6.3 million loss in Q1 of their 2022-2023 season.

Alico's revenue figures look far better this year when considering how their box pricing and accounts receivable works. Alico sells its citrus products through contracted prices. There is a floor and a ceiling price for their products. The floor price represents the lowest amount Alico will receive for its products, and the ceiling price represents the highest price the customer could potentially pay for their oranges. When Alico sells product to its customer, the customer pays a floor price within 7 days of the harvest. Any adjustments in the price thereafter are paid by the customer 30-60 days after the market price has been published. The difference between the floor and the market price of Alico's citrus is accounted for under accounts receivable on their balance sheet and this year Alico had $7.13 million worth of accounts receivable related to market price adjustments compared to just $394,000 on last season's Q1.

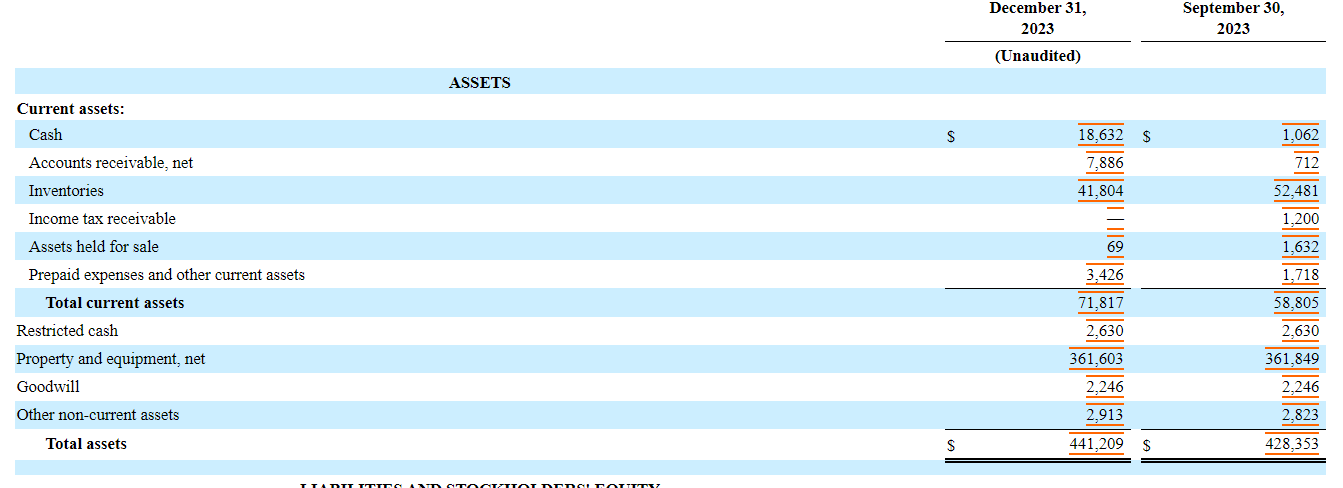

Alico Asset Comparison Between September 30th and December 31st of 2023 (Alico's Q-1 10-Q for the 3 Months Ending December 31st, 2023)

Adding that $7.13 million in price adjustments for their oranges to the company's gross profit and Alico would actually have had a gross profit of $400,000 this quarter. For comparison, if you adjust Q1 of Alico's 2022-2023 season to account for the added revenue Alico would receive from price adjustments, they would still have been negative $5.91 million.

Although it isn't fully expressed in their most recent 10-Q, it does appear that Alico is starting to recover decently. Agriculture is a highly cyclical business and Q2 is where Alico sees the lion's share of its revenues and should give investors a more complete picture of what a post Hurricane Ian recovery is going to look like, however, the same issues Alico saw this quarter could hinder their Q2 results as well. Because of the grove inconsistencies Alico has seen from Hurricane Ian, management might have overestimated grove yields, and they may have to take another large write-down on inventory on their balance sheet. A large gap between the floor and market price of Alico's crop may also lead to a substantial portion of the money Alico will receive for this produce to be left off of its gross profit, which could again make the difference between Alico posting a gross profit or a loss this Q2.

A good Q2 could easily bring Alico's stock price back into the $30.00 - $35.00 range that the stock usually sits at during times of normal operations. If due to the inaccurate inventory assumptions and delayed revenue reporting because of the difference between contract driven floor prices and market prices Alico does not post a gross profit this quarter, it may take until their 10-K this December when these figures from Q1-Q3 all compile together for investors to more easily see the progress Alico is making on its Hurricane Ian recovery. Their 2024-2025 season should yield much better results too and give investors further confidence to jump into a position in Alico.

In 2017, Alico planted 2.2 million new trees in its groves. This planting outpaces tree attrition with the goal of increasing total future crop production. It takes six to seven years for an orange tree to fully mature, which means those trees are hitting their prime citrus producing age right now and once they have made a full recovery from Hurricane Ian, these trees should substantially boost Alico's citrus production. The average number of trees in Florida's orange groves is around 145 per acre and if we multiply that by the 34,985 acres of Alico's citrus groves that actually have fruit growing on them (48,949 acres - 13,964 acres used for storage, equipment, irrigation, roads, etc.) we get an estimated 5.1 million trees. An additional 2.2 million trees would be a 43% increase in trees and would bring the total estimated number of trees on Alico's farms to $7.3 million. This added density of fully matured trees coupled with a near full recovery from Hurricane Ian next year should be more than enough to boost Alico's stock upward to a more historically normal price range of between $30.00-$35.00 and possibly beyond.

In December of 2022, the Consolidated Appropriations Act was signed into law by the federal government and as part of the act federal relief for Hurricane Ian was approved, however, the mechanism and funding for this relief remains unclear as does the extent of relief to which Alico would be qualified to receive.

The last somewhat comparable adverse weather event Alico faced in recent years was Hurricane Irma in 2017. Through a federal block grant, Alico received $24.5 million in federal relief related to Irma damages. Should Alico receive funds anywhere near the amount that they received for Hurricane Irma, it would cancel out the $18.3 million in additional long-term debt Alico accrued during their 2022-2023 Hurricane Ian season.

In an effort to sell off non-core and underperforming assets, Alico sold off 17,556 acres of their land in Q1 of their 2023-2024 season. 17,229 acres of this was Alico's ranch property that it sold to the state of Florida. Alico received $79.09 million for the land, which averages out to $4,505 an acre. The money gained from the sale was used to repay the outstanding balance on their working capital line of credit from Rabo Agrifinance and to repay $19.09 million in Met-Life Variable-Rate Term Loans.

Currently, Alico is having land use professionals evaluating their property in order to assess the best way to maximize value for its shareholders.

Mention of Land Use Professionals Evaluating the Best Use of Alico's Property (Alico's 2024 Investor Presentation )

Alico has also just completed a multi-year entitlement process that I presume is to develop their 4,500 acre grove near Fort Myers, Florida. If this property is approved for development of condos or subdivisions, the value of this property specifically could skyrocket. There's a reason Alico has gone through the trouble of getting this specific patch of land entitled. I suspect this property is worth far more than the $8,000-$10,000 an acre that Alico is currently estimating its citrus property values at. If Alico could sell this land off at a significant premium, it could help them greatly reduce their remaining $83.3 million in long-term debt, helping Alico put more of their revenue towards net income and less of it towards interest and principal payments.

Alico's Mention of Entitlement Process Completion on 4,500 Acres in Collier County (Alico's 2024 Investor Presentation )

A major reason for my buy rating on Alico is the value it has in all of the land that it owns. Alico owns 54,574 acres across Charlotte, Collier, DeSoto, Glades, Hardee, Hendry, Highlands and Polk counties in Florida. 48,949 acres of this land is citrus groves and 5,625 acres is non-citrus producing acreage. The estimated value of this property ranges from $8,000-$10,000 an acre for their citrus properties and $4,500-$5,500 an acre for their non-citrus properties.

Alico's Potential Land Value (Alico's 2024 Investor Presentation )

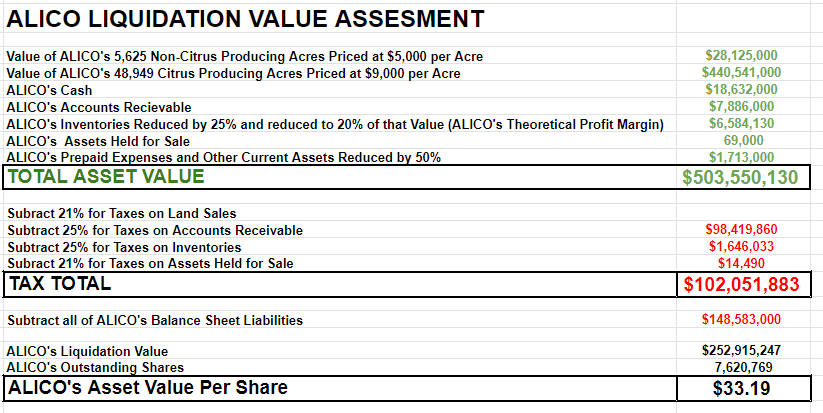

I took these theoretical property values in with Alico's other assets then subtracted all of their debts, liabilities, and the taxes they would likely pay in the event of such land sales in order to get a better idea of what the true value of Alico would look like in the event of a theoretical liquidation.

Theoretical Liquidation Assessment Of Alico (Leland Roach)

As you can see, I priced Alico's acreage value at dead center of Alico's estimated range for each of their respective property categories. I kept the value of Alico's cash at full value, as well as Alico's accounts receivable. The business's accounts receivable is likely to be received at full value as this is an expected somewhat predictable cost between Alico and Alico's customers agreed upon floor pricing and the published market price of Alico's citrus. This pricing scheme also includes an agreed upon ceiling price, making it unlikely the price of Alico's citrus would rise above a level their customers could not pay, especially considering 81.3% of Alico's consolidated revenues in its fiscal 2023 came from Tropicana.

I reduced Alico's inventories by 25% to factor in another possible large write down of inventory to net realizable value should the second half of Alico's 2023-2024 harvest go worse than expected due to the lingering effects of Hurricane Ian in September of 2022. I added just 20% of the value from this newly reduced inventory figure to Alico's asset value, as this is a general profit margin Alico operates around.

I included the full value of Alico's assets held for sale as this is only currently $69,000, and I only included the value of 50% of Alico's prepaid expenses and other current assets under the assumption the company would not be able to fully recover the value of expenses already paid for. From these Figures, you get a total theoretical asset value before deductions for taxes, debt, and other liabilities of $503.55 million.

I estimated Alico's land sales and assets held for sale at a 21% tax rate. I then applied a 25% tax rate to the company's accounts receivable and again a 25% tax rate to the inventories figure that had been reduced to its gross profit margin percentage. This 25% tax rate is generally what Alico's effective tax rate hovers around. After subtracting these tax figures from Alico's asset value, I moved on to their other liabilities.

I subtracted 100% of Alico's total liabilities from the asset value as all of Alico's liabilities seem to be straightforward expenses such as debt, accrued expenses, deferred income tax, and the like. This leaves us with $252.92 million in net asset value to be divided amongst Alico's 7.62 million outstanding shares, leaving us with a value of $33.19 a share, a 14.4% upside from the stock's current share price of $29.01.

The stock price may rise substantially upon news of a successful harvest in Q2. The recovery from Hurricane Ian, however, could be slower than normal, which would reduce investor confidence in Alico and therefore slow or halt the share price recovery.

Due to accounting policies and the difficulty involved with being able to accurately estimate the inventory of its groves after Hurricane Ian, Alico may have to write down more of its inventory as a loss, which could then blunt their gross profit. Depending on what the market price ends up being compared to this year's floor price for citrus, a substantial portion of Alico's revenue from its Q2 harvest could get moved onto Alico's balance sheet under accounts receivable not to be recognized as revenue until Q3. This difference between the floor and market prices for Alico's citrus harvest could be the determining factor between Alico showing a healthy business recovery from Hurricane Ian vs depicting an abnormally slow one. While these numbers inevitably smooth out over the course of the year because of how seasonal the citrus industry is, the timing of them from quarter to quarter could make the difference between Alico's share price rising higher after the company posts results for this year's Q2 or stagnating at its recent price until they release their 10-K results this December.

Citrus greening also poses a severe threat to the Global Citrus Industry. I talked fairly extensively about this in my last Alico article. Alico is currently treating their trees with a chemical called citrus greening therapy Oxytetracycline, but it is unclear currently how effective this treatment will be at preventing or slowing this disease from killing off trees in Alico's groves.

The Effects of Citrus Greening (Credit: J.M. Bové, INRA Centre de Recherches de Bordeaux, Bugwood.org)

Tropicana could also decide to source their oranges from another supplier, but due to citrus greening, coupled with a drought in South America (another large global citrus supplier), I do believe this is unlikely to happen anytime soon.

I would consider selling my Alico stock in the event that another record breaking hurricane or a large frost that damaged Alico's crops came through. This would increase the time it would take for Alico's groves to recover further and would increase the likelihood of the business having to take on additional debt, which could significantly reduce their net asset valuation.

It is hard to currently say if I would sell Alico's stock once the price does reflect a full recovery from Hurricane Ian. Citrus greening does cause an enormous threat to the global citrus industry and any intentions of holding on to shares of Alico in a long term multi-year sense depends primarily on what the land use professionals have to say about what the best possible use of the land is. It also depends on how much money Alico can fetch for its 4,500 acres it recently got entitled outside of Fort Myers, Florida. I will make sure to continue my articles on Alico as more information regarding developments around the use of their properties comes to light.

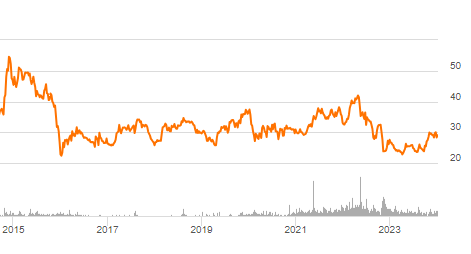

To conclude, I am retaining my buy rating for Alico stock because I believe the company is still in the middle of recovering from Hurricane Ian. As Alico recovers from the effects of this hurricane and its citrus production normalizes, Alico's share price should return to somewhere between the $30.00-$35.00 range, which reflects its net asset valuation. The price could climb even higher than that as before Alico had a freeze event in 2022 their stock had reached over $40.00 a share and the company now currently has $24.5 million less in long-term debt than it did back then.

Alico Stock Price History (Seeking Alpha)

Alico's citrus production should show signs of improvements as their 2.2 million new now fully matured trees recover from Hurricane Ian. These trees were planted in 2017 and should provide an extra bit of assurance Alico can recover to pre Ian production levels. These trees mark a significant increase in Alico's grove density and have the potential to really improve Alico's fruit yield.

Alico also has $33.19 in theoretical liquidation value after taking into account taxes, discounting their inventory for write downs, as well as reflecting the future business expenses Alico would have to expend in order to make that inventory saleable to their customers. This value is a 14.4% upside compared to its current share price of $29.01.