Imgorthand/E+ via Getty Images

Imgorthand/E+ via Getty Images

The market's perception of vision products and medical device firm The Cooper Companies (NASDAQ:COO) appears to be looking up. I say this because, after the market closed on February 29th, shares of the business rose 6.7%. This was in response to management reporting financial results covering the first quarter of the firm's 2024 fiscal year. Based on the data provided, revenue and adjusted earnings per share came in higher than analysts anticipated. In addition to this, there was an increase in guidance for the bottom line for 2024 in its entirety. The company is by no means without some issues. But we need to take the picture as a whole, it could look a lot worse.

Unfortunately, this doesn't mean that investors should buy into the firm. Back in September of 2023, I reiterated my 'hold' rating on the business. Since that time, and excluding the after-hours pop, shares have risen by only 13.2%. That compares to the 18.2% rise seen by the S&P 500. Even though the market's reaction to the earnings release was favorable, how shares are priced on an absolute basis and the continued weakening of the firm's bottom line leads me to be a bit more cautious. Back then, as I do now, I would argue that a 'hold' rating would still be appropriate right now. However, investors who do like the business would be wise to continue watching it closely. After all, there's no telling what changes might occur in the future that could make the company more favorable.

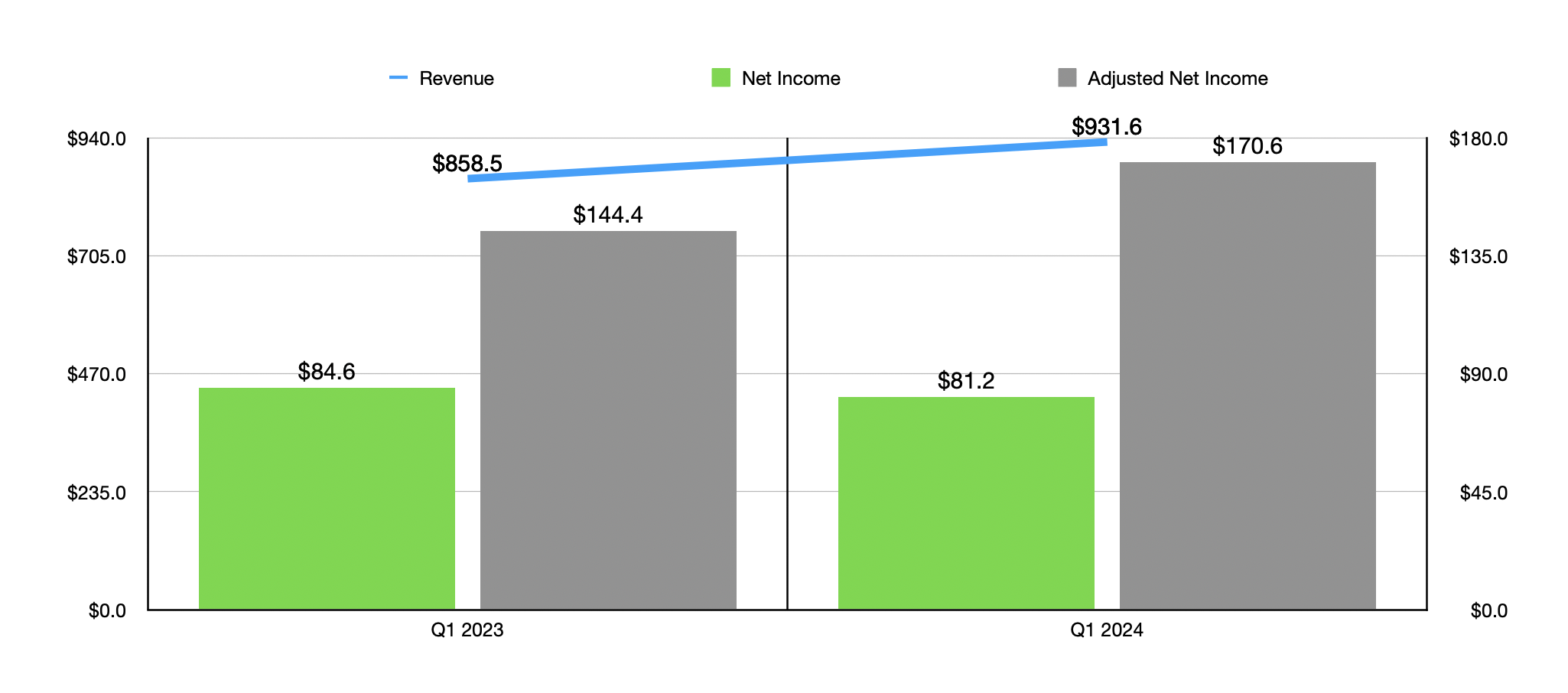

As I mentioned already, after the market closed on February 29th, the management team at The Cooper Companies announced financial results for the first quarter of the 2024 fiscal year. For the most part, it was a pretty solid time. Take revenue as an example. Sales for the quarter came in at $931.6 million. That's an increase of 8.5% compared to the $858.5 million generated one year earlier, and it was about $14.1 million greater than what analysts anticipated. Some small portion of this increase was driven by foreign currency fluctuations. But most of it was organic by nature. There were two primary areas of growth that management reported. First, under the CooperVision segment, toric and multifocal revenue shot up by 14% year over year. That allowed it to grow to $297.3 million. Even more impressive was the CooperSurgical segment, which reported revenue growth of 16% when it came to the office and surgical category of products that it sells.

Author - SEC EDGAR Data

Although the top line was quite robust, the bottom line was in many respects mixed. Earnings per share came in at only $0.41. That's down from the $0.43 per share reported for the first quarter of 2023 and it fell short of analysts' expectations by $0.13 per share. If we look at adjusted earnings, they actually went from $0.73 per share to $0.85 per share. The adjusted figure reported by management was $0.07 per share above what analysts were hoping for. This allowed adjusted earnings to rise from $144.4 million last year to $170.6 million this year. That occurred even as official net profits dipped from $84.6 million to $81.2 million.

Author - SEC EDGAR Data

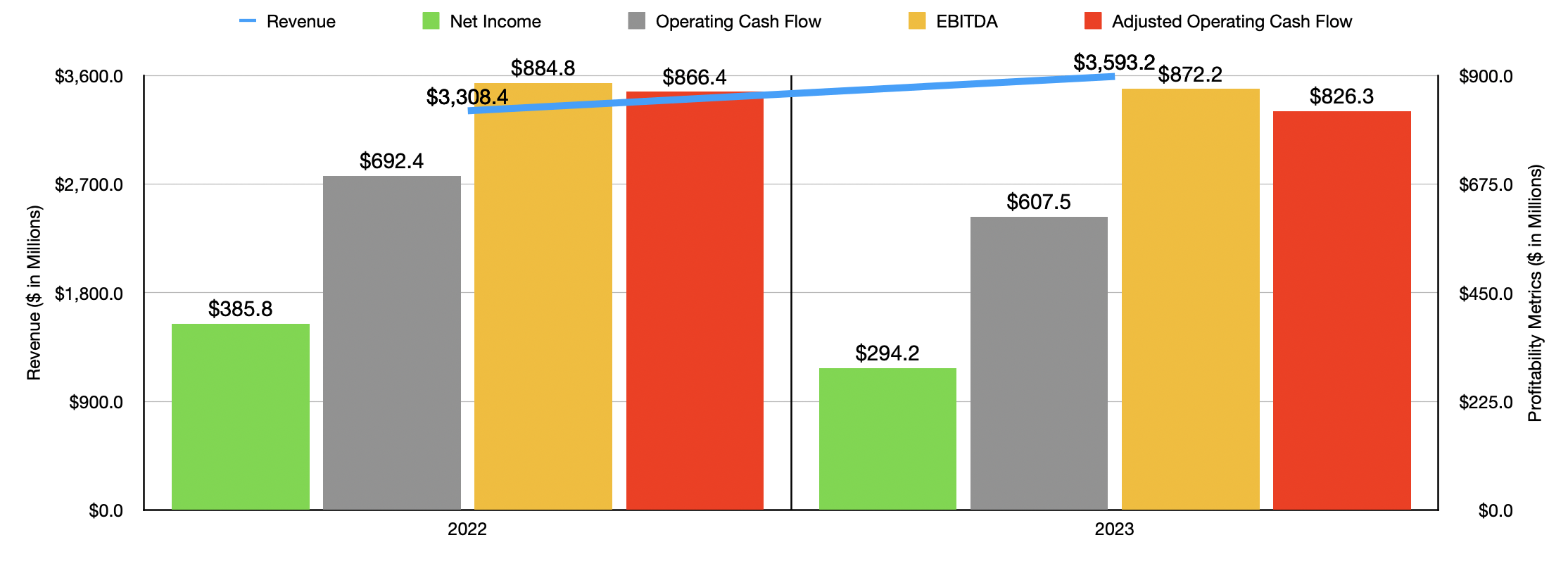

Continued growth on the top line, combined with weakness on the bottom line, is not new to The Cooper Companies. As an example, we need only look at data covering 2023 relative to 2022. Sales for 2023 came in strong at $3.59 billion. That's 8.6% greater than the $3.31 billion generated one year earlier. During that window of time, multifocal revenue jumped 16% from $264.4 million to $305.7 million, while Toric revenue jumped 12% from $737.4 million to $828.7 million. Management attributed this increase to the success of its MyDay and Biofinity offerings. Meanwhile, its fertility products under the CooperSurgical segment, which consist of fertility related consumables and equipment, donor gamete services, and genomic services like genetic testing, shot up by 11% from $431.5 million to $480 million.

Although revenue rose nicely, profits took a hit. Net income went from $385.8 million down to $294.2 million. This was even in spite of a site improvement in the firm's gross profit margin. A near doubling in interest expense, the absence of a $47.7 million investment gain that the company was able to book in 2022 but not in 2023, and a 25% surge in research and development expenses, were all responsible for net income pulling back. Other profitability metrics pulled back as well. Operating cash flow dropped from $692.4 million to $607.5 million. Even if we adjust for changes in working capital, we get a drop from $866.4 million to $826.3 million. And lastly, EBITDA for the company declined from $884.8 million to $872.2 million.

The Cooper Companies

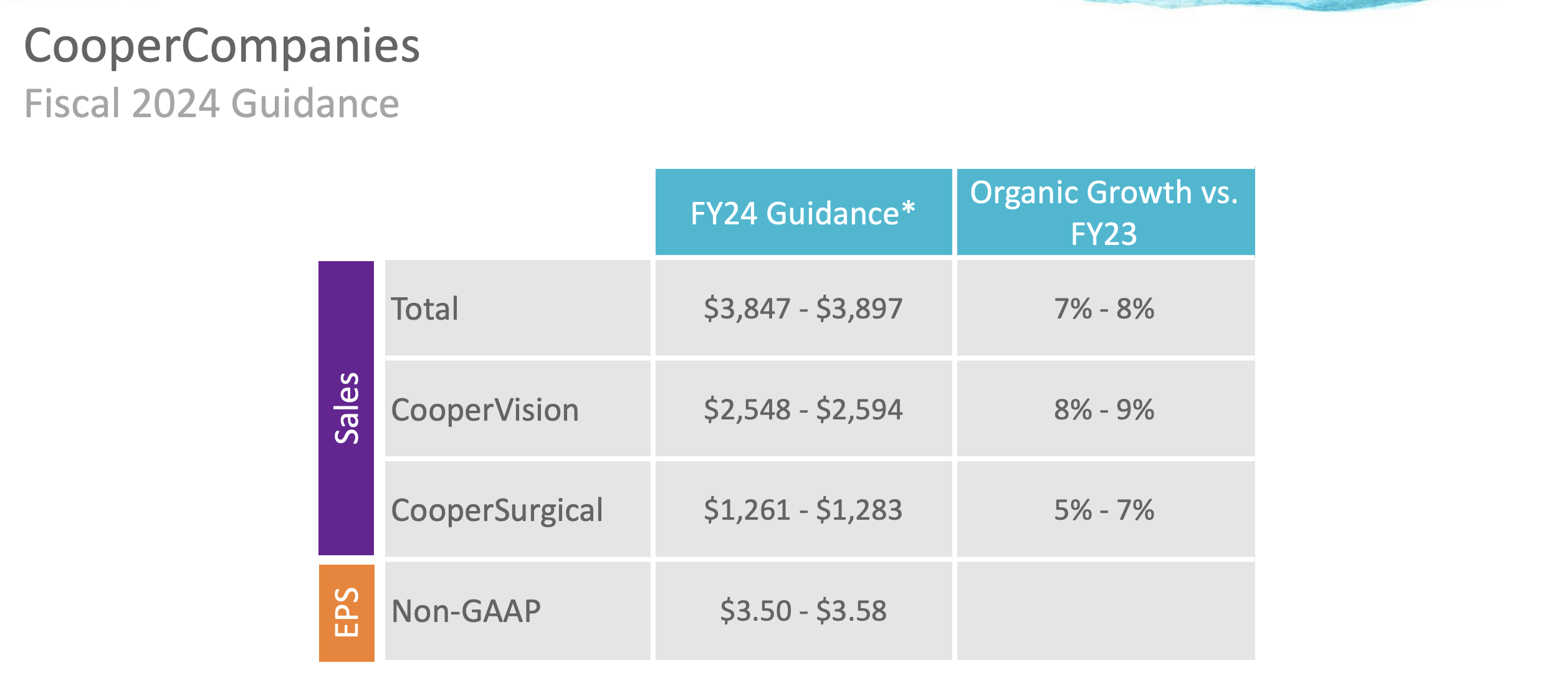

When it comes to 2024 in its entirety, management expects organic revenue to rise by between 7% and 8% compared to what it was in 2023. That would imply sales of between $3.85 billion and $3.90 billion. The greatest growth, according to management, is likely to come from the CooperVision segment. Meanwhile, earnings per share are forecasted to come in at between $3.50 and $3.58 on an adjusted basis. This matches the guidance that management came out with in early January of this year but it's better than the initial midpoint guidance of $3.45 per share that management forecasted when they announced results for the final quarter of 2023.

Author - SEC EDGAR Data

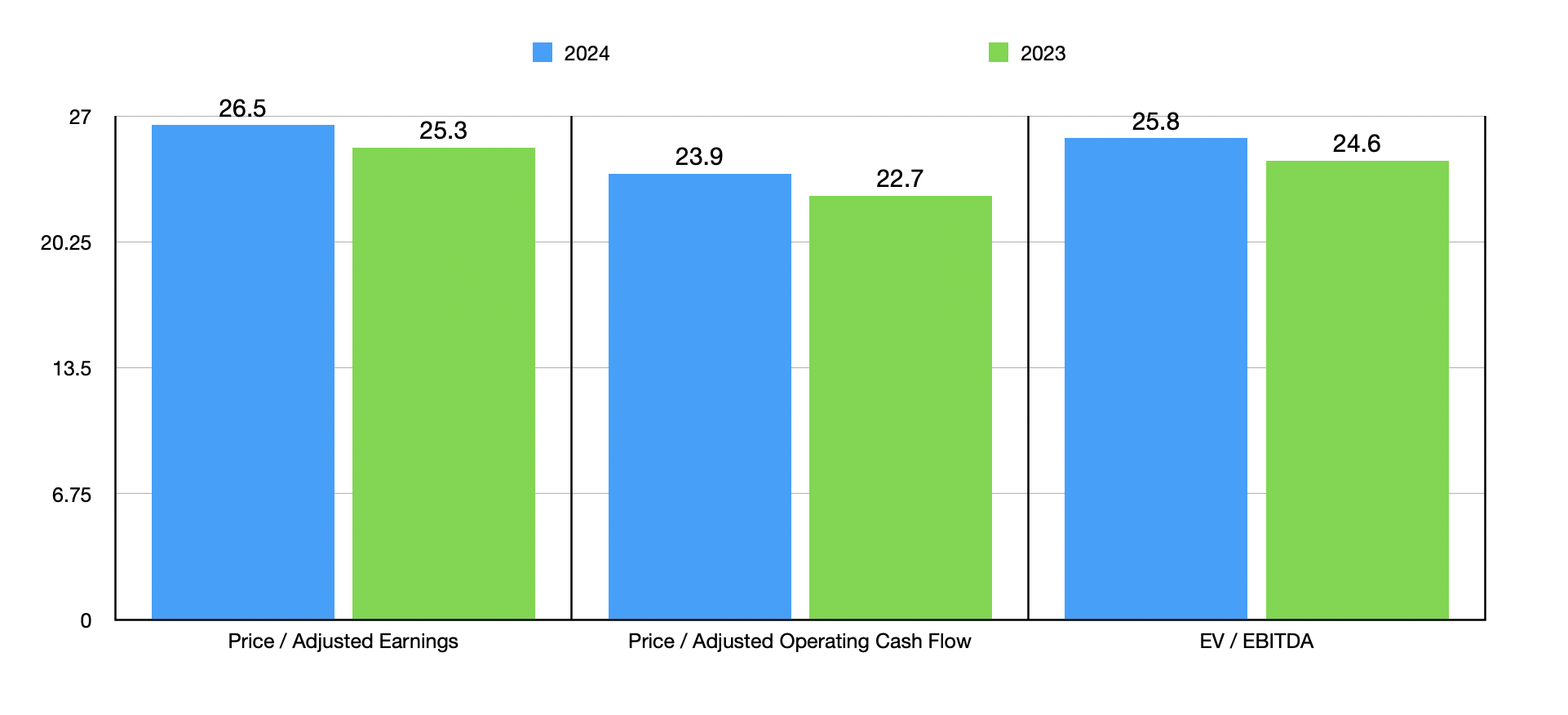

Based on the data we have available, if management does achieve guidance, it would imply adjusted profits of $707.6 million. This would translate to adjusted operating cash flow of around $786.3 million and EBITDA of around $830 million. Using these results, I was then able to value the company as shown in the chart above. As you can see, shares are quite pricey, especially for a business that's seeing its bottom line results worse than year over year. Relative to similar firms, however, things don't look so bad. In the table below, you can see how shares are priced compared to similar enterprises. On a price to earnings basis, only one of the five was cheaper than The Cooper Companies. This number increases to two of the five using the price to operating cash flow approach and to three of the five when using the EV to EBITDA approach.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| The Cooper Companies | 26.5 | 23.9 | 25.8 |

| DENTSPLY SIRONA (XRAY) | 19.3 | 19.5 | 46.0 |

| ICU Medical (ICUI) | 360.7 | 35.9 | 15.9 |

| QuidelOrtho Corporation (QDEL) | 387.9 | 10.9 | 9.9 |

| Neogen Corporation (NEOG) | 308.2 | 33.0 | 23.1 |

| Alcon (ALC) | 93.9 | 28.8 | 42.0 |

Relative to similar firms, it seems to me as though The Cooper Companies is actually toward the cheaper end of the spectrum. But on an absolute basis, shares are quite pricey. It doesn't help that official bottom line results are worsening. Having said that, I am encouraged by continued revenue growth and the overall performance, relative to expectations, that the company achieved during the first quarter. Because of how pricey the shares are, I am not yet ready to upgrade the stock to anything more bullish than a 'hold' rating. But I do think it's important to continue to keep a watchful eye over how things develop. If we start seeing a turnaround in profitability, especially cash flow, I could become more bullish on the business. But for now, a more cautious approach is warranted.