hapabapa

hapabapa

I recommended a hold rating for Akamai Technologies, Inc. (NASDAQ:AKAM) when I wrote about it the last time, as I believed the stock did not provide a sufficient margin of safety. I had no doubts that the business was of high quality, but the upside was simply not attractive enough based on my model. Based on my current outlook and analysis of AKAM, I am upgrading my rating to buy. The pullback in share price has offered an alright entry point, I believe. Although management FY24 guidance is slightly below the 8% expected growth by consensus pre-results, I think the results were strong on an absolute basis (growth is expected to continue trending in the high single-digit percentage range despite major contract renewals in 1H24). Also, AKAM AI strategies seem promising, which I expect to help accelerate growth back to the ~8/9% range.

AKAM saw its 4Q23 revenue grow by 7% on a constant currency [CC] basis to $995 million, which is in line with management guidance for $0.985 to $1.005 billion. Adj EBITDA margin performance was also great, improving by 167bps to 42.8%, beating management's guide of ~41%. The same was seen for the adj. EBIT margin, which came in at 30.4%, beating guidance of ~29%. At the bottom line, adj. EPS saw 23% growth to $1.69, well above guidance of $1.57-$1.62. I believe this was a very strong set of results, and combining this feat with the positive FY24 outlook and AI initiatives, I have turned bullish on the stock.

Management guidance for FY24 (CC basis) calls for total revenue growth of 7% y/y at the midpoint CC; security revenue to grow 15% at the midpoint; compute revenue to grow ~20%; but expects delivery revenue to contract by ~6-7%. On the surface, this does not compare well against consensus expectations for total growth of 8% pre-results, and bearish investors are likely worried about the major renewal cycle for the AKAM Delivery business. In 1H24, seven of the top ten content delivery network [CDN] customers are up for renewal. Moreover, management is looking to improve profitability on this front; hence, they are going to step up on pricing and shed less profitable traffic. The combination of these two will likely result in a big drop in revenue; the uncertainty here is how big the magnitude is going to be. My take is that this is simply a near-term problem. As traffic increases over time, AKAM should see revenue growth post-FY24. I would also note that typically, election years are strong for CDN (more traffic), and coupled with the recently acquired business (that is going to contribute to y/y growth in FY25), my take is that management is guiding too conservatively for delivery revenue (by the way, I believe this weak guide led to the share price decline).

Looking farther ahead, the AKAM AI strategy should elevate the long-term growth outlook. AKAM is aiming to develop its Generalized Edge Compute (Gecko), a new service to be built out at the edge. The goal of this project is to make AKAM the go-to cloud platform for businesses that wish to improve customer experiences by bringing processing power closer to end users, their devices, and their data sources. To put it more technically, this enhances the power of Akamai's cloud platform by bringing virtual machines and containerized workloads closer to users through the efficiency and closeness of the edge. The expectation is that this will be a better product than Cloudflare, Inc. (NET) and allow for better inference AI near consumers. This is huge if true. My view is that the usage of AI is going to proliferate at an exponential rate, and the implication is that it requires more sustainable computing and networking power at the edge. Management noticed from the customer trials that feedback has been overwhelmingly positive thus far. That being said, the management plans to automate the application deployment capabilities in FY25 and deliver this platform to 100 cities by year's end, so the positive effects will only come gradually.

Timothy Horan

If you don't mind me asking, it sounds a lot like what Cloudflare is doing, but you're saying it doesn't exist today. Tom, can you maybe talk about a little bit what's different, what you're doing?

Tom Leighton

Yes, that's a great question. They don't support VMs or containers at all, never mind serverless or anything else, just -- they don't have support for that. They don't do this full stack cloud computing. 4Q23 call

Author's work

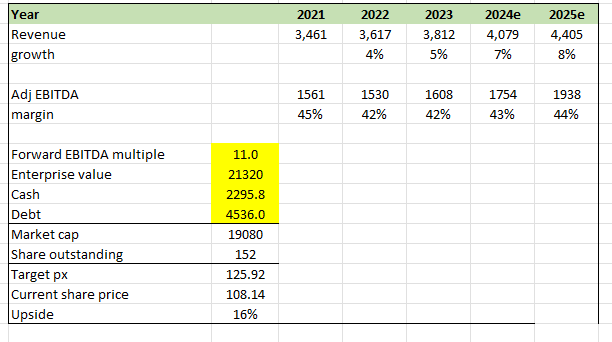

With the pullback in share price, I think the upside has become attractive, despite a more conservative estimate than my previous estimates. For my FY24 estimates, I am using management FY24 revenue guidance, which has historically been quite accurate. AKAM has never missed guidance over the past 6 years (on an annual basis). Since FY24 is going to be a softer year due to contract renewals, I expect growth to accelerate in FY25 as traffic increases and also reflect management decisions to increase pricing. As for adj EBITDA, I assumed the margin will continue to improve back to historical mid-40s percentage levels as management continues to focus on profitability, shedding unprofitable traffic. With improved growth and an improved EBITDA margin outlook, AKAM should trade at a premium to where it is trading today. Before the results, AKAM was trading at ~11x forward EBITDA, and I think it should at least trade back to that level.

The obvious risk is that the contract renewals might cause revenue to fall much more than what management expected. Remember that these are "top 10 delivery customers," which I expect means that they hold quite substantial bargaining power against AKAM. It is likely that AKAM will not be able to increase pricing as much as they wish. In the worst case, revenue could be significantly impacted, resulting in a longer period for revenue to recover.

Overall, I am upgrading AKAM from a hold to a buy rating, considering the recent pullback in share price as an attractive entry point. Despite the near-term challenges related to major contract renewals impacting delivery revenue in FY24, the strong 4Q23 results and positive FY24 outlook, coupled with AI initiatives, have turned my sentiment bullish. The AKAM AI strategy, particularly the Gecko project, holds promising potential for long-term growth. The primary risk remains the potential impact of contract renewals on revenue, emphasizing the need for cautious monitoring.