dem10

dem10

Investors in enterprise Software as a Service ("SaaS") company C3.ai, Inc. (NYSE:AI) experienced a post-earnings surge, driven by the optimism surrounding AI hype on its business prospects. Notwithstanding its CFO leadership transition, investors were likely pleasantly surprised with C3's optimistic outlook for FY25, as it's confident about meeting free cash flow or FCF profitability.

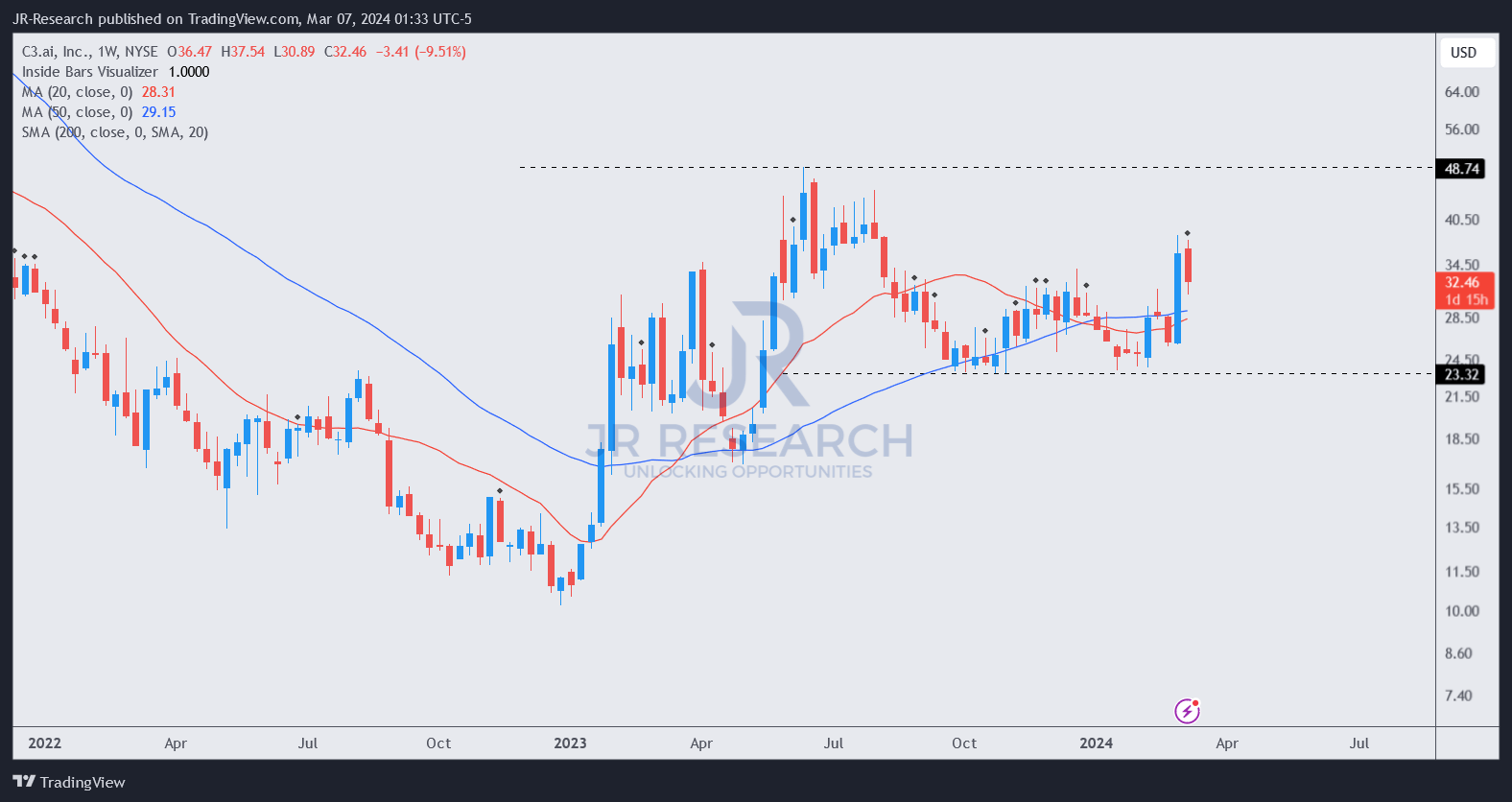

As a result, AI surged toward highs last seen in August 2023, although it failed to reclaim the near-$50 level it achieved in June 2023. Downside volatility followed this week as I assessed some dip buyers likely capitalized on the opportunity to take profit. I had also anticipated a surge in my previous update as I assessed more robust buying sentiments. However, the opportunity didn't occur before its previous selloff to form AI's January 2024 lows. Consequently, I'm increasingly confident that AI investors should find constructive buying support at the low-$20 levels, pivotal toward its ongoing recovery through its 2020 all-time highs.

Notwithstanding the recent recovery, AI is still priced reasonably. Seeking Alpha Quant assigns AI with a "C+" valuation grade. However, it's also critical for C3 investors to note that the company hasn't provided formal guidance yet for 2025, notwithstanding its positive FCF optimism. In other words, the recent optimism could be deflated if the customer engagement cadence on C3's generative AI products weakens over the next three months.

Based on C3's fiscal third-quarter earnings, its business seems to have performed admirably, outperforming Wall Street's estimates. Furthermore, C3's revenue growth momentum has also accelerated, as it delivered revenue growth of 17.6% in FQ3, above FQ1's 10.8% and FQ2's 17.3%. Moreover, C3 also reported robust engagement metrics, delivering an 80% YoY improvement in customer engagement. The company believes that its go-to-motion, or GTM, has been validated. Accordingly, C3 transitioned its previous subscription-based model to a consumption-based model to accelerate pilots and improve the broader adoption of its platform.

C3 believes its LLM-agnostic platform is well positioned to help companies leverage its enterprise AI suites across various industry-specific solutions. Bolstered by the surge in enterprise adoption of generative AI offerings, I assessed that C3's confidence isn't misplaced. I also don't think the market has gotten out of control over AI's valuation, given its "C+" valuation grade.

C3 is valued at a forward enterprise value to revenue multiple of 9.3x at the current levels. While some investors could point to its weak profitability (rated "D-" by Seeking Alpha Quant), the market has not re-rated AI to significant levels yet. While a direct comparison with Palantir (PLTR) may not be entirely appropriate given their platform differences, I think it's noteworthy to consider PLTR's 20.4x forward enterprise value to revenue multiple when assessing AI's optimism.

C3 has also improved its marketplace adoption prospects by broadening C3's industry-specific solution with Google Cloud (GOOGL, GOOG). It should help bolster its GTM with new customers, although we need to assess the revenue flow-through from its pilots. C3's forward guidance suggests a slower YoY growth rate for FQ4. Analysts' estimates also reflect such caution, projecting a 16.6% increase in revenue. Consequently, C3 investors are expected to remain cautious about chasing upward surges if the revenue conversion isn't anticipated to be sustainable.

AI price chart (weekly, medium-term) (TradingView)

As seen above, I gleaned robust support at the low-$20 levels, suggesting AI has shaken off its downtrend bias.

Therefore, I believe the AI hype has bolstered C3's fundamental thesis and buying sentiments, although we need to see a more robust improvement in its profitability.

Notwithstanding the near-term caution, AI's relatively attractive valuation should help underpin a further re-rating if management delivers better-than-expected guidance at its next earnings conference.

Consequently, I see little reason to revise my bullish thesis on C3.ai, Inc. stock, as I believe we are still in the early innings of its generative AI opportunities.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking. Note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn’t? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!