frender

frender

As a buy-and-hold investor, I'm usually on the constant lookout for companies with strong fundamentals that I can buy and hold for the foreseeable future. As an avid dividend investor, buying companies that not only offer attractive yields, but those that offer growth are what I typically look for when investing. Ultimately, I try to find that perfect balance between yield & growth.

To me, a yield is worthless if it's unsustainable for the long term and I try to avoid these at all costs. But depending on who you ask, some investors enjoy higher yields to hold for the short term. One stock that I recently came across that offers a lower yield (of less than 3%), but strong returns and dividend growth is Argan (NYSE:AGX). And in this article, I list 3 reasons why this stock is a buy for long-term dividend investors.

Argan, Inc. is a construction firm that offers power generation, industrial, and telecommunications infrastructure services in not only the United States, but in the U.K. and Ireland as well.

They operate four subsidiaries: Gemma Power Systems, Atlantis Projects Company, The Roberts Company, and SMC Infrastructure Solutions. The construction engineering company is headquartered in Maryland and IPO'd in 1995.

According to their website, their goal is to:

Build the energy and industrial base of tomorrow essential to economic prosperity with motivated, creative, high-energy and customer-driven teams who are committed to delivering the best possible project results each and every time.

Argan investor presentation

As a dividend investor, a company that not only pays a dividend but has some strong dividend growth to go along with it always peaks my interest. Moreover, a solid business model with other fundamentals are also important because they support that strong growth.

And some of these metrics we'll discuss later in this article. But for starters, I have to say I was impressed with the company's dividend. They raised it by a stellar 20% this past September to $0.30. And this is supported by strong earnings through the first nine months of the fiscal year. Although earnings per share have been volatile through the first 3 quarters, it still comfortably covers the dividend.

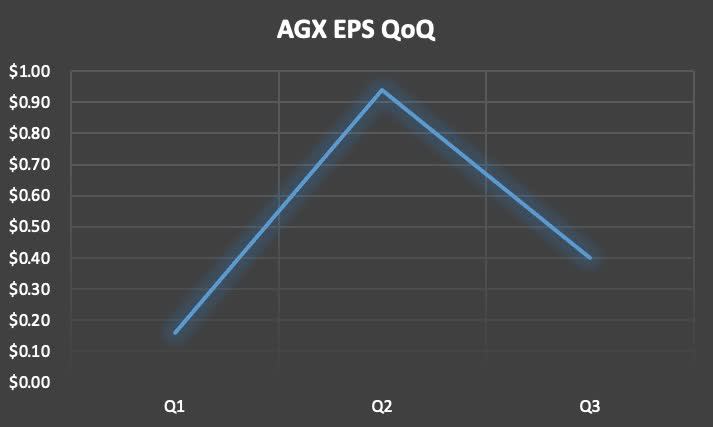

In the chart below, you can see how volatile EPS has been while revenue has steadily increased over the same period. During Q1, AGX brought in $0.16 while revenue was $103.68 million.

During the latest quarter earnings increased to $0.40 but declined from $0.94 in the prior quarter. Management attributed the drop in net income to the Kilroot project which amounted to $11.5 million. This also impacted their gross profit margins which dropped from 19.7% to 14% year-over-year.

Author creation

However, revenue continued to climb steadily, growing from $141.35 million to $163.76 million. Through 9 months earnings per share has grown double-digits at roughly 10% from $1.36 to $1.50 year-over-year. Total revenues have also grown from $336 million to $409 million over the same period.

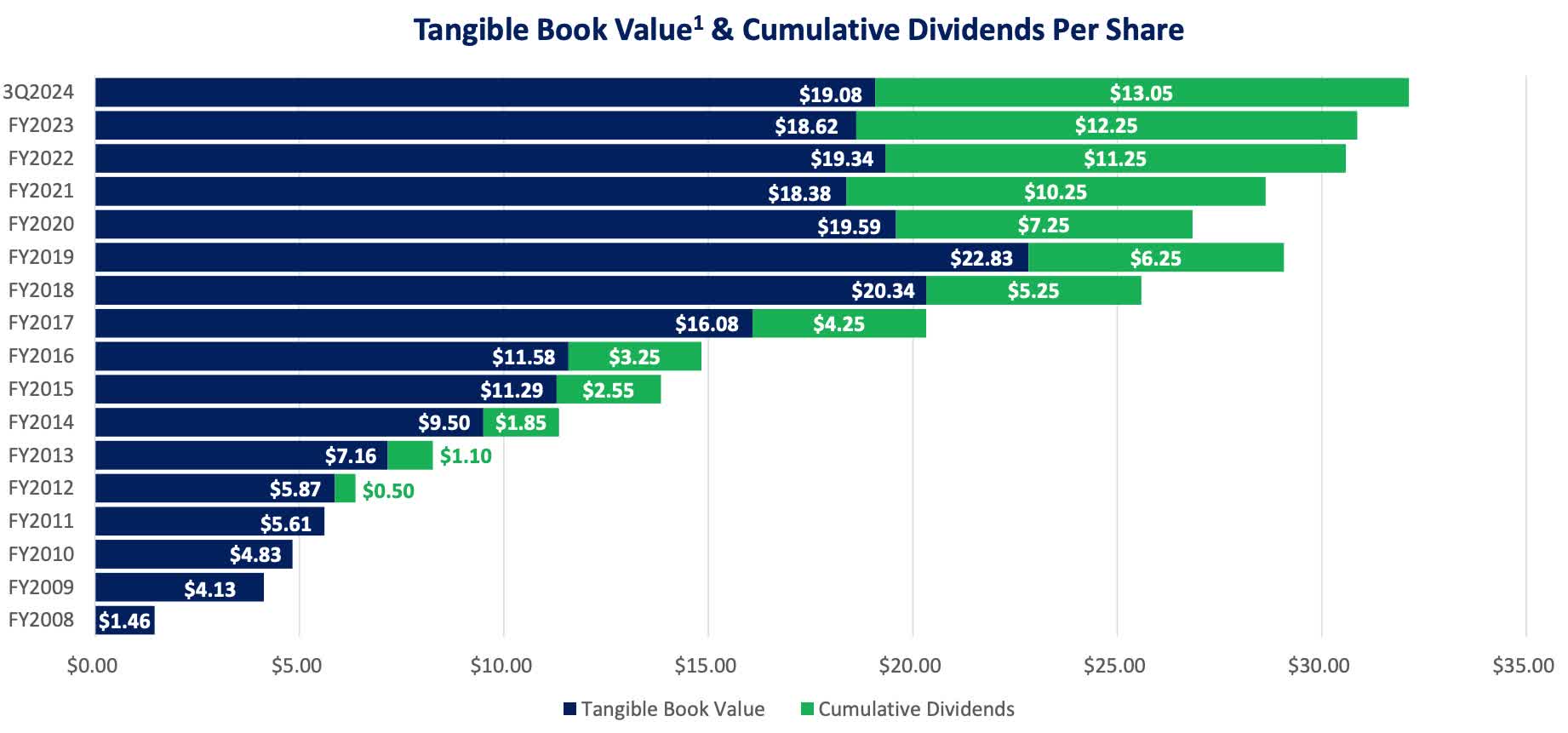

Below you can see the company has steadily increased its book value and dividends over time. They've also paid a couple of special dividends as well with two during the pandemic year.

AGX investor presentation

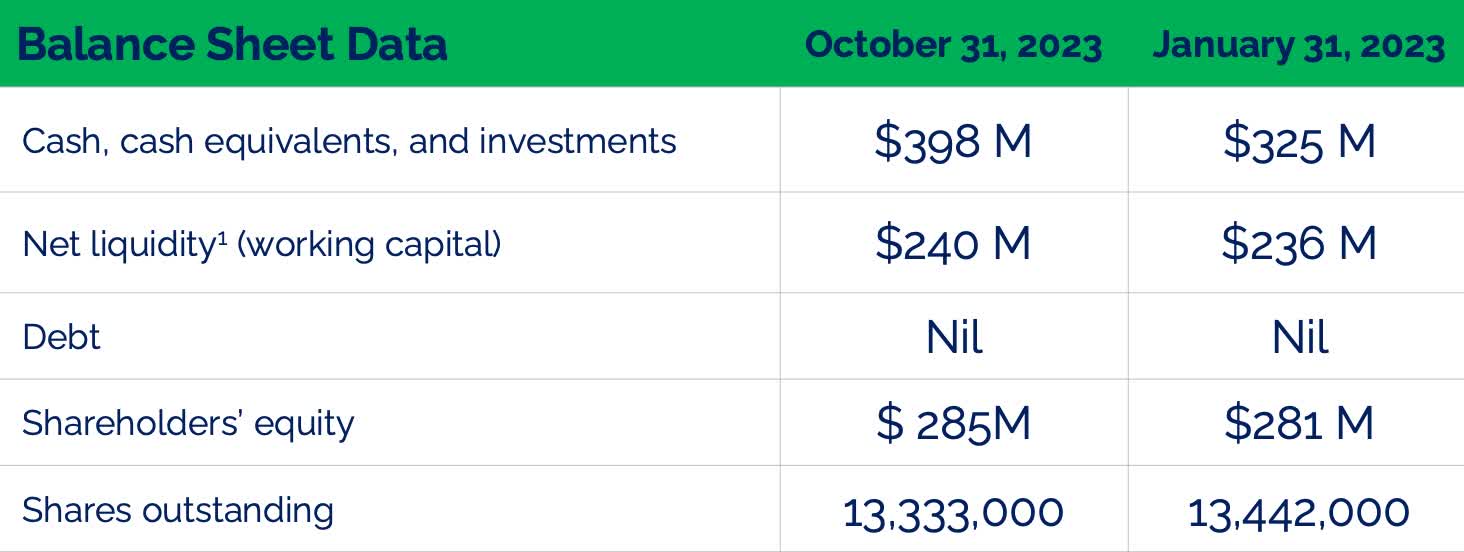

One way Argan supports future dividend growth and occasional specials is the company's fortress-like balance sheet. At the end of their latest quarter, they had no debt. Furthermore, they increased their cash position further strengthening their liquidity position.

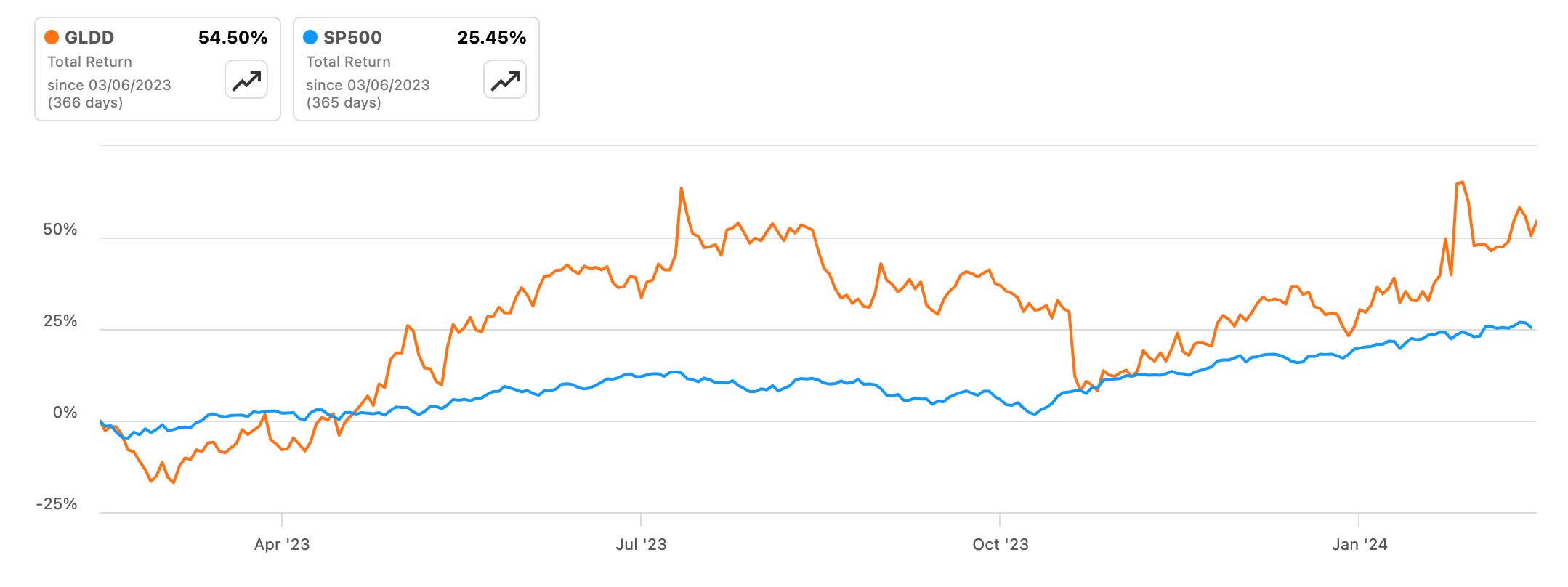

This is in comparison to peers Great Lakes Dredge & Dock's (GLDD) $412 million in long-term debt and Tutor Perini Corp (TPC) who had a long-term debt balance near $800 million.

AGX investor presentation

I also like that the company returns capital to shareholders not only in the form of a growing dividend but share buybacks as well. This shows the company is good at allocating capital since it isn't CAPEX intensive like some businesses.

During Q3, management bought back 43,000 shares for $1.7 million, and they have also been decreasing their share count steadily over the years. YTD they've repurchased 2.6 million shares and at the end of October had 13.3 million shares outstanding.

Over the past 2 years, Argan has managed to decrease its share count roughly 13% from 15.3 million in January of '22. This over time will increase earnings per share as they continue to buy back shares at a healthy rate.

Over the past 3 & 5 years, the company has not done well against the S&P posting negative returns in the past 3 years and up only 7.44% vs the S&P's 82% over 5 years. However, over the past year, you can see the stock has outperformed the index handily with returns of near 55% compared to roughly 25%, more than double. Looking out over the longer term the company was clearly affected by the pandemic but going forward I expect them to continue to outperform or at least compete with the index.

Seeking Alpha

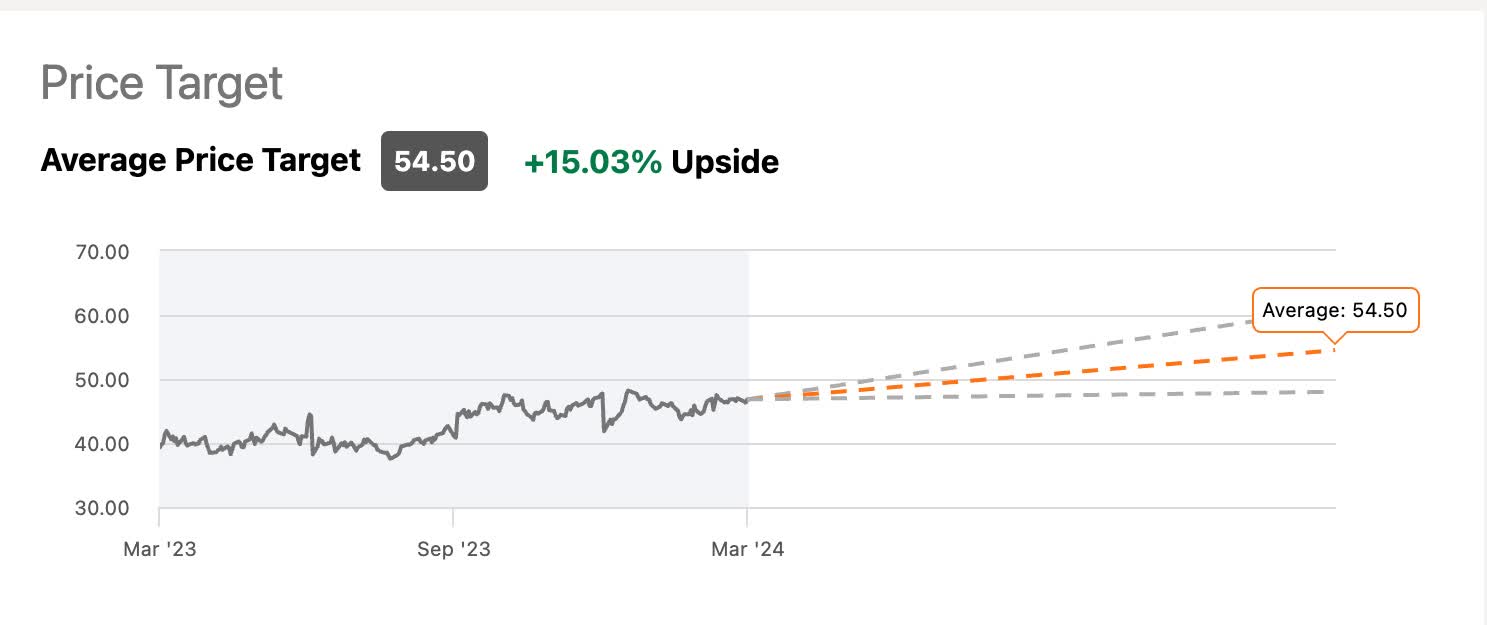

You can see the stock is up double-digits over the last year and has a forward P/E of roughly 20x. While this is not necessarily cheap, they still offer upside to their price target of $54.50 with a strong buy rating from Wall Street as well. I do think currently the share price is attractive. Moreover, the current P/E is roughly in-line with the sector median of 18.95x and below their 5-year average of 25x, further signaling the stock may be undervalued.

Seeking Alpha

Using their FWD P/E of 25x this implies a fair value of roughly $60 a share for Argan giving investors the potential for 25% upside from the current price of roughly $48 at the time of writing. And with the challenging economic backdrop expected to ease in the near future, I see the stock nearing this price in the not-too-distant future.

Due to the company's business model, they are highly susceptible to elements like weather and economic activities. As previously mentioned, their bottom line was impacted by weather-related issues as well as the war in Ukraine and global supply chain delays.

If something like another pandemic, unexpected downturn, or geopolitical issues, this could greatly impact the company's financials going forward, in turn affecting the share price. Unfortunately, companies like Argan are very cyclical and something investors should be aware of if looking to start a position.

Argan is a lesser-known, small-cap company that has strong financials to continue growing its dividend for the foreseeable future. And although the company's bottom line was impacted during the latest quarter, they still managed to grow earnings per share year-over-year by double-digits.

Furthermore, their strong balance sheet and share repurchases show management is aligned and poised to return capital to its shareholders. And even though they suffered headwinds during the pandemic, the company has shown resilience and will likely reward investors with some strong upside in the near future. With their fortress-like balance sheet, strong total returns outperforming the S&P over the past year, and strong dividend growth, I rate this small-cap company a buy.