Just_Super

Just_Super

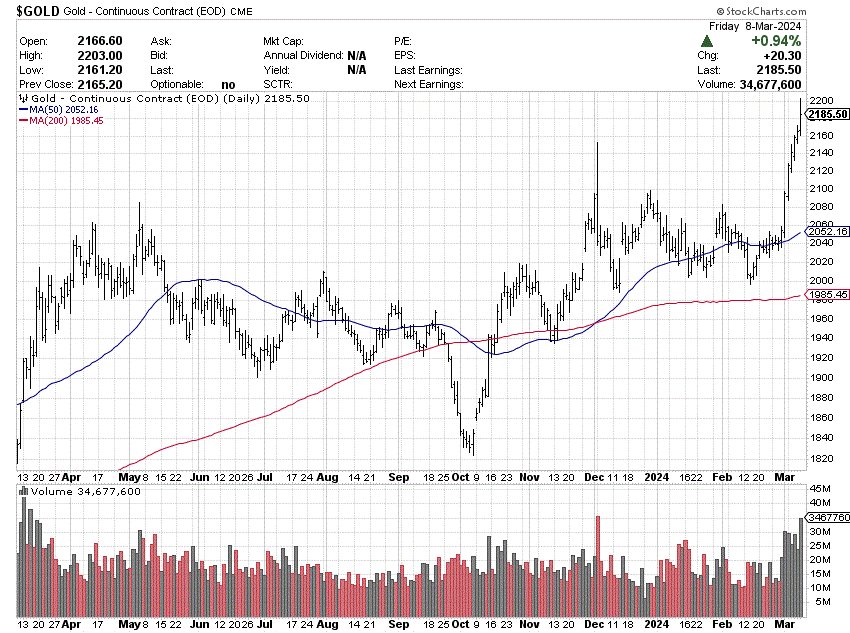

Gold's unexpected breakout to all-time highs in recent trading days has many investors wondering if they should purchase gold miners to leverage future gains. My regular readers know I have been anticipating far higher gold prices over the last year. And, the push above US$2200 oz. intraday on Friday could be just the start of better days ahead for gold bugs and smart portfolio hedgers.

StockCharts.com - Nearby Gold Futures, 12 Months of Daily Price & Volume Changes

I wanted to put out a quick story on which of the major gold miners has the strongest setup on the charts to outperform the sector. I have posted plenty of gold asset buy ideas including Agnico Eagle (AEM) here, Newmont (NEM) here, Coeur Mining (CDE) here, Seabridge Gold (SA) here, Pan American Silver (PAAS) here, and a host of others since late 2023.

Right now, I would like to concentrate on Alamos Gold (NYSE:AGI), which appears to be experiencing a vacuum of sellers in recent weeks on the supply/demand technical charts I follow. I talked about Alamos in September here, as having a terrific setup to take advantage of rising bullion prices. I explained the bullish background summary of the investment like this,

I would say the stock looks more fully valued than other major mining enterprises in the precious metals sector. In term of a cheap valuation, you will need to look at Newmont or Barrick for a high North American asset weighting at a better valuation. Yet, Alamos' higher valuation is well worth the price of admission. You are getting an A+ balance sheet, A+ operating mines for life of reserves and location, A+ cost structure per ounce produced, A+ management team, and a B+ growth outlook in one investment security.

In the end, the above combination of factors leads me to believe Alamos is one of the "safer" individual miners to own, in terms of short-term volatility and longer-term positive performance (having traded the sector since 1986).

One of the investment angles I like to research (that the vast majority of stock market analysts and bloggers ignore) is the share supply/demand dynamics before writing about or buying a security in my own account.

In this vein, Alamos Gold is today standing out as a unique buy candidate. In my work, the odds of investment gains are even better now than my original September story suggested. Not only will rising gold prices pump business sales and earnings (vs. the $1950 price months ago), but the clear absence of AGI sellers in March should usher in a nice stock quote gain into summertime.

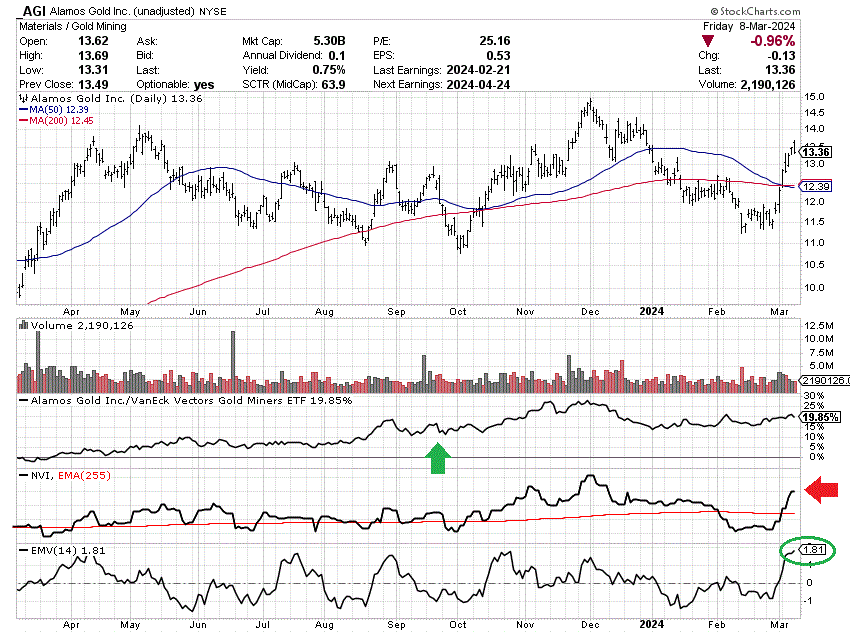

Below I have drawn a basic 12-month chart of daily price and volume fluctuations. You will notice, Alamos has continued to outperform the sector (green arrow marking my September article) as measured by the VanEck Gold Miners ETF (GDX).

In addition, super-strong Negative Volume Index readings in March (red arrow), alongside a spike in the 14-day Ease of Movement indicator (green circle), are highlighting an absence of overhead supply in the shares. Basically, the jump in gold bullion has caught nearly everyone off guard, where few traders and investors are now willing to part with their positions.

StockCharts.com - Alamos Gold, 12 Months of Daily Price & Volume Changes, Author Reference Points

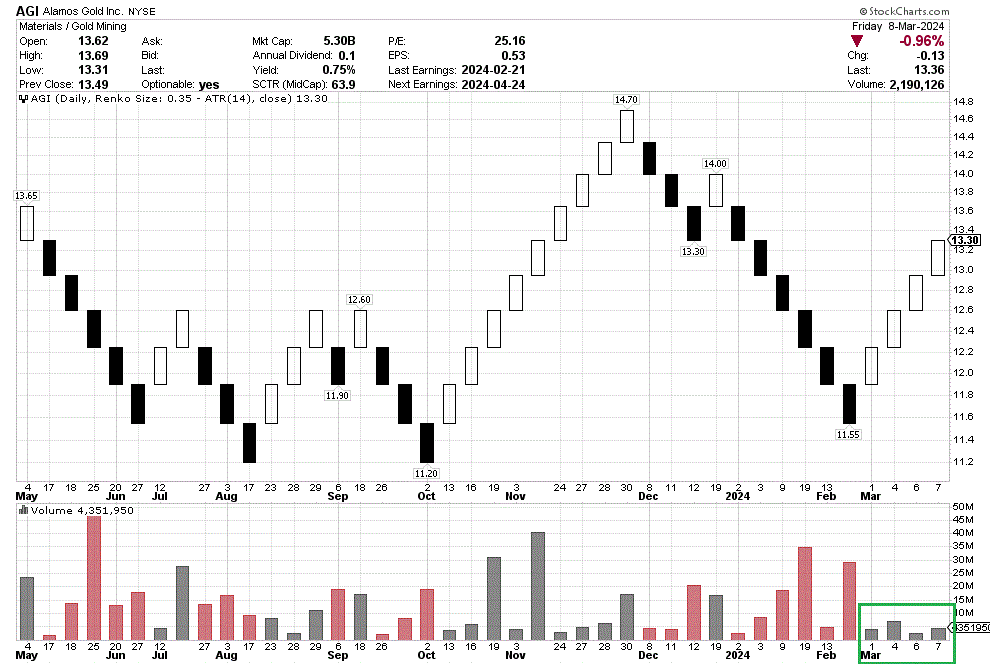

Perhaps even more telling is the ability of price to climb on a Renko chart creation with very little buying interest fueling the gain (boxed in green). In my work, when a string of low-volume sessions can support a big price advance, you are often at the beginning of some sort of bull run. The Renko chart indications cannot tell us how far price will run to the upside, or how quickly. However, a green light for future gains is definitely flashing right now.

StockCharts.com - Alamos Gold, Basic 10-Month Renko Chart, Author Reference Point

I rate the overall chart pattern for Alamos Gold as A+ vs. the gold mining sector in the middle of March 2024. The superb relative strength pattern over the last year, and lack of selling interest in recent weeks should mean AGI will be a top performer out of the group over the next 3-6 months.

If the stock market tanks, or recession strikes, and/or money printing resumes by the Federal Reserve, gold assets could become a leading choice for capital inflows during 2024. Plus, the usual geopolitical worries about China invading Taiwan, Middle East wars leading to crude oil supply disruptions, Russia's intentions with the Baltics and Ukraine, plus America's widening political divide are other reasons to plow money into gold bullion and related miners.

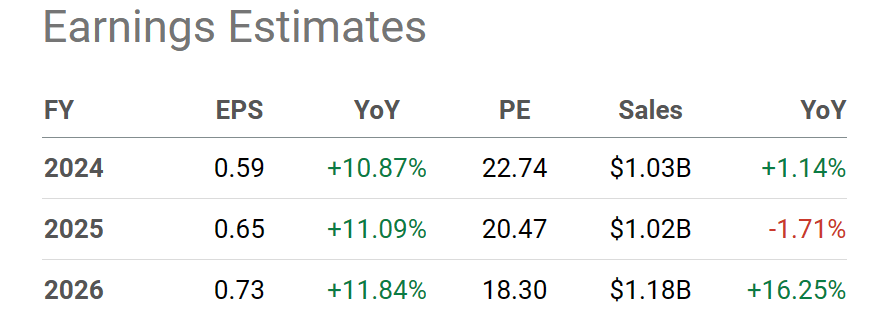

What's the upside proposition for AGI's price? In the olden days when I first started trading gold miners during the 1980s and 1990s, companies with little debt, long-life gold reserves and low extraction costs, located in safer mining jurisdictions like Canada, often traded at 50% to 100% premium P/Es to the general market. Not today. Alamos is going for NO premium, and perhaps a slight discount to the S&P 500 P/E in the low-20x range for 2024-25. To me, gold miner valuations have gotten quite irrational on the downside since late 2023.

Seeking Alpha Table - Alamos Gold, Analyst Estimates for 2024-26, Made March 8th, 2024

Remember, the above analyst estimates are getting stale on the gold price spike of early March. Actual results will likely be 5% (revenue) to 10% (earnings) better than listed, assuming gold remains closer to $2200 oz. for 2024.

As such, a return to premium P/E valuations on the potential for much higher earnings and cash flow with a climbing gold price in 2024 could support a minimum +50% quote jump this year. And, if we get a deep recession or new geopolitical trouble in the world, gold assets could fly higher. Under this scenario, gains of +75% to +100% are possible for Alamos over the next 12-18 months. For example, $2500+ gold could support closer to $1 EPS, with a more rational P/E ratio of 25x generating a price of $24 or better.

What's the downside? At this stage, gold bullion prices would have to reverse course and stay under $2000 an ounce for Alamos to experience a large sustainable share quote loss, in my opinion. I believe a gold move under $1900 oz. is now necessary to pull AGI's price to 52-week lows under $10 and keep it there. Otherwise, I peg the worst-case risk side of the equation at $9 (-35% loss), mostly in a Wall Street crash scenario, pulling down all equities (even gold miners) for a spell at least. The odds of either declining gold prices or a stock market super-bear are not zero, maybe in the 10% to 20% range for the rest of the year.

My personal view is Alamos stock should "outperform" the S&P 500 during 2024 in some shape or form. Too many variables are pointing higher right now for gold assets generally, and AGI in particular.

I am upgrading my rating to Strong Buy, and own a small position. Alamos Gold should be one of many names held in properly diversified gold/silver exposure inside your portfolio. I am comfortable with net precious metal weightings in the 10% to 20% range for the average investor (including both bullion and miners). I am nearer the high end.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.