DarioGaona

DarioGaona

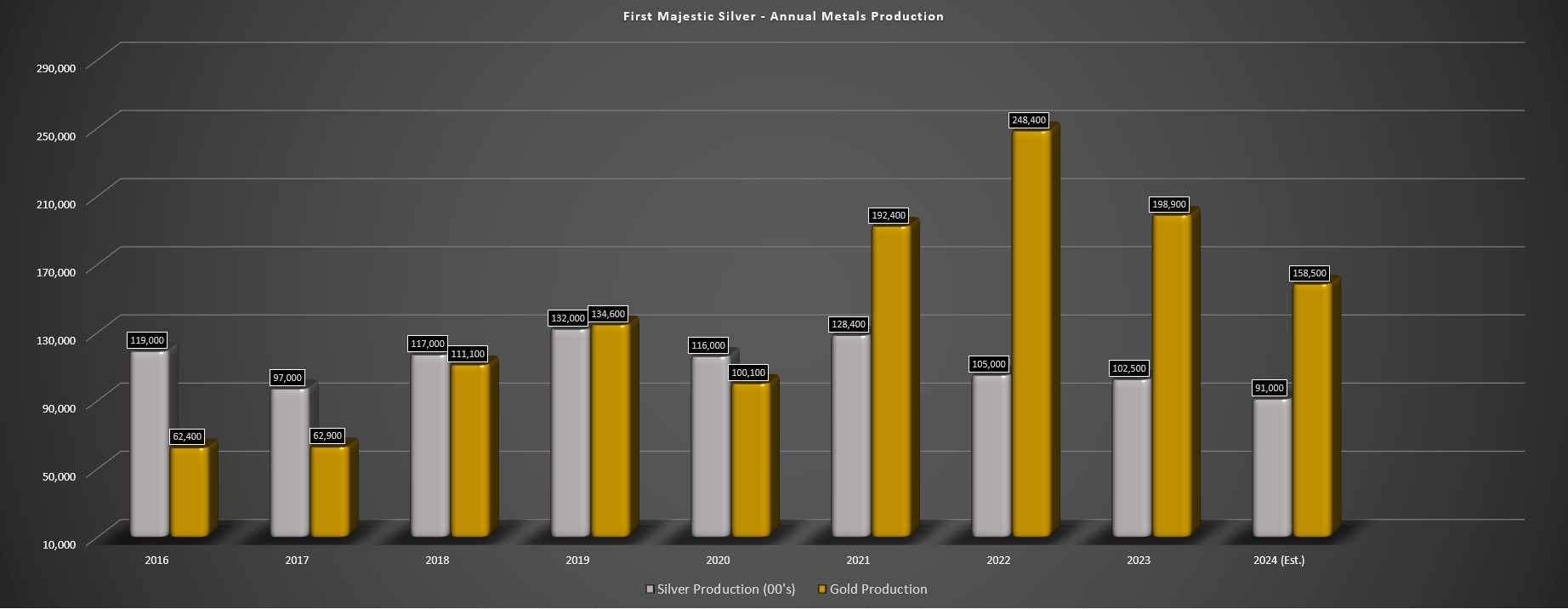

We're more than halfway through the Q4 earnings season for the precious metals sector, and one of the most recent companies to report its results is First Majestic Silver (NYSE:AG). The company had another difficult year with annual silver production declining yet again to ~10.3 million ounces, and gold production also declined sharply, resulting in a significant decrease in silver-equivalent production [SEO] and annual revenue. For those following the story, much of the dip in gold and SEO production can be attributed to moving Jerritt Canyon into care & maintenance, which has improved the company's operating costs given that this was its highest-cost operation.

In this update, we'll dig into the Q4 and FY2023 results, recent developments, and see whether First Majestic is finally sitting at a level where it's worthy of investment.

Jerritt Canyon Asset - Company Website

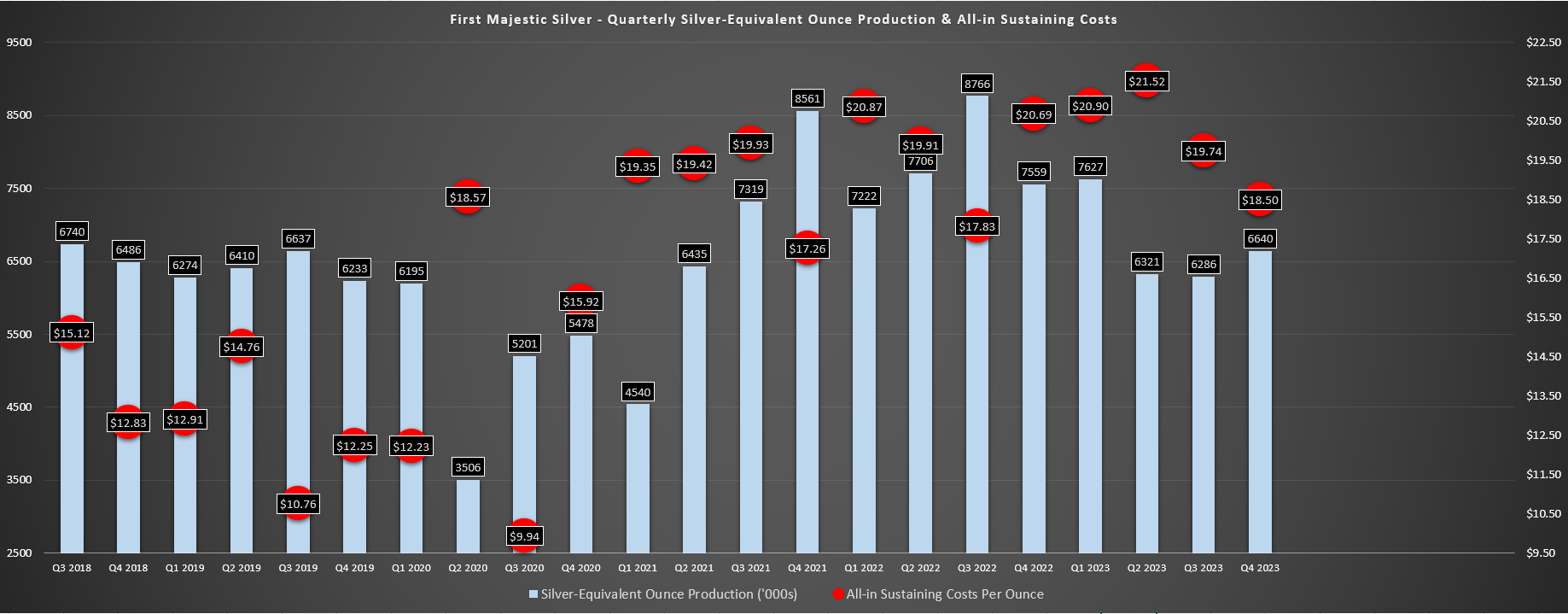

First Majestic Silver ("First Majestic") produced ~2.61 million ounces of silver and ~46,600 ounces of gold in Q4, translating to a 9% increase in silver production but offset by a 26% decline in gold production. The result was that silver-equivalent ounce [SEO] production fell 12% year-over-year to ~6.64 million SEOs. As for its full-year results, annual silver production fell for its second consecutive year and is down substantially from its peak of ~13.2 million ounces of silver production, impacted by lower grades at San Dimas, lower production at La Encantada, and only a slight uptick in silver production at Santa Elena year-over-year with mining at the more gold-dominant Ermitano Mine.

First Majestic Silver - Quarterly SEO Production & AISC - Company Filings, Author's Chart

First Majestic Silver Annual Metals Production - Company Filings, Author's Chart

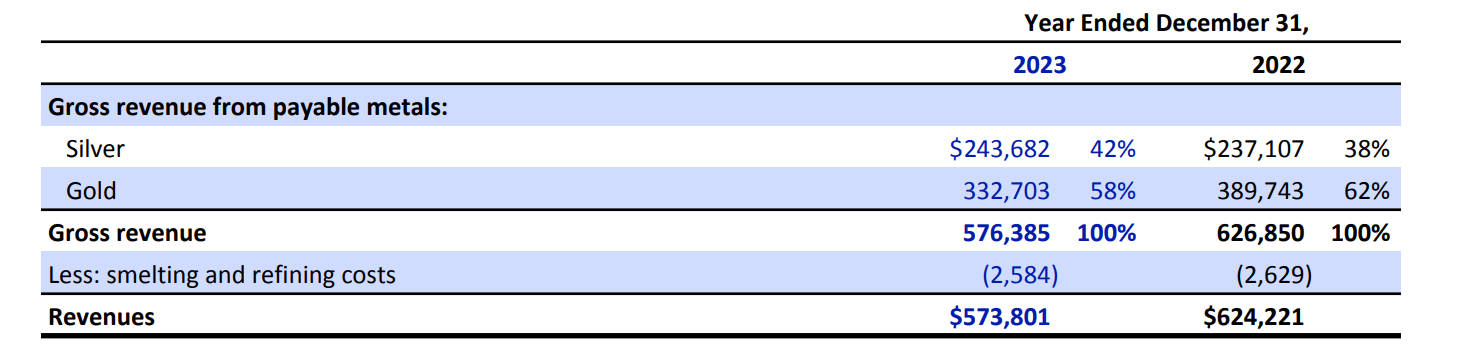

Digging into the results a little closer, we can see that Q4 SEO production has been in a steep downtrend since Q3 2022 with only a minor uptick in the most recent quarter, and while costs are down from their peak, this is largely due to taking its highest-cost asset in Nevada offline. However, all-in sustaining costs [AISC] for its core business (ex-Jerritt Canyon) are up over 50% on a four-year basis to $18.50/oz (Q4 2019: $12.25/oz) due to inflationary pressures, a stronger Mexican Peso and a declining grade profile at San Dimas and La Encantada, and while Santa Elena is doing better at Ermitano, this mine is primarily a gold producer, significantly impacting First Majestic's percentage of revenue coming from silver. In fact, gross revenue from silver has declined from 58% in FY2019 to 42% as of FY2023, stripping away some of First Majestic's premium as a primarily silver producer.

Gross Revenue From Payable Metals - Company Filings, Author's Chart

As for its flagship San Dimas Mine, First Majestic produced ~6.36 million ounces of silver and ~77,000 ounces of gold for the year, translating to a slight in increase in silver production (FY2022: ~6.2 million ounces of silver), offset by lower gold production (~80,800 ounces). The higher silver production can be attributed to higher throughput of ~875,000 tonnes at lower grades of 240 grams per tonne of silver and 2.85 grams per tonne of gold, a meaningful slide from 261 grams per tonne of silver and 3.31 grams per tonne of gold, respectively in the prior year. And not surprisingly, given that any increase in production was driven by higher throughput (not grade driven), full-year AISC increased to $16.48/oz vs. $13.76/oz, putting a meaningful dent in the asset's AISC margins. Meanwhile, total production costs per tonne increased over 13% to ~$177/tonne, creating an increased hurdle for adding new mineral reserves with cut-off grades likely to rise further this year.

Moving to the company's Santa Elena Mine, it had another solid year on the back of Ermitano, with ~1.18 million ounces of silver and ~100,500 ounces of gold produced, an improvement relative to ~1.23 million ounces of silver and ~94,700 ounces of gold in 2022. The increased production was due to higher throughput (~883,000 tonnes) and higher gold and silver grades, in addition to improved gold recoveries with the new dual circuit plant. That said, lower silver recoveries of 64% (FY2022: 73%) impacted silver production on a full-year basis. On a positive note, silver recoveries were much better in Q4 at 73% while gold recoveries hit a record of 96%, allowing for a strong finish to the year for Santa Elena when combined with increased silver grades. And overall, this asset is performing better on a two-year basis since bringing Ermitano online, allowing it to hold costs at more respectable levels at this asset relative to 2022 levels.

Ermitano Mine - Company Website

Finally, while La Encantada has been a steady little contributor to annual silver production, 2023 was not a great year for the asset with annual production declining from ~3.09 million ounces to ~2.72 million ounces while costs soared from $18.48/oz to $24.28/oz. It's worth noting that production got worse throughout the year, with production declining to a multi-year low of ~516,100 ounces of silver in Q4. Not surprisingly, costs came in at even higher levels in Q4 given the lower production ($34.14/oz AISC vs. $19.39/oz in Q4 2022) and 2024 is not expected to be any better based on a guidance midpoint of 2.3 million ounces of silver at ~$29.00/oz AISC. This is related to limited water availability,

As for improving the situation at La Encantada, First Majestic noted that while it hoped production would return to normal by year-end 2023 after losing a water well in Q2, it's had a tougher time than expected sourcing water. The current plan is to drill three additional holes for water this quarter, but to be conservative, it has assumed it does not discovery any water in 2024, which explains the material decline in annual production implied by FY2024 guidance at this asset (2.3 million ounces of silver midpoint vs. 2.72 million ounces in 2023). The company's CEO stated the following on its year-end conference call:

"We debated this among management on how we guide because I think our guidance is quite conservative. I think we've kind of a little gone a little bit overboard quite frankly. But we're assuming that we do not discover any water in 2024. I don't believe it, quite honestly. And we've had this in general discussion among the senior management team, but we actually can't come up with a number. So we decided, okay, go ultra conservative and just assume that there's no additional water we're going to run at this 2.2 million to 2.4 million ounce rate for all of 2024.

Of course, we're not going to accept this. We're going to drive these costs down throughout the first couple of quarters of 2024 and we expect to hit water sometime throughout the next couple of quarters, which will also, of course, bring La Encantada back up to its normal throughput rates and normal cost rates. But we can't guarantee that. We don't have any technical guidance to suggest that we're going to be successful. Therefore, we decided to take the ultimate conservative view on this asset. So that's where that number has been driven from. Hopefully, it turns out better than what we're guiding."

- First Majestic January 2024 Conference Call

Obviously, this sharp decline in production at La Encantada is a negative development that will weigh on costs, but the silver lining is that management has guided conservatively this year, suggesting there could be room for some upside if they are successful drilling new wells. And while costs at this asset have risen to levels that result in negative AISC margins, this is largely a function of now lacking leverage on fixed costs at this asset. Hence, I am cautiously optimistic that La Encantada can get costs back below $22.50/oz in 2025, but this still won't do much for the company unless silver prices cooperate and can head back above $26.00/oz and stay there.

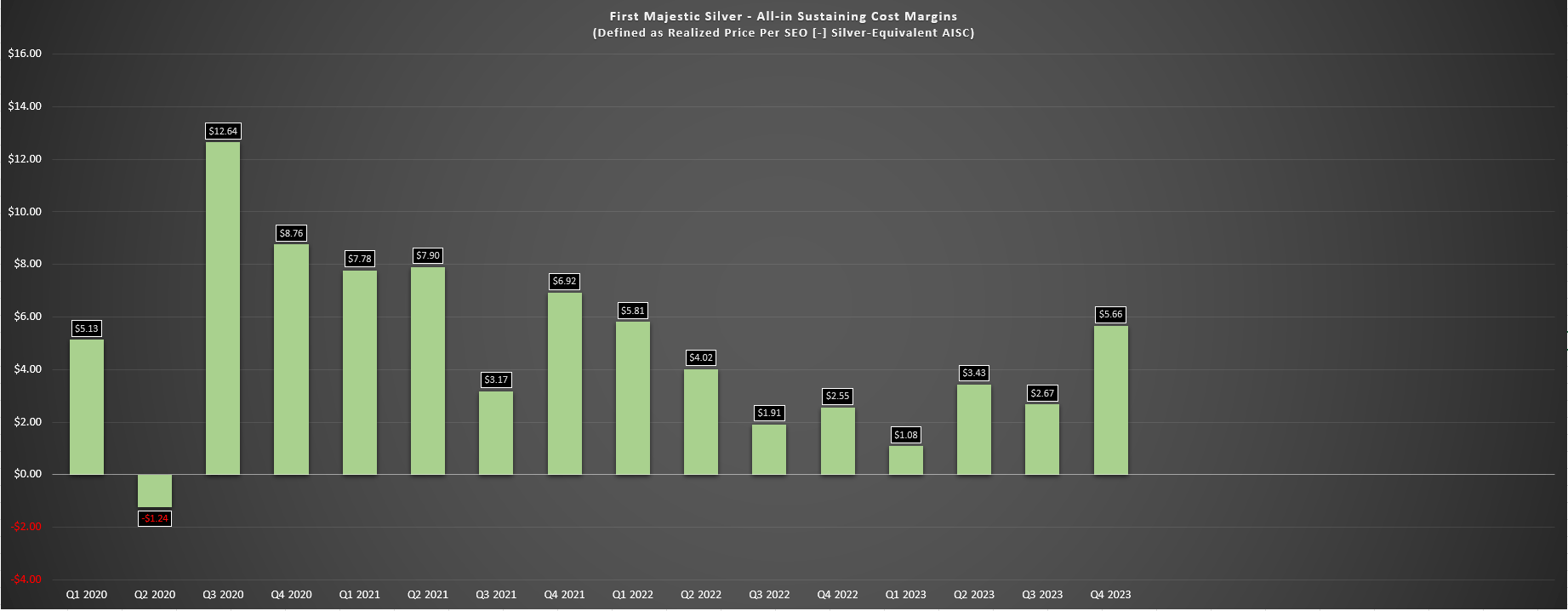

Looking at costs and margins, 2023 was not a year to write home about, with Q4 all-in sustaining costs still elevated at $18.50 per SEO, resulting in razor-thin AISC margins of $5.66/oz or ~23%. As for its full-year results, AISC increased to $20.16/oz vs. $19.74/oz and are expected to remain elevated at $20.00/oz despite the closure of Jerritt Canyon which weighted on H1 2023 costs. The higher costs can be attributed to continued inflationary pressures sector-wide, a much stronger Mexican Peso than what the company was working with on average in 2023 (USD/MXN: 17.70/1.0 in 2023 vs. 17.1/1.0 currently), and lower production. And assuming First Majestic's average realized price per SEO comes in at $24.20/oz this year, we won't see much improvement in AISC margins vs. the $3.13/oz AISC margins (~13%) reported in 2023.

First Majestic AISC Margins - Company Filings, Author's Chart

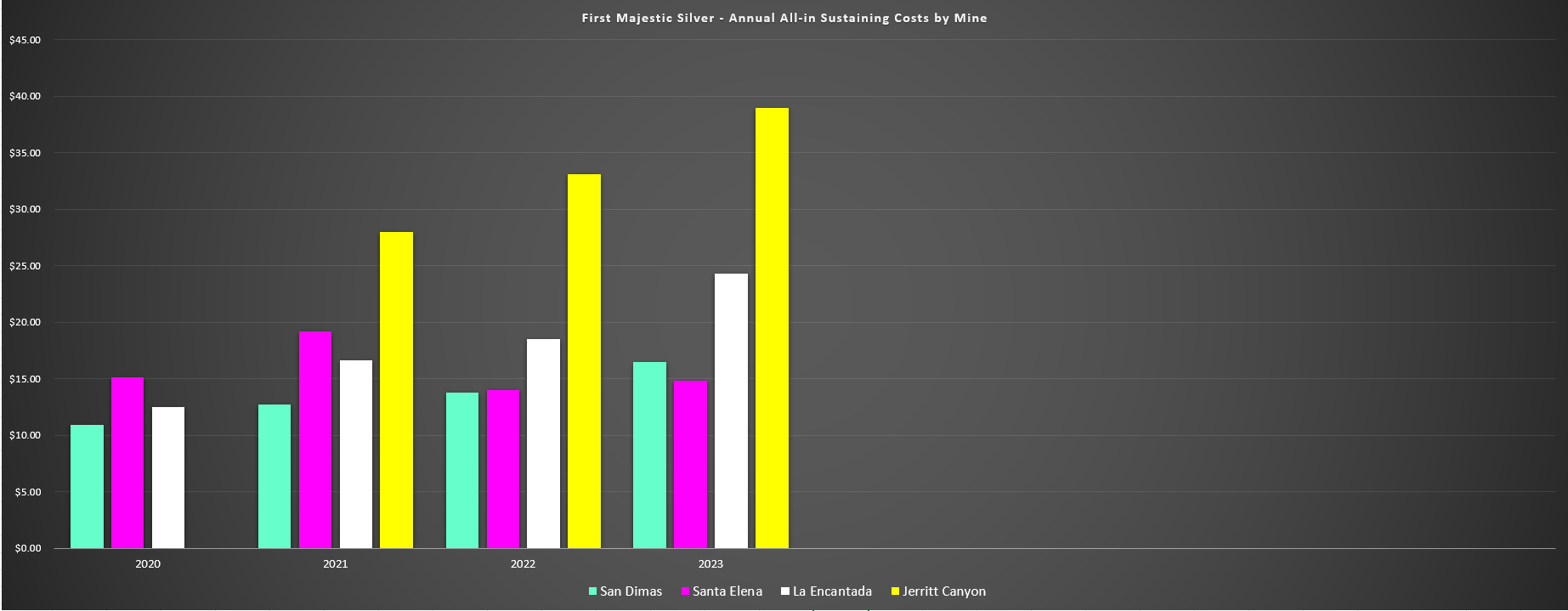

First Majestic Annual AISC by Mine - Company Filings, Author's Chart

Looking at First Majestic's costs across its asset base, it's certainly been a positive that the company turned the lights off at Jerritt Canyon, with all-in sustaining costs consistently above $2,000/oz which made it very difficult to generate any free cash flow at this asset. This was undoubtedly disappointing for shareholders given that the Jerritt Canyon acquisition resulted in significant share dilution, and while gold prices are sitting at much better levels today, it's tough to be optimistic on this asset unless we see a consistent $2,100/oz to $2,300/oz gold price environment and a far more optimized operation than what it looked like over the two years it was online under First Majestic.

That being said, while taking Jerritt Canyon offline has led to a decline in costs as of Q4 ($18.50/oz), it's quite clear that annual AISC has risen materially across its assets with an impact from a stronger Peso, inflationary pressures and lower grades. And while this wasn't an issue in 2021 and 2022 as costs were still relatively low at its largest contributor, San Dimas, the outlook for this asset is not great with AISC set to increase to $16.50/oz at the high end of guidance for 2024, effectively flat-lining at a higher cost base and representing significant margin compression since pre-COVID levels. Hence, without a new high-grade discovery at this asset or much higher silver prices, it's difficult to be overly optimistic about free cash flow generation from this site, especially when it's saddled with a significant stream held by Wheaton Precious Metals (WPM) that impacts its profitability (25% stream on gold-equivalent production with payment of just ~$630/oz), or 42,200 ounces of gold delivered in 2023 to Wheaton.

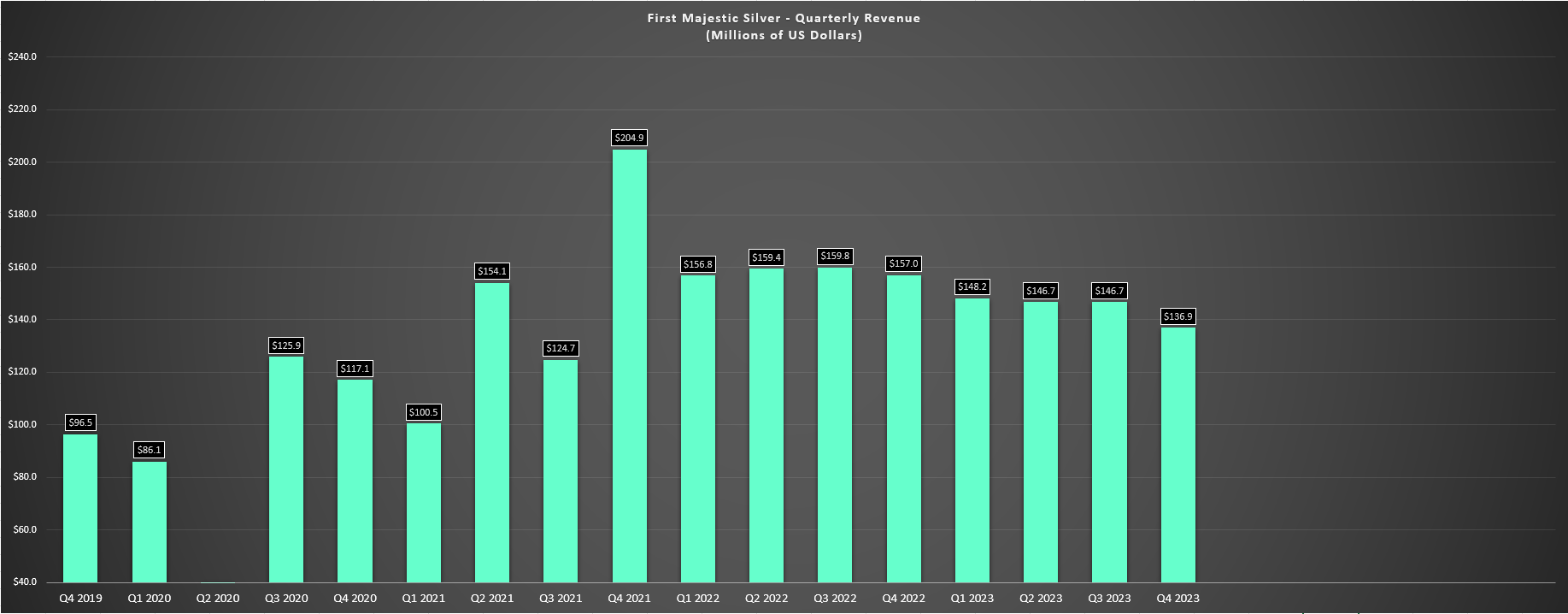

First Majestic Quarterly Revenue - Company Filings, Author's Chart

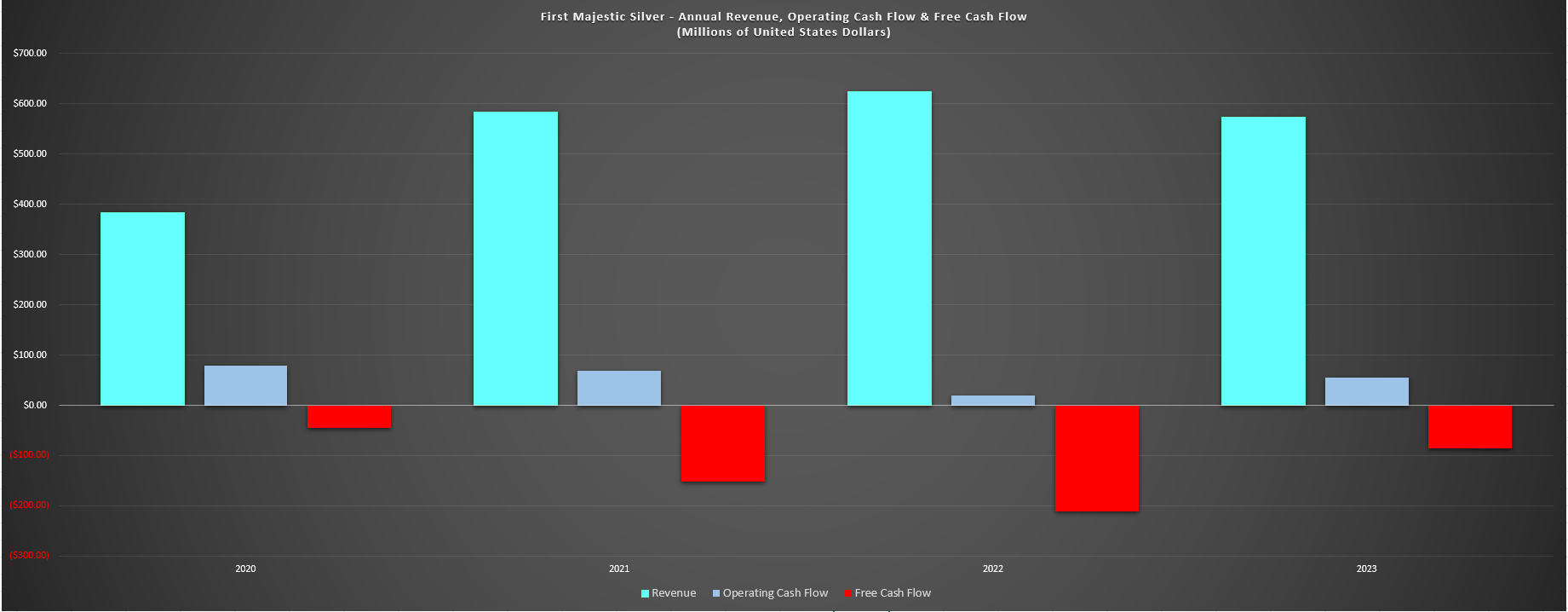

The above point about profitability can be seen by the company's financial results which show that while First Majestic reported $136.9 million in revenue in Q4 and $573.8 million in FY2023, it's not generating much operating cash flow and free cash flow has been consistently negative. In fact, operating cash flow came in at just ~$55.6 million in 2023 even if it improved from FY2022 levels ($19.0 million), but this still resulted in free cash outflows of ~$85 million after capital expenditures of $141 million. Simultaneously, shareholders have been getting diluted further, with ~13.9 million shares sold under the company's ATM at US$6.22 in 2023 after ~11.9 million shares were sold in 2022.

First Majestic Annual Revenue, Operating Cash Flow & Free Cash Flow - Company Filings, Author's Chart

This translated to ~5% share dilution last year on top of massive share dilution in 2021/2022 related to ATM sales and the Jerritt Canyon deal, and we can see how this has impacted its per share growth, which is non-existent. In fact, as the below chart shows, annual SEO production has made little progress from 2019 to 2024 guidance (~23 million SEOs on a constant gold/silver ratio basis), but we've seen over 30% share dilution in the same period as shares outstanding have gone from ~210 million to nearly 290 million. And with little hope of generating positive free cash flow this year, I wouldn't rule out further share dilution for the company. Therefore, and as I've made clear in many past updates, I don't see First Majestic as an attractive investment as I prefer to focus on companies growing per share metrics, with B2Gold (BTG) and Agnico Eagle (AEM) being two examples of producers with glowing track records of improving per share metrics.

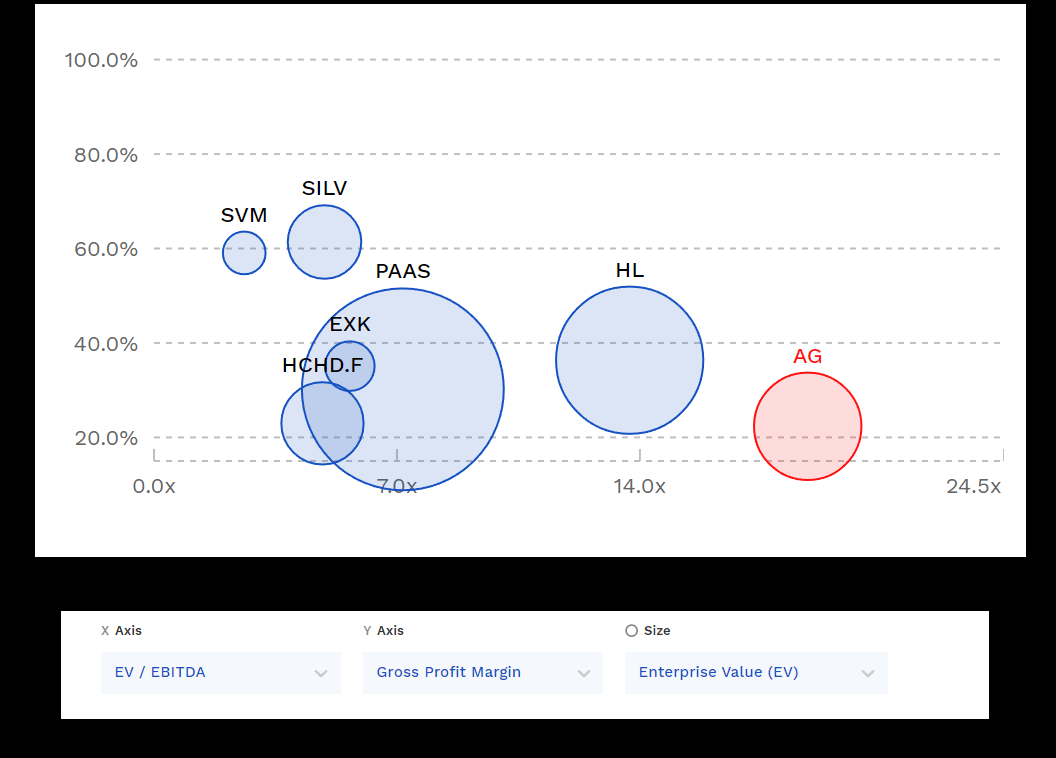

Based on ~297 million fully diluted shares and a share price of US$4.70, First Majestic trades at a market cap of ~$1.40 billion and an enterprise value of ~$1.50 billion. At first glance, this might seem like a reasonable valuation vs. other silver producers like SilverCrest Metals (SILV) trading at half the valuation with less than half of the annual SEO production. However, the two company's margin profiles could not be more different, with SilverCrest expecting to have all-in sustaining costs closer to $15.00/oz, 25% below that of First Majestic. Meanwhile, Las Chispas has a longer weighted-average mine life than First Majestic and is consistently generating free cash flow, allowing it to buy back a significant amount of shares last year at depressed prices rather than selling shares at multi-year lows like First Majestic.

Silver Producers - Margins & Valuation - FinBox

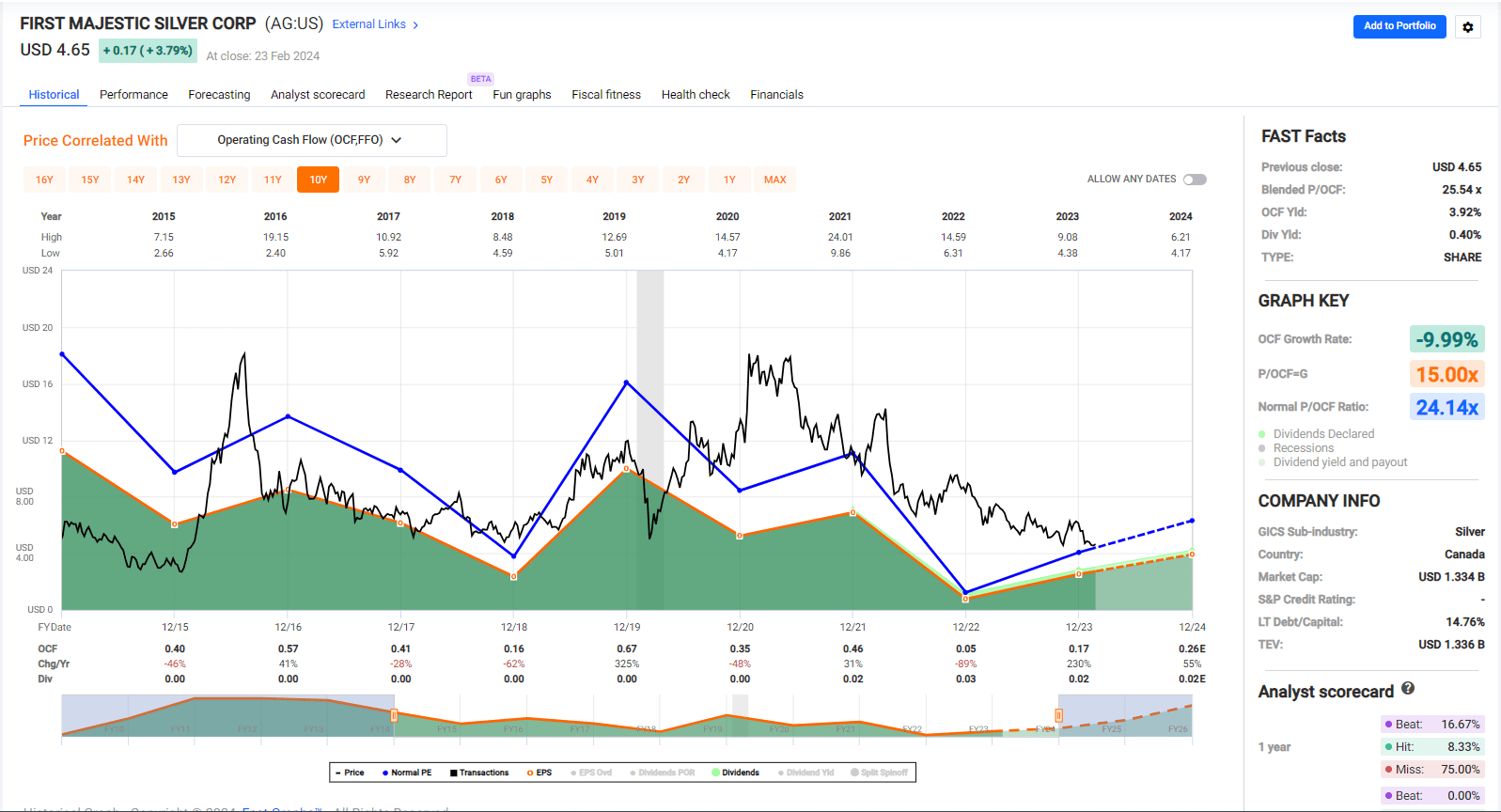

First Majestic Cash Flow Multiple - FASTGraphs.com

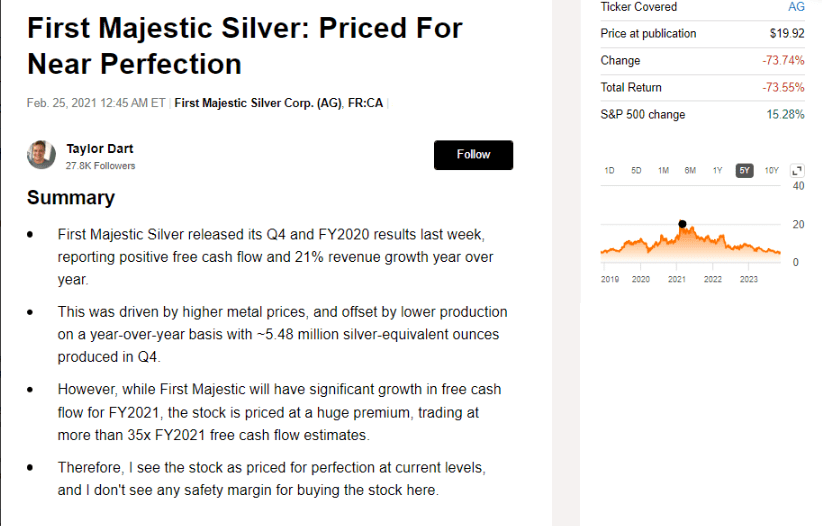

First Majestic Avoid Article 2021 - Seeking Alpha Premium/PRO

Normally, a stock down ~80% from its all-time highs would be an attractive investment, but given the significant margin compression and share dilution that we've seen over the past three years, combined with the fact that First Majestic was priced for perfection at its peak in 2021, this is not the case here. In fact, First Majestic is still trading at ~18x FY2024 cash flow per share estimates and I don't see any reason for a business with these margins and a track record of under-delivering to trade at over 10x cash flow, let alone 18x cash flow. This is especially true when better businesses like Agnico Eagle trade at less than 9x forward cash flow currently with Tier-1 jurisdiction operations, significantly higher margins, a stronger pipeline and a far better track record of creating shareholder value. So, while AG may be down from its highs, I still don't see any margin of safety.

That being said, although First Majestic does not come close to meeting my investment criteria, the stock is the most hated it's been in years, is stretched quite far to the downside and has low expectations coming into 2024. Hence, I would not be surprised to see a significant recovery in the stock if gold/silver prices can have a better year. Therefore, from a swing-trading standpoint, I would expect any pullbacks below US$4.10 to provide a buying opportunity. Still, I am more focused on better-run names that are trading at far deeper discounts to fair value, so I have no interest in First Majestic at current levels even if it may be overdue for a rally.

First Majestic had another disappointing year in 2023 with a sharp decline in revenue, a further decline in its per share metrics and another year of negative free cash flow. Unfortunately, the setup is not any better looking out to 2024, and it's tough to be optimistic about reserve growth at San Dimas and La Encantada without higher silver prices. Hence, if I were looking to put capital to work in the sector today, I see names like B2Gold and i-80 Gold (IAUX) as far more attractive opportunities, with the former paying a ~6.5% dividend yield and trading at just ~6x FY2025 free cash flow and the latter trading at ~0.30x NAV ahead of a transformational year with annual gold production set to quadruple once it brings it ramps up production at its Granite Creek Underground Mine in Nevada.