conejota

conejota

Co-authored with “Hidden Opportunities.”

With inflation on a steady pace of cooling down, the Fed is expected to pursue one of the following three monetary policies.

No change: maintain restrictiveness as inflation drops, but increases the risks of a recession.

Moderate dovish: calibrate monetary policy to a less restrictive stance in the face of falling inflation and a slowing economy

Aggressive dovish: move to easier monetary policy in the face of a recession.

It is clear that rates have peaked, and it is time to put all that cash to work by locking in big yields for the long term. We are currently seeing bond yields that haven’t been around for decades. The issuer guarantees corporate bonds, so the more prosperous and well-managed the company, the better the safety and reliability of the interest payments.

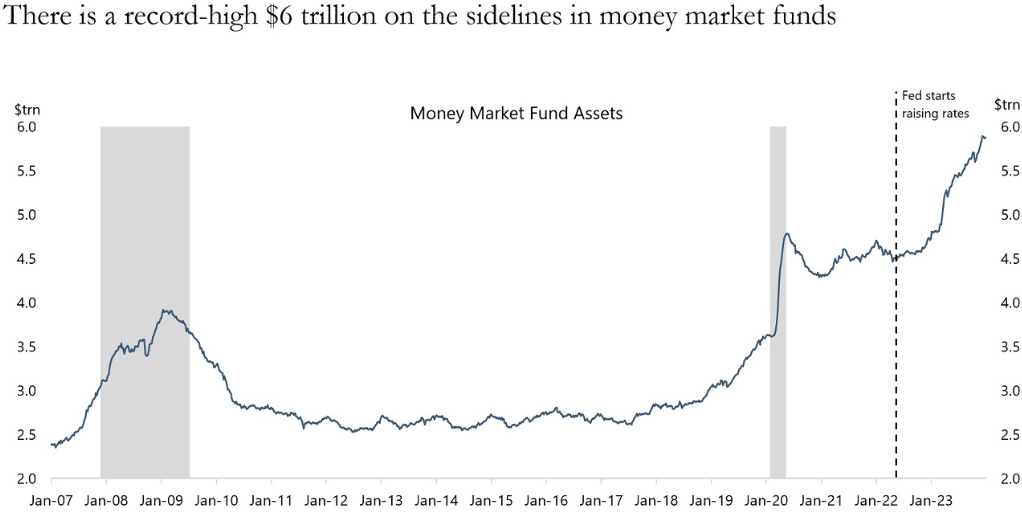

A record $6 trillion currently sits in money market funds, whose interest rates are directly correlated with the Fed Funds Rate. It is only a matter of time before these funds are deployed into equities and fixed-income.

Apollo Academy website

Bond ETFs drew in a record $300 billion in 2023 in anticipation of rate cuts as investors rushed to lock in the high yields. This is only the beginning. BlackRock analysts expect multiple rate cuts this year, potentially causing a solid rally in fixed-income names, as a lot of cash in the sidelines will be hungry to lock in quality yields. We discuss two investment-grade bonds to lock in higher yields for longer.

Oxford Lane Capital Corporation (OXLC) is a CEF (Closed-End Fund) that invests in the equity tranches of CLOs (Collateralized Loan Obligation). CLO are special purpose vehicles set up to hold a portfolio of loans. The interest and principal payments from the underlying loans are used to make payments to the different tranches.

We have extensively discussed OXLC’s business and current fundamentals in several articles. Hence, today’s discussion will be restricted to the fixed-income securities of OXLC.

CEFs have regulatory limits on how much they can leverage their portfolio. For every $1 borrowed through the issue of preferred securities, the fund must have $2 in total assets (asset coverage ratio of 200% including the preferred securities). As such, OXLC’s bond and preferred investors are not just protected by prudent management of CLO assets, but by statutory limits on the fund’s borrowings. Notably, OXLC reported a debt-to-equity ratio of 0.2x at the end of Q2 2023.

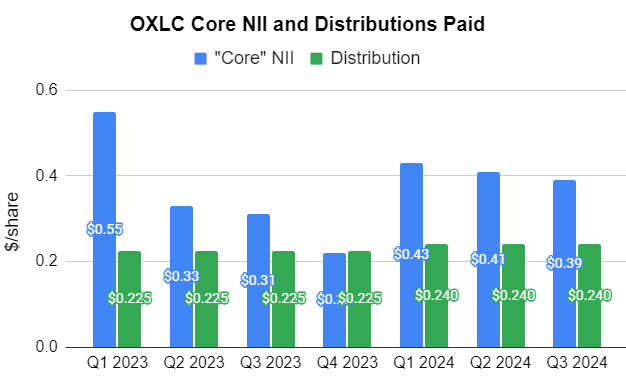

Like other CEFs, OXLC generates total investment income from its CLO investments. Notably, at the end of Q3 2023, OXLC reported a weighted average effective yield of total investments of 16.5%, indicating the highly lucrative nature of its business. After accounting for all fund expenses (including interest payments on the bonds and preferreds), the fund reports the core Net Investment Income. In the past six quarters, OXLC has distributed ~65% of the core NII to shareholders, providing an adequate buffer for reinvestments.

Author’s Calculations

The CEF spent $16.4 million in interest expenses during the first six months of FY 2024 (including $9.3 million towards the preferreds), and generated $86.8 million NII after all fund expenses. Considering adequate common shareholder dividend coverage, OXLC’s BBB-rated bonds present safe income opportunities.

Oxford Lane Capital Corp., 6.75% Notes due 2031 (OXLCL) – Yield 7%

Oxford Lane Capital Corp., 5.00% Notes due 2027 (OXLCZ) – Yield 5.4%.

Among the two investment-grade baby bonds, OXLCL pays an attractive 7% yield that investors can lock until maturity in 2031.

Investment-grade baby bonds from reputable issuers present attractive opportunities when trading below par. OXLC's baby bonds offer robust income protection from the fund's operations, serving as safer income sources for your retirement needs.

American Financial Group, Inc. (AFG) is a 152-year-old insurance company specializing in property and casualty (P&C) insurance, focusing on specialized commercial products tackling unique financial risks and exposures for businesses. AFG’s operations have three major groupings: Property and Transportation, Specialty Casualty, and Specialty Financial.

Underwriting profitability is a fundamental measure of the profitability of an insurance company and is measured as a “combined ratio.” The combined ratio is the sum of incurred losses and expenses from policyholder claims, divided by the earned premiums from the policies. A metric over 100% means an insurance firm is paying out more in claims than collecting through premiums. AFG’s underwriting standards and diligence are clearly seen in the fact that their overall combined ratio was under 94% for ten consecutive years. AFG reported a combined ratio of 91.3% for the nine months of FY 2023, an impressive feat, indicating quality underwriting. The company expects to end FY 2023 with an overall combined ratio between 90-92%.

Higher interest rates are benefitting big insurance firms, who are earning a higher return for far lower risk. 68% of AFG’s portfolio is interest-bearing fixed maturities with an overall portfolio yield of 4.8% and a 2.8-year duration. 93% of AFG’s fixed-maturities were investment-grade securities.

For Q4 2023, AFG reported net earnings of $3.13/share. For FY 2023, AFG’s EPS of $10.06 places the company’s regular common dividend for the period at a comfortable 28% payout ratio. Notably, AFG declared a 12.7% raise to its regular dividend in August and has paid two special dividends amounting to $5.5/share in 2023. AFG’s total dividend payments for 2023 stood at $8.1/share, and the firm reported core net operating earnings between $10.56/share. During FY 2023, AFG also repurchased $213 million of its common stock.

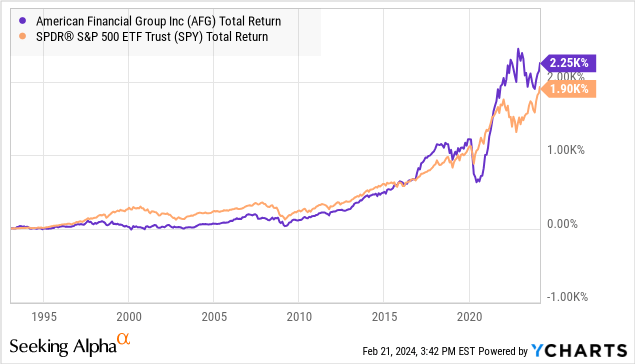

Growing dividends, big special dividends, and share repurchases – AFG has a lot of things going on, and each highlight brings a smile to shareholders. But it is not just that; AFG’s common stock has been a growth superstar, crushing the S&P 500 in the past ten years. Notably, the family of Carl Lindner, Jr., company executives, and the institutional retirement plan for staff owns 24% of AFG's common stock.

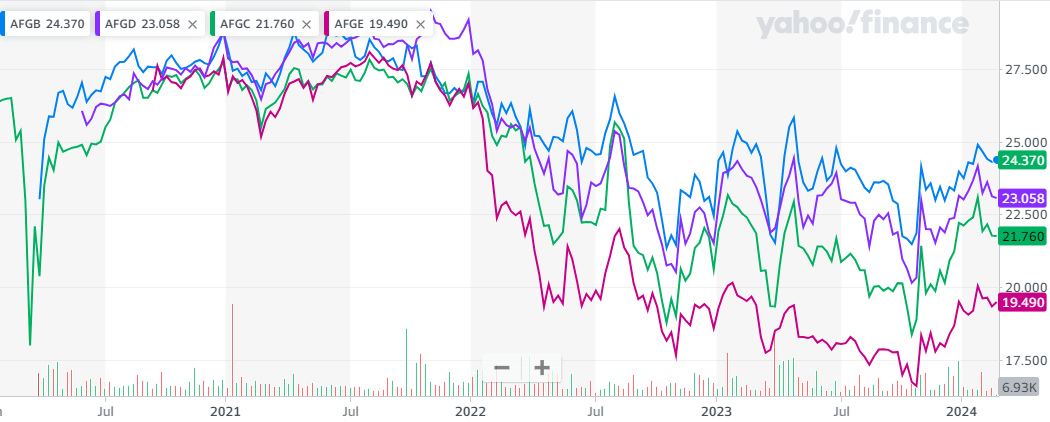

AFG maintains an excellent balance sheet, rated A+/A1 by leading credit agencies, and the company has maintained this rating for 115+ years in a row! AFG has four deeply discounted baby bonds carrying investment-grade “Baa2” ratings that come right below the company’s senior notes in the capital stack.

5.875% Subordinated Debentures due Mar 30, 2059 (AFGB) – Yield 6%

5.125% Subordinated Debentures due Dec 15, 2059 (AFGC) – Yield 5.9%

5.625% Subordinated Debentures due Jun 1, 2060 (AFGD) – Yield 6.0%

4.50% Subordinated Debentures due Sept 15, 2060 (AFGE) – Yield 5.8%.

AFG spent $76 million on interest expenses during FY 2023 (down from $85 million for FY 2022). This is a tiny fraction compared to the sum spent on share buybacks and dividends, and the company generated $852 million in net income after these interest payments were deducted. AFG ended FY 2023 with $5.2 billion in cash and cash equivalents.

AFG’s interest expenses enjoy substantial coverage from the company’s operations and present attractive investment opportunities. Readers must note that AFG purchased $4 million of its Senior Notes during Q2 2023, and despite having maturities in 2059/2060, the discussed baby bonds become callable in 2024-25. As seen from the price action of AFGB and AFGD, we expect the others to inch closer to par with Fed interest rate cuts.

Yahoo Finance

We notably like AFGE at current prices, offering a 5.8% current yield and ~28% capital upside to par value.

Our Investing Group publishes a Preferred Stock & More report every Sunday. We recommended OXLCL to our subscribers last May. Since then, the security has surged almost 8%, delivering a total return of 13.7%, with interest payments worth 5.7%. Similarly, we suggested AFGE in July, which has seen a 6% increase and two interest payments totaling 3.1%, amounting to a total return of 9.1%. These securities still have significant upside potential and offer attractive yields. Our "model portfolio" includes over 20 baby bonds and term preferreds, boasting an average yield-to-maturity of over 9%.

CDs also lack flexibility. The top 3-5-year CD, according to Bankrate, offers around a 4.5% APY but ties up your capital with penalties for early withdrawals. Baby bonds, however, provide much-needed liquidity. You can trade them for gains whenever you're ready to capitalize on upcoming rate cuts.

According to BlackRock, amidst high-interest rates, 2023 was the year of yield. The firm’s analysts expect rates to drop 50-75 bps lower and project 2024 as the year of income. Investors are expected to feel more confident moving away from cash, and high-quality bonds are well-positioned to offer meaningful total returns.