Oleg Elkov

Oleg Elkov

The leasing business is easy to understand. A finance company buys an asset, in this case, aircraft, and leases it out to airlines.

It pays for a portion of the assets in cash and finances the rest with debt. Its cost of capital should be lower than an airline, because it's better diversified, and can repossess the assets and lease to others if an airline goes bankrupt.

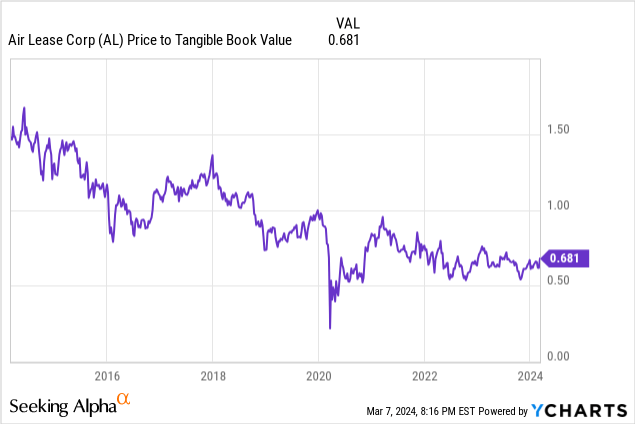

Air Lease (NYSE:AL) looks cheap on most metrics, trading at a 2024 estimated P/E of 9.5x and a 2025 estimated P/E of 7.9x, with a price to book of 0.68x.

With such an inexpensive valuation in an expensive market, you may suspect that the market had doubts about future earnings power or the residual values of the assets. But nothing could be further from reality, as a combination of increased aircraft demand and supply challenges has pushed the prices of aircraft and leases to all time highs.

Pun intended, this business has several of them.

1. Limited Supply

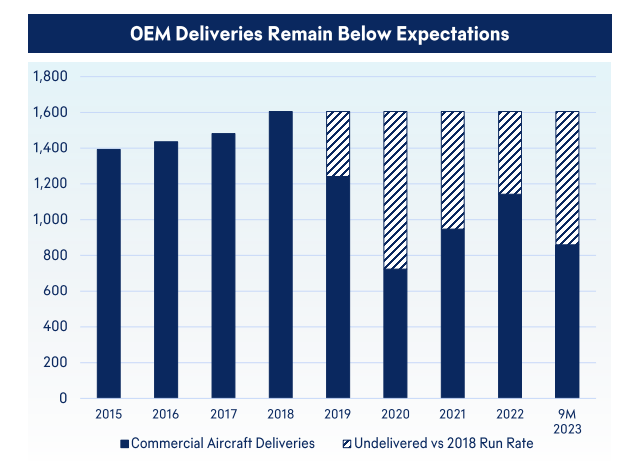

Boeing's (BA) challenges are well noted. Ryanair CEO Michael O'Leary is stating that Boeing is unable to deliver the planes on order and is looking for compensation. Airbus (AIR.PA) is also warning of delivery delays. Add to this RTX Corporation (RTX) engine issues, and the industry is short aircraft.

OEM Aircraft Deliveries (AerCap)

I think these industry production challenges will persist for many years, this coupled with the lower past delivery rates during COVID, will keep supply limited for a long time.

2. Strong Demand/Lease Rates

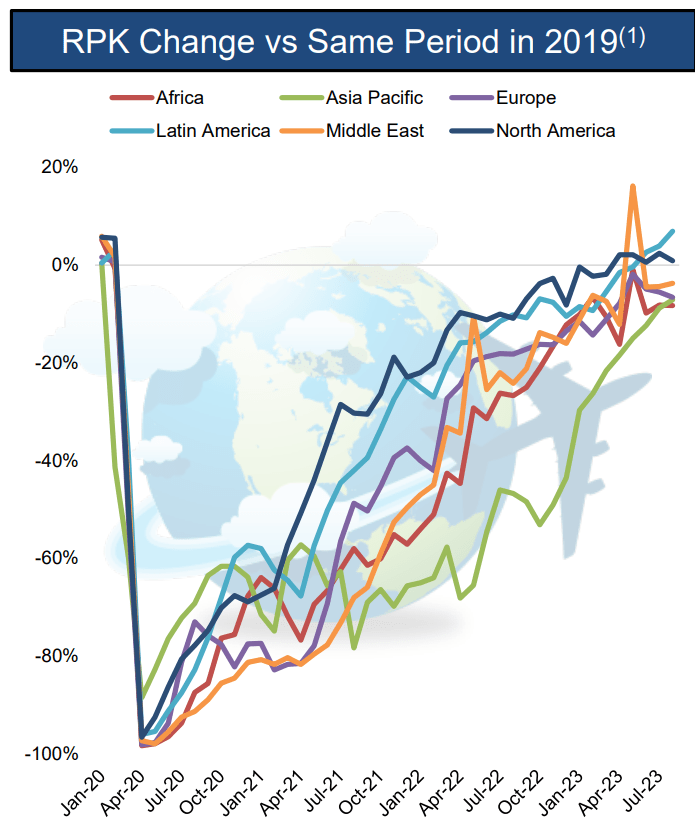

Along with supply challenges, air travel demand is recovering to pre-COVID levels.

Global Air Travel Demand (Air Lease Investor Presentation)

Narrow-body aircraft, which makes up 75% of Air Lease's fleet, are seeing demand jump on the back of a global recovery in air travel and a constrained supply situation.

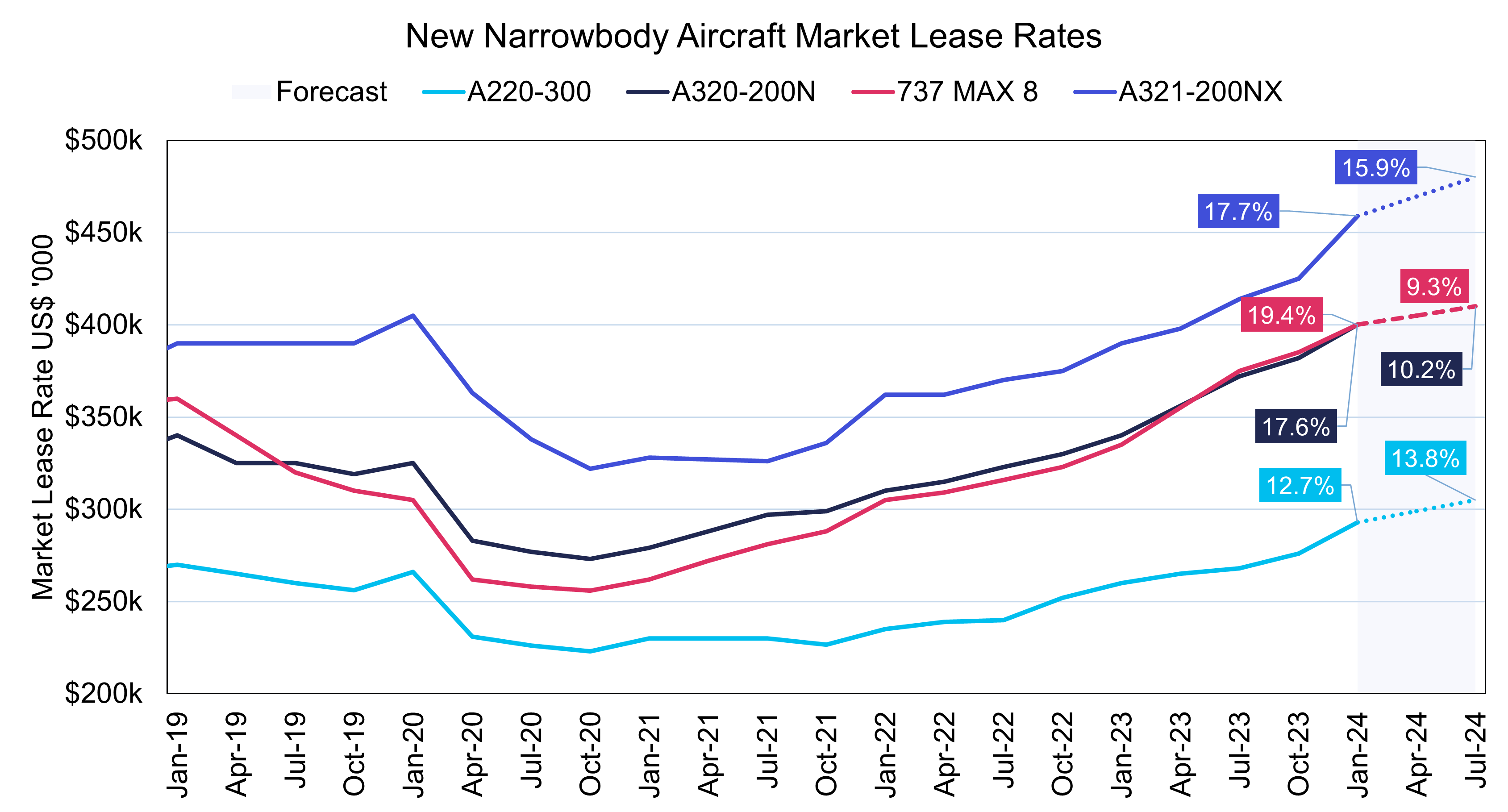

Narrowbody Aircraft Lease Rates (IBA Research)

Air Lease's current results have been good, but most of the benefit from these stronger lease rates are still due to show up. There is a lag of about two years from lease signing to when the aircraft is placed into service. This lag was discussed on both Air Lease's last conference call as well as on competitor AerCap's (AER) last conference call. If you're considering an investment here, I strongly recommend reading the last few conference calls from both companies.

One particular quote, from Air Lease Executive Chairman Steven Hazy, noted the following:

And just by way of example, one of the aircraft that was in this category was an A321 and the new lease that we signed with another airline as a follow-on, is paying us a higher rental rate than the original lease and the other aircraft being a 737-800, we had the same phenomenon with a new lease, had higher lease rates than at least that just expired.

Think about this for a minute. Imagine leasing a brand new car for seven years. After those seven years pass, you re-lease the same car and your payment is higher than your original lease. That's how strong this market is.

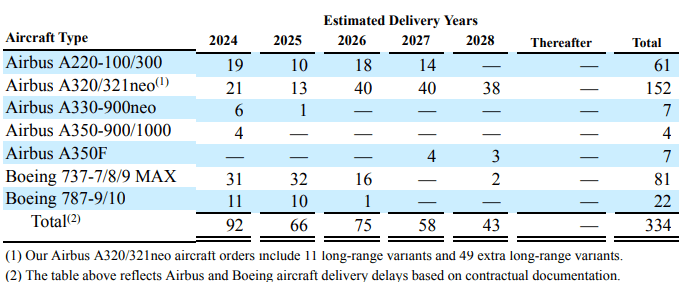

3. A strong order book filled with in-demand aircraft

The majority of Air Lease's order book is narrow-body aircraft, which is seeing the highest demand right now.

Air Lease Order Book (Air Lease 2023 10-K)

4. Medium term interest rates declining

In the next few years, especially this year, Air Lease has a lot of aircraft to pay for. It will pay for these through a mix of Operating Cash Flow ($1.75 Billion in FY23), planned Aircraft sales ($1.5 billion planned for FY24) and new debt. They recently issued $500 million of 2029 notes at 5.1% and C$400M of notes due 2028 at 5.4%. Lower interest rates are a benefit when they roll over debt.

From Air Lease's 2023 10-K, they describe their business as "In order to maximize residual values and minimize the risk of obsolescence, our strategy is to own an aircraft during the first third of its expected 25-year useful life."

Generally, Air Lease owns very new aircraft, and sells them when they're around ~8 years old. They depreciate their aircraft on a straight line over 25 years, with a 15% terminal value, similar to AerCap.

Air Lease has $30.4 billion in assets. $26.2 billion of those are aircraft. We already know from the above that used aircraft are holding their values incredibly well right now, so the below depreciation is almost certainly overstated.

Air Lease Flight Equipment (Balance Sheet in 2023 10-K)

There's evidence of this. In FY23, Air Lease recognized $156 million in gains from the sale of 27 aircraft with sales proceeds of $1.5 billion, representing a gain of approximately 11%. AerCap has been similarly selling assets for 15-20% gains.

I expect these gains to increase in 2024 and beyond. If Air Lease can continue to sell aircraft for 10% above book value, it represents another $2.6 Billion in value, which is over half of Air Lease's $4.8 Billion market cap!

Against the $30.4 billion in assets, it has $23.3 billion in liabilities, $19.2 billion of which is debt.

It also has two other "assets" that have real-world value, but not accounting value (yet.)

So ignoring all of the following:

The market is currently valuing Air Lease at $44, a fraction of its (understated) Tangible Book Value of ~$65.

I have a few theories as to why Air Lease is trading so far under liquidation value.

The first is just a perceived lack of catalysts. It has traded under tangible book for all of post COVID. This probably made sense in 2020 and 2021 when travel was all but shut down and faced an uncertain future. It makes very little sense now; in fact, Air Lease is "cheaper" now than it was in 2021!

Shares traded near current levels in 2017/2018 while the broader market has almost doubled. There is real selling pressure from frustrated shareholders that are sick of seeing the "dead money" company in their portfolio and indiscriminately sell without regard to valuation.

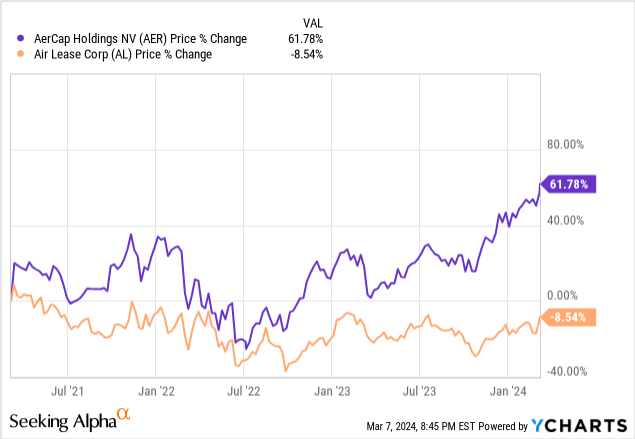

The second reason is that there is a similar company in the market that is outperforming. There's a lot to love with AerCap and its CEO (I also own it.) Their Book Value is also likely materially understated, and they've been selling assets for above book and using the proceeds to repurchase shares below book value, which is proving to be a winning formula.

That said, at this point, the difference in valuation is becoming extreme. Air Lease's order book is extremely valuable (particularly since 213 of the 334 aircraft on order are of the Airbus A220/A320/A321's) and it is trading at a very steep discount.

I think there are a couple catalysts that will move shares far higher by the end of 2025.

One catalyst is happening next Friday and responsible for the small run up in price this past week (although it's just getting back to levels where it traded earlier in 2024.) Air Lease is being added to the S&P600. Estimates are showing that $413 million, or 10.37M shares, need to be purchased, which would represent almost 8.6% of all outstanding shares. This is a big number and could help push shares higher.

The other major catalyst is share repurchases. Air Lease has stated it considers the 2.5 debt-equity ratio sacrosanct, as it is a large component of keeping its investment grade credit rating. With $6.8 billion in new aircraft set to be delivered in 2024, the goal of reaching a debt to equity of 2.5x times will be difficult, but I expect them to reach this level sometime in 2025.

Share repurchases at such a large discount to book value are enormously accretive. There was a question about this on the Q3 Conference Call

Hillary Cacanando

Hi, thanks for taking my questions. So with $1.8 billion in your sales pipeline and attractive stock valuation, I was wondering how you were thinking about share buybacks and if that's something you will consider in the near to medium term?

John Plueger

Sure. Look, capital allocation including share buybacks is always a really big consideration for us. Keep in mind that we are still trying to lower our debt-equity ratio to the target of 2.5 to 1, that's important for our investment grade ratings, and that we have always said is sacrosanct. So given all those elements, we are prioritizing, reducing our debt-equity ratio down to our guidance level first.

They are at ~2.61 to 1 currently. Had they not had to write off the Russian fleet, they would be at 2.41 to 1. They have repurchased shares recently, $159 million in the first half of 2022, before stopping because of the lost Russian aircraft.

They should reach the 2.5 to 1 level sometime in 2025 when the order book steps down significantly ($6.8 billion/92 deliveries in 2024 steps down to $4.4 billion/66 aircraft in 2025.) Additional Russian recoveries and (ironically) delivery delays could have this happen sooner.

I expect the shares to jump 10% when it is announced.

The aircraft leasing business model has survived a number of shocks in the past 25 years: 9/11, the global financial crisis, COVID, and the Russian invasion of Ukraine. COVID in particular was a huge black swan for the airline industry, and Air Lease survived it well. But this is certainly a business that is exposed to geopolitical instability and shocks.

Air Lease is leveraged and requires access to capital markets to refinance debt, which always carries some degree of risk, although I believe they are managing this risk well.

I believe the largest risk to Air Lease would be China invading Taiwan. Air Lease's exposure to China is 7% and has been decreasing, and I doubt China would confiscate civilian aircraft the same way Russia has. If this did occur, it would not have a positive impact on air travel, or Air Lease's share price!

Air Lease's current market cap is $4.8 billion, compared to a tangible book value $7.1 billion. But if we believe that the true value of the assets are understated by 10%, a level slightly under recent sales, then the real book value is $9.7 billion, and Air Lease is trading at half of its worth.

I believe the market will start to appreciate this over the next year as earnings increase and book value continues to build. It's worth noting that 100% of Air Lease's orderbook for 2024 and 2025 has leases signed.

With continued earnings, aircraft sales above book value, and some share repurchases, Air Lease could easily reach $80 by 2026, which would represent it trading near stated book value - where it traded most of pre-COVID, and near where AerCap trades today.