imaginima

imaginima

American Electric Power (NASDAQ:AEP) is one of the largest electric utilities in the United States.

Only smaller than a handful of competitors, including NextEra Energy (NEE), Southern Co (SO), Duke (DUK), and Constellation Energy (CEG), the company is an agglomeration of generation, transmission, and distribution subsidiaries that serve electricity to a portion of the eastern seaboard, as well as the midwestern United States.

Given the company's size and financials, one might expect that AEP trades at a premium to the general market and competitors.

However, as a result of interest rate hikes (which appear to be sticking around in the medium term), as well as generally negative sentiment on the Utility Sector (XLU) due to yield un-competitiveness vs. fixed income, AEP has, in our view, become critically underpriced by the market.

With a stable underlying business and a strong outlook, AEP appears to be well positioned to continue providing value to shareholders into the distant future.

Plus, with a multiple that appears historically attractive, we think now might be the right time to begin accumulating shares in this company.

Today, we're taking a closer look at AEP's prospects and valuation to determine whether or not this 4.25%-yielding critical infrastructure stock belongs in your portfolio.

Sound good?

Let's jump in.

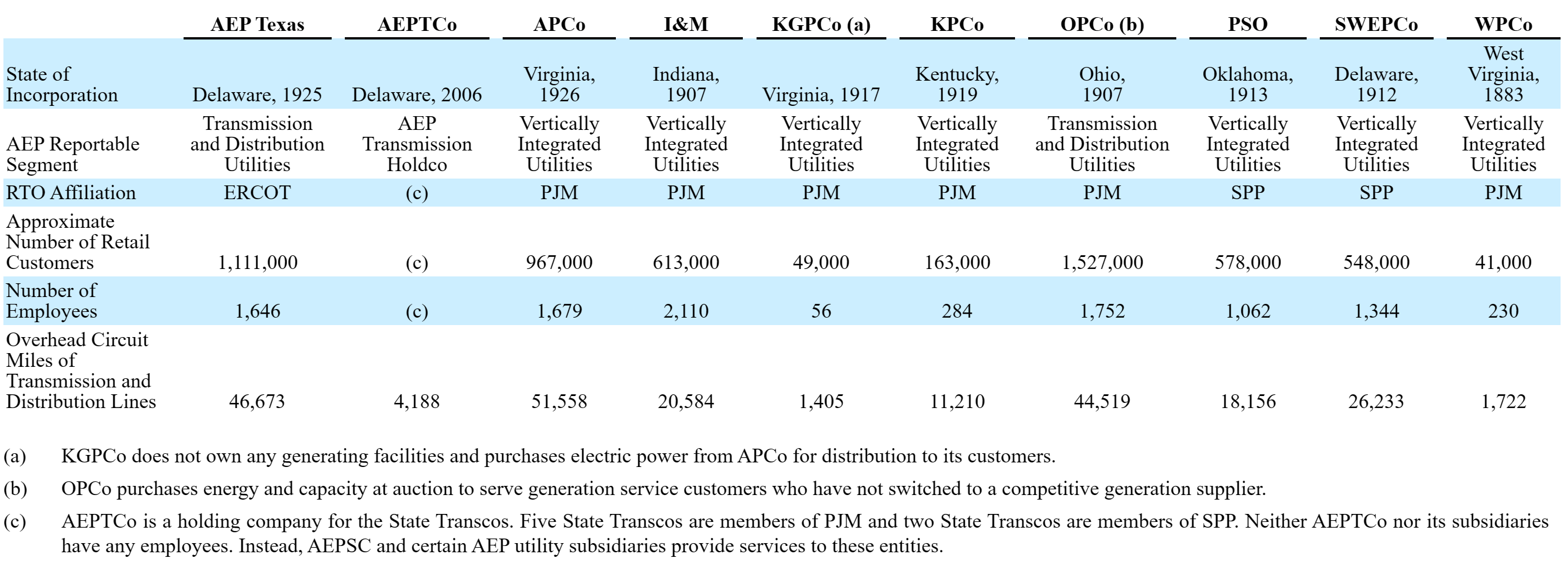

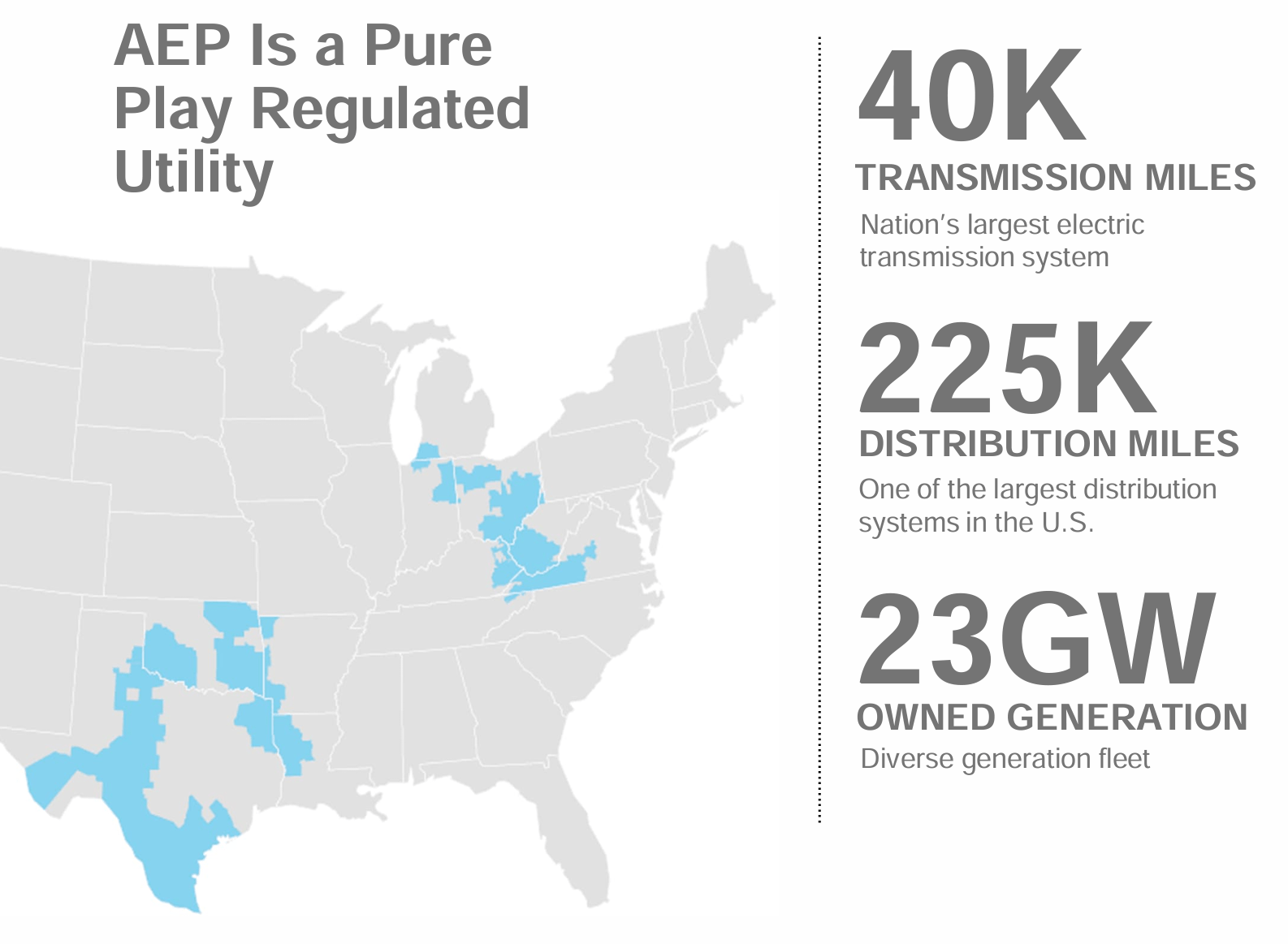

At first glance, AEP appears to be a highly complex company, but it's really just a holding company for a number of subsidiaries that all provide power generation, transmission, or distribution services to a number of different markets in the eastern United States.

This table gives a nice overview of the company:

10-K

As you can see, some of these related companies actually conduct business with one another, and many are members of either the PJM or SPP regional transmission organizations that operate throughout Arkansas, Indiana, Kentucky, Louisiana, Michigan, Ohio, Oklahoma, Tennessee, Texas, Virginia and West Virginia:

Earnings Presentation

RTO's, in case you are unaware, are regional organizations that coordinate, control, and monitor multi-state electric grids:

The transfer of electricity between states is considered interstate commerce, and electric grids spanning multiple states are therefore regulated by the Federal Energy Regulatory Commission (FERC).

In any case, the company has done a good job at turning these power generation and distribution networks into cold hard profits for investors.

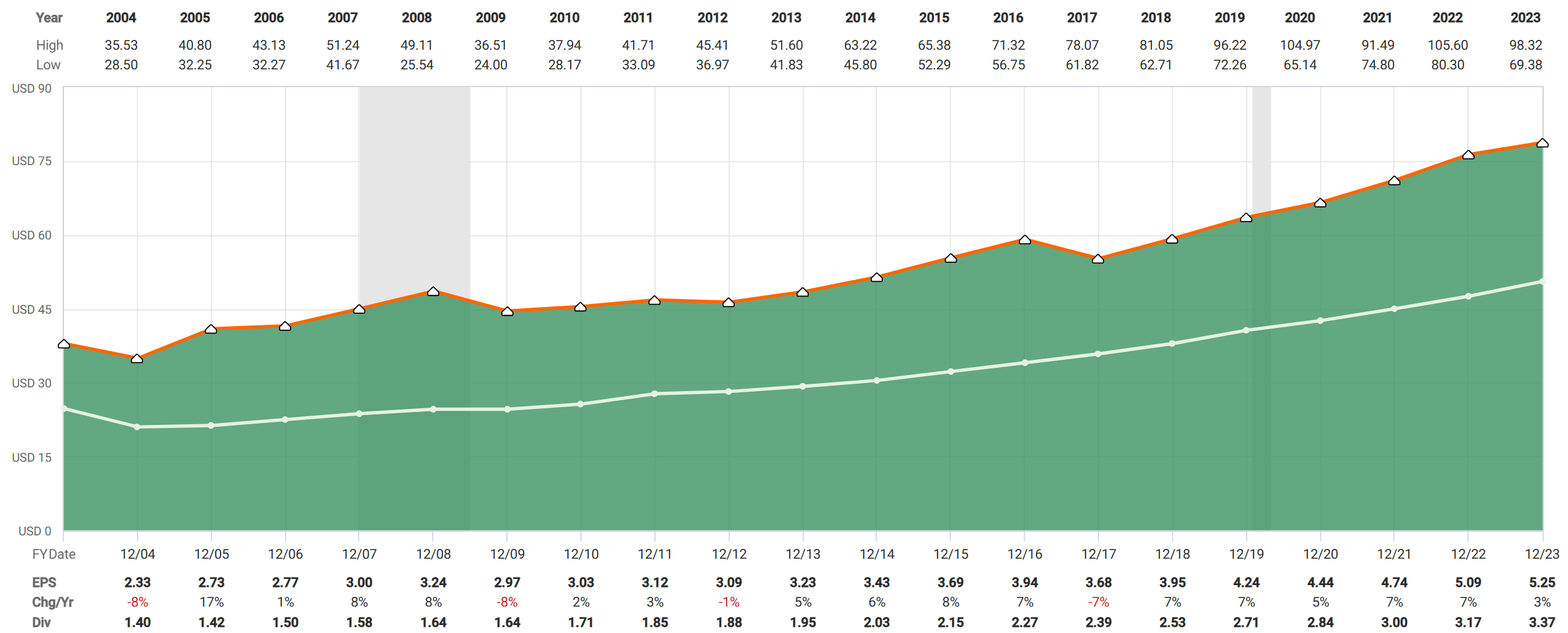

In FY23, AEP announced AOEPS of $5.25, which was the latest profitable year among a streak of profitable years that has continued since at least 2004:

FAST Graphs

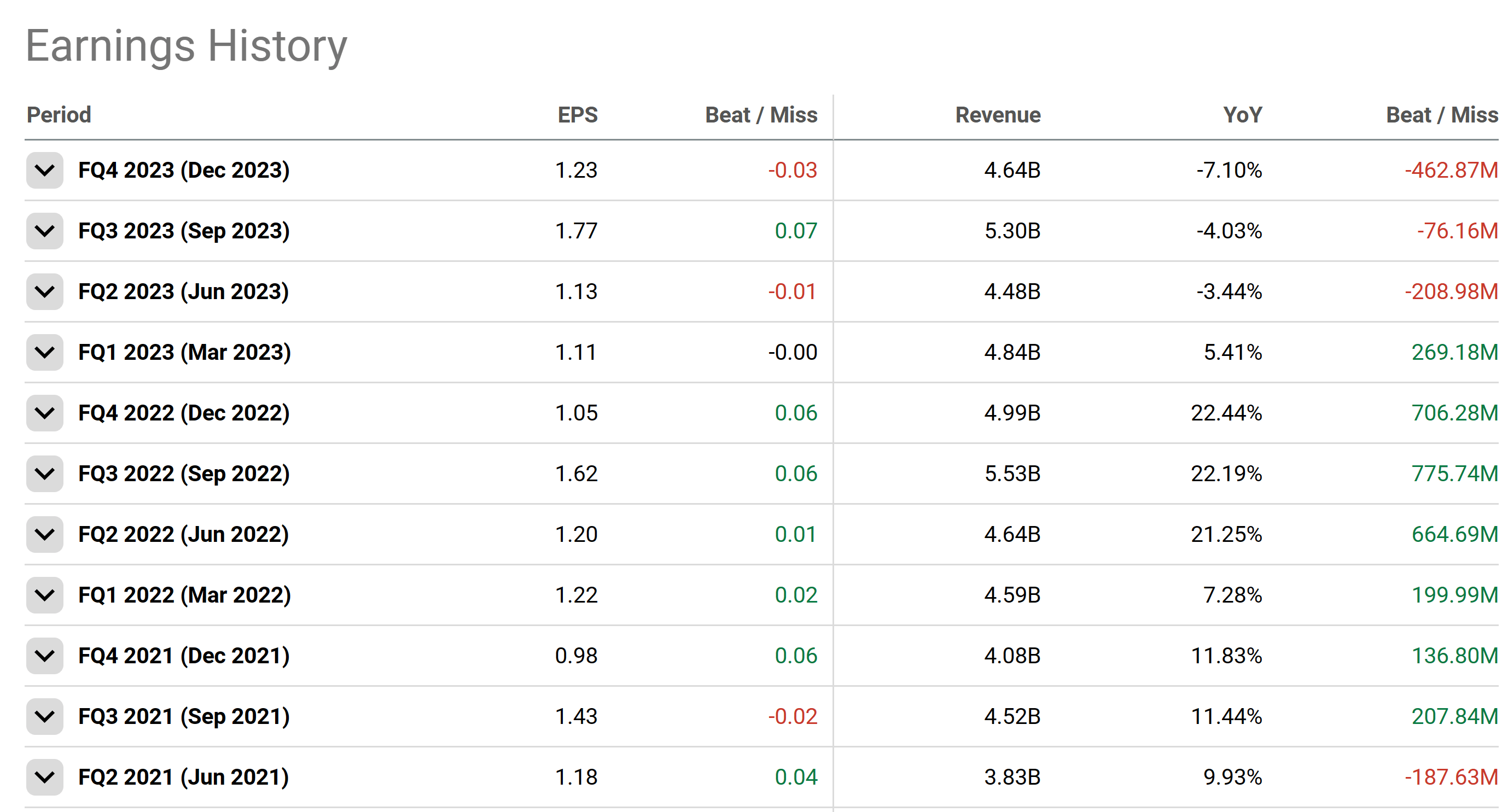

That said, zooming into recent quarters shows that there have been some hiccups along the way.

In Q1, Q2, and Q4 of this last fiscal year, AEP's performance was sub-par, with EPS coming in line or well under analyst expectations:

Seeking Alpha

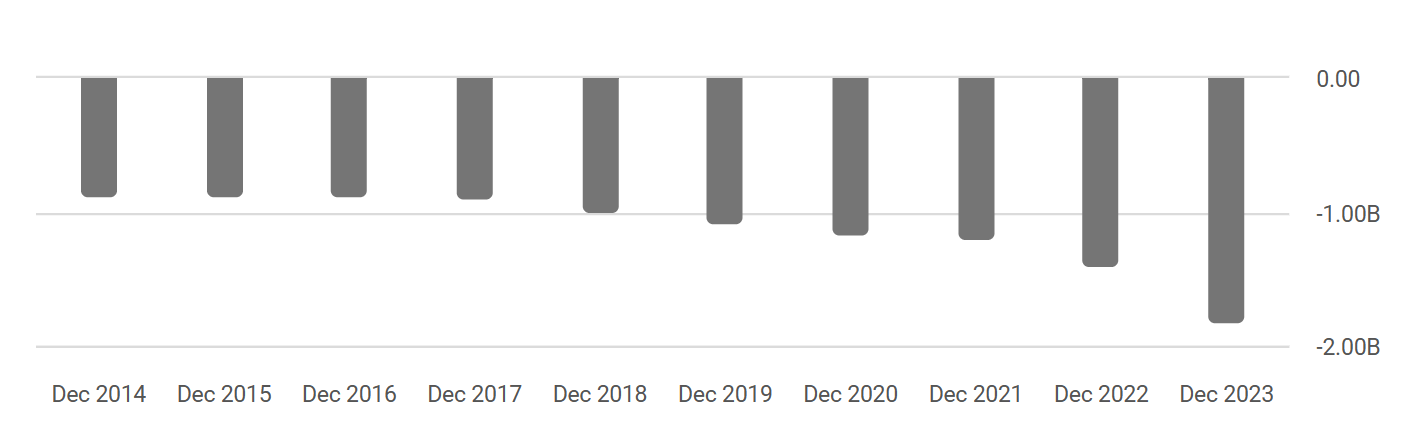

While concerning, this has largely been a result of increases in interest expense, which has been on the rise over recent years:

Seeking Alpha

Top line sales and operating results have been largely stable or grown slightly, both nominally and on a percentage basis, but increases in AEP's interest costs have hurt the bottom line, growing from an $800 million annual outlay in 2014 to $1.8 billion in 2023.

While some of this has come from increased Capex and spend, a moderate chunk has also come from higher interest rates as a result of the current interest rate environment.

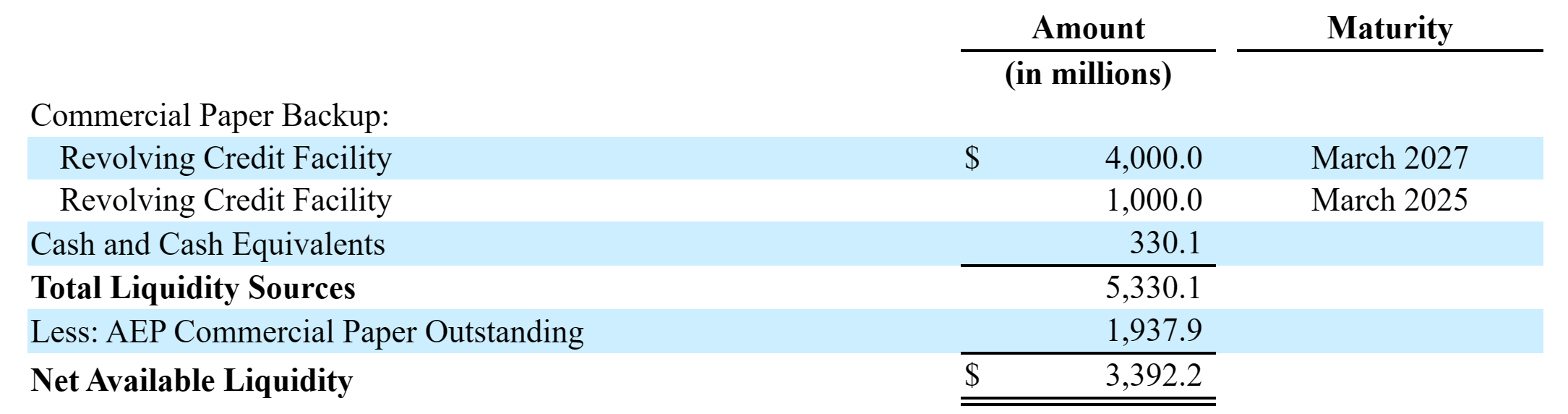

In addition to the debt, AEP's revolving credit facilities are due to mature soon, which could tack on even higher credit costs to the interest expense line item:

10-K

However, while the interest is a potential concern, Management is aware of this and has been taking steps to raise cash and deleverage.

This includes asset sales of the NMRD project, as well as AEP's retail and distributed resources businesses.

Together, these represent continued optimization of AEP's balance sheet by management, which is a good sign.

Additionally, from a coverage perspective, FFO is currently 13% of AEP's total debt, which shows that while interest is hurting EPS, there's no liquidity or existential threat presented by the increase in borrowing costs.

As rates come back down over the next few years, as is what the Fed dot-plot suggests, we expect that improving interest delta should provide a tailwind to EPS in the stock, not a headwind.

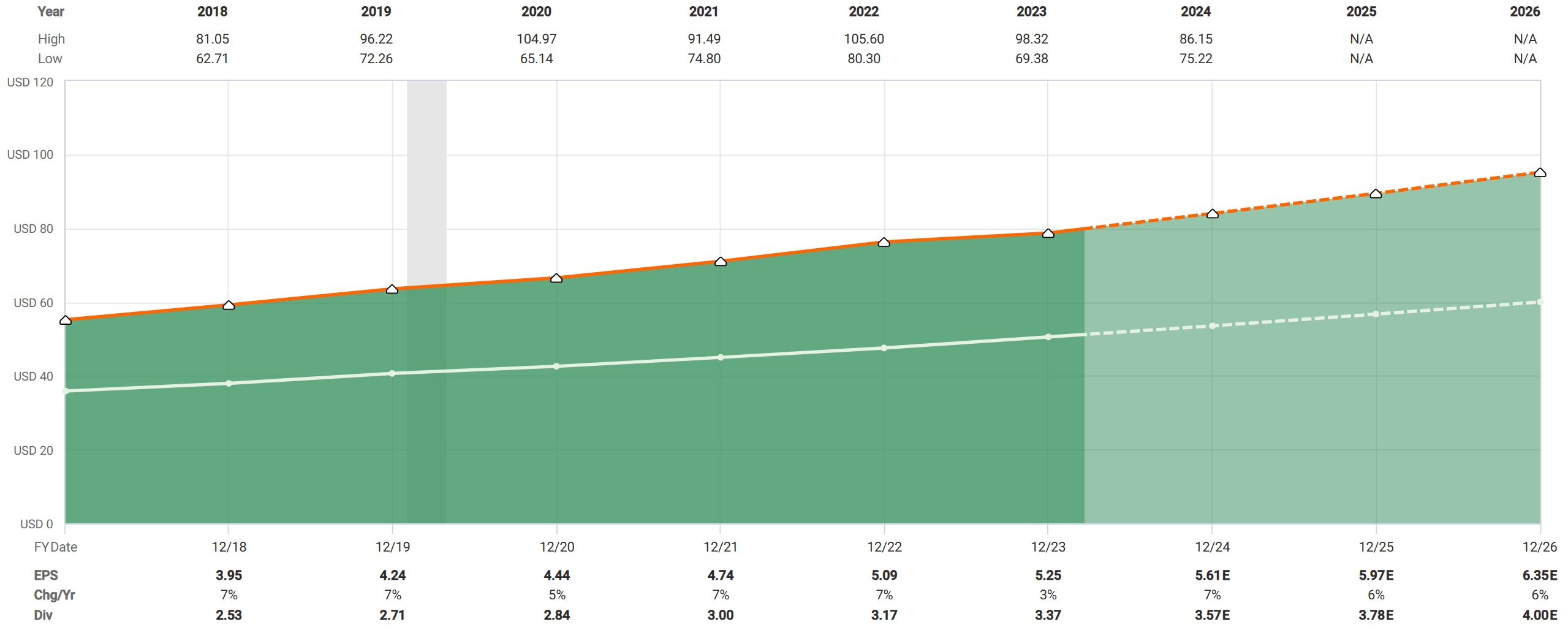

This is what analysts believe as well, given the position EPS outlook when examining future projections for the company:

FAST Graphs

All in all, we believe that AEP is well positioned to re-accelerate EPS growth as a result of asset base earnings power and continued capital stack optimization.

Rates have also had an impact on AEP's multiple.

Prior to the recent rate hikes, AEP traded at a P/E of around 20x.

However, since rates have increased, the multiple has come in line closer to 15x. This 25% reduction in AEP's valuation has hurt the stock price, but this has been a common occurrence across the Utility industry, due to the fact that most utility businesses are inherently asset-heavy.

As rates come down over time, we expect that AEP's valuation will rise to come back in line with where it has been historically.

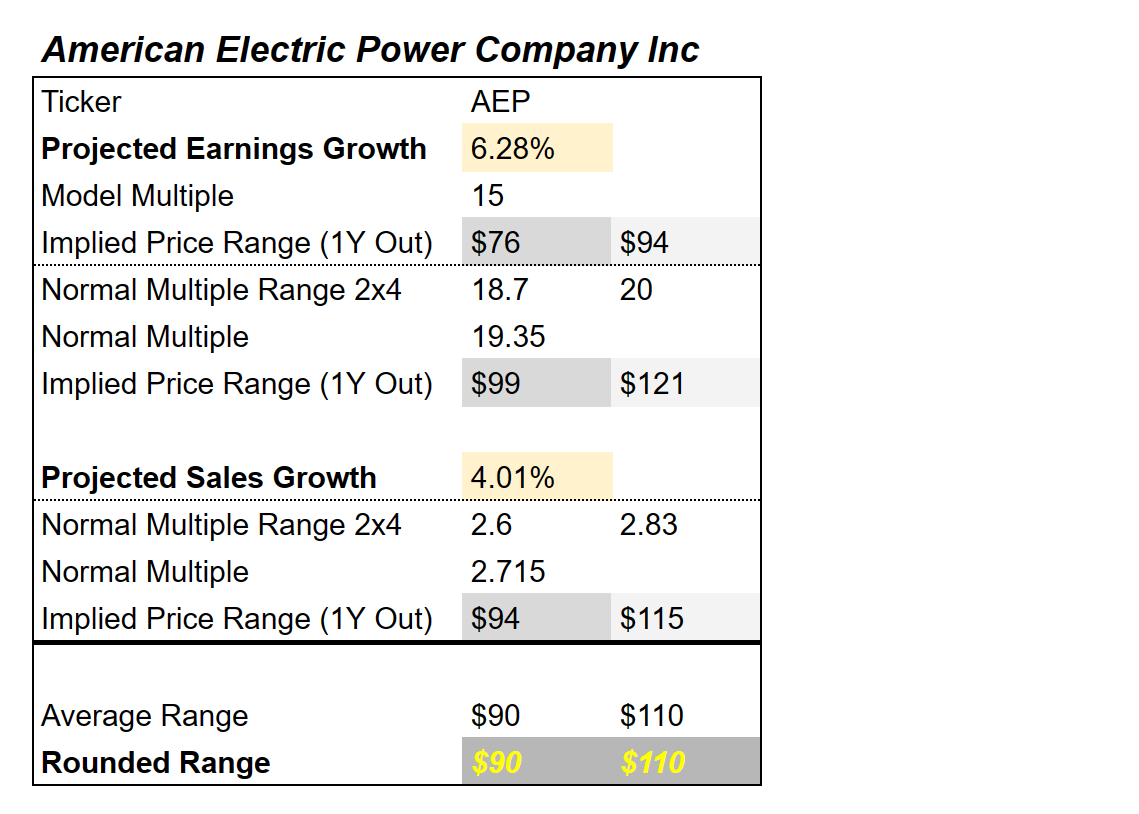

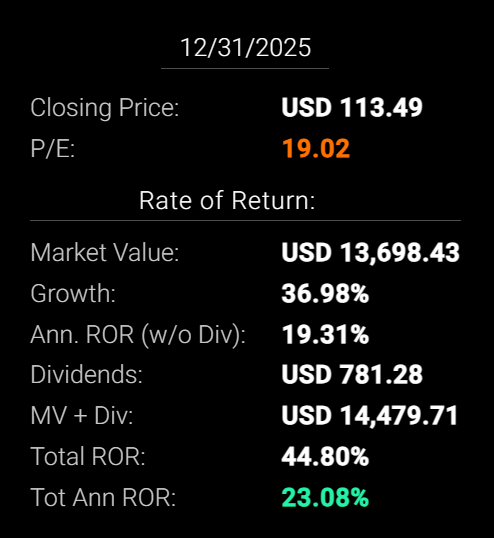

Combined with potential incremental improvements in EPS that we just laid out, and it would appear as though AEP could see serious upside back to our estimates of the stock's Fair Value zone, which is somewhere between $90 and $110 per share:

www.propnotes.co

This model incorporates a blended average of AEP's historical top and bottom line multiples over the last few years, along with a 'model' range based on the company's expected AOEPS growth rate of 6.3% over the next few years, which reveals a potential multiple of 15x.

Together, and based on this model, it would appear as though AEP is potentially undervalued, by 10% or more, given AEP's closing price yesterday of ~$83/share.

Thus, at this price, it would appear as though investors can potentially earn both AEP's future EPS growth, as well as some multiple expansion on top of that, which adds up to a potentially handsome return by the end of 2025:

FAST Graphs

This ~23% annualized return over the next two years is our base case for the stock.

That said, there are some risks for AEP investors that are worth thinking about before entering a position.

First off, AEP is a highly regulated utility company, which comes with a number of natural barriers to profit growth. This includes margin caps on rates and regulatory burdens that could kneecap profit.

Right now, AEP is involved in significant ongoing litigation with regulators over adverse price decisions, which shows how much of an impact this risk has on the business.

However, zooming out, we see this as the price that needs to be paid for limited competition in each regional market.

Secondly, AEP could continue to suffer on interest payments if borrowing costs remain high.

If inflation remains higher for longer, then it could adversely impact AEP's business due to the Federal Reserve's need to keep rates high.

Finally, AEP has a huge amount of physical infrastructure that it operates to power returns. As a result, there are a number of environmental risks associated with AEP that could occur as a result of adverse weather or environmental disasters that may strike.

None of the regions that AEP operates in are particularly high risk when it comes to environmental concerns, but it's worth considering.

All of that said, we believe that AEP is well positioned to deliver returns to investors through both organic EPS growth, as well as potential multiple expansion over time that could come as a result of lower interest rates.

There are risks with AEP, but with a well-covered 4.3% dividend, excellent FFO coverage on debt and capital returns, and management's continued optimization of AEP's balance sheet, we think that the future is bright for investors considering AEP as this juncture.

As a result, we rate AEP a 'Buy'.

Cheers!