Juan Jose Napuri

Juan Jose Napuri

The Q4 Earnings Season for the Gold Miners Index (GDX) is nearly over, and one of the first companies to report its results (fiscal Q2) was Evolution Mining Limited (OTCPK:CAHPF). Unfortunately, the company's production figures came in below my expectations due to weather-related setbacks at Cowal and Mt. Rawdon and another disappointing quarter at Red Lake. This has resulted in production being trimmed yet again at its Red Lake Mine in Ontario, Canada, and has left Evolution Mining tracking well behind its FY2024 guidance.

In this update we'll dig into the fiscal Q2 and H1 2024 results, recent developments, and where the stock's updated buy zone lies:

Evolution Mining Operations - Company Website

All figures are in Australian Dollars (A$) unless otherwise stated with a US$ in front of the dollar figure.

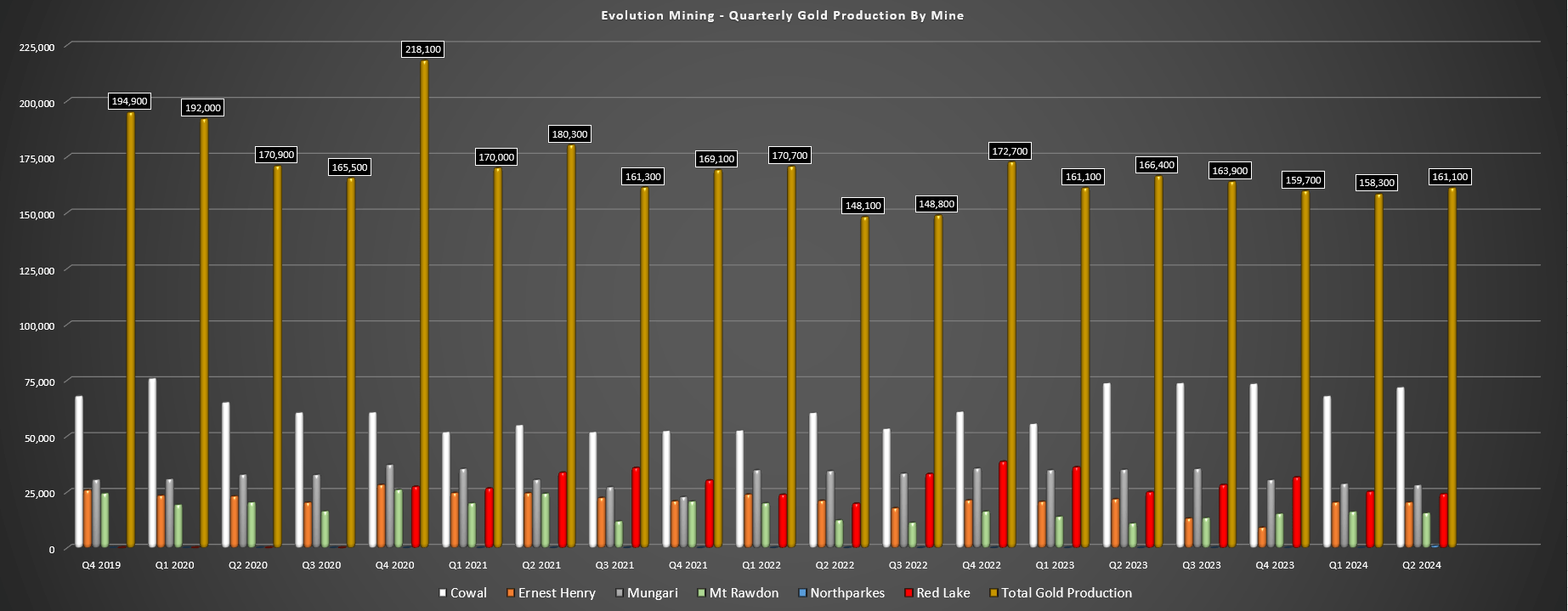

Evolution Mining released its fiscal Q2 results earlier this year, reporting quarterly production of ~161,100 ounces of gold, a 3% decline from the year-ago period. The lower production relative to fiscal Q2 2023 was related to related to another soft quarter at its Red Lake Mine, lower grades at Mungari, and lower grades at Ernest Henry for both gold and copper. This was partially offset by ~1,000 ounces of gold from its newly acquired Northparkes Mine (80% ownership) and a better quarter year-over-year at Mt. Rawdon. Finally, while Cowal had a solid quarter with ~71,800 ounces produced, this was down slightly from fiscal Q2 2023 levels on the back of lower throughput. Let's take a closer look at the results below:

Evolution Mining Quarterly Production by Mine - Company Filings, Author's Chart

Starting with the company's Cowal Mine, quarterly output came in at ~71,800 ounces of gold (down 3% year-over-year), with ~2.15 million tonnes processed at 1.22 grams per tonne of gold vs. ~2.37 million tonnes at 1.14 grams per tonne of gold in the year-ago period. The lower production combined with higher sustaining capital resulted in higher all-in sustaining costs of A$1,226/oz (fiscal Q2 2023: A$1,042/oz), which were still well below the industry average but up sharply year-over-year.

On a positive note, the paste plant has been commissioned, commercial production remains on track for the end of fiscal Q3, and the mine remains on track to produce 320,000 ounces this year, making up ~40% of total production from this key low-cost operation, with underground mining rates set to double to ~1.4 million tonnes per annum.

Ernest Henry Operations - Google Earth

Moving to Ernest Henry, it was a solid quarter for the asset, with production of ~20,400 ounces of gold and ~12,800 tonnes of copper despite these figures being lower year-over-year (~21,800 ounces of gold and ~15,500 tonnes of copper). The lower production was related to lower grades of 0.49 grams per tonne of gold and 0.85% copper and flat throughput, partially offset by much higher gold recoveries of 82.2% (+500 basis points year-over-year) with the benefit of projects focused on lifting concentrator recoveries. That said, while this was a decent quarter for the asset, we did see a significant decline in all-in sustaining cost [AISC] margins, with margins impacted by lower copper by-product credits from the lower copper production and lower average realized copper price. The good news is that the copper price has ticked materially higher in fiscal H2 2024 and will be a nice tailwind for the fiscal Q3 and fiscal Q4 results.

Ernest Henry's all-in sustaining costs in fiscal Q2 were [-] A$1,470/oz vs. [-] A$3,748/oz in the year-ago period.

Red Lake Operations - Company Website

Unfortunately, the decent performance at its two lowest-cost assets (Ernest Henry and Cowal) was overshadowed by a weaker quarter at Red Lake. In fact, production came in at just ~24,100 ounces at AISC of A$3,343/oz [US$2,173/oz], a much worse result relative to ~25,000 ounces at A$2,761/oz in the year-ago period despite lower sustaining capital spend. The lower production in fiscal Q2 2024 was related to lower grades (4.02 grams per tonne of gold vs. 4.40 grams per tonne of gold), with the company noting that quarterly output was impacted by materials handling constraints at Cochenour and the Reid haulage shaft (since resolved), and seismicity at the Balmer Mine. On a positive note, a new permanent raisebore ore pass at Cochenour is in place and development was up year-over-year to ~3,900 meters vs. ~3,500 meters in the year-ago period.

The only saving grace for the quarter was the higher gold price (A$3,290/oz vs. A$2,592/oz) which nearly offset the higher costs, but the updated guidance of 125,000 to 135,000 ounces was certainly not pleasing for the market, especially relative to previous FY2024 guidance of 200,000 ounces at sub A$1,900/oz AISC. That said, Evolution did share that the material handling constraints and impeded access due to seismicity at Balmer led to a ~13,000 ounce impact to production, so we'll have to see the mine can get back on track next year and deliver above the elusive 160,000 ounce per annum mark.

Overall, Evolution has found itself sitting at just ~40% of its FY2024 production guidance of 789,000 ounces, though it did see an impact from elevated rainfall at Cowal and Mt Rawdown which was a 10,000 ounce impact. So, when combined with the shortfall at Red Lake, the company should be sitting closer to ~342,000 ounces in H1 2024 (~43%) of back-end weighted annual guidance vs. the ~319,300 ounces it sits at today. That said, while this is undoubtedly a disappointing start, the gold price has made it much less painful, especially if the metal can hold onto most of its recent gains. In fact, all-in cost margins improved to A$676/oz vs. A$466/oz in fiscal Q2 2023, a more respectable figure given the challenges in the period.

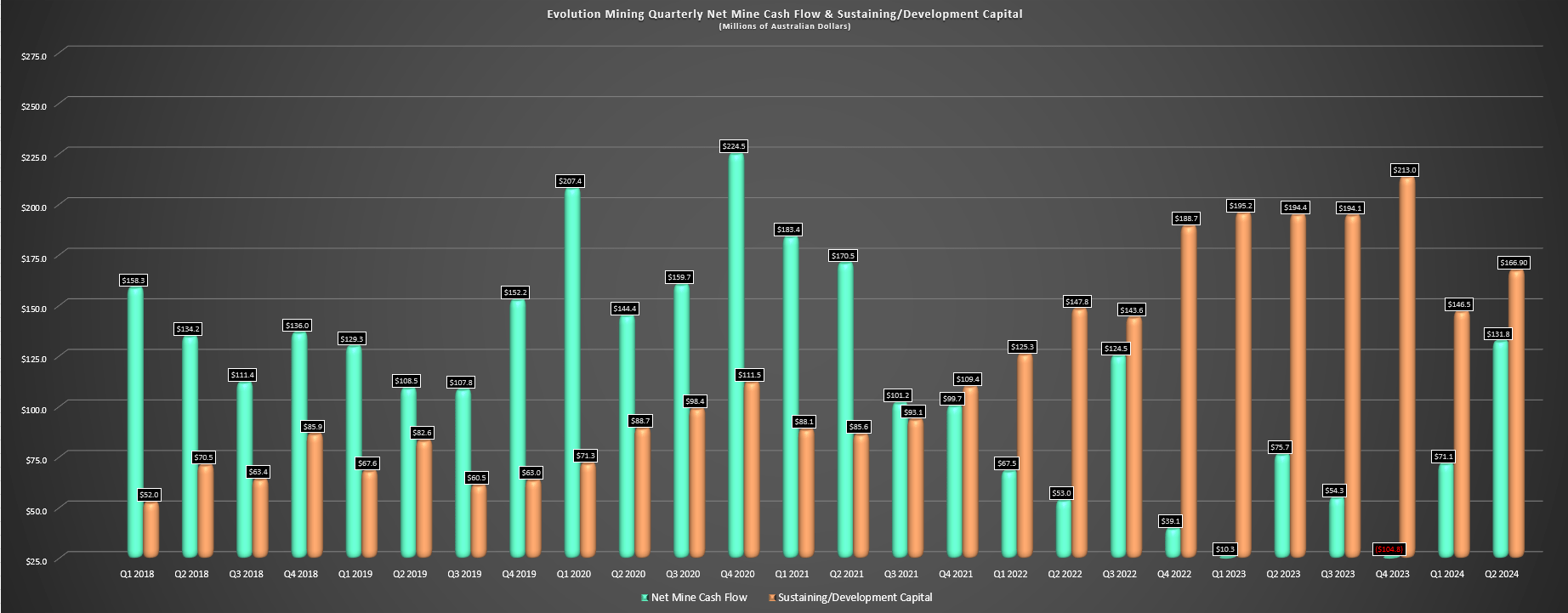

Evolution Mining Quarterly Net Mine Cash Flow & Sustaining/Development Capital - Company Filings, Author's Chart

Digging into the financial results a little closer, Evolution sold ~169,500 ounces at A$3,089/oz [US$2,008/oz], a higher average realized price vs. the A$2,551/oz price [US$1,676/oz] in the year-ago period. The benefit of a higher gold price, lower capex and the lower group tax expense post-Northparkes deal resulted in a ~237% increase in net mine cash flow to A$131.8 million, up from A$39.1 million in the year-ago period, and Evolution ended the quarter with A$191 million in cash and A$716 million in liquidity with its undrawn A$525 million credit facility. This is a significant step in the right direction as is the improved debt maturity profile (no debt repayment commitments until fiscal Q2 2025), and the company is in a much better position than it was 18 months ago in September 2022 at its lows, when it was highly leveraged and working with a much weaker gold price that made things look much more fragile if the gold price couldn't get up off the mat (which it since has - in fact, it's sitting at all-time highs).

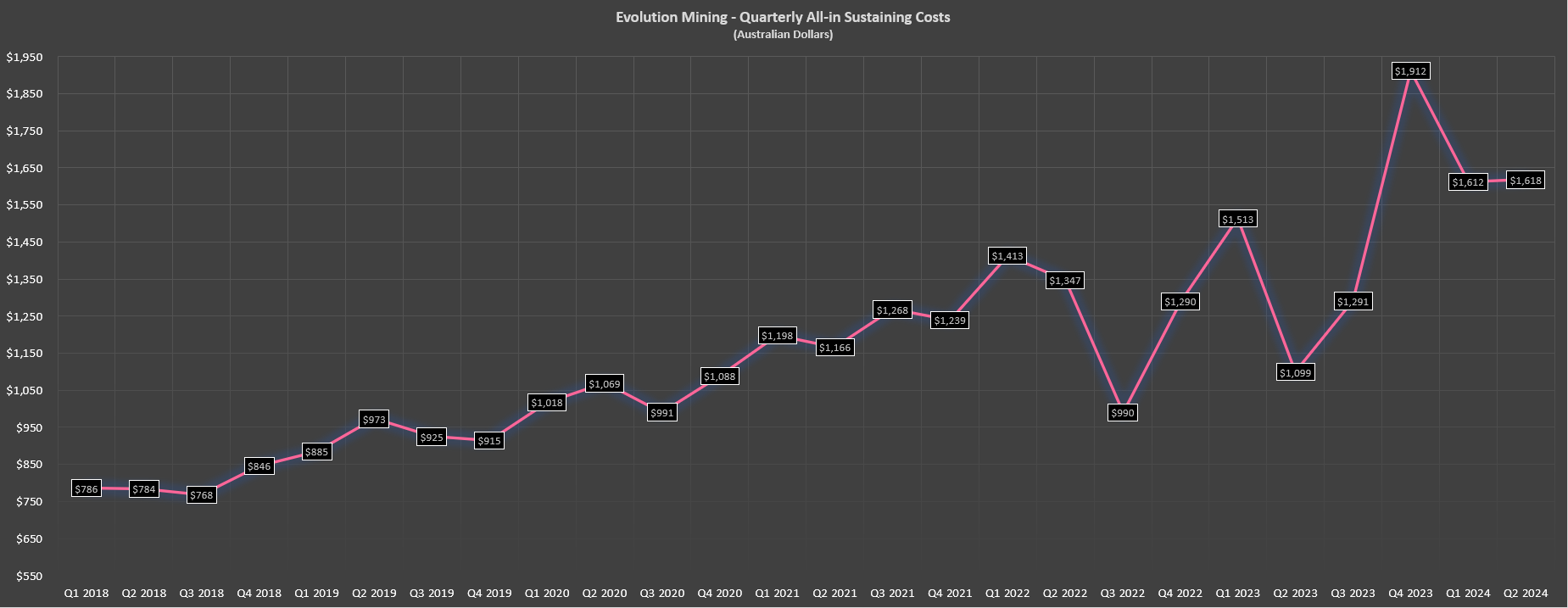

Moving over to costs and margins, Evolution reported all-in sustaining costs of A$1,618/oz in fiscal Q2 2024 (US$1,052/oz), up significantly from A$1,099/oz [US$722/oz] in the year-ago period. This was related to the lower by-product credits at Ernest Henry that didn't do as significant of a job at dragging down costs, much higher costs at Red Lake (despite easy comps with higher dilution and absenteeism last year), higher costs at Cowal, and limited contribution from Northparkes which also has negative AISC when factoring in by-product credits.

Finally, Mungari also saw higher AISC year-over-year (A$2,558/oz vs. A$2,178/oz) due to the lower denominator, but we will see significantly improved costs once the Mungari 4.2 Project is complete. And while this significant increase in AISC was disappointing, this was a kitchen sink quarter with fewer ounces than planned and AISC margins still held up pretty well at A$1,471/oz vs. A$1,452/oz in the year-ago period.

Evolution Mining All-in Sustaining Costs (A$) - Company Filings, Author's Chart

Some investors will argue that Evolution's costs are skewed due to its significant copper by-product credits, especially with the addition of Northparkes. And while this is a fair point and they are not an apples to apples comparison vs. a low-cost producer like Agnico Eagle (AEM) without the benefit of copper by-product credits, there's no denying that the higher gold price has led to a significant improvement in its financial performance with major capital down materially at Cowal (A$32.4 million vs. A$79.2 million) as the transition to underground mining is nearly complete.

Hence, if gold prices can stay at current levels above A$3,300/oz, we should see a much better H2 from Evolution, with this being a 5%+ improvement from fiscal Q2 2024 levels with the benefit of lower costs in the second half of the year providing a nice boost to margins.

That said, Red Lake will be an asset that will need to be monitored because it's clearly massively underperformed expectations to date and continues to be a drag on Evolution's consolidated performance.

Gold Price Long-Term Chart - StockCharts.com

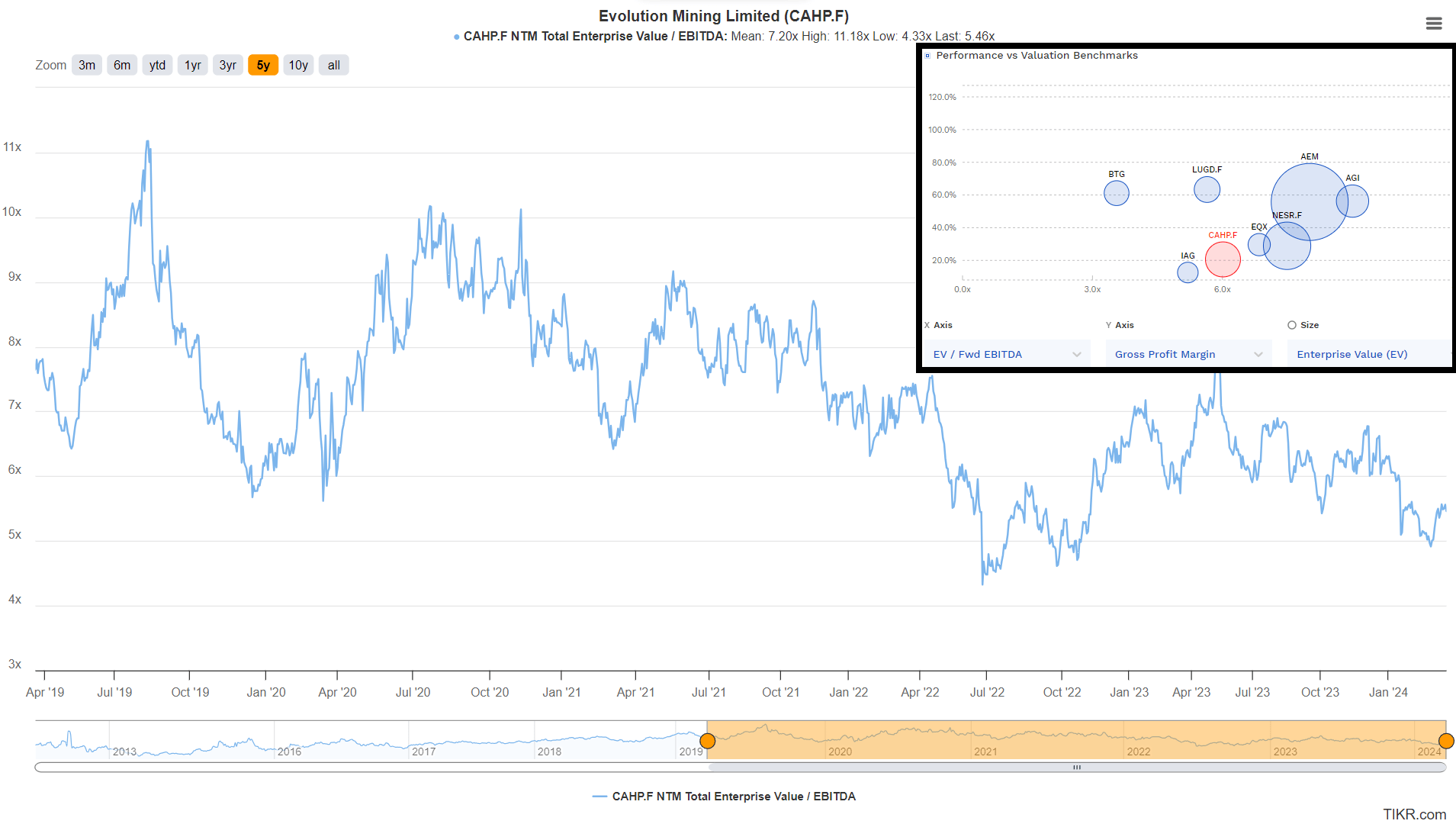

Based on ~1.98 billion shares and a share price of US$2.28, Evolution trades at a market cap of ~$4.5 billion and an enterprise value of ~$5.6 billion. This makes Evolution one of the higher capitalization names producers in sub million-ounce producer space, ahead of other 500,000 to 800,000 ounce producers like Equinox Gold (EQX), Alamos Gold (AGI) and others. However, as stated in past updates, Evolution is unique in that it makes up a small group of large-scale producers with over 95% of production from Tier-1 ranked jurisdictions, with its two peers in this category peers, including Northern Star Resources (OTCPK:NESRF) and Agnico Eagle Mines.

Hence, it's not surprising that the company trades at a premium to its peer group, and while its costs are lower due to by-product credits and it doesn't have the same glowing track record as Agnico Eagle, it is one of the safer ways to get exposure to producers in the gold space, especially with recent headaches in other jurisdictions like Kyrgyzstan and Panama.

Evolution Mining Valuation & Margins vs. Peers + Forward EV/EBITDA Multiple - TIKR, Finbox

Using what I believe to be fair multiples of 1.20x P/NAV and 8.0x forward EV/EBITDA to account and a 65/35 weighting to P/NAV vs. EV/EBITDA, I see an updated fair value for Evolution Mining of US$2.85. This points to a 24% upside from current levels, suggesting that Evolution Mining could make a run at its 2023 highs if it were to trade up towards fair value. However, I prefer to buy those producers that are hated, trading at a deep discount to fair value and already have ultra-low expectations built in and I don't see this as the case anymore, with Evolution like it was over a year ago at US$1.25. So, while I do see Evolution as a decent buy-the-dip candidate among the producer group, I continue to see more attractive bets elsewhere in the sector today.

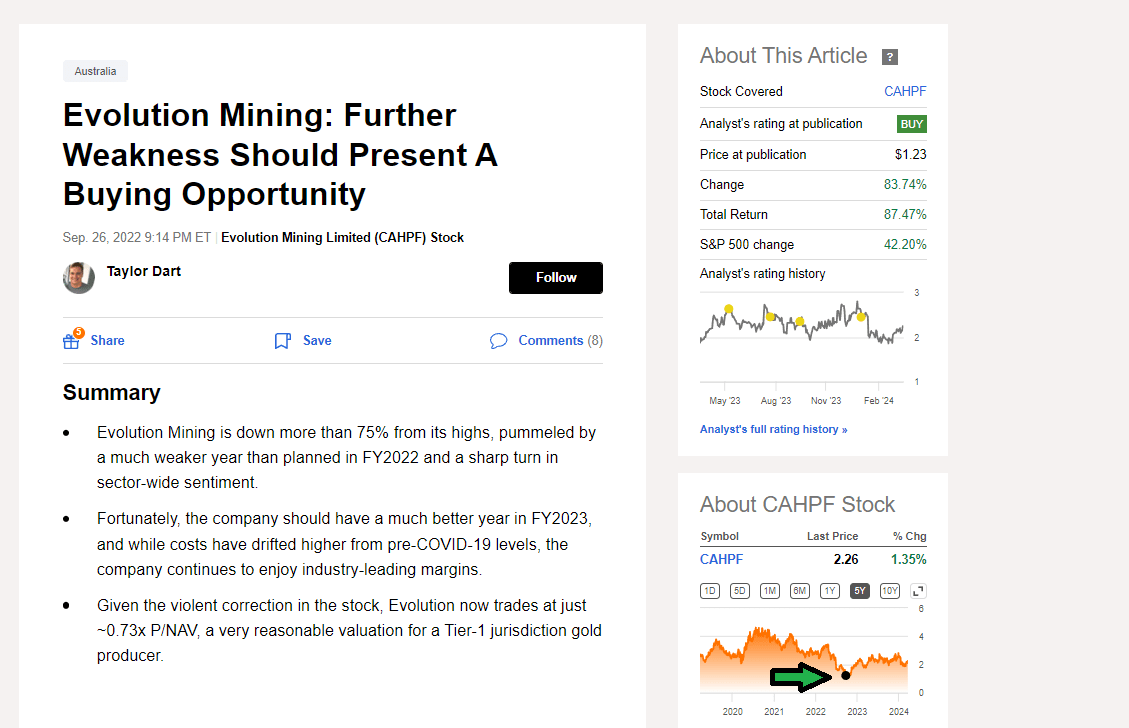

Evolution Mining September 2022 Update - Seeking Alpha Premium/PRO -

Evolution Mining had a tough H1 2024 and is tracking at just ~40% of its FY2024 guidance, with little hope of delivering an 800,000 ounce year which was previously forecast for FY2024 even without Northparkes. This has set the company up to come in below its annual guidance of 789,000 ounces and while production will be much better in H2, this has continued the trend of weaker than planned performance, with FY2023 impacted by flooding at Ernest Henry which was out of its control, but also a disappointing year at Red Lake.

On a positive note, Evolution's weighted average mine life has increased materially with Mungari 4.2, exploration success at Ernest Henry and the addition of Northparkes. In addition, higher metals prices are padding the bottom line and will help Evolution continue to de-leverage. Finally, Cowal is set to ramp up as planned and become one of the lower-cost gold mines globally.

In summary, if I were looking for a gold producer with low jurisdictional risk from a swing-trading standpoint, I would view pullbacks below US$1.95 for Evolution Mining as buying opportunities.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.