adventtr

adventtr

Autodesk’s (NASDAQ:ADSK) business continues to perform relatively well against a varied demand backdrop. It should be noted that the company is benefitting from enormous fiscal stimulus and automotive strength, both of which are unlikely to persist longer term. The last time I wrote about Autodesk, I suggested that 2024 could be difficult. The stock has performed in line with the market since then but my views on the risks facing the company remain unchanged.

Autodesk’s strategy is strengthening its competitive position though, and AI should provide the company with a genuine tailwind. While Autodesk's fundamentals are strong, the stock is expensive, and as a result, it is difficult to see Autodesk outperforming the broader market by a wide margin longer term. In addition, Autodesk’s valuation makes it vulnerable to a large pullback in the event of more serious macro weakness.

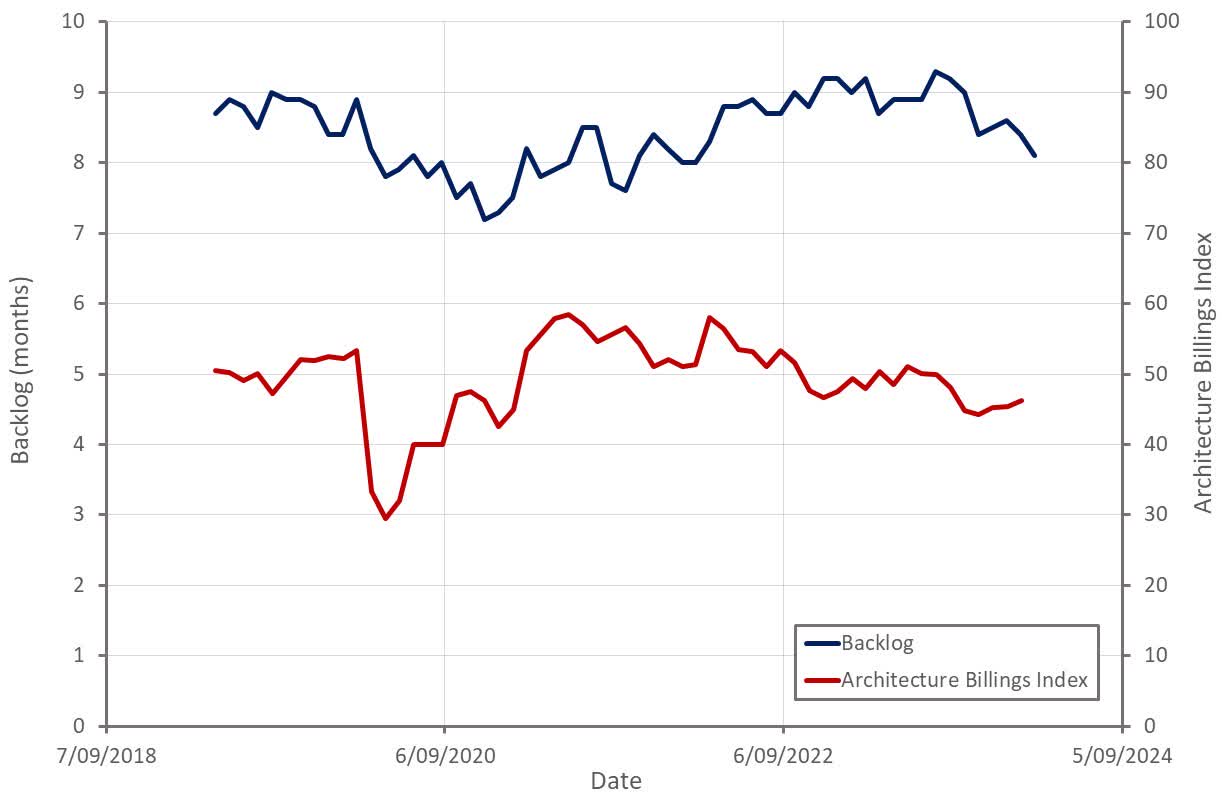

Autodesk's business gives it exposure to a range of end markets and the strength of those markets varies significantly at the moment. Infrastructure and construction have unsurprisingly been an important part of Autodesk's recent growth. Outside of fiscal stimulus, AEC strength is questionable though, with data pointing towards an ongoing slowdown.

Figure 1: Construction Demand Indicators (source: Created by author using data from AIA and ABC)

Manufacturing has been an area of weakness, although data suggests that the demand environment is beginning to stabilize. While conditions have been soft, Autodesk hasn’t seen an impact on its close rates. Autodesk’s renewal rates also remain strong, although new business growth continues to be relatively soft.

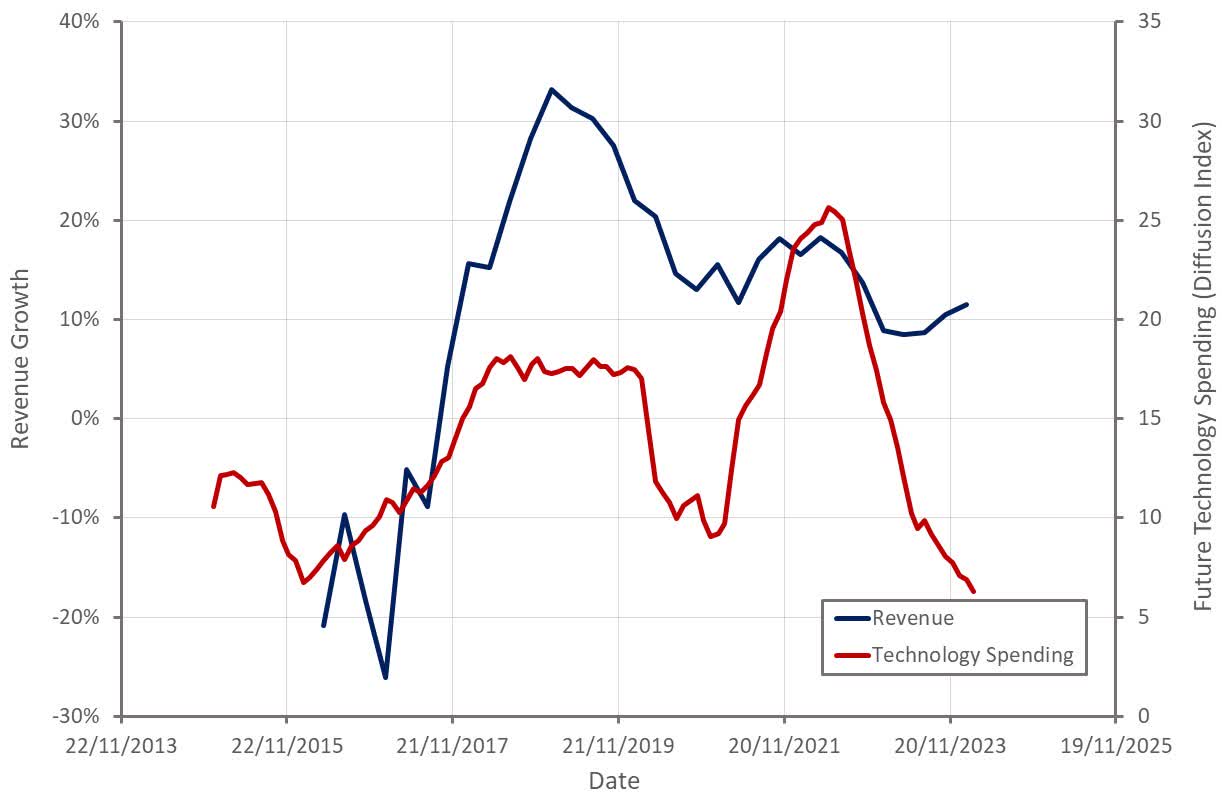

Future technology spending plans continue to soften based on survey data. This has historically been closely related to Autodesk's revenue growth, with the current divergence likely driven by government supported infrastructure spending.

Figure 2: Planned Technology Spending (source: Created by author using data from Autodesk and The Federal Reserve)

Outside of the macro environment, there are a lot of reasons to be optimistic about Autodesk's prospects. AI is a genuine tailwind, with Autodesk developing viable solutions for high value use cases. Autodesk is developing multimodal foundation models to help Design and Make customers automate repetitive tasks and improve designs. For example, converting a 3D model to 2D and generating 3D models from images.

This is not just Autodesk trying to ride the AI hype train either. The company has been working on AI for design and manufacturing for more than 10 years. This includes introducing a consumption model so that AI does not hurt margins. Over the past 4 years, Autodesk has also been taking data out of files and shifting it into a cloud database, which lowers data extraction costs and helps the company realize the value of this data.

AI not only has the potential to expand Autodesk's addressable market, but it could also improve the company's competitive position. Data exhibits economies of scale in machine learning applications, potentially providing Autodesk with a scale-based advantage. Autodesk is also developing lifecycle solutions within and between its industry clouds, which are powered by shared platform services and data. Moving data to the cloud where it can be utilized in more applications and by more users helps to create data gravity.

Make is also becoming an increasingly important part of Autodesk’s strategy. The company believes it now has best-in-class CAM capabilities and plans on expanding its capabilities in areas like factory planning, factory simulation and manufacturing execution systems. This effort is gaining traction in automotive, where Autodesk's footprint is expanding into manufacturing. Fusion is one of the fastest-growing products in the manufacturing industry and ended the quarter with 255,000 subscribers. In support of driving adoption in manufacturing, Autodesk recently acquired FlexSim, a provider of discrete event simulation technology for factories which helps with things like layout and workflow optimization.

Autodesk also recently acquired Payapps, which will enable the company to embed payment and compliance management into the project lifecycle.

Autodesk’s revenue growth was 11% YoY in the fourth quarter, with upfront revenue responsible for 2% of that growth. The Americas was an area of strength, increasing 17% YoY in FY24, while APAC was relatively soft, only increasing 1% YoY.

AEC and manufacturing were areas of strength, while AutoCAD and M&E were relatively soft. AEC and manufacturing both benefited from EBA true-up and upfront revenue though. Water is reportedly an important part of this EBA success.

Figure 3: Autodesk FY24 Revenue Mix (source: Autodesk)

Autodesk is currently guiding to 1,385-1400 million USD in Q1 FY25, representing approximately a 10% increase YoY at the midpoint. For the full financial year, Autodesk is expecting 5,990-6,090 million USD revenue, up 10% YoY. The acquisition of Payapps is expected to provide roughly a 0.5% growth tailwind.

Autodesk is targeting 10-15% revenue growth annually, but this is contingent on the macro environment. Autodesk is also targeting a 50/50 split between growth from volume and pricing. Pricing is an important driver of growth at the moment, with Fusion’s price up significantly over the last 18 months. Fusion is priced low and offers customers significant value though. Pricing is likely to continue increasing as Autodesk adds capabilities to its products.

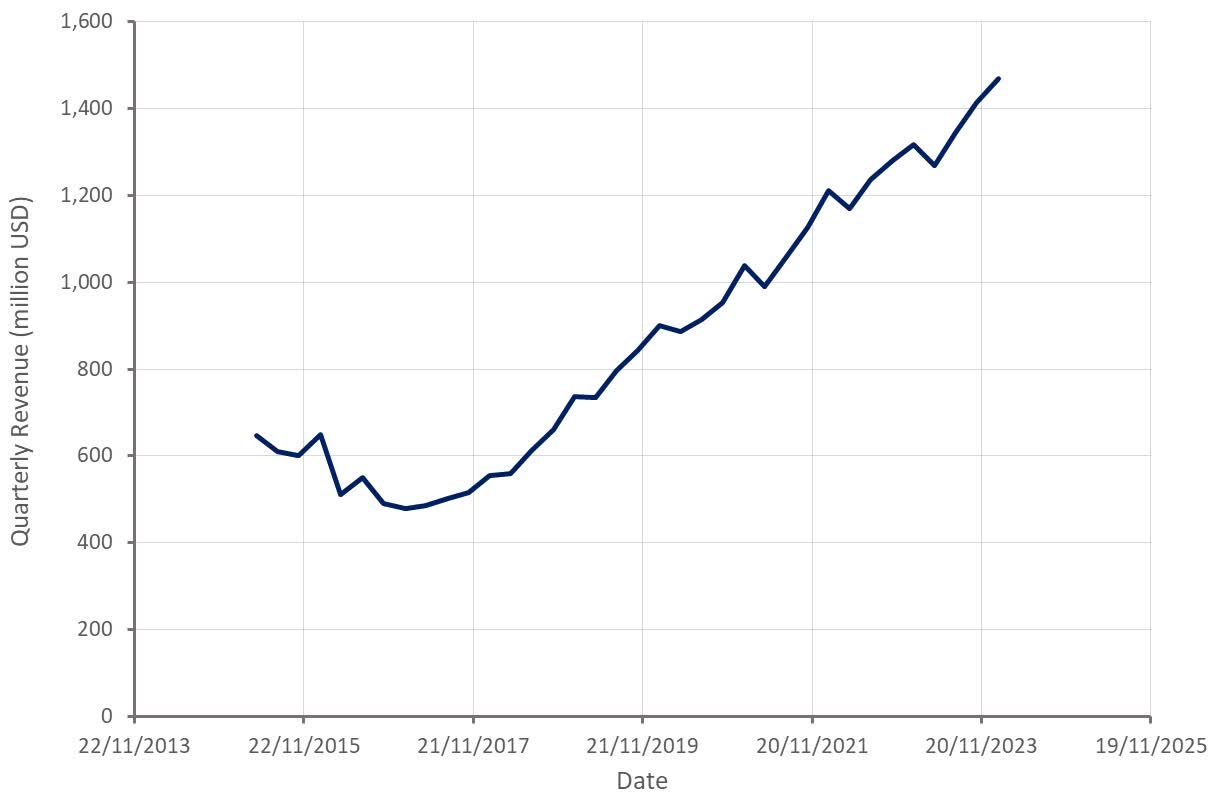

Figure 4: Autodesk Revenue (source: Created by author using data from Autodesk)

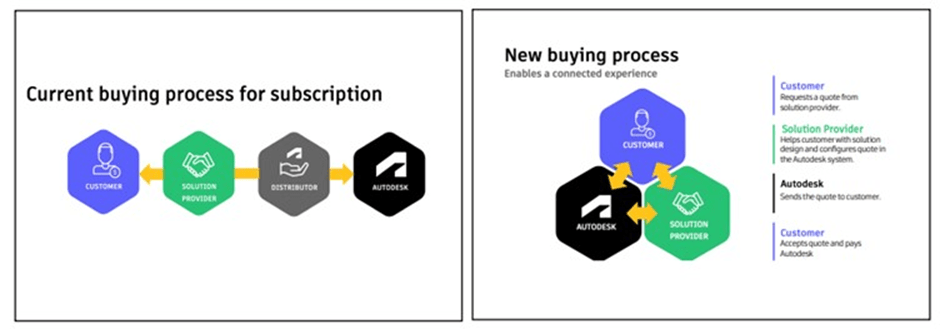

Autodesk's revenue will also be boosted by a shift in its transaction model and the associated accounting treatment. The new transaction model shifts reseller compensation from contra revenue to a sales and marketing expense. This will boost revenue and lower operating margins, while leaving the bottom line unimpacted.

In FY2024, Autodesk recognized around 600 million USD of developed market reseller compensation in contra revenue. As a result, Autodesk probably benefits from something like a 1-2% annual revenue growth tailwind in coming years.

Figure 5: Autodesk's New Transaction Model (source: Autodesk)

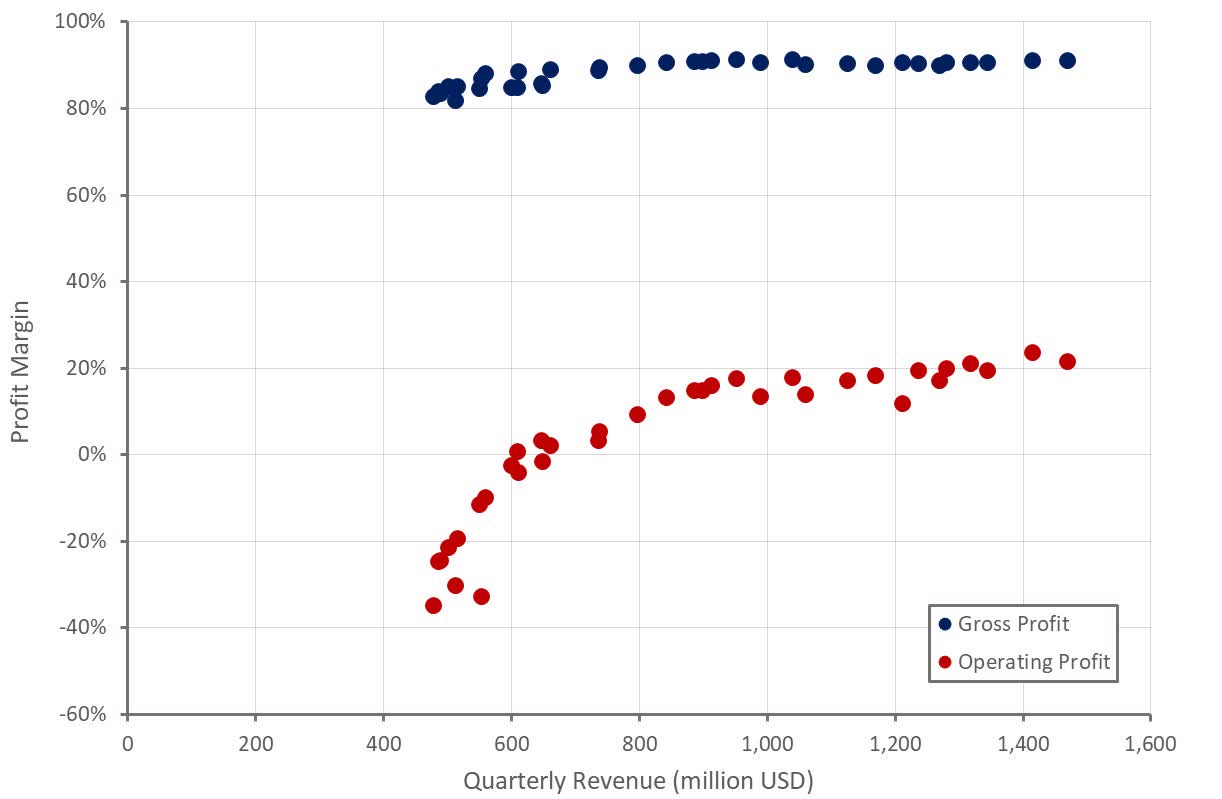

Autodesk's margins are still generally improving. despite the fact that difficulty attracting new customers is likely a modest headwind at the moment. I would expect fairly modest improvements in margins going forward though, which means future earnings growth will increasingly need to be driven by revenue growth.

The majority of the cash flow headwinds associated with a transition to multi-year contracts are now behind Autodesk, which is supportive of cash flows. Autodesk expects stock-based compensation to fall below 10% of revenue over time.

Figure 6: Autodesk Profit Margins (source: Created by author using data from Autodesk)

Outside of fluctuations in the macro environment, Autodesk's prospects continue to look strong. It is questionable whether this is enough to justify the company's valuation though. Autodesk trades on a forward PE multiple of over 50 and yet will likely only generate high single digit / low double digit revenue growth going forward.

Organic growth excluding accounting changes will probably be in the high single digits in 2024, with pricing providing much of this growth. While demand in some end markets should pick up, there is also the prospect of the current infrastructure spending boom eventually winding down. Autodesk's margins should continue to expand, but this will be much more modest than in the past.

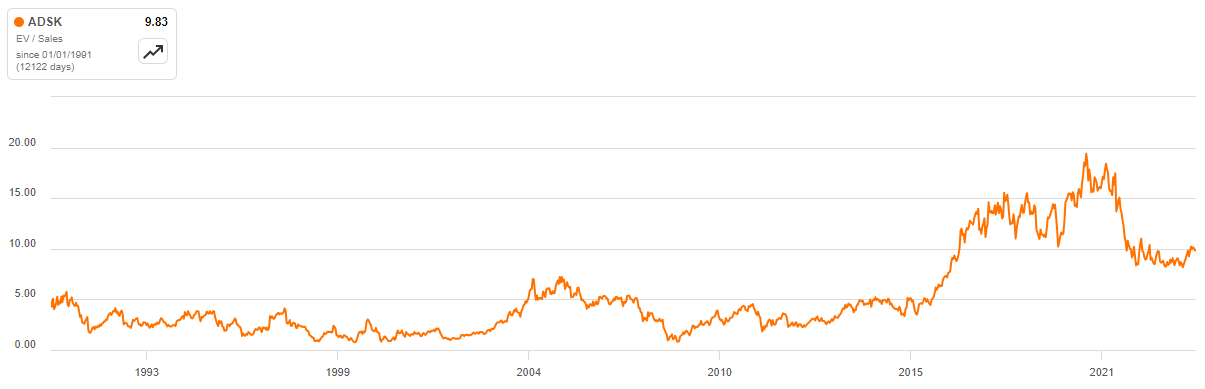

Figure 7: Autodesk EV/S Multiple (source: Seeking Alpha)