IvelinRadkov

IvelinRadkov

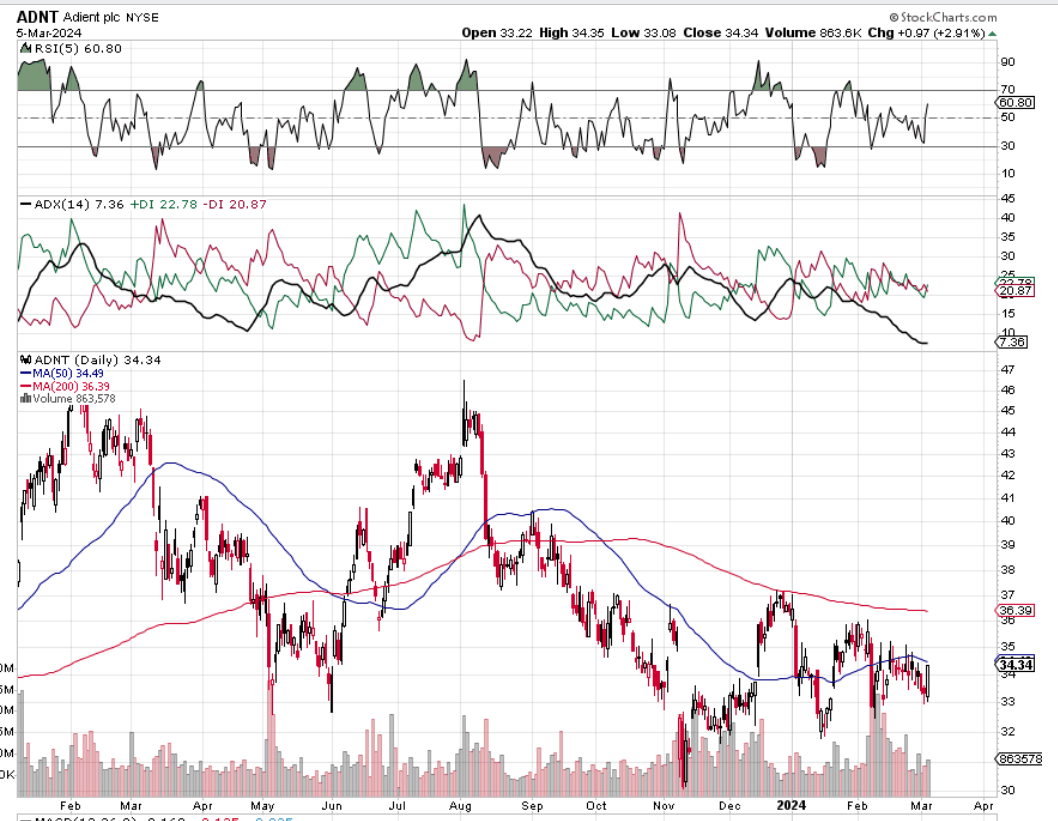

We wrote about Adient plc (NYSE:ADNT) back in May of last year when we stated that ongoing macro uncertainty had to stack up for the company so forward-looking growth projections could indeed be met. We rated Adient a 'Hold' at the time of writing. The company was just off the back of a fiscal 2023-Q2 earnings miss, which resulted in the share price continuing its pattern of lower lows. Although shares did manage to bottom roughly one month post the Q2 announcement in May of last year as we see below, this rally did not last long in that shares tested the $30 level in November of last year. The subsequent rally out of these lows has brought back shares above the $34 mark, meaning the return has been flat (0%) over the past 10 months. This validates our 'Hold' rating at the time, especially considering the S&P500 has returned 24%+ over the same timeframe. (Sizable opportunity cost if one was long the stock in this timeframe).

ADNT Daily Technicals (Stockcharts.com)

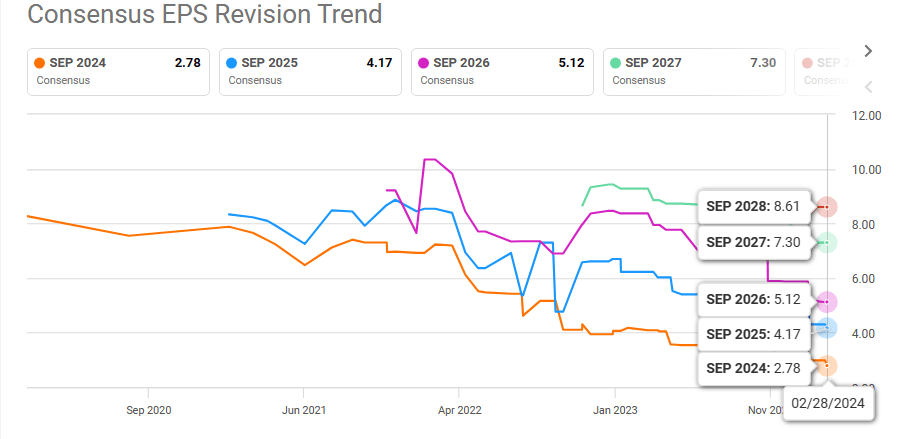

As outlined in May last year, Adient's cheap valuation coupled with consensus' forward-looking growth projections is the main calling card in this stock. However, with another earnings miss announced in Adient's fiscal 2024 earnings report last month & with forward-looking guidance also delivering a blow to consensus, the company's forward-looking growth prospects continue to come under pressure. As we see below, $2.78 in earnings per share is the current bottom-line estimate for fiscal 2024 followed by $4.17 in fiscal 2025 (ending September 2025).

Suffice it to say, it is becoming glaringly obvious how bottom-line revisions have been significantly dialed down in recent times. For example, just 10 months ago, the consensus was estimating $3.90 in earnings per share for fiscal 2024 & $5.94 per share in bottom-line earnings for fiscal 2025. Remember that Adient's current value, to a large extent, is based on the value of its future cash flows, which in turn are derived from the company's bottom-line earnings. Therefore, we are reiterating our 'Hold' rating in Adient until we see more encouraging trends in the areas discussed below.

Adient Consensus EPS Revision Trends (Seeking Alpha)

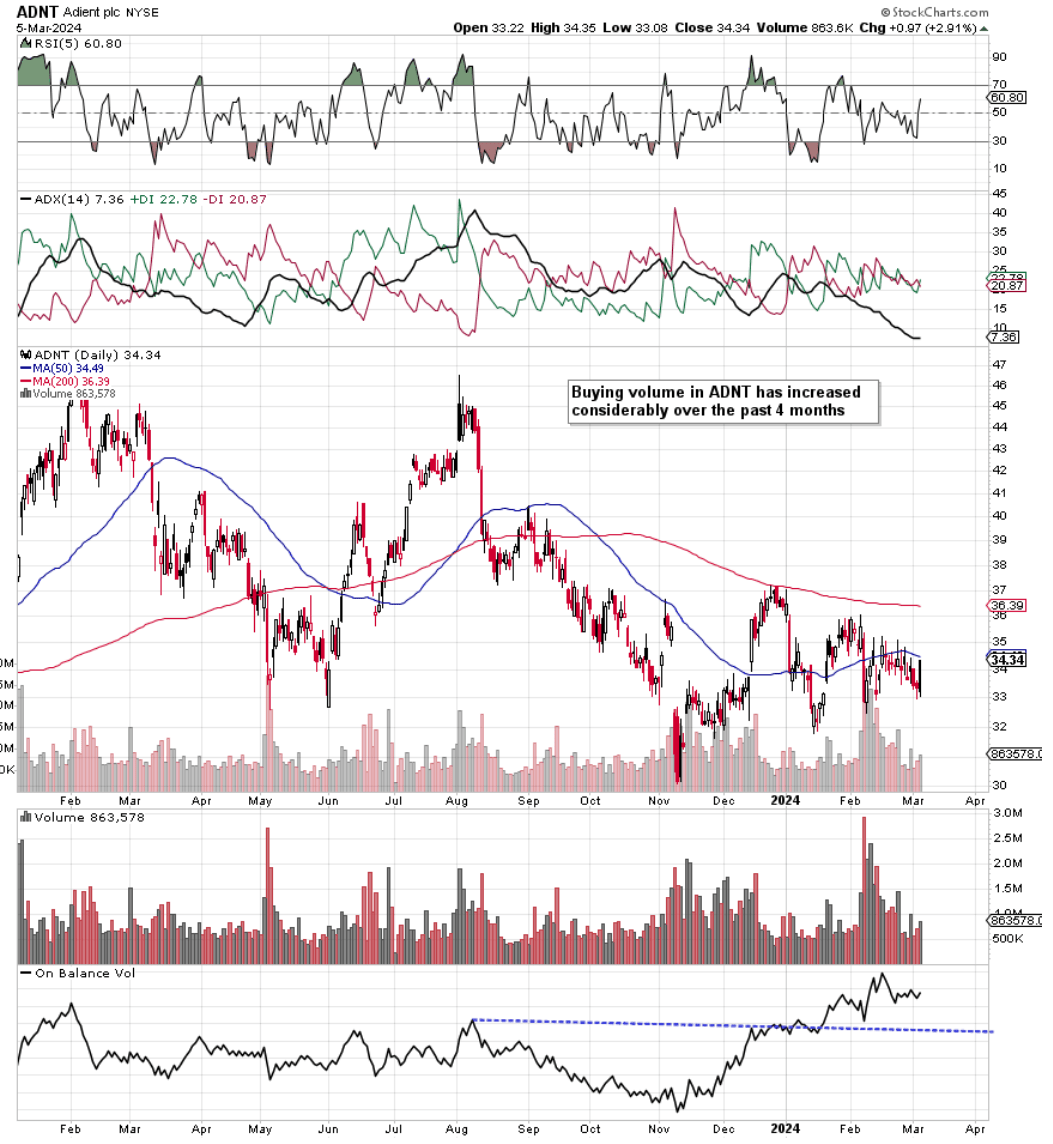

As we see below, since November of last year, buying volume has increased considerably in Adient, which is a positive sign. Although the 200-day moving average put a stop to the strong recent upmove in the stock, the subsequent downturn did not stop investors from continuing to buy Adient aggressively. We believe the technicals at all times have digested all known fundamental news regarding Adient at any given point in time so recent trends may indeed be pointing to a potential bottoming pattern. In effect, if one scrutinizes Adient's volume trends, it can be seen that buying volume has continued to remain higher even on down moves in the stock. Therefore, since volume trends many times precede share-price action on the technical chart, sustained buying could enable a breakout above resistance to take place ($36.39) sooner rather than later if present trends persist.

ADNT Bullish Volume Trends (Stockcharts.com)

Although management on the Q1 earnings call again talked up how the company's fortunes will change for the better over time despite near-term challenges, it must be acknowledged that some encouraging internal trends have come to light. For one, earnings in Q1 were adversely affected by roughly $25 million in EBITDA by the UAW strike so a resolution here over time will benefit Adient's earnings.

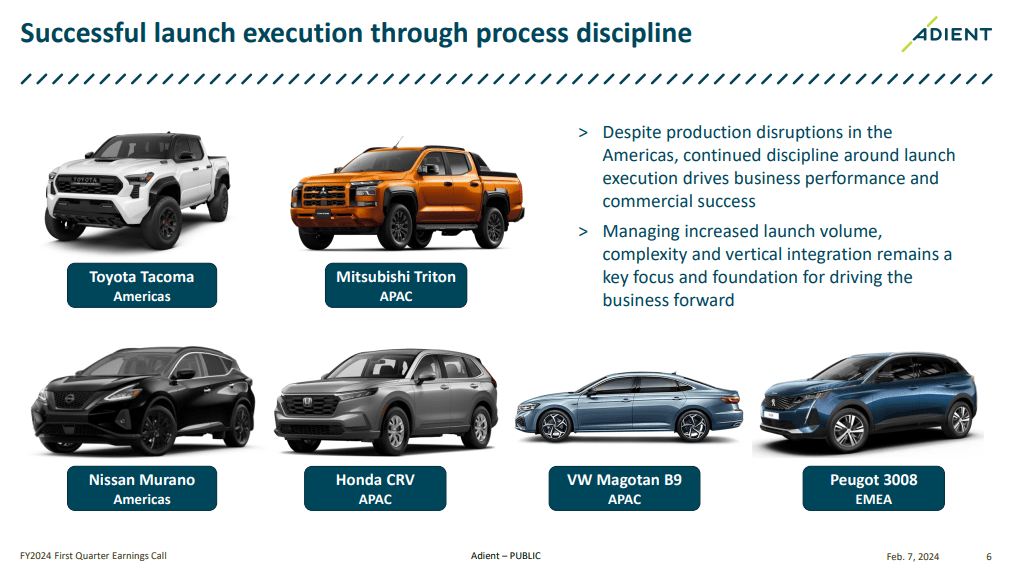

Then when we go under the hood of the company, we see how Adient continues to secure multiple business wins & business awards. Furthermore, what is encouraging is that the vast number of Adient's orders feature some form of vertical integration, strengthening the company's competitive position as a result. As we see below, despite the ramifications of the UAW strike concerning production levels, Adient still had the wherewithal to execute multiple launches. The CEO on the Q1 earnings call pointed to how 'process discipline' is enabling Adient to manage increasing launch volume, vertical integration & complexity as we see below.

we highlight several of the important recent and ongoing launches. Although the production environment in the Americas was disrupted in the quarter, our process discipline and execution enabled us to effectively execute on launches, including launches in our JIT, foam, trim, and metals business that support the deepening levels of vertical integration and business that we are winning. We can successfully navigate the delays caused by strike-related production stoppages at our customers that caused certain program starts to be delayed. The team continues to maintain process discipline, which is key to managing the number and complexity of launches scheduled for this fiscal year.

Adient Updated Business Wins & Launch Performance (Company Website)

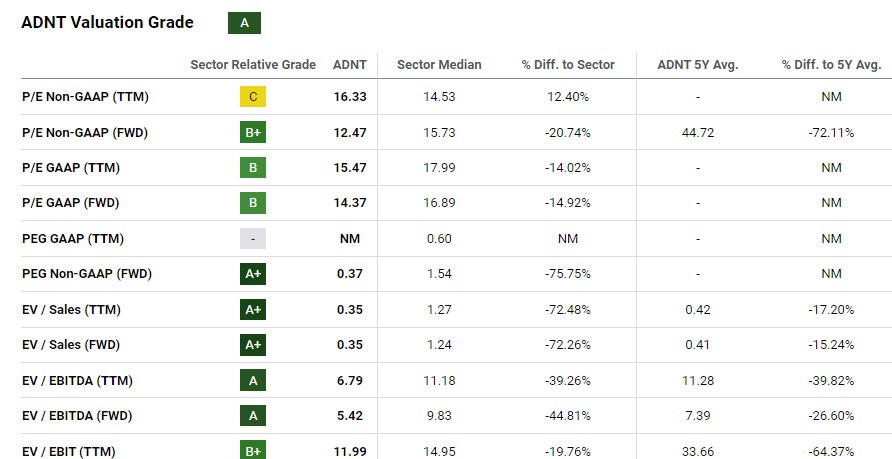

As we see below, Adient has a compelling valuation, especially concerning its sales & EBITDA multiples. Furthermore, the stock's forward GAAP earnings multiple of 14.37 also comes in well below the sector median (16.89) by some distance. Another strong driver of a company's valuation is its ROC profile or return on capital. Although Adient trails the sector in this respect (Reported (Trailing ROC of 5.1%), investors must remember that the company's true return on its capital is much higher due to the company's large cash balance ($990 million) on the balance sheet.

However, as alluded to in previous commentary, Adient's rather high debt load is also a significant factor in the company's valuation but we also are beginning to see green shoots here. Although long-term debt has remained consistent at roughly the $2.4 billion level, liquidity continues to improve, which is encouraging from a forward-looking basis. Moreover, as mentioned, the company's large cash position and associated earned interest help in suppressing that interest expense on the income statement over time. Recent debt restructuring (which succeeded in spanning out the average tenure of the company's debt from just over 4 years to almost 5 years) plus encouraging earnings & cash-flow forecasts resulted in multiple credit rating upgrades & bullish undertones from analysts, which the market took positively. Furthermore, Adient continues to be a shareholder-friendly company, returning approximately $100 million in Q1 through share buybacks to its shareholders.

Adient Valuation Grade (Seeking Alpha)

To sum up, although Adient missed the consensus earnings estimate in its recent first quarter, there were some notable trends that we took from the earnings report. Business wins & awards continue to mount and the company's liquidity position continues to improve on the balance sheet. Furthermore, strong technical buying volume in recent sessions may be pointing to a bottoming pattern, although we need to see a successful breakout above the stock's 200-day moving average to confirm the bottom. We look forward to continued coverage.