Dennis Garrels/iStock Editorial via Getty Images

Dennis Garrels/iStock Editorial via Getty Images

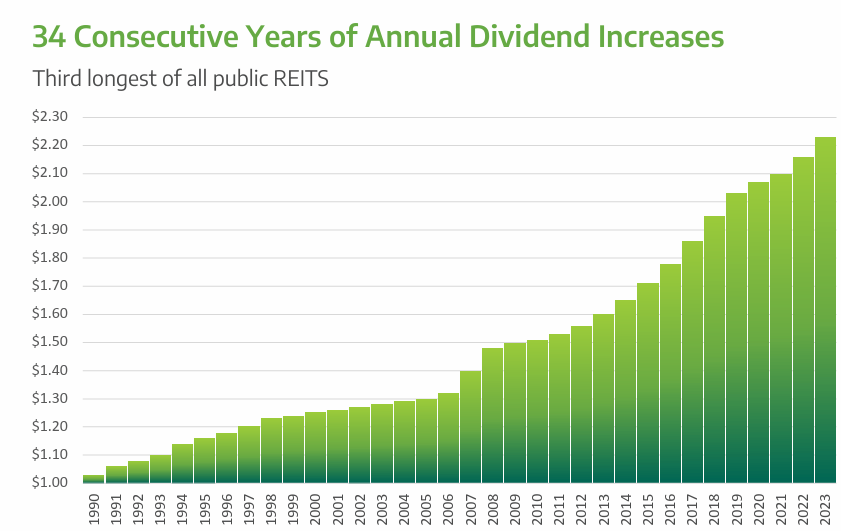

NNN REIT (NYSE:NNN) is a single tenant net lease REIT that develops and acquires retail properties across the United States. Like many net lease REITs, NNN emerged from humble beginnings. NNN was founded in 1984 as Golden Corral Realty Corporation. At that point, the company served as a landlord for the restaurant chain, much like Realty Income (O) began as a Taco Bell landlord. Over the past several decades, NNN has steadily grown to become a top tier net lease REIT. NNN has even become a dividend aristocrat and maintains the third longest streak of annual dividend increases in the real estate sector. As of 2024, NNN has raised its dividend for 34 consecutive years.

NNN REIT

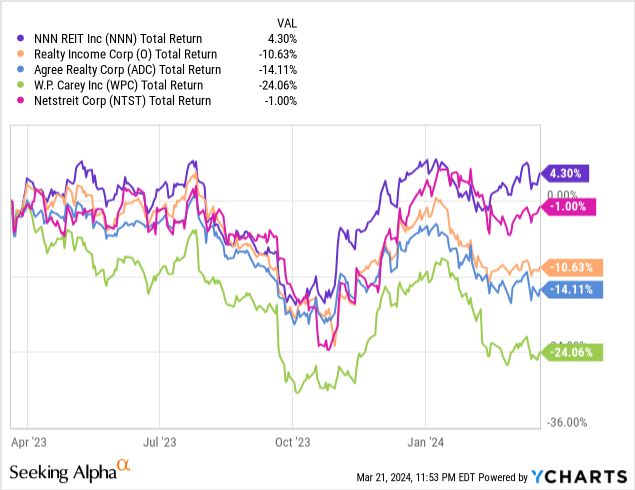

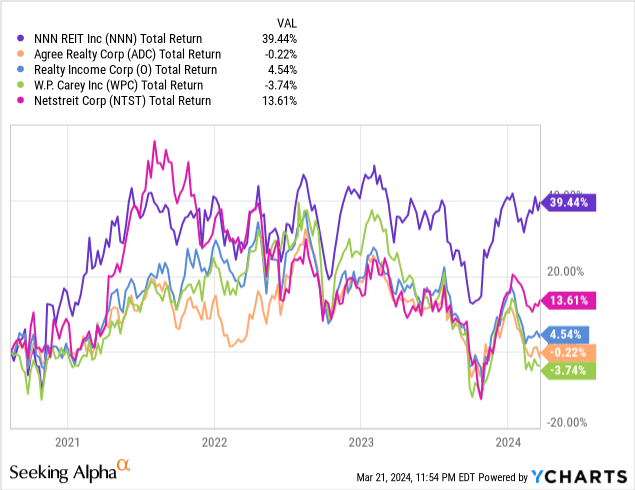

However, more impressive is NNN’s recent performance. NNN has been a sector leader which has earned praise for decades, but only recently has NNN begun to outperform peers meaningfully. We’ve discussed NNN previously, cueing in on management’s dedication to their mission and consistent growth. Our last coverage of NNN was dated December 2021, close to the start of the rising rate environment. In fact, as of our last coverage, NNN REIT was called National Retail Properties. Today, we will stack up NNN’s key metrics against Agree Realty (ADC), Realty Income (O), W.P. Carey (WPC), and NETSTREIT (NTST). NNN has outperformed each of these firms over the past twelve months.

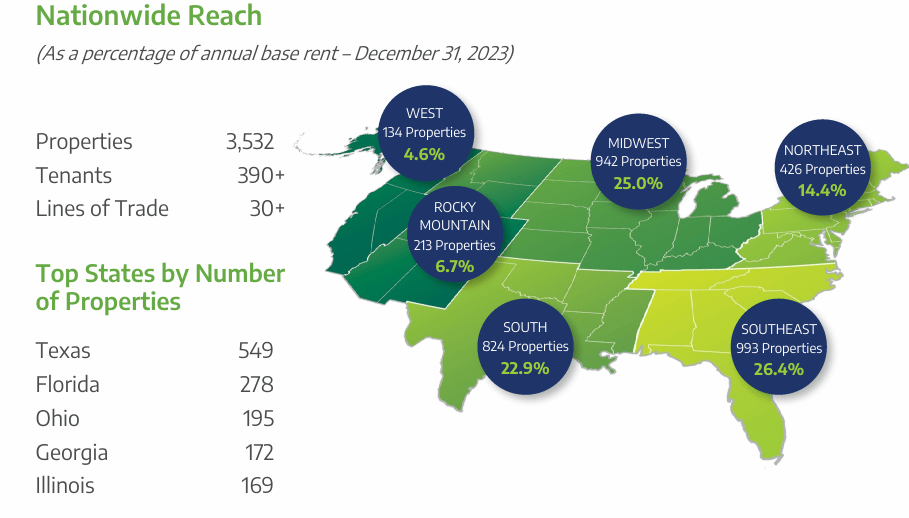

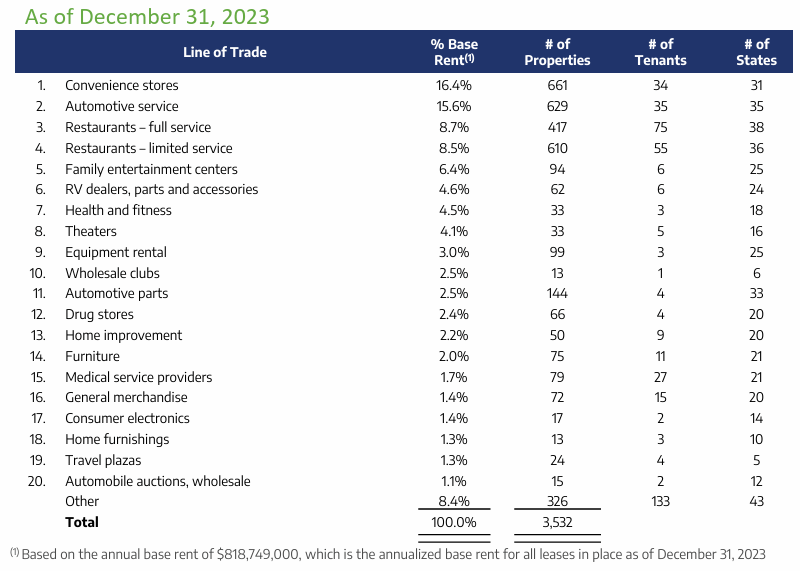

NNN manages an impressive STNL portfolio which has been widely diversified across the United States and the broad retail sector. As of year-end, NNN owned 3,532 properties located in 49 states. These properties are leased to 390 tenants, the top 20 of which account for nearly 50% of portfolio rent.

NNN REIT

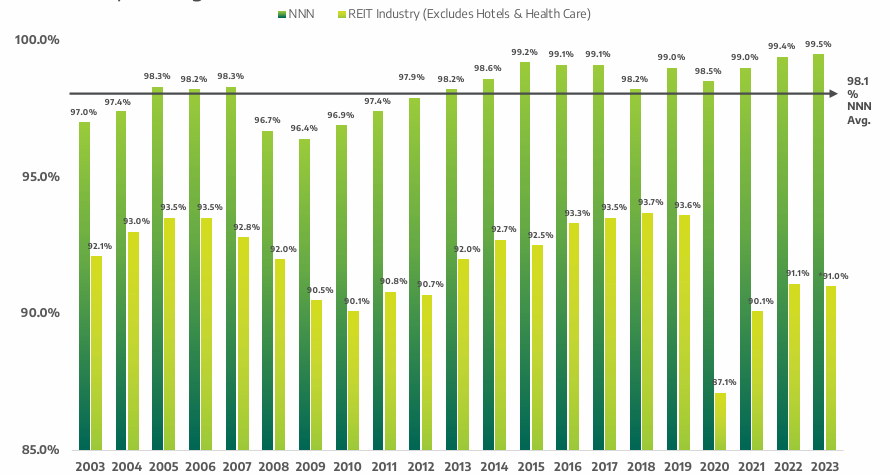

Occupancy has been a historical strongpoint for NNN. The REIT has been able to maintain a 98.1% average portfolio occupancy over the past two decades, including the pandemic and the Great Recession. Today, occupancy is even stronger at 99.5%.

NNN REIT

From a sector standpoint, NNN is diversified across modern retail sectors including convenience stores (16.4%), automotive service (15.6%), and restaurants (17.2% combined). Together, these three sectors account for approximately half of NNN’s annual base rent.

NNN REIT

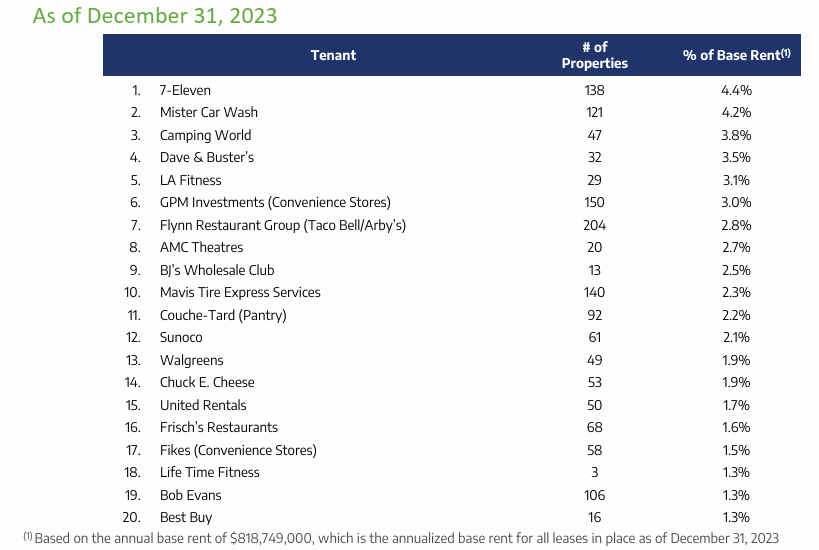

Many of NNN’s top tenants are nationally recognized brands including 7-Eleven and LA Fitness. Given NNN maintains a strong retail focus, all of the top 20 tenants are within the retail sector.

NNN REIT

A common point of criticism is the firm’s low investment in investment grade tenants. NNN invests in what is considered “Main Street” real estate. This means focusing on buildings which have strong fundamental aspects such as replacement cost, location, access, fungibility, and traffic counts. The rationale behind this strategy being that the tenant will be easily replaced should they vacate the property.

In most markets, retail real estate is located efficiently, meaning a replacement tenant would likely be within the same industry. For NNN’s fungible space, this means quick releasing and minimal concessions for incoming tenants. NNN has proven their ability to manage their portfolio. Between 2007 and 2023, 83% of leases were renewed with the current tenant. The leasing spreads were 67% above, 8% at, and 25% below in place rent. Additionally, NNN notes hesitancy to capitalize tenant improvements into future rent payments. Keeping rent lower in the near term leads to healthier leasing spreads down the line.

NNN also capitalizes largely on the development and sale leaseback segments. Many of the tenants that NNN targets are sponsored. Given the increase in debt costs, many of these investors have turned to alternative financing mechanisms to raise capital or recapitalize their targets. Sale leasebacks have remained somewhat disconnected from movements in the treasury, rising slower than the risk free rate. This means sponsors can unlock value by either selling property to pay down floating rate debt or extract capital. For NNN, this means a healthy pipeline of new opportunities and potential partners.

NNN is also conservatively capitalized. The firm’s balance sheet includes unsecured debt (42%) and common stock (58%). With a total enterprise value of over $10 billion, NNN is considerably smaller than O or WPC, meaning individual acquisitions have a larger impact on share level earnings. NNN is rated investment grade by both Moody’s, Baa1, and S&P, BBB+.

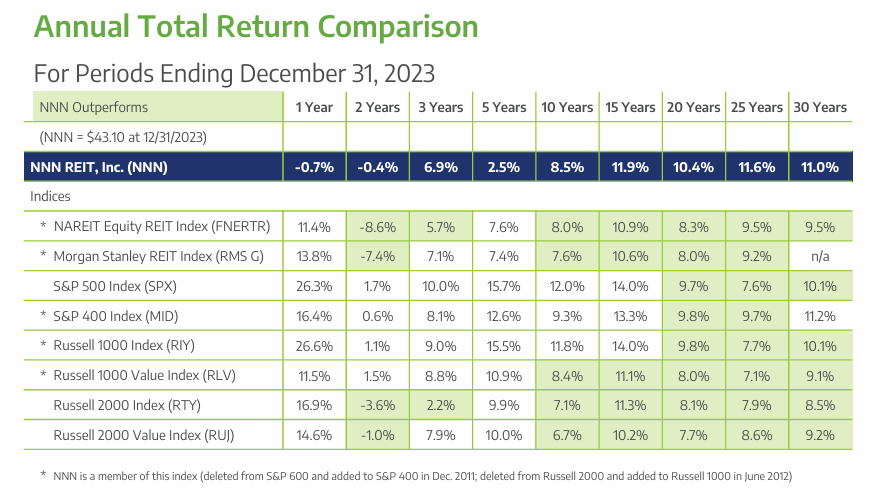

NNN has been an outstanding investment for shareholders over the course of decades. Through management’s nearly flawless long term execution, NNN has outperformed REIT indices and general benchmarks over a period of 20 years. Over the past 25 years, NNN has outperformed the S&P 500 by 4% annually.

NNN REIT

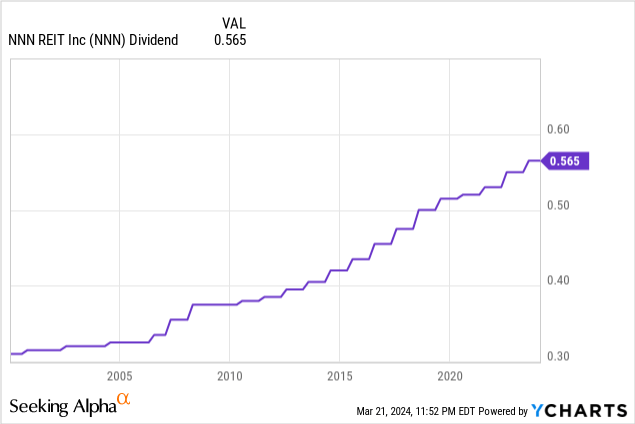

A large component of the success comes from NNN’s steadily rising dividend. As mentioned earlier, NNN has successfully grown the dividend for the past 34 years, earning one of the most impressive dividend histories in real estate. Over decades, NNN has been able to compound its dividend in line with long term inflation rates of approximately 3%. Since 2004, NNN has averaged 2.92% annual dividend growth.

NNN maintains a conservative dividend, leaving significant capital inside the business for future investment. As of year end, the dividend payout ratio was 68%, meaning NNN retains nearly one third of capital.

AFFO per share came in at $3.26 for 2023, a modest 1.6% increase over 2022. While the growth is anemic, it shines against a difficult environment for net lease REITs where financing costs have been heavily impacted by interest rate movements.

NNN actively manages their portfolio with an acquisition and disposition platform. Last year, NNN invested $819.7 million in retail properties including acquiring 165 new properties. NNN notes a going in yield of 7.3% on these new acquisitions. At the other end of the pipeline, NNN disposed of $115.7 million in assets at a capitalization rate of 5.9%. It’s worth noting that NNN maintains financial productivity by reinvesting proceeds from dispositions at higher yields.

With NNN’s strong performance against the broader sector, let’s open the hood of several competitors and compare some key metrics.

REITer's Digest, Data from Annual Reports

AFFO Multiple: Based on current share prices, NNN’s AFFO multiple is 12.7x, towards the lower end of the net lease ecosystem. Over the long term, NNN has maintained a slower growth rate than competitors such as O, ADC, or newer NTST. During the prior era of low financing costs, this was a detractor for NNN. As other firms grew aggressively, issuing stock and debt to fund acquisitions, NNN maintained a more conservative approach. While it accounts for NNN’s slower dividend growth, it resulted in a more conservative multiple for NNN. Over the past two years where net lease REITs have suffered, NNN exhibited less room for multiple compression. For shareholders, this meant better long term performance as NNN’s AFFO multiple stuck closer to long term levels. As of 2021, NNN’s AFFO was $3.06 corresponding to an AFFO multiple of 15.7x based on year-end share prices. Compare this to O’s multiple at that same time of 17.8x. The bigger they are, the harder they fall. The conservative valuation provided cover for NNN’s share price once rates began to rise.

Weighted Average Lease Term: Net lease REITs typically target long term leases. Accordingly, their weighted average lease terms are generally long. As a rule of thumb, a WALT over 10 years is typically a positive sign for a balanced net lease REIT with a healthy growth trajectory. Interestingly, each of the five REITs compared have a WALT of approximately 10 years. While longer is usually better, there is no clear winner amongst the five.

Occupancy: Occupancy is a critical measure of success for a net lease REIT. Occupancy is a marker of the asset management team’s capability to keep the portfolio moving. In the world of net lease investments, occupancy is an even more critical marker. As is common knowledge, triple net leases offload the responsibility of the three nets (property taxes, maintenance, and insurance) onto the tenant. However, if there is no tenant in place, these responsibilities (financial and otherwise) are returned to the landlord. This compounds the impact of a vacancy, as the property is no longer producing rent and the tenant is no longer covering these expenses. Portfolio occupancy is often an underappreciated metric for net lease REITs. NNN’s occupancy rate of 99.5% is stellar for a long operating net lease REIT. Bested only by ADC as another long term REIT who has maintained an exceptional occupancy percentage. NTST has reached 100% occupancy, but the company is less than ten years old, meaning many of the properties are still on their original leases. In contrast, WPC’s occupancy is 98.1% which while only modestly lower, still negatively impacts earnings. The higher occupancy for NNN has been a driving force for their strong performance.

Percentage of Rent from Investment Grade Tenants: IG tenancy is another critical success marker for net lease REITs. Investment grade ratings are generally a bellwether for the quality of a company’s balance sheet and financial health. For a net lease REIT, IG tenancy is an easy way to peer into the credit quality of a portfolio. In the simplest terms, more revenue from tenants with stronger credit is better. Backing up, net lease REITs are a hybrid investment of credit and real estate. Net lease REITs invest in properties encumbered by long term leases. Those leases are generally guaranteed by the corporate entity of the tenant or a creditworthy subsidiary. This means the leases are only as good as the creditworthiness of the occupying tenant. NNN clearly trails the pack with only 17% of annual rent coming from investment grade tenants. However, NNN’s focus on highly fungible, well located assets mitigates the risk of lower credit quality tenants. NNN’s long term occupancy average of 98.1% shows management can clearly mitigate credit risks and keep the buildings occupied. While the lower percentage of rent coming from investment grade tenants is a risk for NNN, management’s ability to mitigate the risk is proven. ADC has maintained a significantly higher portion of rent coming from investment grade tenants than NNN or O.

Percentage of Debt Maturing in 2024/2025: Net lease REITs finance their acquisitions with long term, fixed rate debt. NNN is no exception, capitalizing their balance sheet with only two components, unsecured debt and common stock. The simplicity is beautiful and reduces risk as opposed to more complex balance sheets. Increases to the federal funds rate have created significant headwinds for net lease REITs. These landlords are beginning to refinance into substantially higher interest rates, causing interest expenses to rise. However, some REITs are better insulated with debt maturities pushed out further and further. NNN has only 8% of debt maturing over the next two years, meaning most of their debt will remain in low rate debt. ADC and NTST have less debt maturing over the next two years at 2% and 0%, respectively. On the other hand, O and WPC have significantly more debt to refinance in the near term with 17% and 25%, respectively. NNN remains in the middle of the pack, but overall well protected. Additionally, NNN was unique in placing a significant amount of debt at long maturities. NN has approximately 15% of debt maturing after 2048.

Having looked at each of these five key metrics, we’ll note that NNN falls short in none. While the IG tenancy percentage lags the sector, it is consistent with NNN’s long term strategy and goals. Shareholders have benefitted strongly from the management’s focus on generating long term value consistently. NNN’s conservative valuation has helped protect shareholder from rising rates and other near term risk factors which have adversely impacts REITs.

While O remains sweetheart of most net lease investors, NNN is an exceptional REIT with an unparalleled track record. NNN’s fundamental strength is on par with ADC, making it one of the top net lease REITs. Maintaining the third longest streak of dividend increases, NNN has outperformed competitors in the sectors in terms of reliability. A conservative payout ratio leaves room for growth. Healthy acquisition and disposition activity consistently produces value for shareholders. The conservative valuation has resulted in NNN outperforming peers over the past twelve months. There is a lot to like and NNN remains well positioned as one of the best managed, but least recognized REITs across the real estate sector.