Erik Isakson

Erik Isakson

Astera Labs (NASDAQ:ALAB) is one of the few AI pure plays in an industry dominated by tech giants and private companies. Publicly traded AI giants like Microsoft (MSFT), Alphabet (GOOGL), and Amazon (AMZN), all have large businesses outside of AI. While AI is an increasingly important part of these companies' businesses, it still only accounts for a small percentage of their overall revenues. Astera Labs, on the other hand, has centered its entire business around the AI boom.

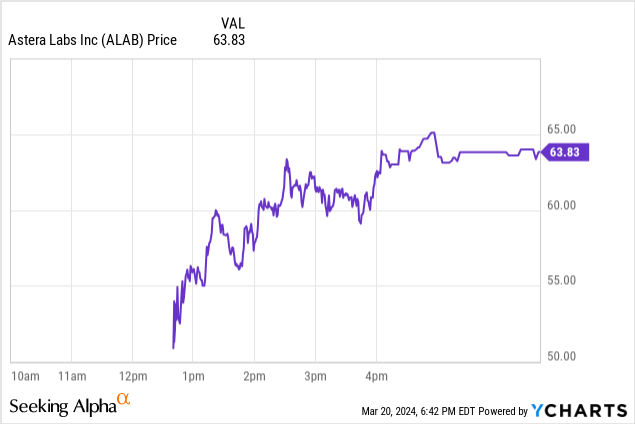

Astera Labs' share prices jumped dramatically after the company IPO'd.

The foundation of Astera Labs lies in its high-performance connectivity chips and software platform. Traditional data centers are having an increasingly difficult time handling the data movement required for large-scale AI applications like ChatGPT and other LLMs. Astera Labs chips act to more seamlessly and efficiently connect GPUs within AI clusters.

The company's PCIe (Peripheral Component Interconnect Express) and CXL (Compute Express Link), for instance, help extend GPU connectivity and reduce bandwidth/capacity bottlenecks. As AI infrastructure grows in size, which is to be expected given how important scale is in LLMs, Astera's products will be perfectly suited to address data center scale and performance requirements.

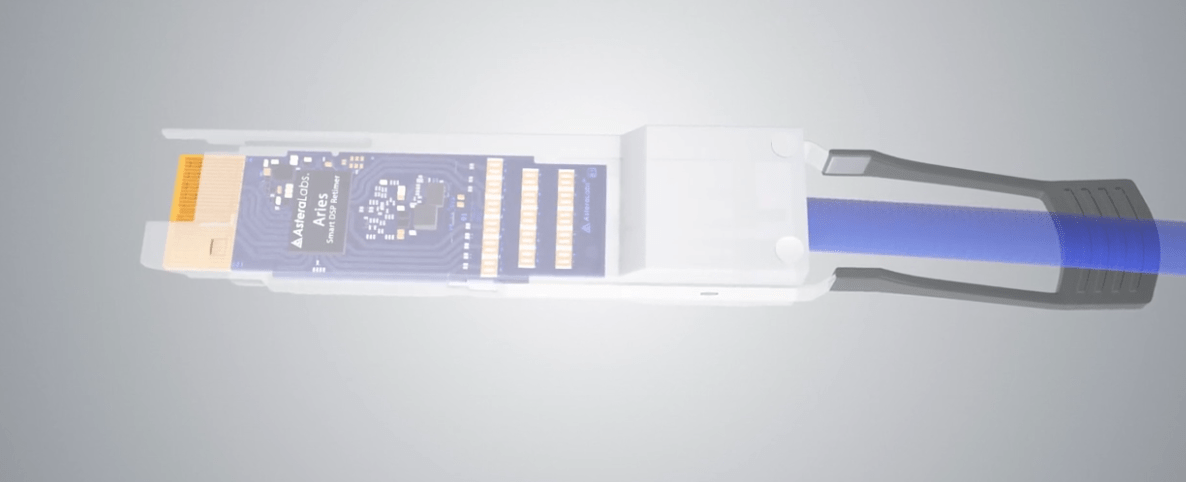

The Aries PCIe/CXL Smart Cable Modules extends "PCIe 5.0. PCIe 4.0, and CXL signal reach to enable GPU-to-GPU interconnects in larger AI clusters and connectivity between processors and attached memory resources at cloud-scale.

Astera Labs

The global AI market will likely be worth trillions of dollars by the end of the decade, making it one of the fastest growing markets. Much of this growth will likely be driven by advancements in generative AI and LLMs (large language models) like ChatGPT, Gemini, Claude, and Mistral. The scaling laws that have applied to these models so far do not appear to be slowing down in any meaningful way, which means that these LLMs have far more room to grow.

Astera Labs has positioned itself perfectly to cater to this growing AI market by offering products to assist in the development of hyperscale data centers. What's more, companies outside of big tech are also starting to utilize their own models to enhance their products. Adobe (ADBE), for instance, has its own generative AI offering specifically designed for image and video generation. This demand of generative AI will likely drive sales for Astera Labs products.

Astera already has partnerships with industry giants like Intel (INTC), Nvidia (NVDA), and AMD (AMD). Not only do these partnerships lend credibility to Astera's technology, but they also give Astera access to cutting-edge AI technologies. Establishing ties to industry heavyweights this early on gives Astera a certain safety net that many of its competitors do not have. Moreover, these established partnerships will likely help validate its products to other potential hyperscalers.

Axios believes that Astera's TAM will exceed $27 billion within three years, which seems entirely possible given the appetite for hyperscale data centers of its current and potential partners. However, even this may be an underestimation of how much demand there will be for Astera's products. In terms of training costs alone, Anthropic CEO Dario Amodei believes that there could be $1 billion models in 2024 and $10 billion models in 2025. These figures far exceed the ~$100 million training cost of GPT4. If these figures are anywhere near accurate, Astera's TAM could be far greater than anyone anticipates.

Astera Labs has showcased strong financials in recent years, with its revenue jumping for $79.9 million in 2022 to $115.8 million in 2023. This 45% growth rate is indicative of Astera Labs leading position in an incredibly fast-growing industry. While Astera Labs is still losing money, this is to be expected of a small high-growth company investing in nascent technologies. Moreover, the company has managed to narrow its losses from $58.4 million in 2022 to $26.3 million in 2023.

Astera Labs is still a relatively small company in a fast-growing and highly competitive industry. Larger players like Marvell and Broadcom are already major competitors to Astera Labs. In addition, a great deal of new entrants are likely to emerge if the market continues to grow at its current pace. Astera Labs will need to continually innovate to keep ahead of the competition, which may be difficult given their relative lack of resources.

Astera Labs is also catering to a few hyperscalers, which means that the company could lose large portions of its business should any of its customers leave. The customer concentration on a few large players comes at a major risk should they choose other solutions or even create their own. Should a company like Intel or Nvidia decide to manufacture its data center connectivity products in-house, this would be a huge blow to Astera Labs.

Astera Labs has experienced a wildly successful IPO, jumping a whopping 72% on Wednesday to end the day with a market capitalization of $9.5 billion. This jump in valuation showcases the demand for AI pure plays like Astera Labs. Despite this dramatic jump in market capitalization, Astera Labs still has more room to grow given its strong positioning in an integral AI market.