Ibrutinib, the BTK inhibitor which Corvus CEO Richard Miller was able to sell to AbbVie in 2015 while CEO of Pharmacyclics.

ollaweila

Ibrutinib, the BTK inhibitor which Corvus CEO Richard Miller was able to sell to AbbVie in 2015 while CEO of Pharmacyclics. ollaweila

We first heard the name Corvus Pharmaceuticals (NASDAQ:CRVS) in a text message from Derek’s dad, asking our opinion on them. A cursory review of their company materials led us to conclude they were, for a clinical-stage company, in good shape and maybe worth considering for investment. Curious how he heard about this small name, it appears they had recently featured in a TipRanks article after getting some analyst love from Oppenheimer.

The more we dug, though, the more it seemed like there may be some real substance to this name. Their recent “all-in shove” on the ITK inhibitor soquelitinib, including the plans to commence a Phase 3 clinical trial in relapsed peripheral T-cell lymphoma (PTCL) early next year, has them positioned in a place we wouldn’t expect from a clinical-stage pharma this size. That trajectory could cause trouble, however, as advanced clinical trials will put increasing pressure on the company’s cash flow, a fact that did not go unnoticed on the latest earnings call. From our estimates on the opportunity for an ITK inhibitor, there is a huge upside potential here, but not without a significant chance for a zero.

The decision to jump directly to a Phase 3 clinical trial may smack of overconfidence, but it is also a huge opportunity to make a difference in a part of the heme-onc space that, by all accounts, needs a shot in the arm. From our research, the last high-profile drug that went from Phase 1/1b to Phase 3 was Aduhelm, the much-maligned Alzheimer’s drug from Biogen (BIIB) and Eisai (OTCPK:ESALF), which doesn’t exactly instill confidence in the strategy. That being said, we listened to the call where leadership discussed the meeting with the FDA and the plan to begin the Phase 3 trial, and they definitely made it sound like PTCL is a subtype of lymphoma that is overlooked (eligible for “orphan drug” designations) but so severe that it warrants investigation:

The only currently approved and recommended course of treatment is chemotherapy, full stop

Median progression-free survival (PFS) is 12-14 months following chemotherapy, and 5-year disease-free survival rates are 20-30%, indicating this is a particularly aggressive cancer with a high likelihood of relapse

According to CEO Richard Miller on the strategy call, if there is relapse, the next recommended action is to enroll in a clinical trial (although this may be true of other cancers for which chemotherapy is the only approved treatment)

As the company themselves released a preprint in July of this year highlighting the positive results in in vitro and murine models, the company’s clinical partners have been showcasing the results at conferences, including ICML in June and ASH in December of this year. Results of the Phase 1/1b trials do appear encouraging, even dramatic in some of the pictures of patients included in the ICML poster.

By the numbers, PTCL makes up 5-10% of all non-Hodgkin Lymphomas diagnosed in the US yearly, which comes out to about 6,000-8,000 new cases every year. With a high incidence of relapses, it’s safe to assume most if not all of these new cases will likely be flowing into the market for soquelitinib. The aggressiveness and the poor prognoses for patients also likely played into the decision to target this label first. Miller commented that since PFS is their primary endpoint for the Phase 3 study, there is technically no set end date for the study, they read out when there are sufficient “PFS events” (which means an enrolled individual experiences disease progression or dies for any reason). Given the median time for relapse in the status quo and the advanced age of the typical PTCL patient, they anticipate about two years to be able to achieve a readout.

The study has 87% power to see a prolongation of survival, which comes out to somewhere in the range of four to six months at p < 0.025. While 4-6 months doesn’t feel that long in the grand scheme of things (Derek certainly felt so when he saw the TV spots for Opdivo back in the day), that is 33-50% of the current median PFS, which is a high bar to clear. We’re cautiously optimistic they’ll meet their primary endpoint, but cynically, we’re still heavily leaning towards a wash-out.

Given that tightly-binding ITK inhibitors have been in the scientific literature with full atomic-resolution structures since as early as 2010 (including covalent inhibitors in 2012), it is surprising it took this long for anyone to actually pursue it in the wake of ibrutinib’s blockbuster success. Granted, oncology, immunology and drug discovery were in a very different place 10+ years ago versus today. That also raises the stakes for Corvus in case these old studies from names like Pfizer (PFE) and Roche (OTCQX:RHHBY) lead to an infringement claim, invalidate the patent, or inspire additional competition into the space.

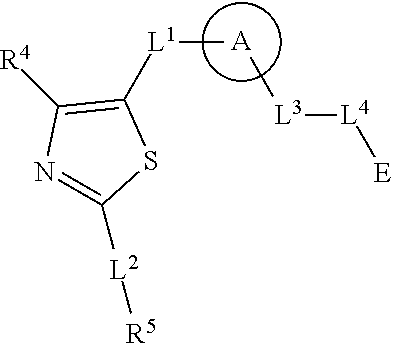

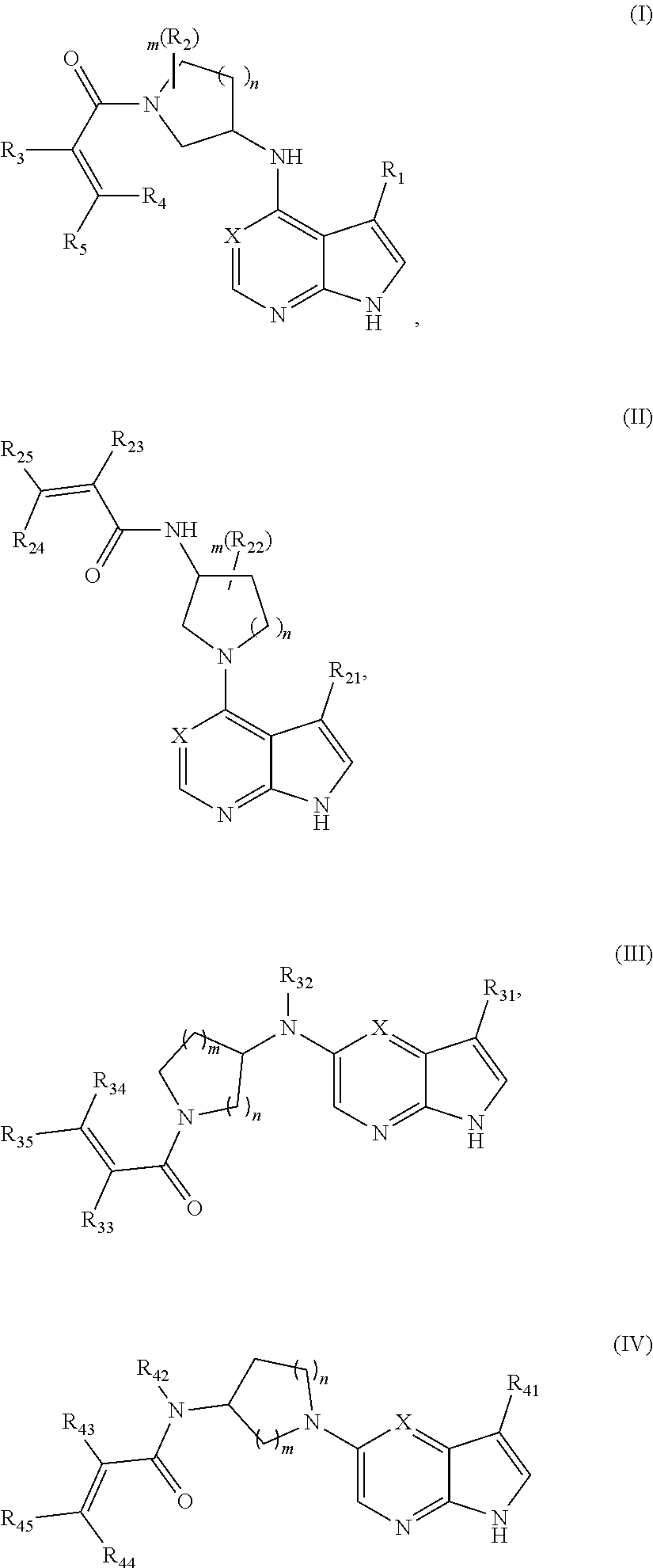

Reviewing the patent application for soquelitinib and its related compounds, we see that only two small parts of the molecule, an “aminothiazole ring” and the acrylamide group which reacts with the cysteine on ITK, are explicitly called out. The remainder of the molecule is described in the application with an immense wall of combinatorial chemistry. For want of a tool to parse the dense, deeply nested descriptions of each possible variable, we estimate this patent covers a library of thousands of compounds. Of the other patent applications related to BTK and ITK inhibitors that we’ve reviewed, the one other equally comprehensive library has to be the pyrrolopyrimidine inhibitors from Aclaris (ACRS), another clinical-stage pharma company focused on the immuno-modulatory nature of kinase inhibition.

The ITK inhibitor library over which Corvus holds patents. Groups labeled R#, L# and A may vary as described in the patent body. (US Patent 11,008,314) The ITK inhibitor library over which Aclaris holds patents. R#, m and n may vary as described in the patent body. (US Patent 11,820,775)

On the strategy call, Miller mentioned that they already have second- and third-generation ITK inhibitors more aimed at the autoimmune and allergy space. During the Q3 earnings call, Miller also commented that they have more latitude in terms of partnership due to the breadth of the immunology space as opposed to the oncology space:

“the inflammation immune disease represents a good partnering opportunity because we have a series of backup molecules that are pretty close to the clinic…

...we're already getting significant inbound interest on partnering the immunology part of it, the immune disease part of it. Now, we like that because our expertise is cancer, and autoimmune disease, as you know, there are many different types of autoimmune disease that crosses disciplines like pulmonary medicine and dermatology and rheumatology, et cetera. So we think a company at our stage with our resources, partnering the immune disease aspects makes the most sense and allows us to continue to focus on T cell lymphoma and solid tumors.”

Now that we’ve established that the drug itself is well-positioned in its portfolio, the pilot oncology trial is looking promising and the interest in the immunology story is heating up, we need to address the other players in this space. Immune cell kinase inhibition occupies a unique intersection in the pharmaceutical world, crossing both oncology and immunology indications, so naturally there are many companies out there with drug libraries and patents on various kinase inhibition schemes that could impact the long-term potential of soquelitinib.

Patents for at least two classes of small-molecule ITK inhibitors were filed and approved prior to soquelitinib: benzimidazole derivatives from Principia, a now-subsidiary of Sanofi (SNY); and arylpyridinone inhibitors from a now-subsidiary of Aclaris. Sanofi’s acquisition of Principia was more for their portfolio of BTK inhibitors, notably rilzabrutinib, and no mention of “ITK inhibitor” or IL-17 is found on their drug pipeline page. Aclaris is investigating the small-molecule kinase inhibitor space for oncology as well, but their emphasis is on MK2 inhibition, not ITK inhibition.

Turning to indications, both oncology and immunology are both rife with Big Pharma names and other clinical-stage companies looking to make their mark. Within PTCL alone, the Lymphoma Research Foundation's fact sheet lists at least nine drugs being trialed as of 2022, but searching each company’s page reveals only four are still in pipelines for PTCL:

duvelisib from Secura Bio

azacitidine from Bristol-Myers (BMY)

lacutamab from Innate (IPHA)

valemetostat from Daiichi Sankyo (OTCPK:DSKYF)

All of these drugs have different modalities and mechanisms, from chemotherapy-style treatments to monoclonal antibodies targeting T-cell-specific interactions, but as best we can tell from pipeline information, all of these drugs are still in Phase 2.

Soquelitinib doesn’t have to compete with these other modalities, however; as we’ve seen with other small-molecule immune kinase inhibitors like ibrutinib, they can often reactivate otherwise “cold” tumors and increase the efficacy of the standard battery of immuno-oncology therapeutics. In particular, suppressing ITK downregulates a phenomenon known as “T-cell exhaustion”, which is what leads to increases in the oft-targeted checkpoint molecules PD-1, LAG3 and TIGIT.

Immunology may be a much steeper hill to climb. During the strategy call, Miller mentioned the first major indication they wanted to target was atopic dermatitis. As soon as we heard that phrase, the big boys came to mind: Dupixent (REGN), Rinvoq (ABBV), etc. There’s even topical JAK inhibitors now coming to market that are meant for dermatological indications. Almost any immunological condition, Type 1 or 2, will have some kind of small-molecule kinase inhibitor or biological therapeutic already established (if not the old standby methotrexate), so the old adage applies that any new challenger needs to be “way better” or “way cheaper”. Better, in this case, means either better efficacy or reduced side-effects. The bar to clear for side-effects is actually pretty low compared to drugs like JAK inhibitors, which carry that dreaded “black-box warning” (Derek heard a TV spot for Rinvoq and the black-box warning equivalent must have taken up at least two-thirds of the runtime).

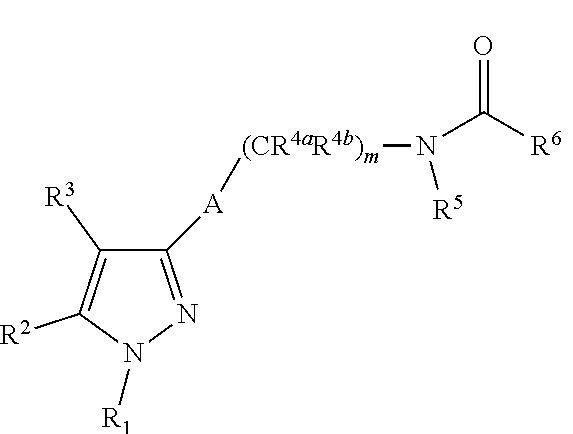

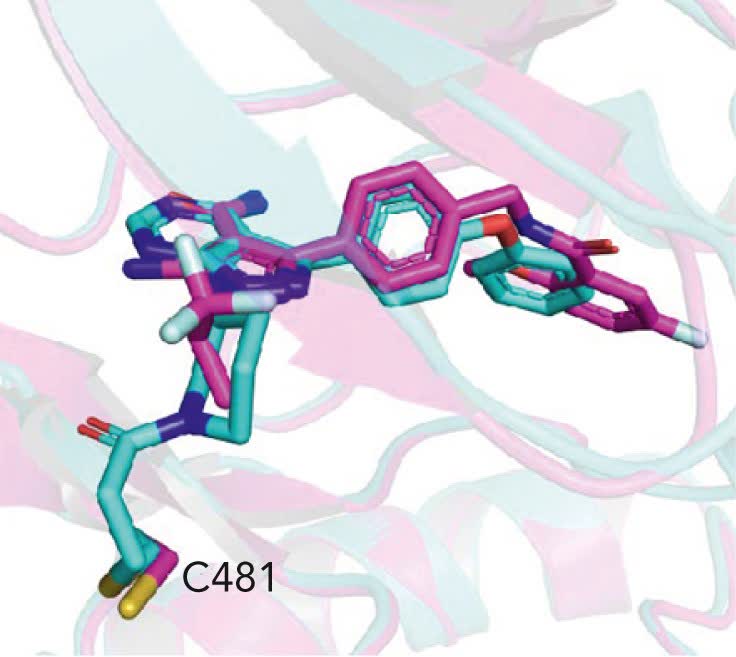

Another key mechanistic consideration is the irreversible nature of soquelitinib, echoing how ibrutinib rose to stardom after being relegated to “tool compound” status in Celera’s portfolio. As we discussed with BTK inhibitors in our piece on Merck, the market share is shifting away from irreversible inhibitors towards reversible-but-strongly-binding-and-specific inhibitors, in large part because BTK in cancers evolved a mutation that imparted resistance to ibrutinib and other inhibitors were too broad-spectrum, leading to off-target effects. The patent covering pirtobrutinib, the first approved reversible BTK inhibitor, describes another broad library of compounds with just a pyrazole ring and an amide linkage as the only non-combinatorial moieties in the whole patent. They’re able to pretty easily tack on hydrogen bonding groups, mostly amines and amides, in order to stabilize the drug in the active site, then use big bulky fluorines to take up space.

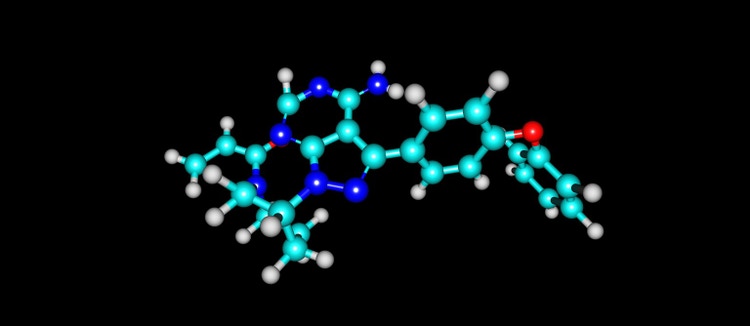

The BTK inhibitor library which includes pirtobrutinib. R# and m may vary as described in the patent body. (US Patent 10,464,905) Ibrutinib (cyan) and pirtobrutinib (magenta) binding to BTK as captured by X-ray crystallography. Note ibrutinib bound to C481. Despite the large differences in the molecules' cores, they both offer up hydrogen bonding partners in nearly the exact same spaces of the binding pocket. (Blood (2023) 142 (1): 62–72.)

Now that companies have proven this works for BTK, it can’t be too long before they start the same process for ITK. That’s a problem we’d relegate to beyond the clinical-stage, but it’s nonetheless important for whomever comes to own this asset.

And that segues nicely into the last major discussion point: the operational side of things and how to value them. Corvus’ management has a stellar track record and seems to be navigating this productionization very smoothly. Cash burn may be a concern as the Phase 3 trial progresses, but it sounds like there are enough knobs to turn to keep the lights on without selling too much of the farm.

We already quoted CEO Richard Miller several times during this article; perhaps burying the lede a bit, but this man has already struck gold twice in his pharma career. He was one of the discoverers of rituximab while at Idec prior to the Biogen merger, and afterwards managed to flip ibrutinib while at Pharmacyclics into a $21B acquisition. It stands to reason he has a deep Rolodex across pharma and the clinic, which is priceless for a company this size. It’s no surprise that, even with reversible BTK inhibitors starting to make waves, he’s sticking with what he knows in building out soquelitinib. Circle of competence, you love to see it.

Naturally, the big scary caveat exists that a track record is strictly “one-sided error”. He won’t run the company into the ground, but it doesn’t mean that soquelitinib is guaranteed success. Another consideration is that if Corvus gets acquired, Miller will probably not stick around, both because of the stage of his career (he’s on the board of Bolt Biotherapeutics (BOLT), which is a sign that “you’ve made it”) and because he fits the bill of a “serial entrepreneur” always looking to launch the next big thing.

“Assets” here refers to both the drug IP and their balance sheet for actually keeping the lights on. On Seeking Alpha’s summary page, soquelitinib is not even listed as the “lead compound”, they list the CD-73 inhibitor mupadolimab with top billing. Corvus has actually offloaded their other clinical-stage drugs to a joint venture with a Chinese partner, Angel Pharmaceuticals, in the interest of focusing on soquelitinib. Angel is leading the clinical trial effort for these drugs, mostly in mainland China, and also providing clinician support for soquelitinib. The lead presenter for the soquelitinib materials at ICML and ASH is from the Department of Lymphoma at Peking University Cancer Hospital, a connection likely facilitated by the Angel founders. Corvus also has a 49% ownership stake in Angel valued on their balance sheet at $17M as of Q3 2023, and on the earnings call they stated they were willing to sell part of that stake if they needed to raise capital, although this stake’s book value has been written down steeply in recent years:

| Year | Carrying value of Angel stake ($MM) |

| 2020 | 37.225 |

| 2021 | 34.266 |

| 2022 | 21.877 |

| 2023 (Q3) | 17.072 |

The balance sheet lists $32M in cash and equivalents as of September 2023, and on the Q2 earnings call they stated they will require around $20M to run the Phase 3 clinical trial. R&D Expenses have been on the decline since 2017, and the decision to shift other drugs to Angel is likely having a beneficial impact there. The company has no debt, which is nice to see, but the easy money times are over so how much debt a pre-revenue clinical-stage company can reasonably take on is in question.

The company’s financial statements also disclose they have a program in place to sell up to $90M of equity at the market. They have used $7.8M of that allotment, most of which came in Q2 2023. If they were to fully utilize this plan, at their current share price that would translate to just under 49M shares issued, which would more than double the shares outstanding. Even if they funded the entirety of that projected $20M clinical trial budget from this program, that would add 11.9M shares, about a 25% dilution. Clearly not the greatest outcome, but it’s a nice option to have in the back pocket if the stock price gets rich (almost like a “reverse share buyback”, you would want to issue more equity when you’re overvalued).

The option to partner with larger companies with more experience on the immunology side is a veteran move that avoids costlier forms of financing operations, as commenters on our Regeneron articles called out concerning deals like the Dupixent arrangement. No doubt Miller has contacts at firms like Biogen, AbbVie, etc. that would be eager to partner up.

Lastly, we’re talking about a clinical-stage company, so one of the large beasts in the room has to be the endgame. Judging by Miller’s previous two triumphs, an acquisition sounds like the surest outcome. The question is whether it will be a windfall or a firesale.

We can’t use our standard approach for this one, the company is pre-revenue and likely will have one of a small number of terminal valuations. The scenarios we projected are based on the following data:

Pharmacyclics was purchased for $21B by AbbVie in 2015, exclusively for ibrutinib in oncology indications

Rinvoq, the biggest JAK inhibitor on the market, brought in $15B in revenue last year for immunological indications

The oncology story and the immunology story are partially orthogonal, which gives us four possibilities: both work, one or the other works, neither work.

In the oncology case, we project that soquelitinib is worth the same as ibrutinib with a premium for inflation, around $30B

In the immunology case, we project that soquelitinib is worth the same as Rinvoq, $15B, if the oncology story is successful. If that part fails, we build in a 25% haircut because they’ll likely have to scramble to raise capital to run more trials, and that will mean a reduced ROI.

As pessimistic as it may sound, we’re assigning a zero to the scenario that nothing pans out. They’d likely just license out the library and relegate soquelitinib to a “tool compound”, or liquidate and fade into obscurity. Seems only fair to balance out the optimism of the drug working for both oncologic and immunologic indications at parity with the standard of care.

Our sense is that the probability of the oncology case succeeding is 15%. Given the team’s expertise and how quickly they’re moving it through the pipeline, that’s a good sign, but there’s no such thing as a sure thing in clinical trials. For immunology, we’re less certain since they haven’t disclosed any clinical trials for soquelitinib or later-generation ITK inhibitors, so we assign a success probability of 10%. The weighted average valuation comes out to:

Total | $5.75B | 100% |

Case | Valuation | Probability |

Oncology + Immunology | $45B | 5% |

Oncology alone | $30B | 10% |

Immunology alone | $10B | 5% |

No success | $0 | 80% |

Since we’re speculating that acquisition is an exit strategy, we assign an exit multiple to the hypothetical deal to get our present value. Pharmacyclics’ price-to-sales ratio was in the 13-15 range in the year after ibrutinib was approved and prior to the AbbVie acquisition, so that multiple feels fair to apply in this case. We back out a present valuation of $382.95M, which comes out to an $8/sh price target, right in the meat of the analysts' targets. Given that this is a weighted valuation with a large chance for a complete loss, it’s the classic high-risk, high-return play.

Going deep on a clinical-stage pharma is definitely not the sort of thing we routinely consider as value investors, but it certainly taught us a lot, as did putting together this analysis. We opened a position to be there in case it does go supersonic, but if they flame out, we won’t lose sleep over it. The science looks promising, and if they can really move the needle, it would be a huge win for our understanding of immunology. There’s a long road to get there, though, but we’re excited enough to put some skin in the game and take a ride. If you have the risk tolerance and are okay with the tightrope walk that is Phase 3 clinical-stage, by all means give Corvus a look.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.