MicroStockHub

MicroStockHub

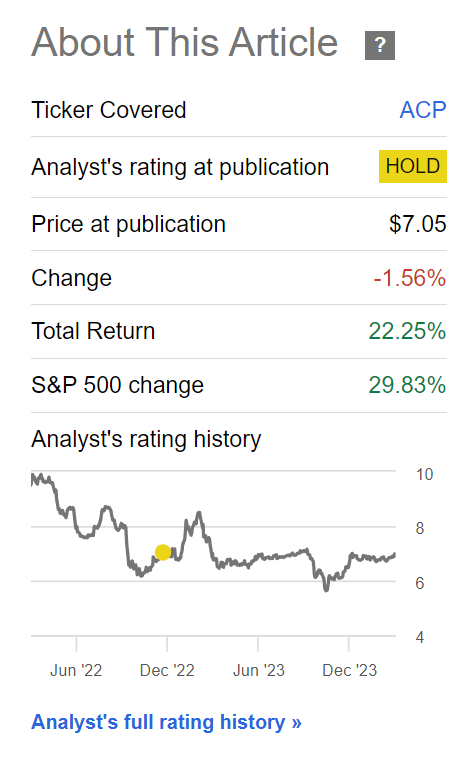

Back at the end of 2022, I reviewed the abrdn Income Credit Strategies Fund (NYSE:ACP). Although the ACP fund paid a very attractive 17%+ distribution yield, I was cautious on the strategy as I worried the fund's distribution was not sustainable given the earnings power of the asset class. However, since my article, the ACP fund has actually performed very well, delivering 22% in total returns and proving me wrong in the past year (Figure 1).

Figure 1 - ACP returned 22% since December 2022 (Seeking Alpha)

What did I get wrong and has my views changed on the ACP fund given its recent performance?

First, for those not familiar with the abrdn Income Credit Strategies Fund, the ACP fund has a broad mandate of delivering a "high level of current income with a secondary objective of capital appreciation". It achieves its mandate by primarily investing in non-investment grade senior loan and debt instruments (and related securities) in a variety of industries and geographic regions.

The ACP fund acquired the Delaware Ivy High Income Opportunities Fund (“IVH”) in March 2023, adding approximately $190 million in assets.

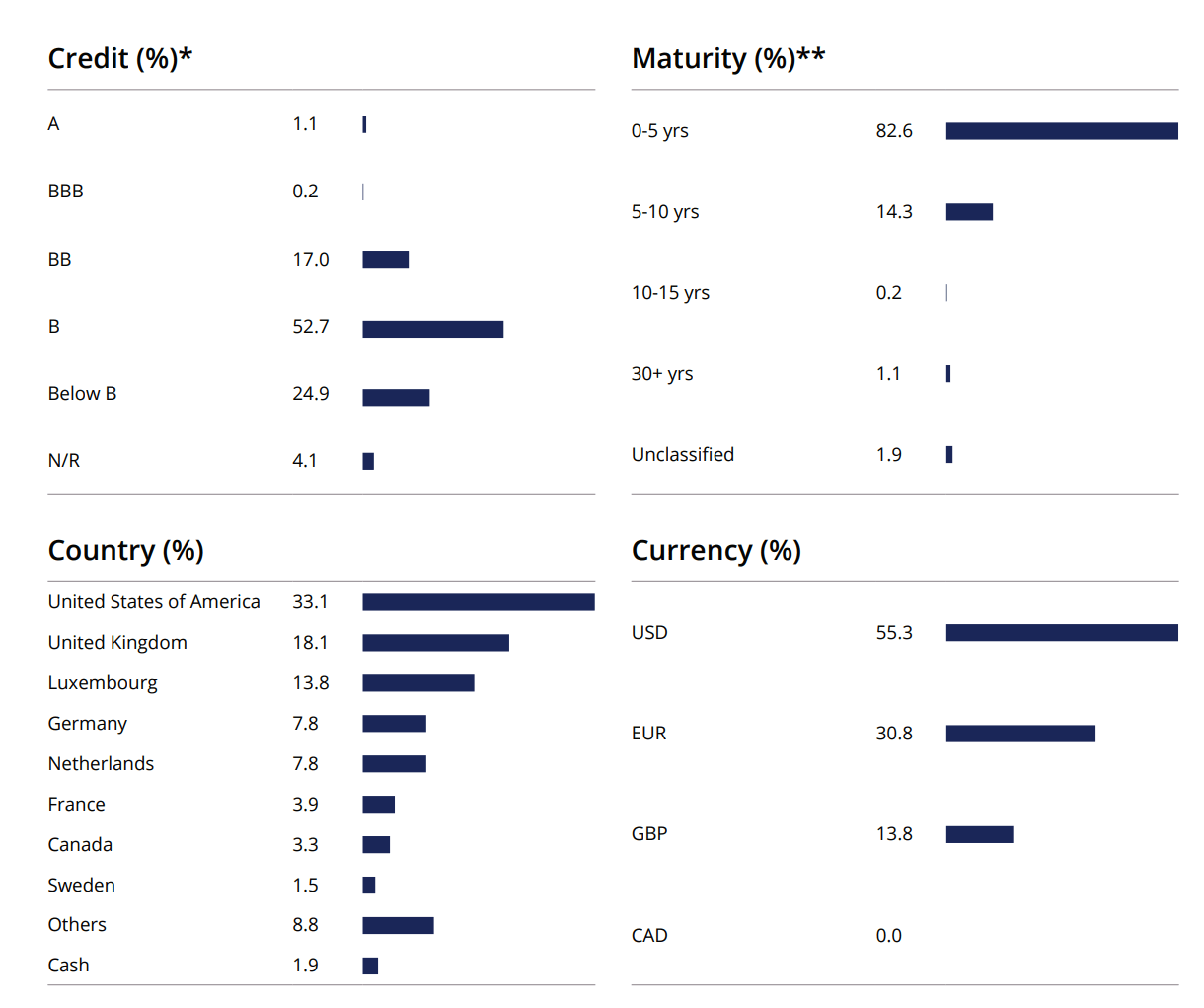

The ACP fund's portfolio is typical of many leveraged credit funds, with 98.7% of the fund's assets non-investment grade rated as of January 31, 2024 (BB or below) (Figure 2). The ACP fund is globally diversified, with only 33.1% of the fund's investments domiciled in the U.S. while 18.1% is in the U.K., 13.8% in Luxembourg, 7.8% in Germany, and 7.8% in the Netherlands.

Figure 2 - ACP portfolio allocations (ACP factsheet)

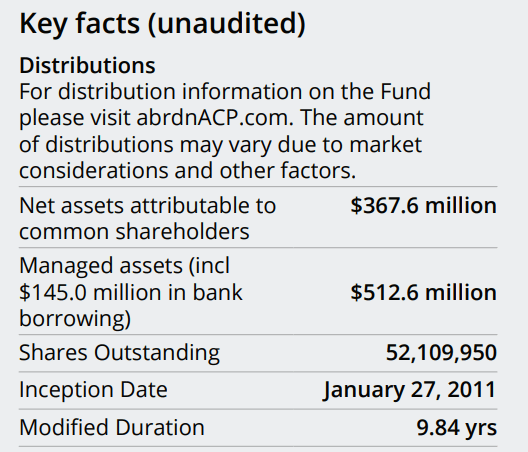

The ACP fund also has high interest rate exposure, as measured by the fund's 9.8 year modified duration (Figure 3).

Figure 3 - ACP has a 9.8 year duration (ACP factsheet)

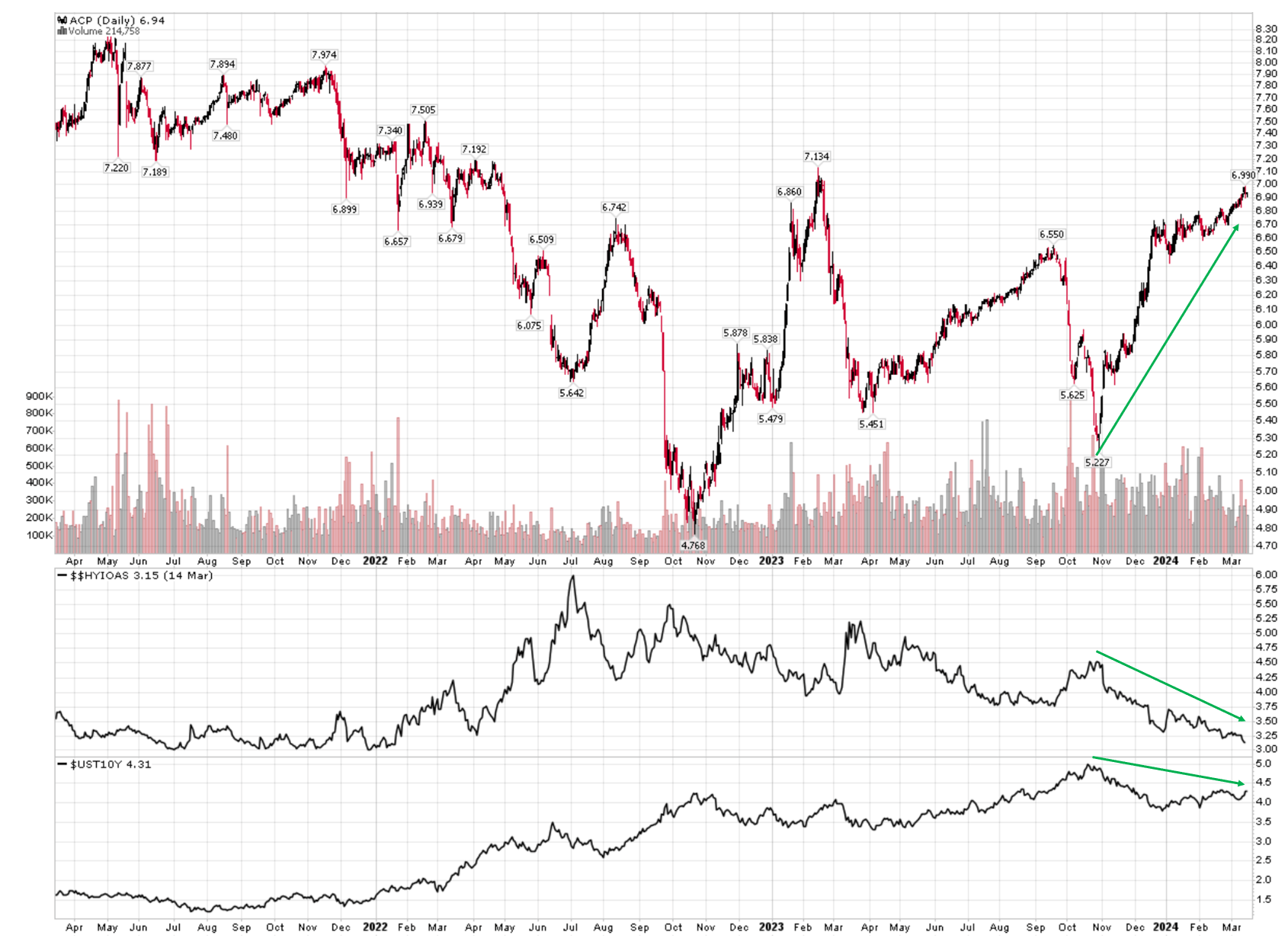

The ACP fund's strong rebound in recent months can best be explained through the lens of two important macro drivers: interest rates and credit spreads.

Since November and the Fed's dovish pivot, high yield credit spreads have tightened from 4.5% to almost 3% while 10 year treasury yields have declined from 5% to 4.3% (Figure 4).

Figure 4 - ACP vs. high yield credit spreads and 10 year treasury yields (Author created with price charts from stockcharts.com)

The combination of these two factors have sparked a 30%+ rally in total returns of ACP shares.

However, the important question for investors going forward is whether these factors will continue to be tailwinds in the coming months and quarters.

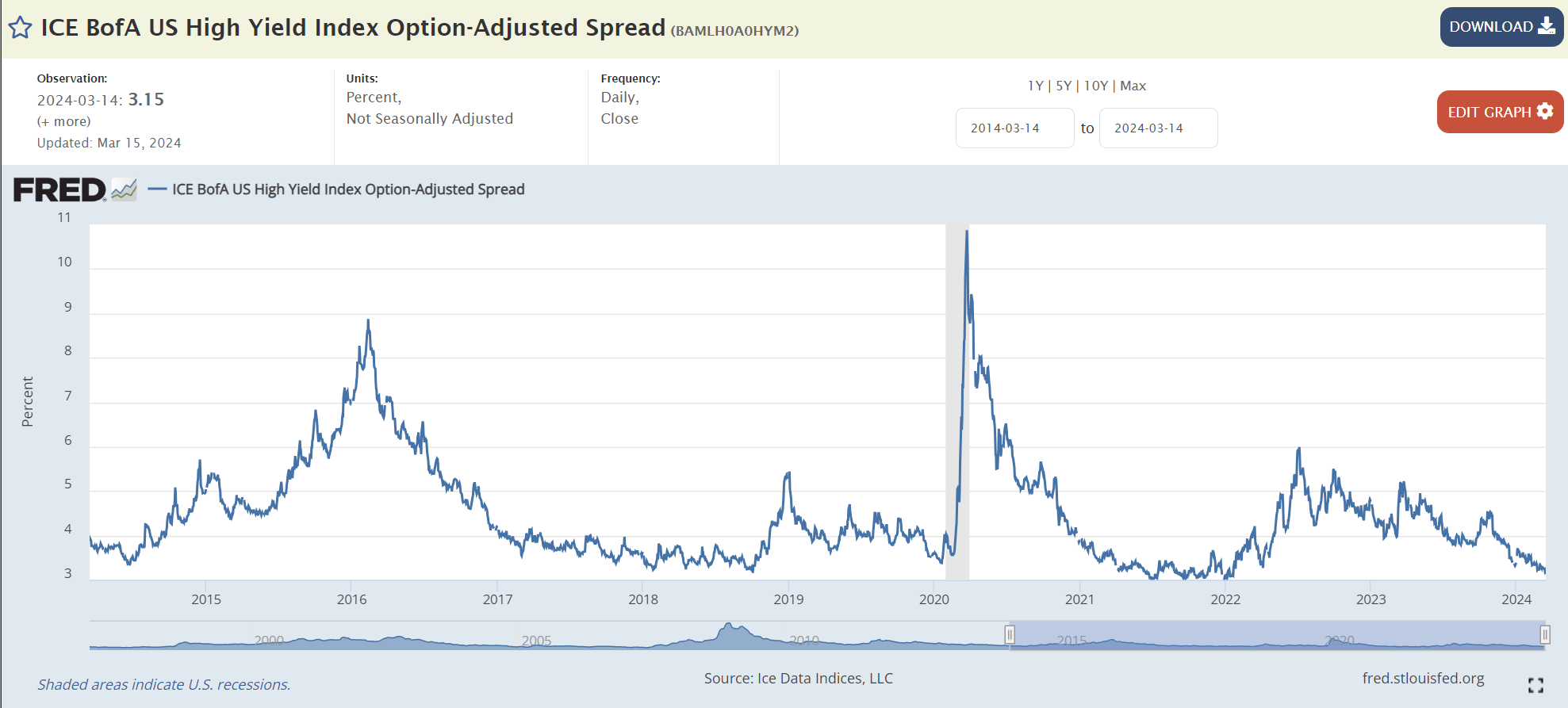

First, on the question of credit, the current high yield credit spread of 3.15% is basically as good as it gets (Figure 5).

Figure 5 - High yield credit spreads near historic lows (St. Louis Fed)

While credit can remain benign for an extended period of time, like in 2017 to 2018 when high yield spreads remained in the low 3% range for almost 2 years, future returns of the ACP fund will unlikely see the tailwind from narrowing credit spreads like we saw since November.

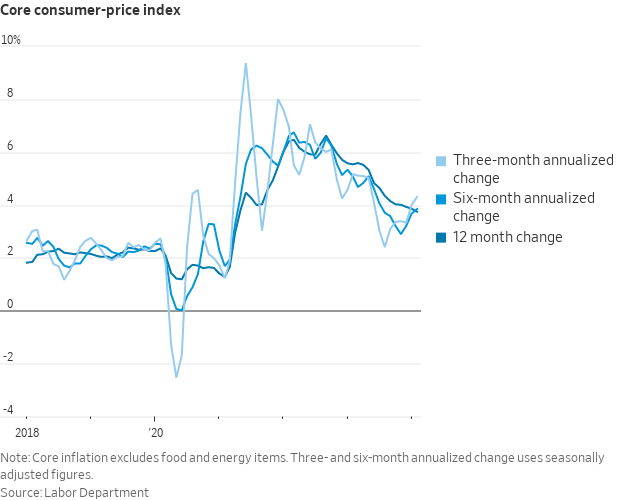

Furthermore, after a reflexive short-covering rally in October and November, long-term interest rates have also stopped declining in recent months. This is because with a booming economy, there are signs that inflation is rebounding and that the timing for Fed rate cuts may be pushed farther out (Figure 6).

Figure 6 - Inflation readings appear to be reaccelerating (WSJ via Nick Timiraos' X feed)

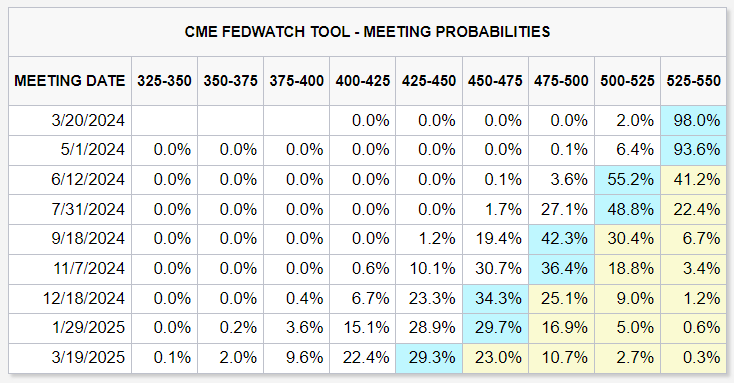

While investors were betting on 6 rate cuts starting in March at the beginning of 2024, those expectations have now moderated to just 3 rate cuts beginning in June (Figure 7).

Figure 7 - Rate cut expectations have been pushed out (CME)

Depending on upcoming inflation reports, expectations for 3 cuts may even be too optimistic.

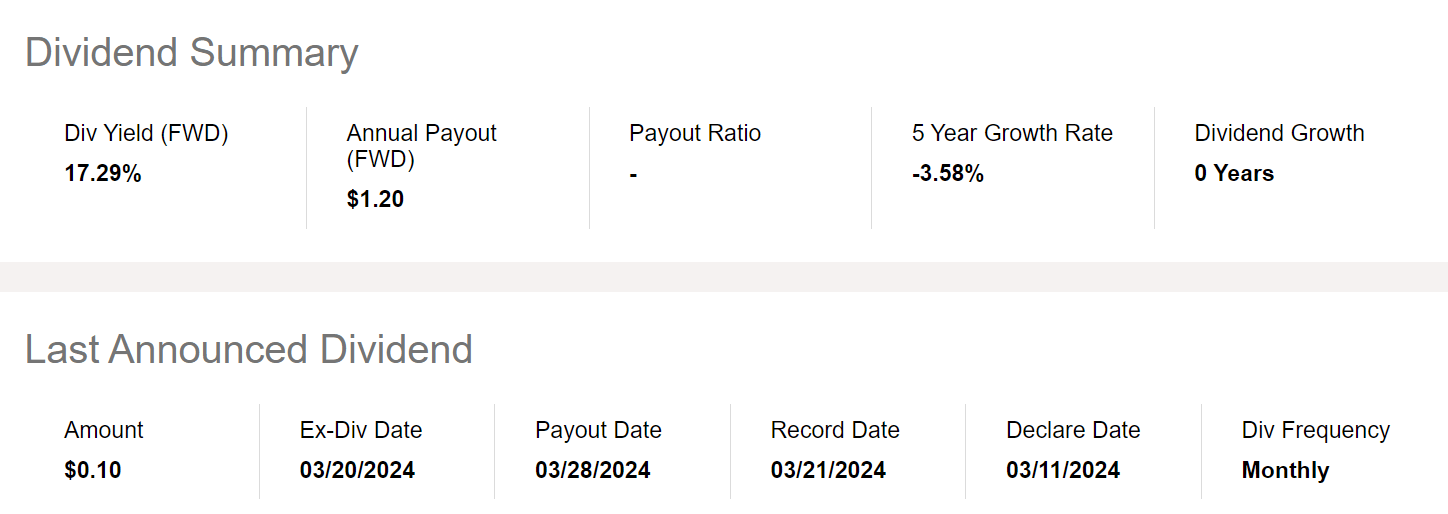

My main concern with high yielding credit funds like the ACP fund is the sustainability of its distributions. Recall, the ACP fund pays an aggressive $0.10 / month distribution which annualizes to $1.20 or a 17.3% forward yield (Figure 8). On NAV, the ACP fund is yielding 16.9%.

Figure 8 - ACP yields 17.3% (Seeking Alpha)

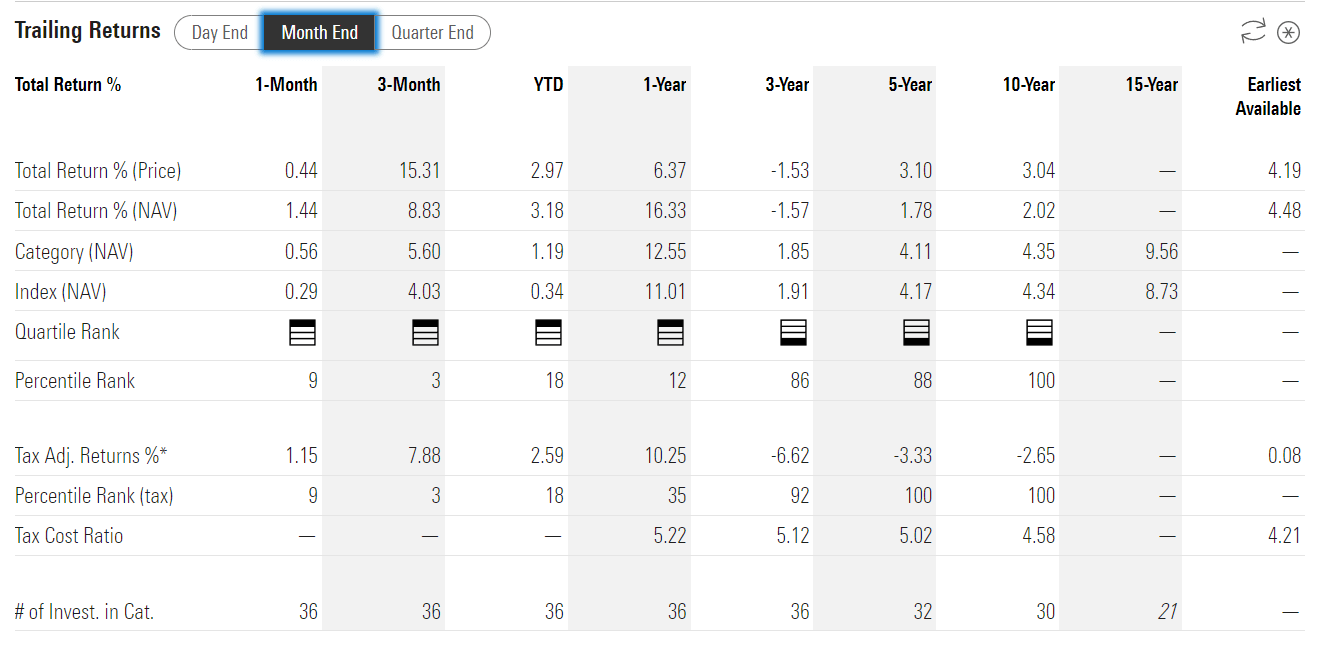

Unfortunately, over the long run, the ACP fund does not earn 17% returns on its capital. In fact, in the past 10 years, the ACP fund has only earned 2.0% p.a., and 4.5% p.a. since inception (Figure 9). This is inclusive of 2023, when the ACP fund earned 22.0%.

Figure 9 - ACP historical returns (morningstar.com)

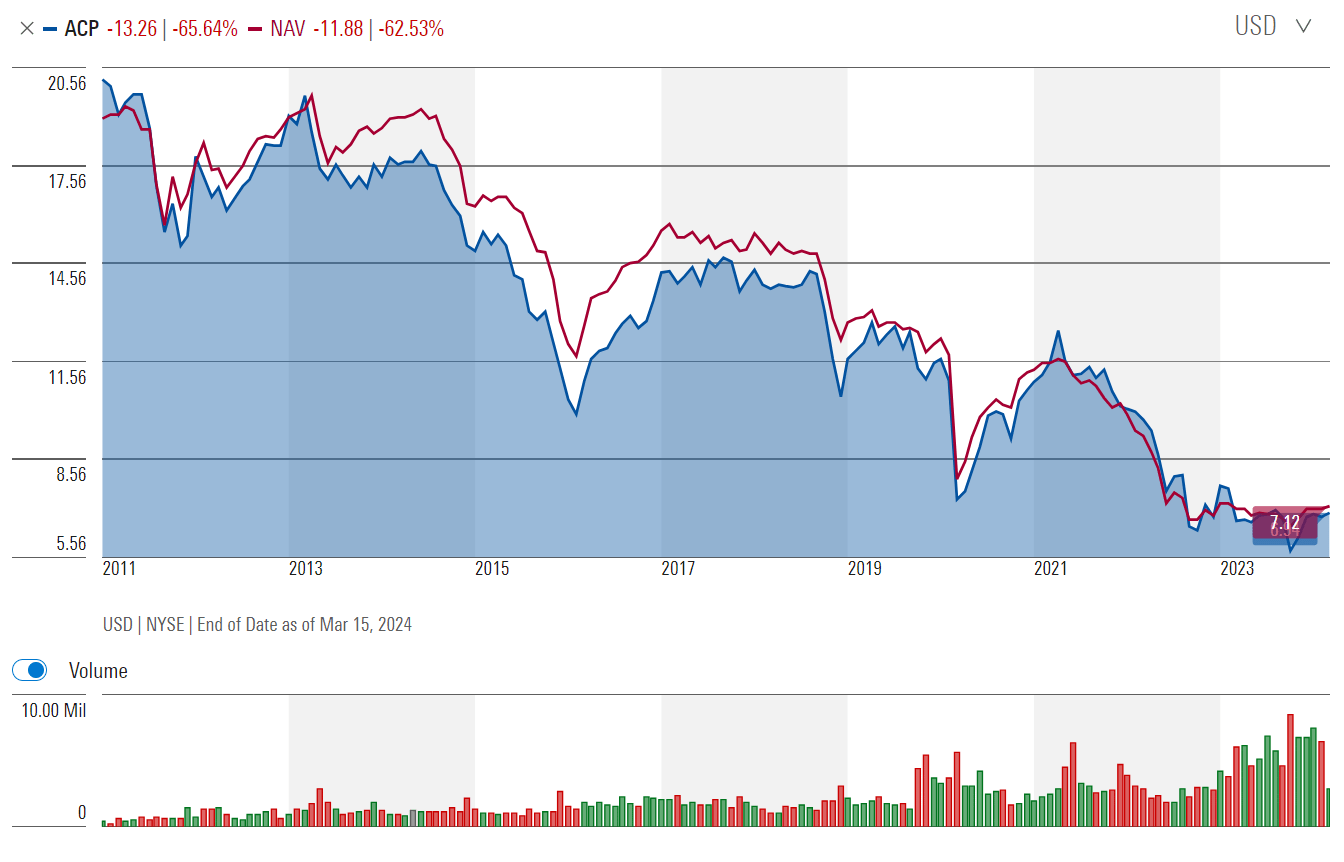

By under-earning its distribution, the ACP fund is forced to liquidate NAV in order to fund its distribution yield. Funds that do not earn their distributions are commonly called 'return of principal' funds and are characterized by amortizing NAV values over the long run, like that shown for the ACP fund (Figure 10).

Figure 10 - ACP has an amortizing NAV over the long-run (morningstar.com)

The problem for investors is that market prices tend to track NAV, so as NAV is amortized, investors see a decline in their investments.

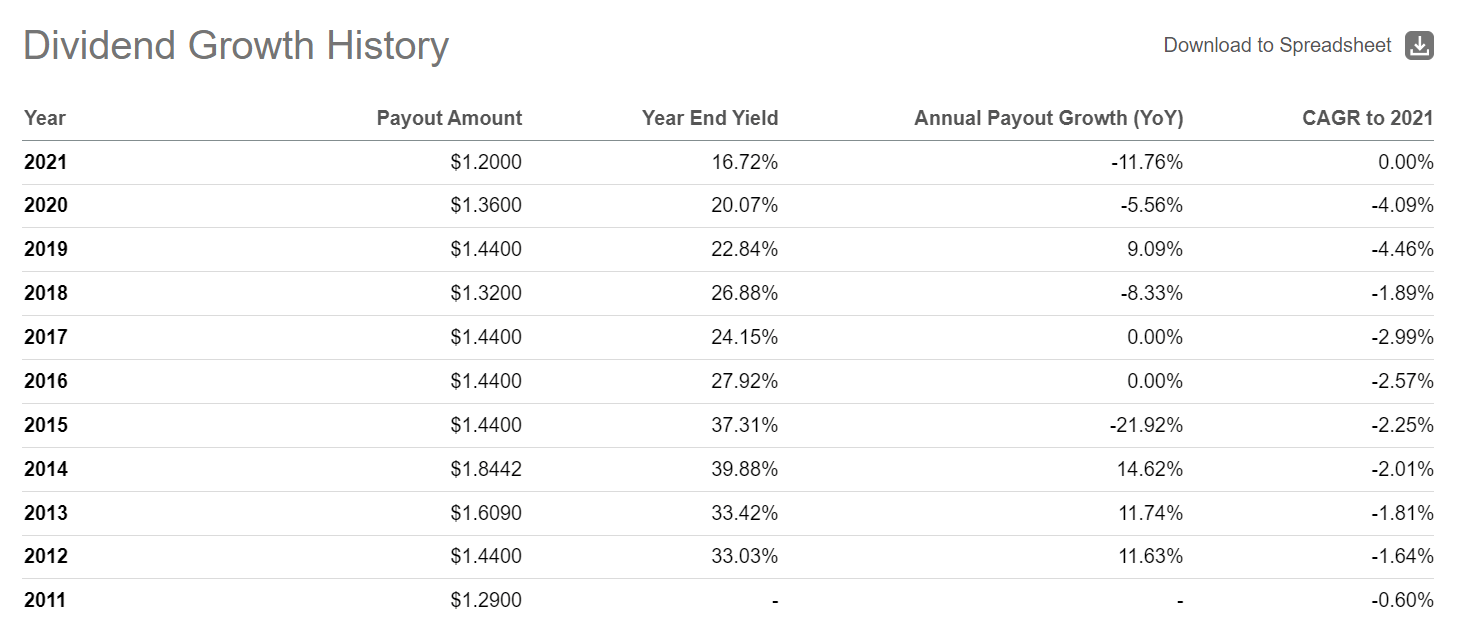

Furthermore, as NAV is amortized, there are less assets to earn income to pay future distributions. Eventually, distributions are also cut as they become unsustainable. Historically, ACP's annual distribution has declined from $1.84 in 2014 to $1.2 currently (Figure 11).

Figure 11 - ACP historical distributions (Seeking Alpha)

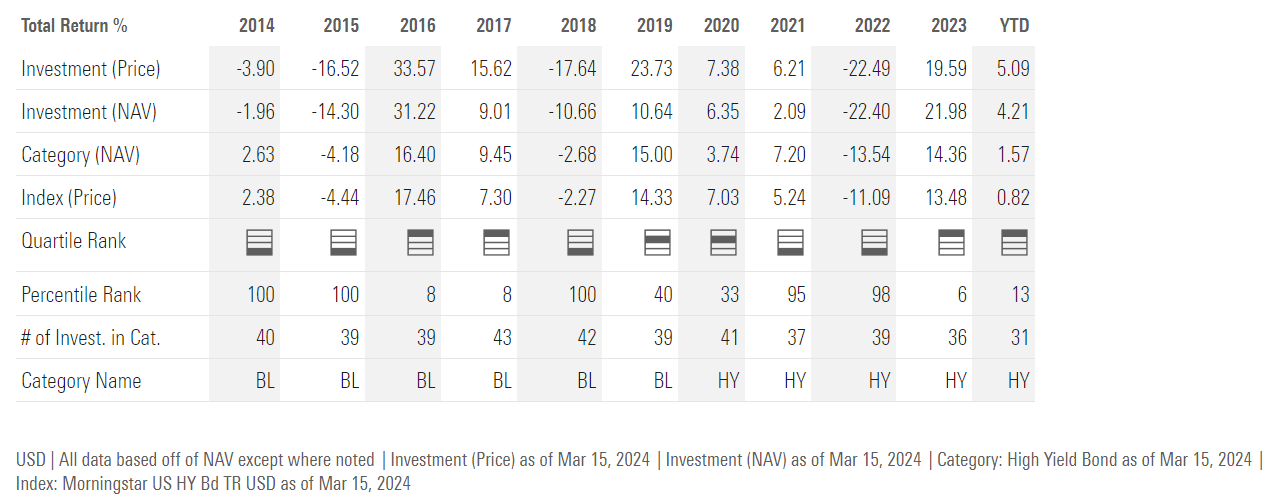

I suspect another distribution cut is in the cards for the ACP, especially if returns normalize from the extraordinary 2023 levels (Figure 12).

Figure 12 - ACP annual returns (morningstar.com)

As I have mentioned above, the past 5 months is basically as good as it gets for the ACP fund as it benefited from the dual tailwinds of tighter credit spreads and lower long-term interest rates. However, since credit is as good as it gets with high yield credit spreads in the low 3% range, I believe future returns for ACP will be significantly lower than the 22% recorded in 2023.

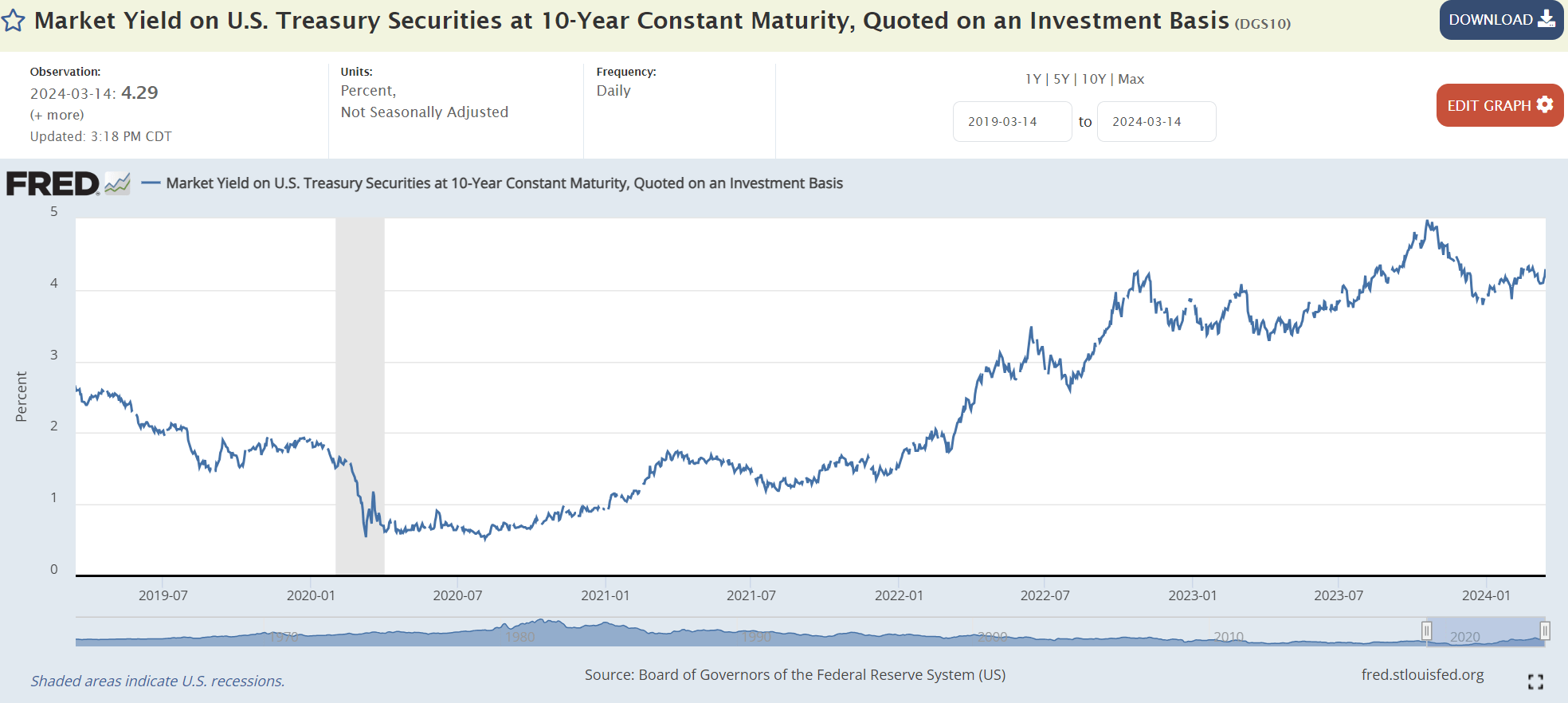

While long-term interest rates may decline further from the current 4.29% yield on 10 year treasuries, this will likely be accompanied by a slowdown in the economy and thus wider credit spreads (Figure 13).

Figure 13 - 10 year treasury yields (St. Louis Fed)

So for the ACP fund, NAV risks appear to be asymmetrically skewed towards the downside.

In summary, the ACP fund benefited from the dual tailwinds of tighter credit spreads and moderating long-term interest rates in the past few months, leading to a bonanza return in 2023. However, looking forward, risks appear skewed to the downside as credit is unlikely to repeat 2023's performance and interest rates remain stubbornly high.

While the fund's 17.3% forward yield appears attractive, I do not see how the ACP fund can earn that level of return annually based on its asset allocation. I remain cautious on the fund and recommend investors sell it here.