Scott Olson

Scott Olson

My last article about The Kroger Co. (NYSE:KR) was written in November 2023 and I rated the stock as a “Buy”. In the meantime, the stock increased almost 30% and clearly outperformed the S&P 500 (which increased 12.5% in the rather short timeframe). And the biggest part of this move came in the last two weeks, and it seems like two fundamental events drove the stock price: Kroger reported full-year results for fiscal 2023 last Thursday, March 7, 2024, and about two weeks ago the Federal Trade Commission filed a lawsuit to block Kroger’s purchase of Albertsons Companies, Inc. (ACI).

For starters, Kroger beat estimates for revenue as well as earnings per share in the fourth quarter. And while revenue was only $40 million higher than estimates (not worth mentioning), earnings per share beat by $0.21.

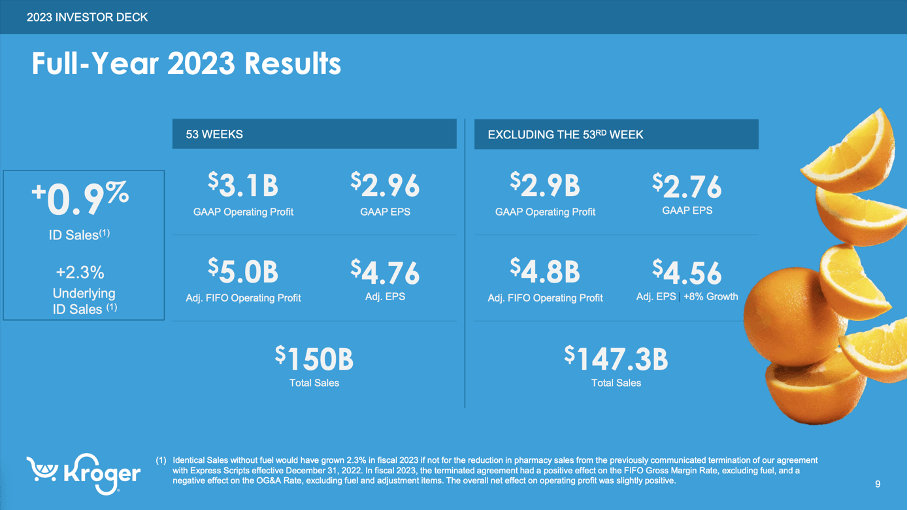

When looking at full-year results for fiscal 2023, I am actually not so impressed. Sales increased slightly from $148,258 million in fiscal 2022 to $150,039 million in fiscal 2023 – resulting in 1.2% year-over-year growth. When excluding fuel, sales increased 0.9% from $130,562 million in the previous year to $131,748 million in fiscal 2023. And while the top line still increased, operating profit declined from $4,126 million in fiscal 2022 to $3,096 million in fiscal 2023 – resulting in a decline of 25.0% YoY. And diluted earnings per share also declined 3.3% YoY from $3.06 in fiscal 2022 to $2.96 in fiscal 2023.

Kroger Q4/23 Presentation

And while EPS according to GAAP declined, adjusted earnings per share increased from $4.23 in fiscal 2022 to $4.76 in fiscal 2023 – resulting in 12.5% year-over-year growth. And finally, free cash flow doubled from $1,420 million in fiscal 2022 to $2,884 million in fiscal 2023. However, the free cash flow in fiscal 2022 was rather the outlier here.

In this case we must point out that fiscal 2023 had a 53rd week and therefore results are not completely comparable to the previous year. And when excluding the 53rd week, earnings per share would be $2.76 and adjusted earnings per share would be $4.56. Hence, about 40% of bottom-line growth are only due to an additional week.

Kroger Q4/23 Presentation

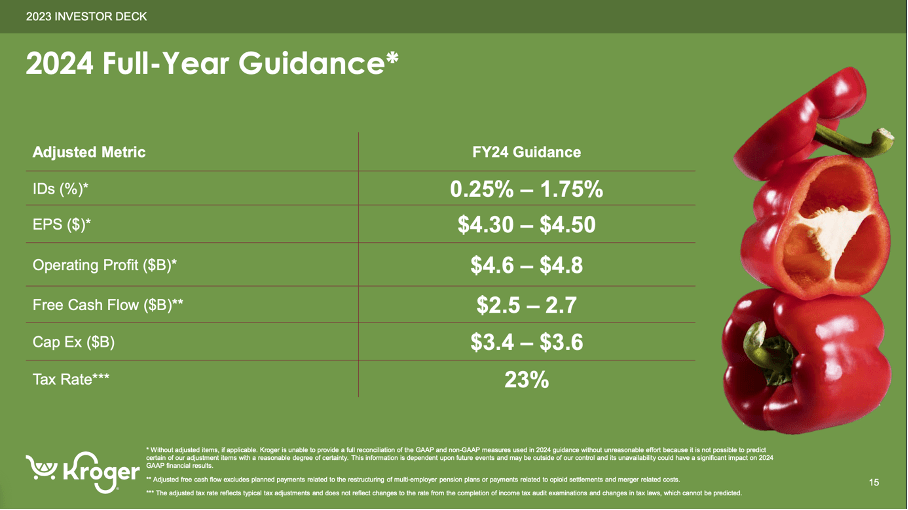

This additional week will also make it more difficult for Kroger to grow in the coming year with only 52 weeks again. Identical sales are expected to increase between 0.25% and 1.75% (without fuel). Adjusted operating profit is expected to be in a range between $4.6 billion and $4.8 billion and compared to adjusted operating profit of $5.0 billion this is a decline of 4% to 8%. Adjusted earnings per share are expected to be in a range between $4.30 and $4.50 which results in about 5% to 10% decline year-over-year.

Overall, neither the results nor the guidance is great (it is also not terrible). The stock market nevertheless received the earnings report well and the stock increased.

Aside from the reported full-year results, the intended merger between Kroger and Albertsons was the second topic generating headlines. In my last article I already pointed out that I don’t like the merger and that it is not a good strategic move for Kroger in my opinion. I wrote:

My reasoning is certainly different than FTC Chair Lina Khan’s reservations regarding the deal, but I also don’t like the merger. For starters, I am always a bit cautious when it comes to “mega mergers” as they often don’t work out as planned and are not the best use of cash. And second, the deal would also have an impact on the balance sheet – in a negative way.

And as I wrote above, my reasoning for disliking the merger is different and therefore it is not surprising that the FTC is not talking about the balance sheet and Kroger being as profitable as possible. Instead, the FTC is arguing that the merger would lead to rising prices for consumers as the two companies would have a monopoly. FTC is even arguing that executives of the two companies admitted this by themselves. Henry Liu, Director of the FTC’s Bureau of Competition said in the statement:

This supermarket mega merger comes as American consumers have seen the cost of groceries rise steadily over the past few years. Kroger’s acquisition of Albertsons would lead to additional grocery price hikes for everyday goods, further exacerbating the financial strain consumers across the country face today

Additionally, the FTC is arguing that an acquisition would lower incentives to compete on quality:

The FTC charges that the deal would eliminate head-to-head price and quality competition, which have driven both supermarkets to lower their prices and improve their product and service offerings. If the merger takes place, grocery prices will increase, and Kroger and Albertsons’ incentive to improve product quality and customer service will decrease, further harming customers.

And finally, the FTC is arguing that the merger would harm workers as today the two companies try to poach workers from each other but after the merger a combined Kroger/Albertsons would have increased leverage over workers and their unions. And as a result, the Federal Trade Commission sued to block the merger.

Kroger-Albertsons Acquisition Presentation

Kroger on the other hand is making the case for constantly lowering prices over the years and its commitment to do so in the years to come (even after the proposed merger with Albertson). In the statement, Kroger issued following the FTC decision, the company argued:

As a combined company, Kroger committed to investing $1 billion to raise wages and comprehensive benefits. This builds on the incremental $1.9 billion Kroger invested to improve wages and comprehensive benefits since 2018. To provide the best holistic support for each associate, the company will also extend continuing education and financial literacy benefits to all associates following the merger close. As union membership continues to decline nationwide, especially in the grocery industry, this merger is the best way to secure union jobs. Kroger has added more than 100,000 good-paying union jobs since 2012.

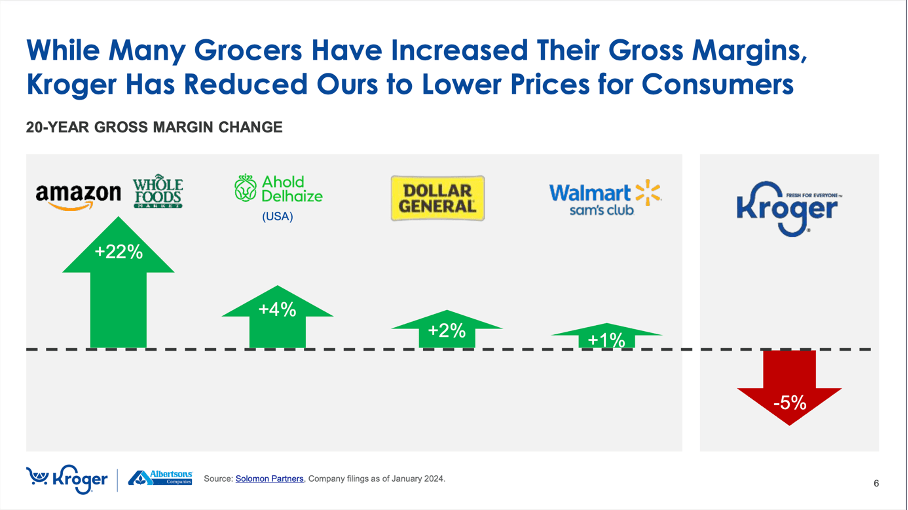

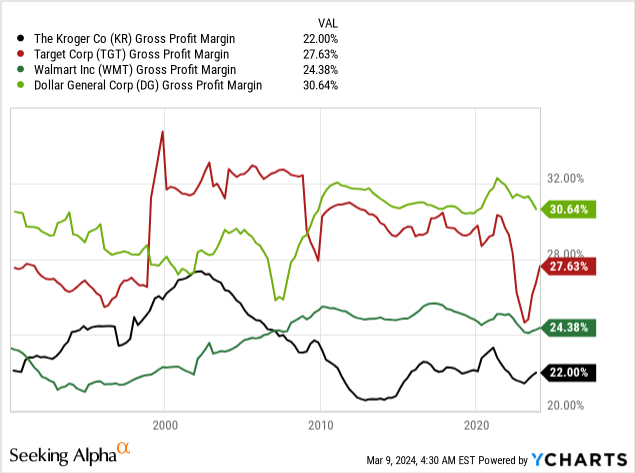

And it is interesting how Kroger is arguing with the declining gross margin in the last two decades and is making the case for keeping prices low for consumers and paying its employees well. Management is making the case that Kroger is the only company with declining gross margins while competitors saw increasing margins.

Kroger-Albertsons Acquisition Presentation

First, it is true that Kroger could raise its margins by increasing prices for customers and paying its employees less. But it is greatly simplified to look at margins just from that point of view. Lower gross margins can have many reasons and are seldom a sign of companies being generous to customers or employees. It is rather showing increased competition and missing pricing power – and that is actually not the best argument we can make from an investor’s point of view.

And the data seems carefully selected in our opinion. Not only is a 1% increase (Walmart (WMT) for example) over 20 years not really worth mentioning as this could be quarterly fluctuations. We also find other businesses with declining margins as well – Target (TGT) for example. And a rather young business like Amazon (AMZN) on its way to profitability in the last 20 years certainly is reporting increasing margins.

And it is not like I am rooting for the FTC, but I also think that it would better for Kroger not to go through with the deal – although my reasons from an investor’s standpoint might be different.

I remain rather undecided about the question if the FTC is right to fight the decision. Of course, we see a few companies dominating certain industries, which is seldom good for consumers. On the other hand, Walmart is generating twice the revenue of Kroger and Albertsons combined and Costco (COST) is playing in a similar league as Kroger. The merger will not create such a behemoth that can’t be matched by other retailers anymore.

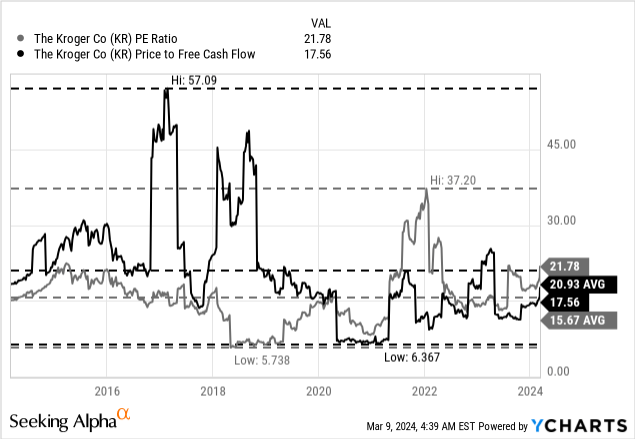

Turning back to Kroger as an investment case we also have to answer the question if the stock is undervalued or not. And I would still make the argument that Kroger is rather undervalued. We can start by looking at the P/E ratio. Kroger is trading for 22 times earnings and while that might not be called extremely cheap and is above the 10-year average of 15.67, the price-free-cash-flow ratio is 17.5 right now and below the 10-year average of 20.93. But valuation multiples around or slightly below 20 can certainly be seen as reasonable for high-quality businesses.

We can also calculate an intrinsic value by using a discount cash flow calculation. In my last article I calculated an intrinsic value of $72.32 for the stock, but now I would update my calculation a little bit. As always, we are calculating with a discount rate of 10% and use the last reported number of diluted outstanding shares – 725 million in case of Kroger. As basis for our calculation, we can use the free cash flow of the last four quarters, which was $2,884 million. And for the years to come I assume a growth rate of at least 5% annually. When calculating with these growth rates we get an intrinsic value of $79.56 for Kroger making the stock still 30% undervalued at the current stock price.

Kroger Q4/23 Presentation

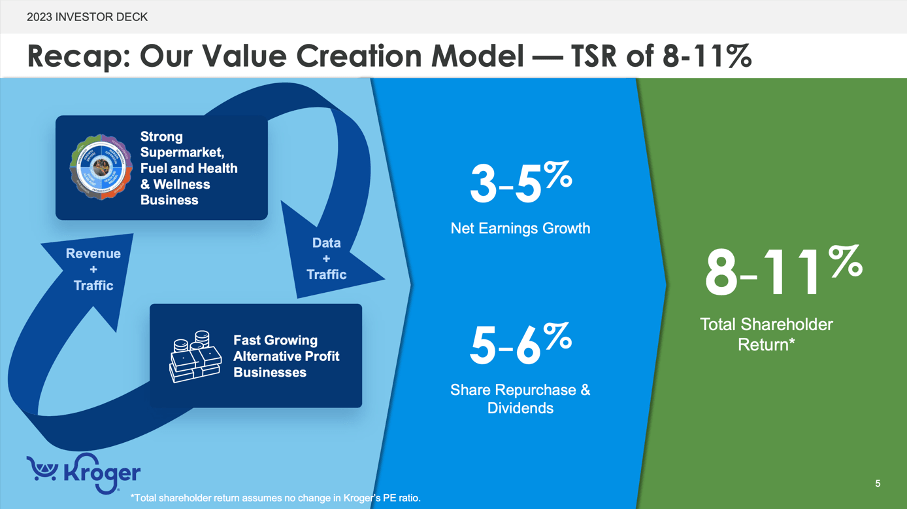

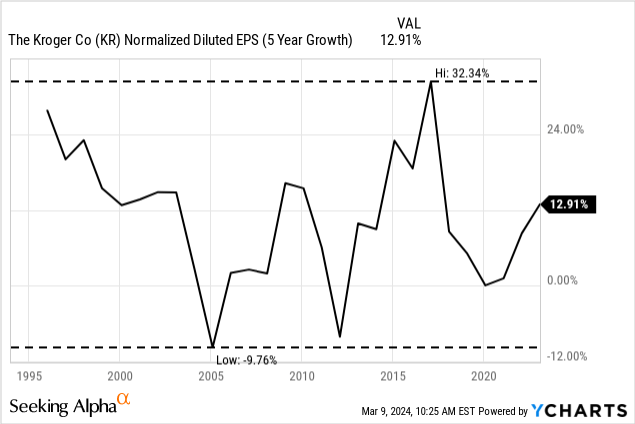

And when comparing this growth rate to Kroger’s long-term targets of 8% to 11% shareholder return it seems very cautious. But the total shareholder return is also including dividend payments, which we must subtract. In the last ten years, the average dividend yield was about 1.75% and therefore expecting a bottom-line growth between 6% and 9% seems to be management’s long-term guidance. In my opinion, 5% growth is still cautious and when looking at the growth rates in the past, Kroger was able to grow with a much higher pace.

We also should point out that analysts are way more pessimistic about Kroger (which might explain why Kroger is trading for a rather low valuation multiple). Analysts are expecting earnings per share to grow only with a CAGR of 4.59% in the next nine years. But even when calculating with this growth rate we get an intrinsic value around $73, and the stock is still undervalued.

I remain bullish on Kroger and in my opinion the stock is still undervalued. And it doesn’t matter that the guidance and last results were not so great – the stock was (and still is) undervalued, and we now see a reversion to the mean. As long as the stock is clearly trading below its intrinsic value Kroger remains a “Buy” and in my opinion it would be even better if Kroger does not acquire Albertsons, but I might be wrong here and it remains to be seen how events will unfold in the coming months and quarters.