mikkelwilliam

mikkelwilliam

Morgan Stanley published a paper suggesting that the eVTOL market could be worth $1.5 trillion by 2040 from almost zero today. Archer Aviation Inc. (NYSE:ACHR), along with five other publicly traded startups, countless private companies, and just about every large-scale Aircraft company, are chasing a piece of this market. Some of these companies will be tremendous success stories and make significant returns for early investors. I have been writing about the sector since 2021 and have published over ten articles. So far, I have been successful, making excellent money on EHang Holdings Limited (EH), buying at $5 and selling for over $20. I avoided an 80% fall in Vertical Aerospace Ltd. (EVTL), a drop in Lilium N.V. (LILM), and a 50% drop in Archer.

This will be my third article on Archer; initially, in 2022, I said sell, then in 2023, I upgraded to hold, and now I am upgrading to buy. The reason for this upgrade is the manufacturing deal with Stellantis N.V. (STLA), it gives Archer a significant and sustainable competitive advantage over its competitors.

The industry structure is becoming clear as we approach commercial operations and aircraft certification. The six startups I track are all moving towards commercial operations, but their business models and aircraft mean they will not all be direct competitors. EHang Holdings Limited (EH) has partial certification in China and has begun shipments of their two-seater autonomous aircraft for use in the tourist industry. Joby Aviation, Inc. (JOBY) will be certified next with its five-seater piloted machine. It has already delivered a plane to the US Air Force and is working quickly through the US certification process. JOBY intends to be an air taxi company and will likely begin operations in 2026. Lilium is building its first commercial aircraft, aiming to be more of a regional jet.

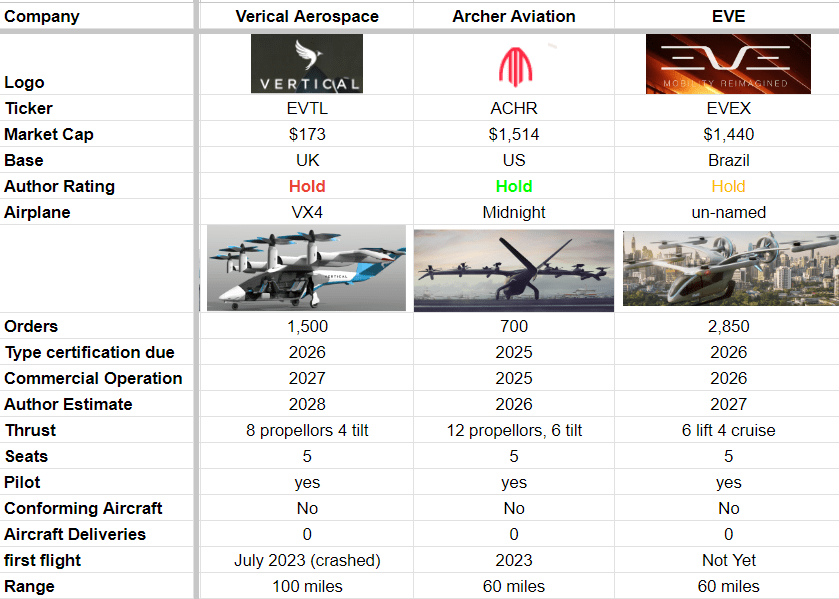

That leaves three companies pursuing the same market with similar strategies: Archer, Eve Holding, Inc. (EVEX), and Vertical Aerospace Ltd. (EVTL), which intend to be aircraft manufacturers selling machines to aircraft operators to be used as air taxis.

I will cover these in depth in the coming month and begin with Archer Aviation.

Below is a shorter version of a graphic I have used many times to highlight the three companies I see competing for this particular market. (market cap in Millions)

The Competition (Author Database)

The three companies have several similarities that separate them from the competition; the aircraft are all five-seat piloted lift and cruise machines with similar specifications. All three look likely to begin commercial operations around the same time.

As their similarities become apparent, so do their differences, and it is these differences that might allow us to choose winners, find inflection points, and identify critical success criteria.

Archer has one significant advantage and one potential threat when compared to Vertical and Eve. It will be a hybrid company that intends to sell aircraft to operators (through its Archer Direct division) and operate an aerial ride-sharing business (through Archer Air). Archer Air will compete with JOBY, and Archer Direct will compete with Vertical and Eve.

Archer is negotiating with Stellantis N.V. (STLA) to be the exclusive contract manufacturer for the Archer eVTOL machine and may well take on all of the CAPEX, costs, and problems of building the world's first volume eVTOL manufacturing plant.

If the Stellantis deal goes ahead as outlined and the company's hybrid strategy does not put off the aircraft operators, then Archer has every chance of being a dominant force in this market sector, delivering enormous returns for investors. If either of those two things does not go according to plan, then Archer will be short of cash, and its future profitability will be a concern. It will look more like a cash pit than a cash cow.

When I first covered Archer, with my sell rating in 2022, it had a share price above $4. It started 2023 below $2, but by April 2023, it had pushed over $7 and has since fallen back to $5.

I believe Archer has developed a competitive advantage since I last wrote about them. Its manufacturing plan, which may have de-risked the company and lowered the risk around any potential investment. The threat may be the hybrid sales model; the competition targets either aircraft sales or operations, and Archer stands alone in its attempts to do both.

The Initial development phase for these companies was to design and build an aircraft and get it certified to fly. All of them are approaching the end of this first phase. Archer, Vertical, and Eve are utilizing existing Aerospace companies to provide the components and subsystems for their aircraft; all three companies say this reduces the cost and complexity of certification as the suppliers are using designs and systems that have previously been certified, meaning the FAA is already familiar with them.

The second phase will be manufacturing the aircraft at scale. Manufacturing aircraft in volume is an expensive and challenging undertaking. Ehang has built its factory, and it is operational. EVE Air will be converting an Embraer factory and is currently working on the long-term financing required. JOBY is building a facility with Toyota's help and advice, but Archer has a unique plan in this area, and I think it is a winning formula.

In the Q4 2023 earnings call, the CEO laid out his plan for manufacturing. The plan is not yet confirmed, but it is the main reason for my decision to upgrade Archer to a buy.

Stellantis seems to want to be Archer's exclusive contract manufacturer, and it is Archer's aim that Stellantis take on all of the CAPEX related to the build-out of the factory and manage the volume production of aircraft. This represents a saving of hundreds of millions, possibly even billions of dollars, compared to the competition.

When Archer first announced the Georgia facility, they said it would be completed by the end of 2023 and begin producing in 2024. The 2024 shareholder letter added 12 months to both of those dates.

A press release in January 2023 may have been the spark that started the price appreciation of Archer stock. The press release says Stellantis will join forces with Archer to manufacture its aircraft, contributing expertise, capital, and personnel. Stellantis stated its goal to be Archer's exclusive contract manufacturer and said it would save Archer hundreds of millions of dollars in spending; Stellantis would provide $150 million in equity capital and purchase more shares in the open market to increase its strategic shareholding.

The agreement with Stellantis began in 2020, and they are jointly building a manufacturing site in Georgia. Archer indicated in the earnings call that they believe they will be the only company selling an FAA-approved aircraft that can be produced in high volumes in the second half of this decade. EVE would dispute this claim.

In the earnings call, the CEO said;

Our plan is for Stellantis to absorb past and future CapEx required to manufacture

CAPEX will be a big issue for these new manufacturing companies. If Stellantis takes on Archer's CAPEX, it will give them a significant advantage over their two competitors.

Archer and Stellantis are still negotiating the manufacturing contract and will release further information throughout 2024. The development of this agreement is the crucial element of my bullish views, and if it begins to falter, so will the thesis.

It was noted in the earnings call that Archer's cash position was relatively flat over the last year as the company developed its manufacturing lines and laboratory test sites and began the building of its aircraft because Stellantis invested hundreds of millions of dollars from its balance sheet. (This positive hides the 25% dilution shareholders suffered while keeping the cash position high.)

The manufacturing site will be staffed by dozens of full-time employees from Stellantis (earnings call); suppliers are building multiple production lines to supply parts and components to the Georgia site, including Honeywell International Inc. (HON), Garmin Ltd. (GRMN), and Safran SA (OTCPK:SAFRF). FACC, which manufactures carbon composite structures for aircraft OEMs, will manufacture these structures at its sites across Europe and ship them directly to Georgia; the savings from building these structures in-house are immense.

It should be pointed out that Archer spent $60 million in non-recurring expenses to allow the suppliers to build these production lines, so they were not free.

Stellantis has been buying Shares in the open market, as they indicated they would, with five purchases in 2024 for a total of $42.8 million and are now the largest shareholder with 12.4%; the other notable buyer is Ark Investments, who now own 9.29% of Archer having been a regular buyer in 2023. The company is 24% owned by the general public, and the individual insiders have 25%; institutions and public companies own the rest. Shareholders were diluted 26% in 2023, a substantial amount, and this dilution is likely to continue.

The Georgia site, run and paid for by Stellantis, accepting subsystems from world-leading aviation companies, will have a greater capacity than the competitors who have revealed capacity numbers. JOBY talks about dozens a year, Ehang dozens a quarter, and Archer dozens a week. Eve and Vertical have yet to confirm the capacity figures.

If the plan works, they will be the first volume producer with an FAA-authorized eVTOL aircraft that will represent massive value and likely lead to significant share price appreciation.

The business model is unique in this industry sector. Archer Direct is expected to deliver significant revenue while they build out Archer Air, the ride-sharing Air Taxi service.

The Archer order book of 700 planes at $3.5 billion implies an aircraft price of $5 million per plane (EVTL is at $4 million on the same calculation). United Airlines Holdings, Inc. (UAL) has already made some pre-delivery payments, and other orders seem firm. As soon as the plane is authorized, it would be reasonable to assume that Stellantis will start cranking up production at the Georgia site and generate significant revenue.

Archer expects the order book to grow during 2024 and 2025 (CFO prepared remarks).

In the earnings call, one could interpret these words from the CFO as implying they will sell directly to airlines to get the money they need to pay for the build-out of the taxi company

This hybrid approach allows us to take advantage of direct sales opportunities early on in our business to generate significant revenues while the aerial ride-sharing piece of the business builds out.

The Boeing Company (BA) and Airbus SE (OTCPK:EADSF) do not compete with airlines, and one wonders how a large Boeing customer like United would react if Boeing started running an airline on the same routes as United. Airbus would probably be the only beneficiary of such a move.

Archer has announced MOUs in India and UAE to operate air taxi services. United, Archer's largest customer, announced plans to operate a service in Chicago.

No pricing details have yet been released regarding the taxi services; however, the Chicago service will be a 10-minute journey to the airport, which would take 1 hour by car, which is likely to prove popular. The Chicago service highlights the benefit of the eVTOL market, a 1-hour car journey turning into a 10-minute zero-emission flight. It is not difficult to imagine this being a success in every densely populated city worldwide.

The way Archer's two divisions will work needs clarifying. What happens if United wants to operate in India or the UAE? Has Archer already signed exclusive deals, so that is not possible? Will they enter a price war with a big customer? Can they stop the international partners from starting such a war?

It is a strategy full of risk and potential; if they can manage it all harmoniously, they will have a second profitable business arm. However, the risk remains that EVE or Vertical could see an opportunity to take the business of United or other large airlines. The aircraft have similar specifications and prices so the sales strategy may become significant.

The balance sheet of Archer looks solid. Archer has shareholder equity (Assets-Liabilities) of $367 million and debt of $7 million. They have $465 million in cash and $114 million in short-term liabilities.

The CFO guided non-GAAP operating expenses of $80 million in Q1 2024, down from $87.5 million in Q4 2023, slightly over previous guidance. Expenditure will almost certainly pick up as Archer moves towards flight testing the aircraft currently under production and commercial operations.

I have not yet begun to build a mathematical model for Archer, but here are some key line items that show its trajectory so far:

Key financials (Author Database)

2023 free cash flow to the firm was -$416 million in 2023, the CFO quoted total available liquidity of $625 million. This implies Archer has a cash runway into early 2025.

When Archer first announced the Georgia manufacturing facility in November 2022, they suggested it would cost $118 million. In the Q4 earnings call, the CEO said, "competitors who are investing hundreds of millions of dollars in manufacturing" Stellantis agrees it will cost in the hundreds of millions to build the manufacturing facility.

In the previous linked press release, Stellantis said:

Stellantis' contribution will allow Archer to strengthen its path to commercialization by helping it avoid hundreds of millions of dollars of spending

Archer does not have the cash to cover the build-out of the Georgia manufacturing site on their own. If they do need hundreds of millions of dollars, as Stellantis suggests, they would have to raise it.

The importance of Stellantis cannot be overstated to the long-term success of Archer. Archer is expecting a lot from Stellantis (CFO's prepared remarks)

Just last year, Stellantis provided us with a $150 million forward equity purchase agreement that allowed Archer to access that capital at our discretion. This allowed us to opportunistically take advantage of a strong stock price to minimize dilution. We expect that Stellantis will continue to provide this type of liquidity support through commercialization. Given their position as a long-term strategic partner of the company, we expect them to do this on attractive terms and through attractive structures.

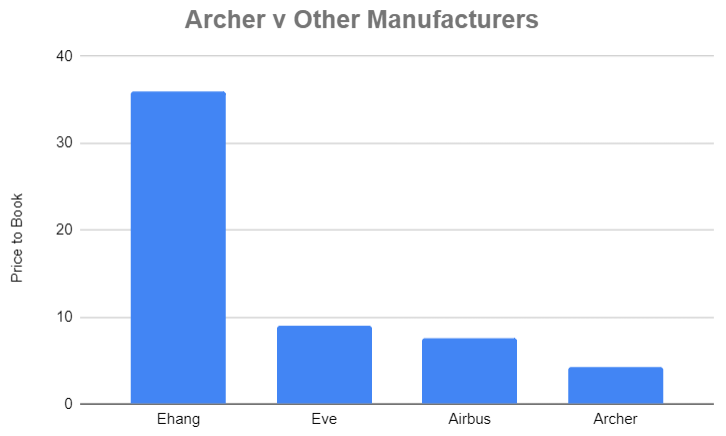

I do not yet have the information needed to provide a fair-value calculation; comparing Archer to other aircraft manufacturers provides some insight, showing that Archer has the potential for significant growth in terms of price-to-book ratio.

Price to Book (Author Database)

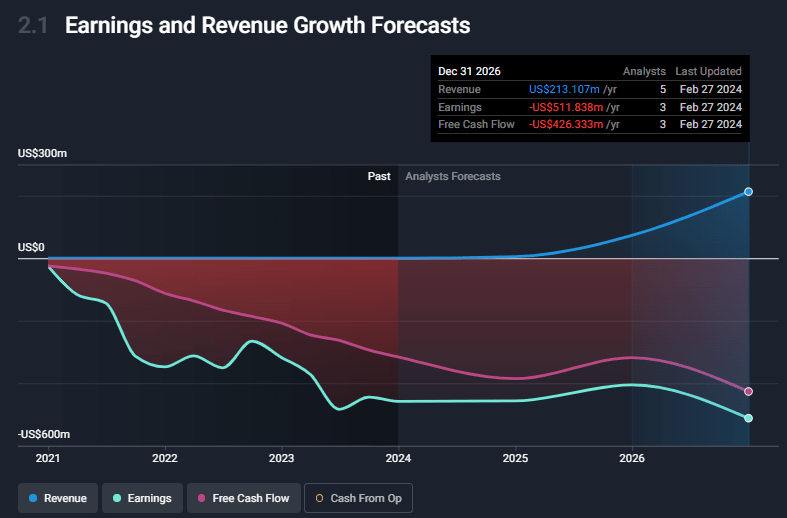

The Seeking Alpha page for Archer gives a Wall Street 1-year price target of $9.36, an increase of 88%, but the quant system scores only 2.82, rating Archer as a hold. The five analysts covering Archer forecast revenue beginning in 2025 and growing through 2026 but have earnings and cash flow falling during this period. Indeed, a negative cash flow of $400 million is forecast for 2026.

Earnings and Cash Flow (SimplyWall.st)

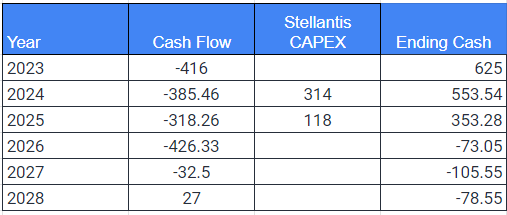

Using the figures quoted for the build-out of the Georgia site and the CAPEX already spent on manufacturing plus the guidance on spending given by the CFO in the Q4 earnings call, we can estimate the cash shortfall of Archer as it moves towards profitability.

Cash Flow and Capex (Author)

The key assumptions here are:

1. Certification comes in late 2025/2026

2. United are prepared to take the aircraft on order immediately

3. Stellantis can ramp up production at the Georgia site in 2026/2027

4. Stellantis takes on the CAPEX of $118 million for the build-out of the Georgia site and the $314 million spent by Archer in 2023.

The CAPEX figures are in the right ballpark for Stellantis, and the break-even date fits with what we know about the business.

The 2023 ending cash does include the cash still available from Stellantis under the $150 million equity agreement, effectively a capital raise and some dilution.

Under these circumstances, Archer will need to raise an additional $100 million, a lower level of dilution than seen in recent years. That figure could be significantly reduced by the existing $143 million DoD contract and future pre-delivery payments, both itemized in the recent earnings call.

The agreement with Stellantis is crucial and cannot be overstated.

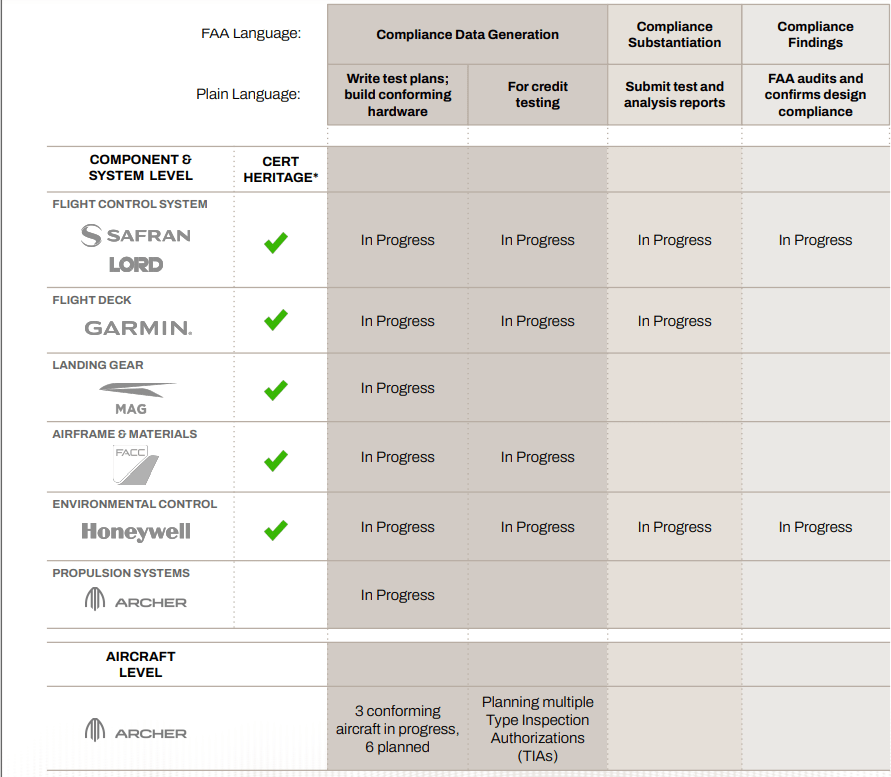

Before Archer sells or operates any aircraft, it must first get the plane certified. In the Q4 2023 earnings call and accompanying shareholder letter Archer started to give more meaningful information about the progress it is making, from P4 of the shareholder letter.

Certification Progress (Archer)

Assuming that "In Progress" does not mean "Completed." We can attempt to compare with other companies. JOBY has completed stage 3 for all systems and the aircraft and is now focused on completing stage 4. Archers and Joby's stages do not entirely line up, so a direct comparison is difficult, however, JOBY has written all of its test plans and built its conforming hardware. The plans have been submitted to and accepted by the FAA. The table from Archer suggests they are still writing plans in several areas. It is difficult to see how Archer will be able to complete all of the work it has ahead in the same timeframe as JOBY. Consequently, I do not think they will meet their deadline for commercial production in 2025, believing that the date will slip into 2026.

Archer is currently building their first conforming aircraft (three in production), which will be used for piloted testing. They completed the prototype build in 2023 and conducted initial flight tests. Eve has yet to build their prototype, and Vertical is building their second machine after the first one crashed. Archer, Eve, and Vertical seem to be at a similar stage and are behind Joby, who has already delivered a plane and conducted thousands of crewed test flights.

There are three reasons to upgrade and one big risk.

Firstly, on the certification front, The FAA now seems committed to certifying eVTOL aircraft. Archer has a team, both internally and with suppliers, experienced and capable of meeting the FAA requirements. Archer has made real progress; they have provided enough information for investors to see they are on a clear line toward certification in late 2025/ early 2026, and there is potential for acceleration of this timeline.

Secondly, they have a strong and growing order book with confirmed pre-delivery payments from United, and, in the Q4 earnings call, they announced they expect more of these payments in the coming months. The 700 orders and pre-delivery payments suggest the product will sell once certified.

Thirdly, the deal with Stellantis is the biggest reason to invest and represents the biggest risk to the thesis.

From my view, Stellantis wants to be the exclusive manufacturer of Archer aircraft and is prepared to take on the costs of building the manufacturing operations to secure this exclusive agreement. Stellantis has the balance sheet to make this commitment; as long as this holds, it removes a lot of risk.

In the Q4 earnings call the Arcer CEO said

Our plan is for Stellantis to absorb past and future CapEx required to manufacture hundreds of Midnight aircraft per year

we plan to have a turnkey relationship with Stellantis who will help us fulfill our needs for aircraft

We are maturing our contract manufacturing plans rapidly and our goal is to finalize the details later this year with Stellantis then absorbing the vast majority of the capital expenditures and working capital requirements to manufacture our aircraft at scale.

We will continue to share more details on the strategy in the coming quarters, but this puts us in an unprecedented position to commercialize this business very efficiently.

The manufacturing plan depends on the agreement with Stellantis, that deal is not yet complete and the CEO of Archer has said he will share details in the coming quarters on how the negotiations are going.

Currently, I think the prospects for the deal look very good. Stellantis is buying shares in the open market, has provided significant funding, and has signaled to its own shareholders via its press release that it intends to use its balance sheet to fund the manufacturing and said the investment would be in the hundreds of millions of dollars.

I will monitor the progress of the Stellantis deal carefully; it is the basis of my bullish call. We may get press releases from either company, and the deal is likely to be addressed in earnings calls in the prepared remarks and the Q and A sections. I hope the news is clear and direct; if I end up reading between the lines or judging the nuance of words used, my confidence in the deal will reduce.

A large capital raise might be an early warning sign that Stellantis is not taking the CAPEX onto its balance sheet.

For me any indication that Stellantis is pulling away will cause me to re-assess this investment thesis, should it happen I will either explain in the comments or write a fourth article if it causes a major change in my opinion.

I agree with the CEO of Archer that the agreement with Stellantis "puts us in an unprecedented position to commercialize this business very efficiently"

Archer has confirmed orders, a pathway to certification, and, with Stellantis, the ability to manufacture aircraft at scale. Archer has an opportunity to become a market leader in a new multi-trillion-dollar industry.

Archer's competitive advantage is its relationship with Stellantis.

If the Stellantis negotiations do not go as well as Archer hopes, they will be short on cash and manufacturing expertise.

On the certification front, significant progress has been made. Still, comparing the work done with that of JOBY implies that Archer may be overly optimistic about its timeline.

The hybrid business model offers Archer a second revenue-generating ride-sharing division, directly competing with Joby and perhaps with Archer's big airline customers.

The next 18 months will be company-defining for Archer if it can exit 2025 with a certified aircraft, an established volume production facility managed and paid for by its partner Stellantis. Archer will be the first company able to mass produce an FAA-authorized eVTOL aircraft and have a first mover advantage on a predicted multi-trillion dollar opportunity.

If Archer captures 10% of the predicted $1.5 trillion of revenue, it would have annual sales above 150 billion dollars, similar to Ford Motor Company (F), Honda Motor Co., Ltd. (HMC), and The Boeing Company (BA) today.

I would be comfortable buying Archer shares below $7 (the high for the last 12 months) while the Stellantis deal is still uncertain. If the deal goes through I would be comfortable below $15. However, if the deal falls through I would exit and re-assess.