baona

baona

In 1979, Jimmy Carter installed 32 solar panels on the presidential mansion, stating, "A generation from now, this solar heater can either be a curiosity, a museum piece, an example of a road not taken, or it can be a small part of one of the greatest and most exciting adventures ever undertaken by the American people." While his actions to disrupt the energy market seemed promising, President Reagan quickly removed the panels once he took office.

The debate over the role and potential of the clean energy sector has continued for a half-century since that time. It remains an important and controversial topic that comes up frequently. We think it is worth watching. And in the case of the ALPS Clean Energy ETF (NYSEARCA:ACES) worth us owning.

We think it is a buy for those who believe this sector will thrive in the long term, despite its recently atrocious performance. (The S&P Global Clean Energy Index has a one-year return of -26.25%).

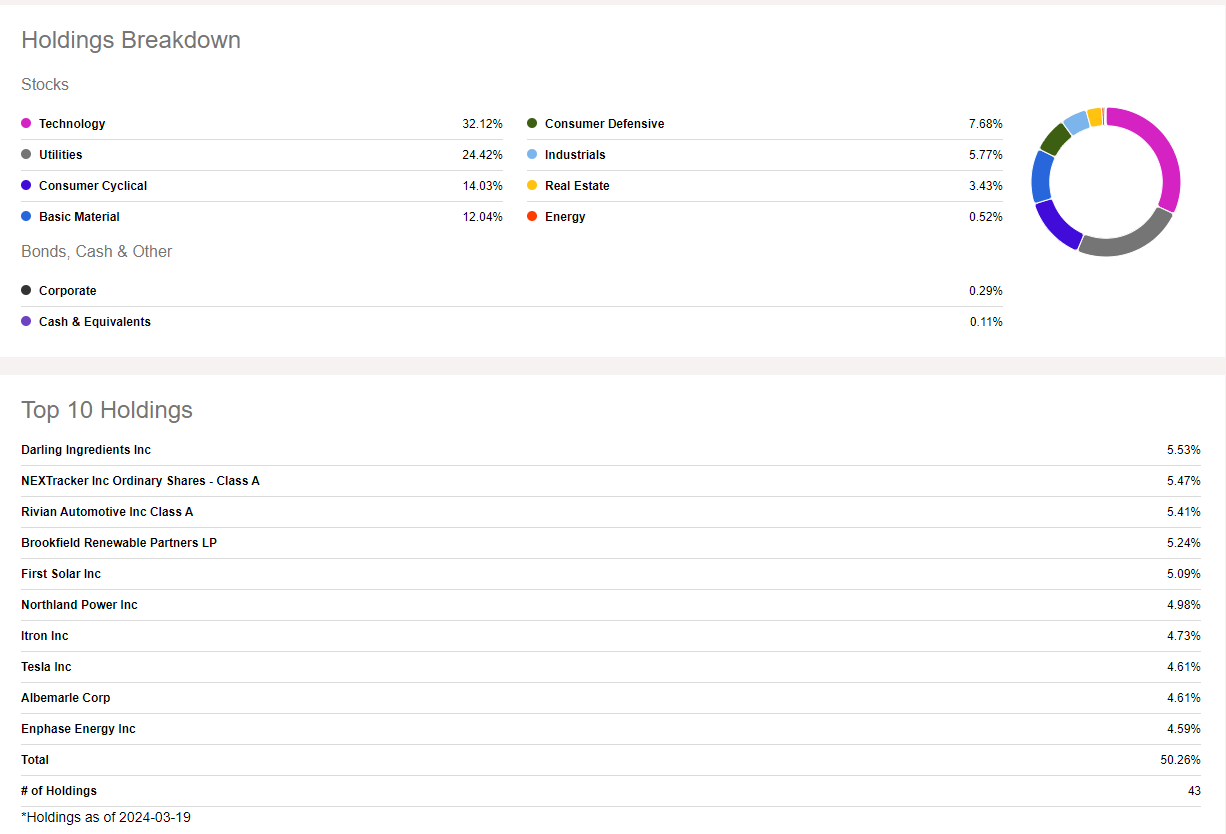

ACES tracks the performance of the CIBC Atlas Clean Energy Index. This market-cap weighted index is composed of U.S. and Canadian equities, involved in the clean energy sector, including products and services that enable the evolution of sustainable energy.

ACES is one of our favorite clean energy ETFs on the market today, because of its broad diversification. ETFs like GRID or TAN are too specific, focusing on smart grids, and solar companies. Even though 10 companies make up 51.82% of the portfolio, it is diversified across many sectors (Utilities 26.76%, Industrials 21.81%, IT 17.43%).

With 41 American and Canadian equities in the fund, ACES has been hit pretty hard the past few years, with a three year return of -27.53%. This shouldn't deter you, given two competing ETFs, TAN and PBW, have had three year returns of -24.74% and -38.01%, respectively.

Seeking Alpha

Again, this comes as no surprise given this is a capital-intensive industry and was negatively affected by the hike in interest rates. 2023 also faced its fair share of supply chain issues, only exacerbated by Russia invading Ukraine, disrupting the energy sector. This helps ACES in that they only hold equities in North America, far from that turmoil, though right on top of the political battles in the US over this industry.

Fundamentally, investors think the underlying companies in the fund are still overvalued-- with a P/E ratio of 19.96, ACES is one of the higher P/E's when compared to competitors. For comparison purposes, XLE is an energy sector ETF (including traditional and renewable energy sources) is trading at 11.38x. ICLN, a competing clean energy ETF, is trading at 16.24x.

We're bullish on clean energy because we are confident demand will increase thanks to financial/tax credits incentivizing American citizens and corporations to invest in clean energy, expanding the sector, providing more jobs, growing GDP. We also believe the younger generations coming into the workforce feel more strongly about environmental factors, lending them the nickname "the climate generation."

As a whole, clean energy can be described as energy sourced from materials that don't release air pollutants. Meaning, these sources keep our air clean. Renewable energy on the other hand, is energy sourced from materials that never run out, and can be replenished. Examples of renewable energy include solar, wind, hydropower, and biofuels, while examples of clean technology include electric vehicles, battery technology, and smart grids.

The Inflation Reduction Act was signed into law in 2022, providing tax credits to any American that make improvements to their home by investing in renewable energy. Residents can claim a tax credit of up to 30% of costs to install solar, wind, geothermal, or battery storage technology. Given that excess credits can be carried over into future years, this act is a great incentive for people to save during annual filings. According to White House statistics, in the year following the act, over 170,000 clean energy jobs have been created, while the private sector has announced over $110 billion in new clean energy manufacturing investments.

This money will expand the sector, by investing in electric vehicles, solar panels, wind technology and more. These numbers guarantee this sector will outperform in the near future, over the course of the next decade, it is more likely to be the case.

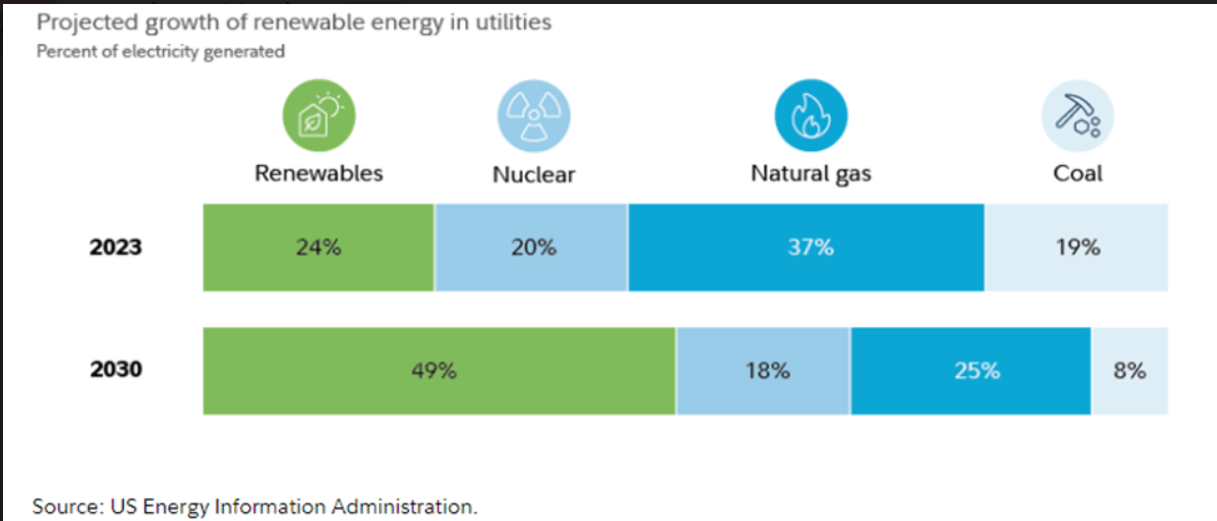

Based on the chart below, we can see that the renewable energy space is expected to more than double, while coal and natural gas are projected to fall significantly.

US Energy Information Administration

Another huge reason, if not the biggest reason, why I think this sector is projected to outperform is due to the shift in consumer sentiment. Consumers run the world; if they don't like a product a company sells, that company goes under.

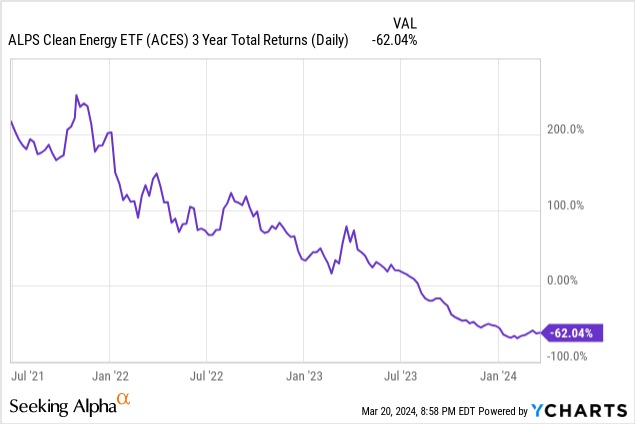

This chart below essentially shows this ETF has been dealt the stock market's version of the "death card. However, this is after a period in which about everything that could go wrong did for this industry, and as long-term investors here, we are comfortable issuing a buy rating down here, rather than potentially chasing it higher later. To us, the long-term story is likely to bring the market, and thus the price trend, along.

While opinions and arguments over this topic cover a wide range, according to a Pew Research Center's survey, people who identified climate change as a major threat soared to 71% in 2022, up from 54% in 2014. So the tug of war is leaning toward public endorsement of initiatives, and the demographic trends cited earlier are more likely to tilt it further in that same direction.

Estimates say that two-thirds of the population aged 18-24 experience climate anxiety, meaning they feel distressed over climate change, and worry what the future holds if energy sources aren't changed. This shouldn't be surprising, given those age groups are likely to be most impacted by the long-term effects of non-clean energy usage, not to mention social media which has done an immaculate job at finding information, and sharing it with the world.

As it is, renewable energy is a growing sector, and there is still so much about the environment and alternative energy sources we don't know about. Those reasons alone make this industry risky, but now add foreign countries with their own regulations to the mix? Not for us. At least for now. There is still a lot of obstacles this sector needs to overcome, such as high installation costs, resistance to change, and unknown regulatory intervention. While these are some hurdles clean energy companies have to overcome, it doesn't change our opinion that this sector will not become obsolete any time soon, nor does it convince us that demand will decline in the near future. ACES gets a long-term buy rating from us.