SolStock

SolStock

In this current environment, it may not dawn on you that some of the more attractive prospects out there could be companies that would be counterintuitive. Furniture and similar goods, for instance, are not exactly the kinds of items that are in high demand when the economy is faced with high interest rates aimed at combating high inflation. It is true that many of the companies dealing in the furniture and lifestyle retail market have experienced some pain from a fundamental perspective. But this doesn't mean that their shares have suffered. Some, because of improvements on the bottom line even in light of pain on the top line, have seen their shares driven higher.

A good example of this can be seen by looking at MillerKnoll (NASDAQ:MLKN). Back in early March of 2023, I decided to revisit the enterprise. At that time, the stock was underperforming my own expectations. But because of how cheap shares were, I maintained hope that the future would be brighter. Fortunately, that has happened to some extent. Since the publication of that article, wherein I reiterated my 'buy' rating for the stock, shares have seen upside of 19.1%. Unfortunately, that does fall short of the 23.1% rise seen by the S&P 500 over the same window of time. But considering the space we are talking about, even coming close to keeping pace with the broader market should be considered impressive.

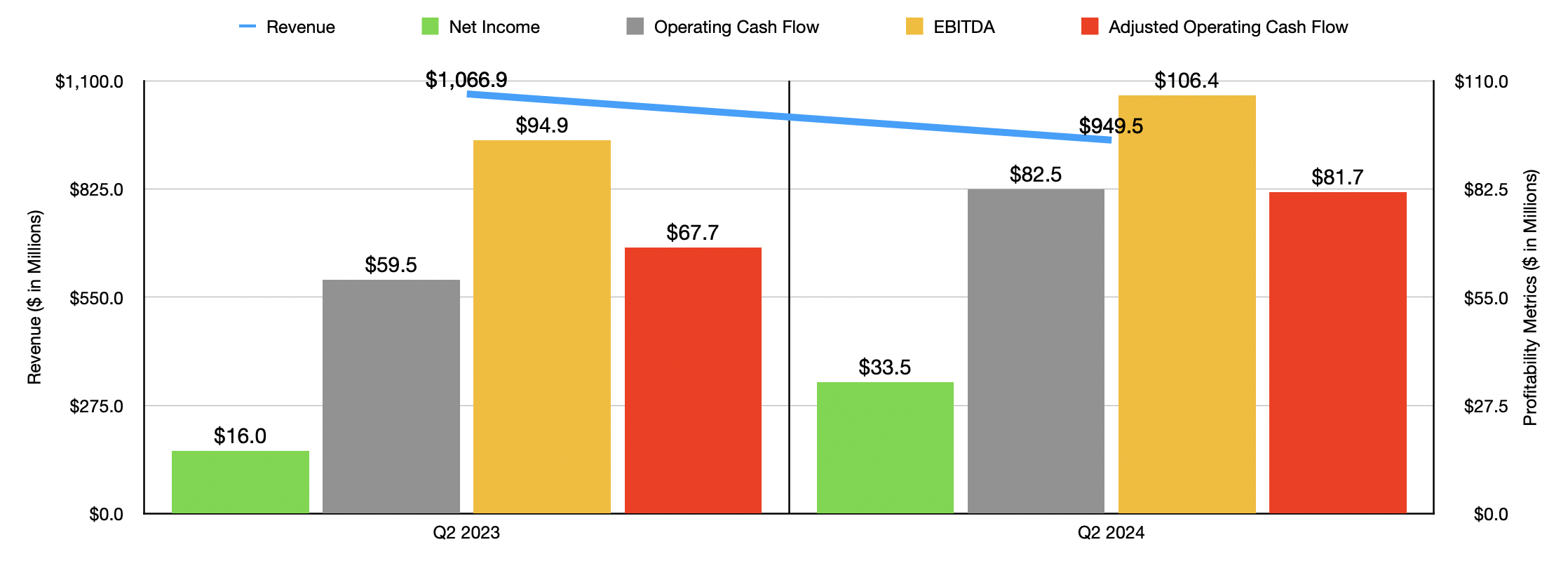

Although enough time has passed that we could dig into the 2023 financial results for MillerKnoll, I think it would be best to focus our efforts on more recent data. Late last year, the management team at MillerKnoll announced financial results covering the second quarter of the 2024 fiscal year. The data that has come out during this window of time has been truly fascinating. During that quarter, revenue for the business was $949.5 million. That's down 11% compared to the $1.07 billion generated one year earlier. That drop, according to management, was driven largely by a 10.1% decline in organic revenue. The rest of the drop, meanwhile, can be chalked up to foreign currency fluctuations.

Author - SEC EDGAR Data

Management attributed the organic revenue decline mostly to general economic uncertainty. They listed items such as geopolitical concerns, high inflation, and high interest rates, as the primary factors behind this. All three of the company's segments suffered during this time. But the one that saw the most downside was the Global Retail segment, with revenue plummeting 14.7% year over year. Orders were down 8.4% compared to the same window of time one year earlier. I don't consider this weakness to be all that surprising. According to the Federal Reserve, furniture and home furnishings retail revenue has been rather weak as of late. For January of this year, for instance, it was 9.8% lower than what it was in January of 2023. This is even worse than the 7.3% drop seen for the industry from the final quarter of 2022 to the final quarter of 2023.

The furniture retail space is not exactly known for its attractive margins. Even when times are good, bottom line improvement can be difficult. This is because the firms in question focus on such commoditized products. Fortunately for investors, MillerKnoll did not see its bottom line results worsen. In fact, across the board, they improved year over year. Net profits shot up from $16 million in the second quarter of the 2023 fiscal year to $33.5 million the same time of the 2024 fiscal year. Management chalked a lot of this up to cost synergies as the firm continues to reinvent its operations. In fact, since completing its acquisition of Knoll to become the MillerKnoll we know today, the firm has achieved an estimated $147 million in annualized run rate synergies. By July of this year, that number is expected to climb further to around $160 million. Of course, this is not the only place on the company's financial statements that should be paid attention to. Other profitability metrics for the company also fared well during this window of time. Operating cash flow shot up from $59.5 million to $82.5 million. If we adjust for changes in working capital, the rise was from $67.7 million to $81.7 million. And finally, EBITDA for the company rose from $94.9 million to $106.4 million.

Author - SEC EDGAR Data

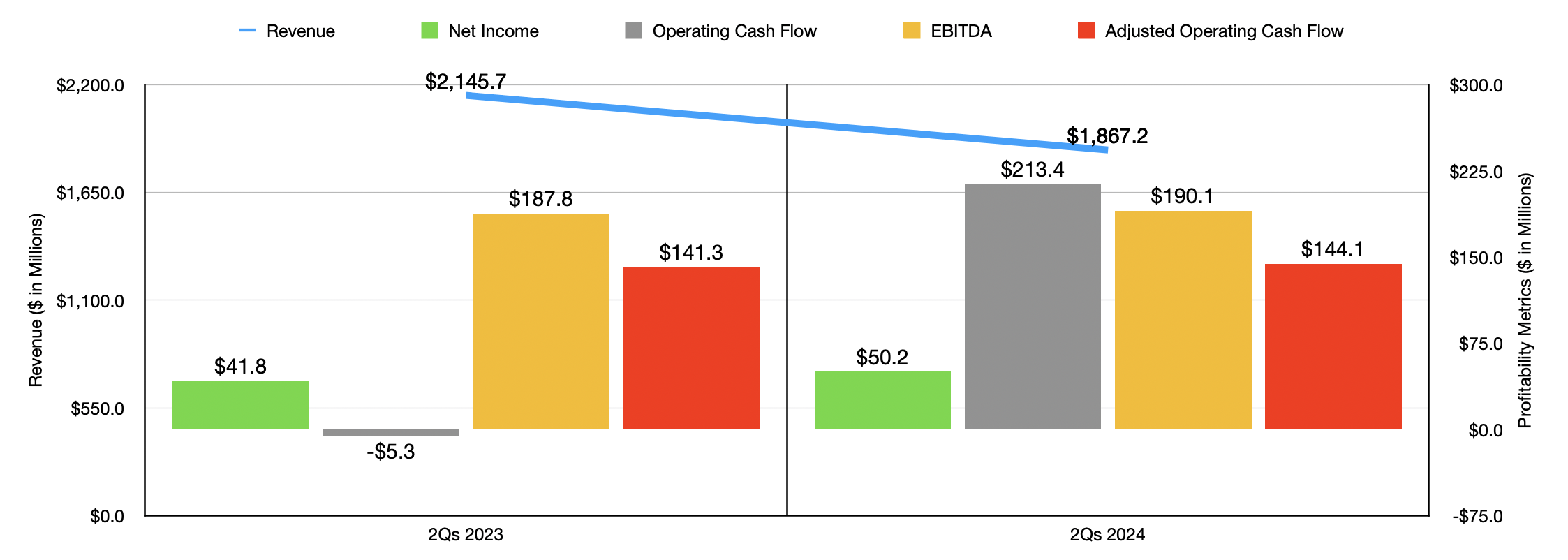

For the first half of the 2024 fiscal year, results look similarly disappointing from a revenue perspective, with sales down 13% year-over-year due to the same aforementioned factors. The bottom line, however, is looking solid just like with the second quarter on its own. Profits are up, having risen from $41.8 million to $50.2 million. And cash flows are all up year-over-year. This shows that the second quarter is part of a trend of improvement, which investors should take joy and comfort it.

For the 2024 fiscal year as a whole, the only guidance management gave involved earnings per share. They anticipate this coming in at between $2 and $2.16. At the midpoint, that would translate to net profits of $154.4 million. That's well above the $42.1 million in profits generated for the 2023 fiscal year. Management has not, much to my chagrin, provided estimates for the other profitability metrics. However, if we annualize the results seen so far, we would anticipate adjusted operating cash flow of around $258.5 million and EBITDA of $479.6 million.

Author - SEC EDGAR Data

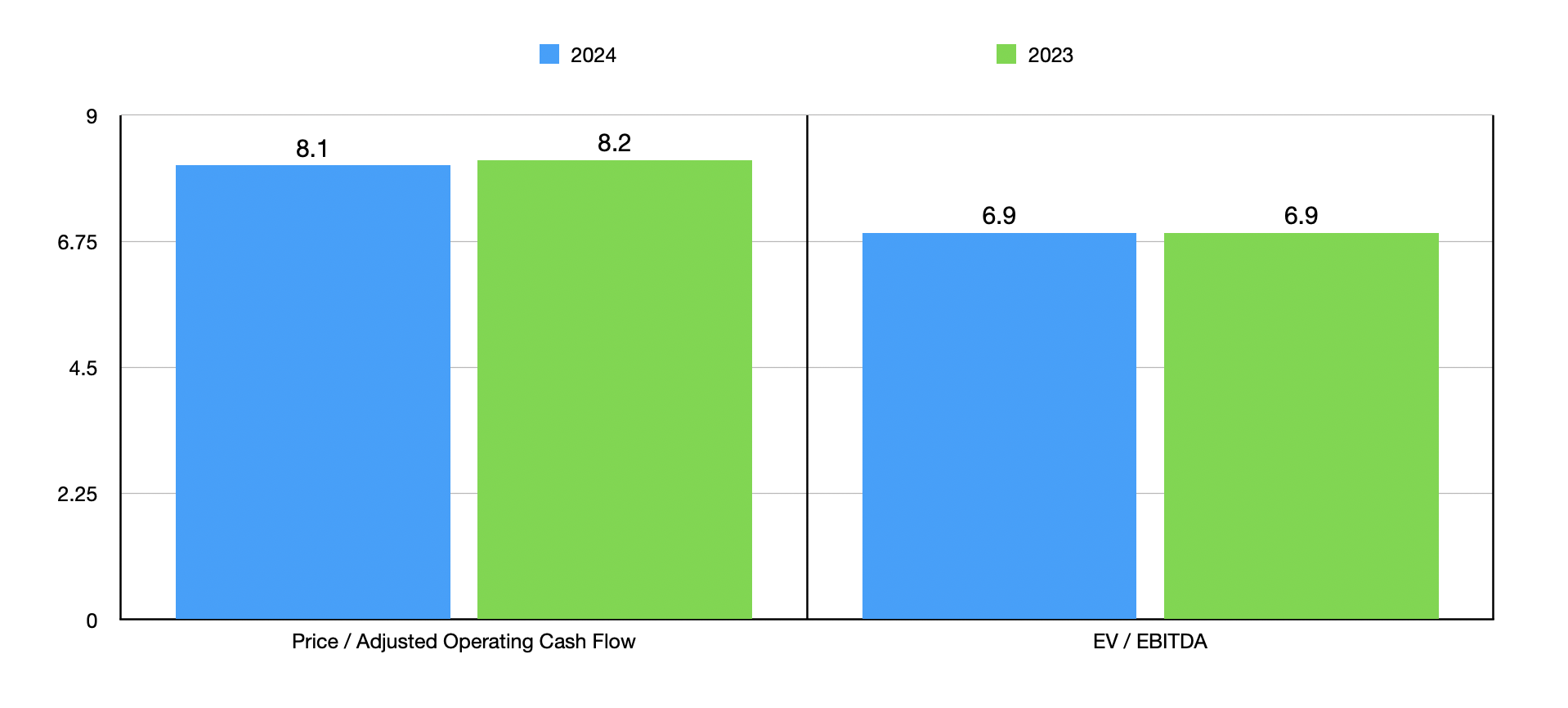

Thanks to these figures, as well as the results the company achieved for the 2023 fiscal year, I was able to value the firm as shown in the chart above. Because of the volatility from an earnings perspective, I focused instead on cash flow figures. On a price to operating cash flow basis, for instance, the stock does look a bit cheaper using results from 2024 compared to 2023. The same holds true when using the EV to EBITDA approach. Seeing multiples that are in the mid to high single digits is almost always a positive. Of course, we should also look at how the firm stacks up against other players. I did this using both of the profitability metrics in the table below. In this case, four of the five enterprises ended up being cheaper than MillerKnoll on a price to operating cash flow basis. But this number plummets to one of the five when using the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| MillerKnoll | 8.1 | 6.9 |

| HNI Corporation (HNI) | 8.9 | 14.5 |

| Steelcase (SCS) | 4.3 | 7.5 |

| Interface (TILE) | 5.3 | 12.1 |

| Pitney Bowes (PBI) | 5.1 | 16.5 |

| ACCO Brands (ACCO) | 3.9 | 6.7 |

Purely from a revenue perspective, times have definitely been difficult for MillerKnoll. The company, as well as the industry as a whole, seems to be suffering because of economic conditions. After all, when times get tough, it's pretty easy to kick the can down the road on a new couch. Even in spite of this, shares have seen some nice upside as the market has come to realize that the stock was undervalued. In the long run, I would argue that some additional upside is probably warranted. But with mixed results likely moving forward, it's only enough to warrant a soft 'buy' rating at this time.